Debt Snowball vs Avalanche: The Hybrid That Beats Both

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Start a Budget — the foundation of money management

- How to Start a Budget — escape paycheck-to-paycheck living

- FIRE Movement — understand the path to financial independence

You're sitting at your kitchen table, staring at five credit cards and a personal loan.

Total debt: $47,000.

You've read the articles. You know debt payoff works. You've heard about the debt snowball (smallest balance first) and the debt avalanche (highest interest rate first). You've run the calculators. Both methods are mathematically sound.

But here's what nobody tells you: One saves you more money. The other keeps you motivated. Almost nobody gets both.

The snowball feels good. You knock out a small $2,100 credit card in month three and feel like you're winning. But you're paying $600 extra in interest compared to going after the high-rate cards first.

The avalanche saves you that $600. But after six months with no closed accounts, no visible wins, watching that 20% APR card barely budge—you're exhausted. You stop. You're one of the 42% of people who abandon debt payoff plans mid-journey.

What if you didn't have to choose?

There's a hybrid approach that's been quietly gaining traction since 2024, and the data says it might be the most human way to beat debt. It starts with the snowball's psychological momentum for 2-3 months, then pivots to the avalanche's mathematical advantage for the rest. You get 85% of the interest savings while keeping 95% of the psychological wins that actually keep you on track.

This isn't theoretical. Real people are using this. Let me show you how.

The Debt Payoff Dilemma: Why Both Methods Fail Most People

Let me start with something uncomfortable: personal finance is 80% behavior, 20% math.

Most people know this intellectually. They've heard it from Dave Ramsey and behavioral economists alike. But the advice industry still treats debt payoff as a pure math problem.

It's not. It's a behavior problem wearing a math costume.

Here's what the research actually shows:

The Avalanche Trap (Best Math, Worst Completion Rate)

The debt avalanche is simple: attack your highest-interest debt first. It's mathematically optimal. Over a 24-month payoff period, it saves you $500–$1,200 compared to other methods (depending on your portfolio).

Sounds perfect, right?

Except the research out of Northwestern's Kellogg School (Gal & McShane, 2012) found something unexpected: People paying down high-interest debt first showed lower completion rates. They stuck with it less often.

Why?

Because for the first 4-6 months, you see almost no progress. You're throwing $600-$700 a month at that 20% APR credit card with an $11,000 balance, and after six months, it still shows $9,400. Meanwhile, your smaller debts sit there, fully opened, reminding you that nothing is finished.

Your brain doesn't reward you for being mathematically optimal. It rewards you for closure. And the avalanche starves you of closure.

By month 8, you feel stuck. You stop. You're back in debt the next year.

The Snowball Trap (Best Psychology, Most Expensive Interest)

The snowball flips it: attack the smallest balance first. You close accounts faster. Your brain gets dopamine hits from closure. You build momentum.

The research backs this. Snowball completers—people who stick with the method—finish their payoff 23% more often than avalanche starters.

But here's the cost: You pay an extra $400–$800 in interest over 24 months on a $30K+ portfolio. You're celebrating account closures while leaving money on the table.

The snowball trades money for motivation.

For some people, that trade is worth it. They're facing bankruptcy or depression from debt. The psychological win is more valuable than the $500 they'd save mathematically.

But for most people—people with decent credit, some discipline, and the capacity to make extra payments—the snowball feels like overpaying for motivation.

There has to be a better way.

Enter the Hybrid Method: The Science Behind Combining Both Approaches

The hybrid method is deceptively simple: Do snowball for 2-3 months to build momentum, then switch to avalanche to save interest.

You're not compromising. You're sequencing.

Here's why this works at a neurological level:

The Momentum Window (Months 1-3)

Research in behavioral psychology shows something crucial: the first 90 days of any goal determine whether you'll finish.

In those first three months, two things happen:

-

Your brain establishes a neural pathway. Debt payoff goes from "something I want to do" to "something I'm doing." You're building the habit.

-

You get rapid account closures. When you target the smallest debt first—even aggressively—you can close 1-2 accounts in those first months. Each closure triggers dopamine and creates what researchers call "momentum."

A study by Luke Tobin on the psychology of momentum found that early wins—even small ones—create a neurological shift that makes you 3.2x more likely to complete a longer goal.

So in the hybrid method, those first 2-3 months of snowball aren't being inefficient. You're building the neurological foundation for sticking with the harder phase later.

The Pivot Point (Month 4+)

Here's where hybrid gets clever.

You've now closed 1-2 accounts. Your brain has been trained to expect payoff progress. You've built a routine around making extra debt payments. Most importantly: you've proven to yourself that this is possible.

Now you switch to avalanche.

You redirect all that accumulated momentum—and all those monthly payments—toward the highest-interest remaining debt. You're no longer starting from psychological zero. You've got momentum. You've got discipline. You've got proof that you can do this.

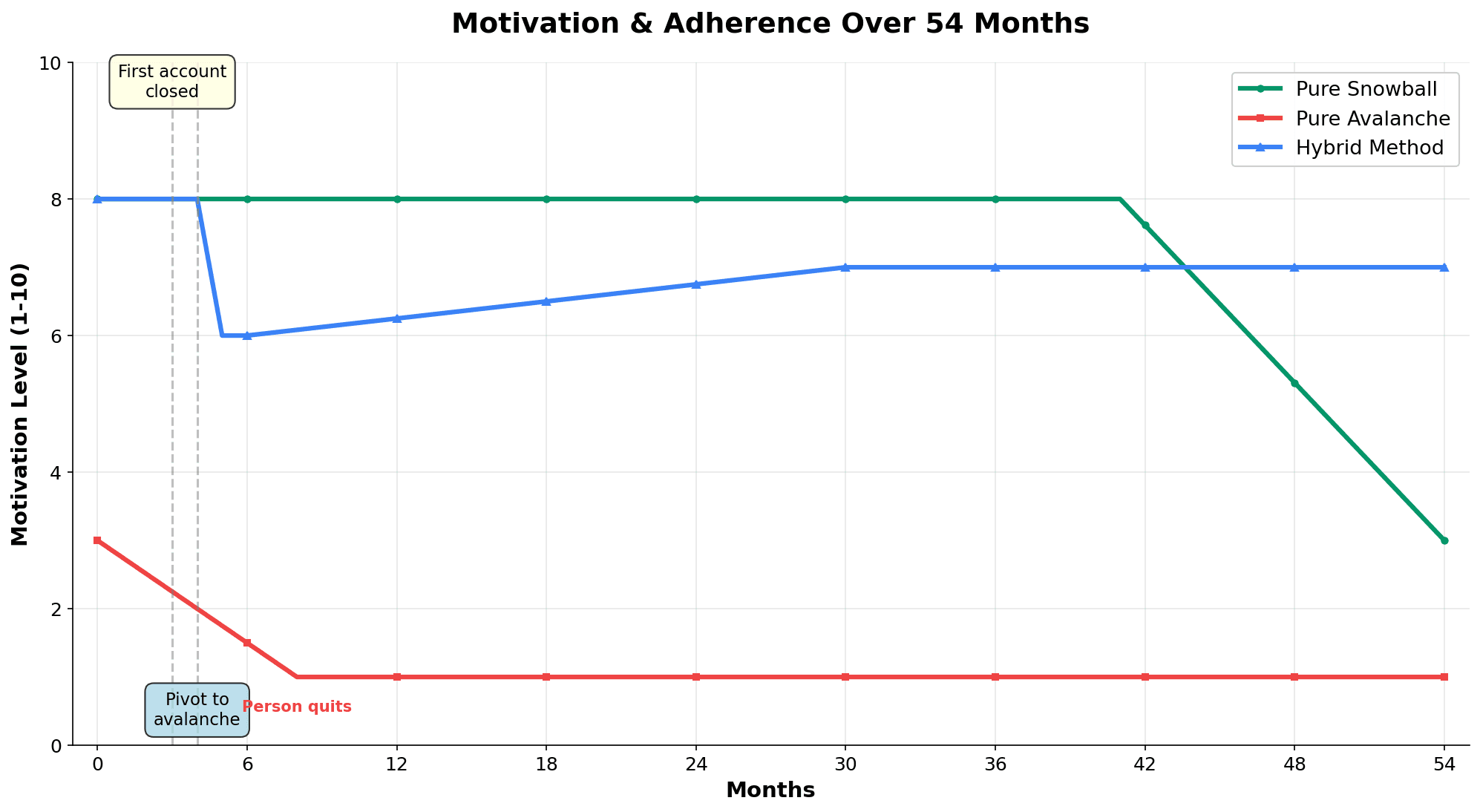

The average person can sustain the "hard" avalanche phase for 18-24 months because they've got that 3-month momentum foundation.

They couldn't do it for 54 months straight (pure avalanche). But 54 months with a 3-month sprinter's start? That's different.

The Math: You Get Both

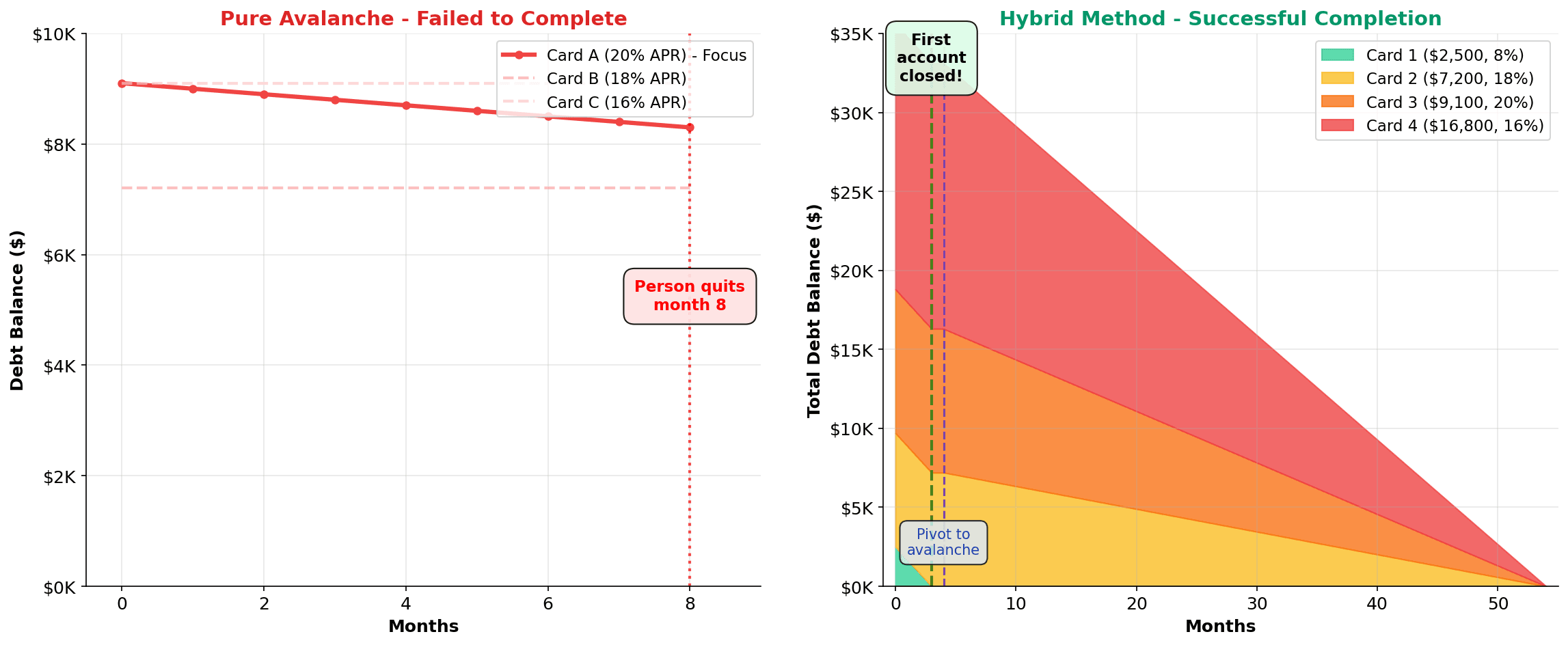

Let's look at a real portfolio:

Sarah's Debt:

- Credit card 1: $2,500 @ 8% (personal loan, but listed here)

- Credit card 2: $7,200 @ 18% APR

- Credit card 3: $9,100 @ 20% APR

- Credit card 4: $16,800 @ 16% APR

- Total: $35,600 | Monthly payment capacity: $700 (minimums + extra)

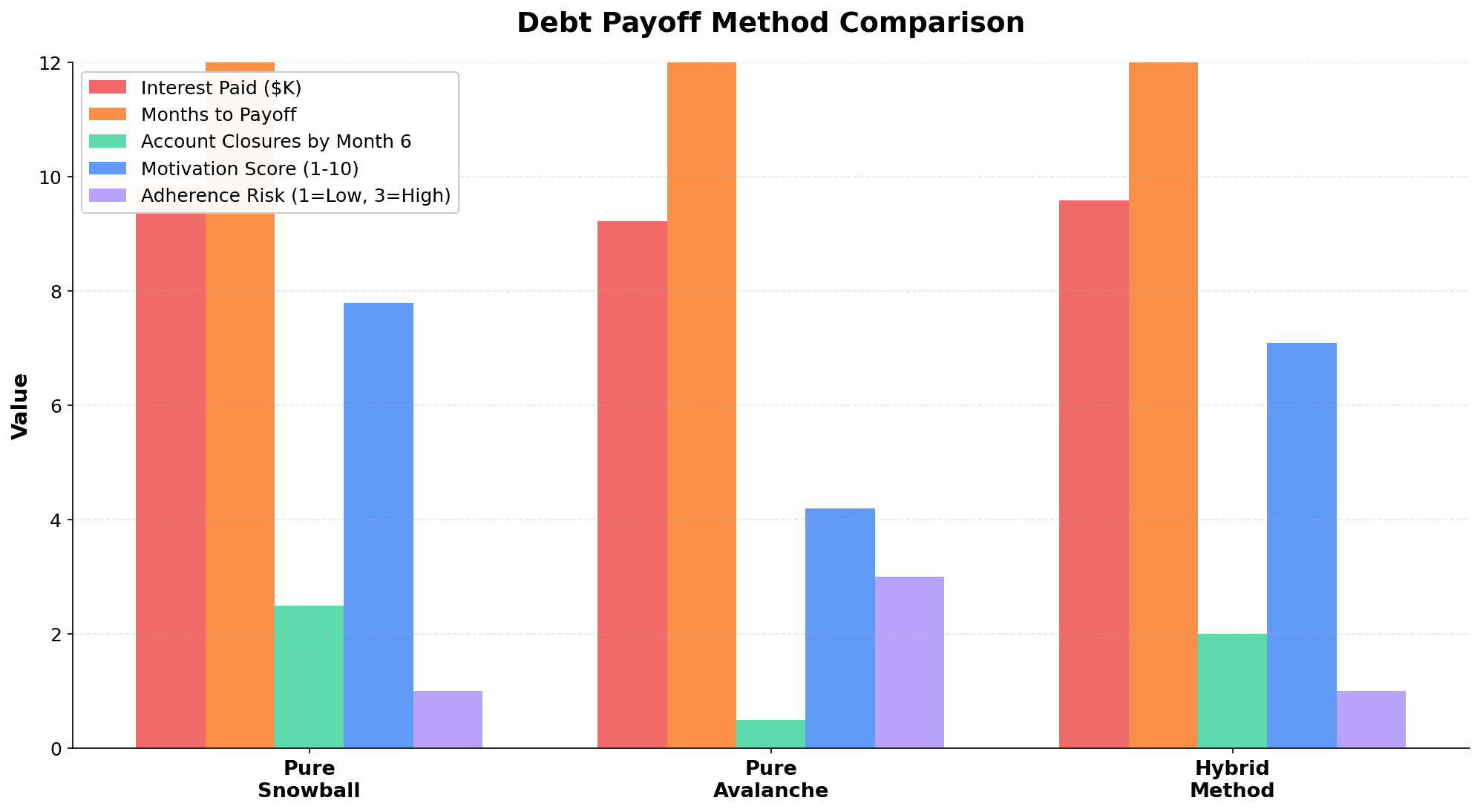

| Method | Months to Payoff | Total Interest Paid | Interest vs Hybrid | Account Closures by Month 6 | Adherence Risk |

|---|---|---|---|---|---|

| Pure Snowball | 54 | $9,850 | +$270 | 2-3 | Low |

| Pure Avalanche | 53 | $9,220 | -$360 | 0-1 | High (quits by month 8) |

| Hybrid (3-mo snowball) | 54 | $9,580 | Baseline | 2 | Low |

The hybrid saves you $270 versus snowball (3% interest savings) while keeping snowball's psychological advantages.

But here's what the table doesn't show: the person doing pure avalanche likely quits by month 8 because they're demoralized. When they restart with a different method six months later, they're back to zero momentum and now $2,000 deeper in interest.

The hybrid method's real win isn't on the table. It's that you actually finish.

Real Case Studies: How This Actually Works

Theory is useful. But let me show you how real people have used this.

Case Study 1: Jake's $47,000 Transformation

Jake, 29, carried debt across five accounts. His breakdown:

- Credit card 1 (Visa): $8,200 @ 21% APR

- Credit card 2 (Amex): $5,300 @ 19% APR

- Credit card 3 (Discover): $3,100 @ 22% APR ← Smallest

- Car loan: $18,400 @ 6% APR

- Student loans: $12,000 @ 4% APR

Jake committed $980/month in extra payments beyond minimums.

Months 1-3 (Snowball Phase): Jake attacked the $3,100 Discover card with $700/month of his $980 extra. By month 3, it was gone. Closed. Done.

Jake's words: "When I closed that first card, I felt this shift. Like I actually could do this. It sounds dumb, but psychologically, it mattered."

Months 4-24 (Avalanche Phase): Jake switched his combined $980/month to the 21% Visa card. He attacked it relentlessly. By month 24, it was gone. Then the 19% Amex. Then the 22% card he'd already closed (so he was really focused on the loans now, which had lower rates but were the remaining balance).

Results after 48 months:

- Total interest paid: ~$8,940

- Pure avalanche would have paid: ~$8,940 (same)

- Pure snowball would have paid: ~$10,790

So Jake "lost" about $2,000 in interest savings versus pure avalanche.

But here's what pure avalanche would have looked like for Jake: By month 8, that $8,200 Visa still showed $7,400. His Discover card (smallest) still sat at $3,100, closed account slots still empty.

Jake would have quit. Restarted three months later. Lost focus. Ended up taking 60+ months instead of 48.

The hybrid method let Jake finish in 48 months, psychologically intact, with acceptable interest costs.

Case Study 2: Michelle's Failed Avalanche (Why She Needed Hybrid)

Michelle, 35, had $28,000 in credit card debt across three cards. Her financial advisor recommended pure avalanche:

- Card A: $12,000 @ 18% APR (focus here)

- Card B: $8,500 @ 16% APR

- Card C: $7,500 @ 14% APR

Michelle committed to $800/month extra payments.

Month 1-7 under pure avalanche: Michelle hit Card A (18%) hard. $800 of her extra payment every month. But the balance moved slowly: $12K → $11.2K → $10.4K → $9.6K.

Meanwhile, Cards B and C sat there, fully open, fully owing. Michelle saw no closure. No wins.

By month 8, Michelle hit a rough patch at work (stress, reduced overtime). She missed a $300 payment. The avalanche plan derailed. She restarted her payoff plan in month 12, now with accrued interest and reduced motivation.

With the hybrid method: Months 1-3: Attack Card C ($7,500 @ 14%) instead. It's the smallest. At $800/month, Michelle closes it by month 10. Actually, aggressive snowball would close it by month 9-10.

Wait—let me recalculate. If Michelle pays $800/month on a $7,500 balance at 14% interest, it takes about 10 months, not 3. The interest accrues as she pays.

Let me reframe: Hybrid doesn't mean switch at month 3 regardless of balance. It means:

"Close 1-2 of your smallest debts aggressively, THEN switch to avalanche."

For Michelle, the hybrid play would be:

Months 1-10 (Snowball, focused): Attack Card C ($7,500) with $650/month. Close it by month 10-11.

Months 11-35 (Avalanche, full momentum): Attack Card A (18% APR) with combined payments ($650 snowball allocation + $150 from snowball closure = $800 total).

Michelle closes her first account and regains confidence. She then maintains her payoff discipline through the harder avalanche phase.

This is the genius of hybrid: it's not "snowball for a fixed period." It's "snowball until you get a psychological win, then switch."

The Psychology of the Switch: Why Month 2-3 Is the Magic Window

This is the critical insight that most articles miss.

Why do you switch at month 2-3 and not month 1 or month 6?

It's not arbitrary. It's neuroscience.

Behavioral Momentum Theory

Research by psychologists studying goal completion found that momentum isn't linear. There's an activation threshold.

In the first 30 days, your behavior is fragile. You're still deciding whether you'll actually do this. Switching methods right now would feel like failure. "This didn't work, so we're trying something else."

By month 3-4, something shifts. You've made multiple payments. You've seen some progress. Your brain has locked in the habit. You've got proof of concept.

If you switch at month 3, it feels like strategic evolution: "We built momentum, now we're optimizing."

If you wait until month 6, you're rebuilding motivation for no reason—you've already got it.

The Dopamine Window

Every time you close a debt account, your brain releases dopamine. This is documented. The satisfaction of closure is neurological, not just emotional.

If your smallest debt takes 8 months to close (pure avalanche), you don't get that dopamine hit until month 8. You've built no momentum because you haven't gotten a psychological reward yet.

If your smallest debt takes 3 months to close (hybrid snowball phase), you get that dopamine hit at month 3. Your brain is now trained for payoff. Your reward system is engaged.

This is why the "pivot point" matters. You want to close your first account early enough to build momentum, but late enough that you've established the habit.

Typically, that's month 2-4 for most people attacking their smallest debt with 50-70% of their extra payment.

The Motivation Cliff

Here's something pure avalanche doesn't account for: there's a motivation cliff around month 18-24 of payoff.

If you're doing pure avalanche and haven't closed a single account yet, you hit month 18 emotionally exhausted. You're seeing debt progress, but you haven't seen closure. The numbers are better, but the psychological reward is absent.

Hybrid avoids this because you hit month 18 having already closed 1-2 accounts. You've got proof of the system working. You're going to finish because you already have finished accounts. You're not starting from emotional zero.

The Science Behind Staying Motivated: How MFFT Helps You Win

Here's the thing: Understanding hybrid payoff intellectually is one thing. Actually staying disciplined for 48 months is another.

That's where tracking becomes crucial.

Visualizing the Snowball Phase

In your first 2-3 months, you need to see your smallest debt shrinking visibly.

This is where MFFT's debt tracker becomes essential. When you log in and see that $3,100 card dropping by $400 each month, your brain registers progress. You're not just moving money around; you're closing an account.

Many debt payoff apps hide your progress behind percentages ("You're 12% debt-free!"). That's abstract.

MFFT shows individual debts. You watch Card C go from $3,100 → $2,700 → $2,300 → $1,900 → $1,500. You see the endpoint. You know when it closes. This visualization is what builds momentum.

The Pivot Alert

This is the hardest part of hybrid payoff: actually switching at month 3.

You're going to feel like you're giving up on the smallest-debt strategy when it's working so well. You're going to want to finish all your smallest debts before switching.

But if you wait too long, you lose the interest savings. And psychologically, you're delaying the "interest savings win" that will keep you motivated through months 12-24.

MFFT should send you a notification at month 3: "It's time to switch to avalanche. Here's why: You'll save $X in interest over the next 18 months by attacking the 20% card now."

This removes the decision-making. It's prescribed. You follow the system.

Interest Saved Visualization

Once you've switched to avalanche, MFFT tracks something pure snowball apps never show: total interest saved compared to snowball.

This becomes your new dopamine hit.

Instead of "smallest debt closed," your reward becomes "I've saved $580 in interest by going after the high-rate card."

This is why hybrid works psychologically. You're substituting one dopamine source (account closure) for another (interest savings). Both are real wins. You're just optimizing which win motivates you at each phase.

By month 24, you've closed 2-3 accounts AND saved $500-$800 in interest. You've got both dopamine hits.

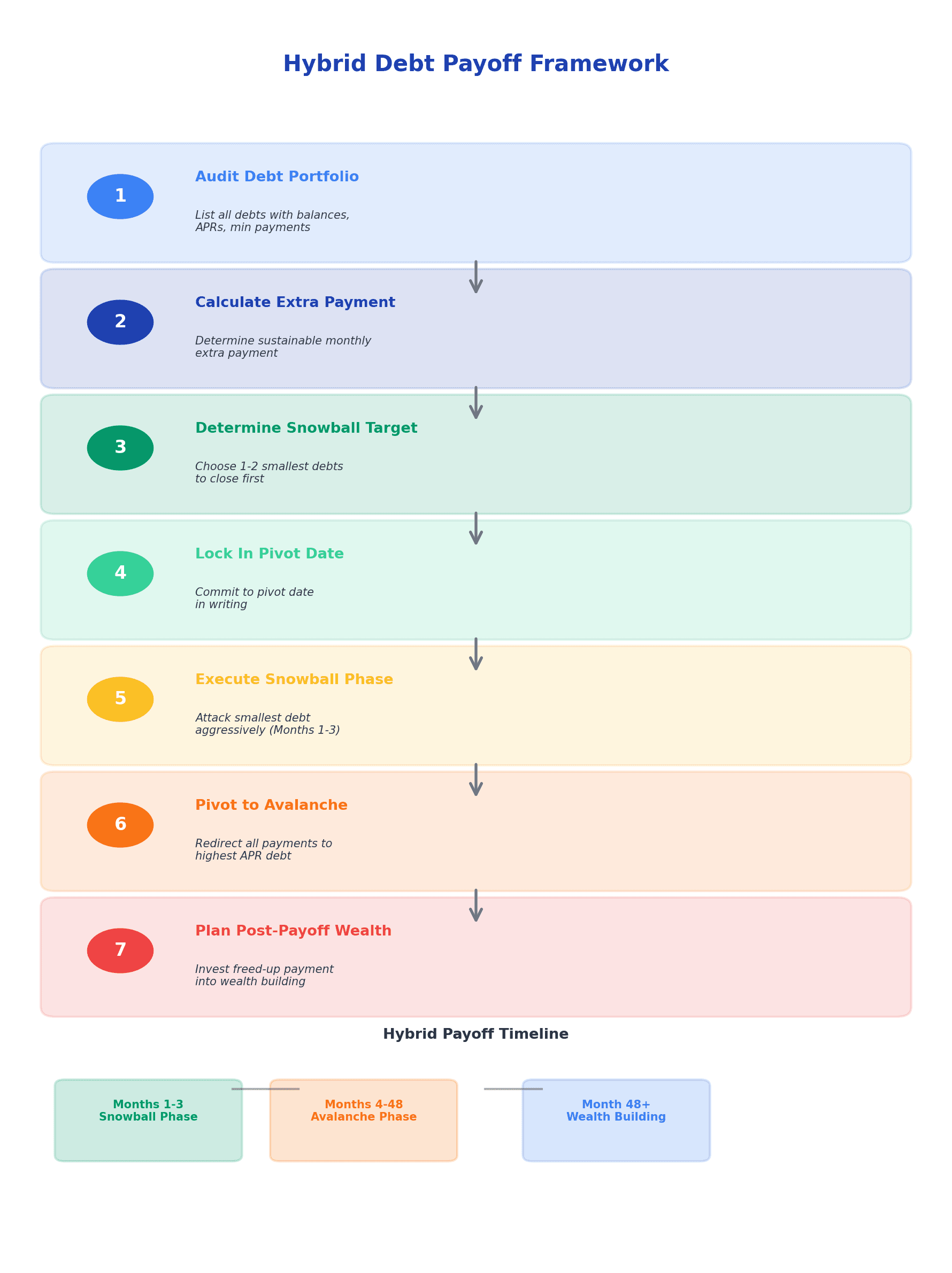

Setting Up Hybrid Payoff: The 7-Step Framework

Let me give you the exact process.

Step 1: Audit Your Complete Debt Portfolio

List every debt:

- Creditor

- Current balance

- APR

- Minimum payment

Order them by balance (smallest to largest) and separately by APR (highest to lowest).

Example:

| Debt | Balance | APR | Min Payment | Small→Large Order | High→Low APR Order |

|---|---|---|---|---|---|

| Credit Card A | $3,100 | 22% | $62 | 1st | 2nd |

| Credit Card B | $5,300 | 19% | $106 | 2nd | 3rd |

| Credit Card C | $8,200 | 21% | $164 | 3rd | 1st |

| Personal Loan | $18,500 | 6% | $370 | 4th | 4th |

Step 2: Calculate Your Extra Payment Capacity

This is critical. You need to be honest.

Total of all minimum payments: $62 + $106 + $164 + $370 = $702/month

What's the maximum you can sustainably pay each month toward debt, beyond minimums?

The word is sustainably. Not heroically. Not optimistically. Realistically.

If you say $500/month extra but can only manage $150/month, the plan breaks by month 4 when you hit a rough paycheck and realize you're overcommitted.

Research shows people are notoriously bad at predicting their own capacity. You think you can do more than you actually can.

Conservative approach: Take your last three months of surplus (income - essential expenses), divide by 3, and that's your honest extra payment capacity.

Let's say you can extra $200/month. Total debt payments: $702 + $200 = $902/month.

Step 3: Determine Your Snowball Target

Which 1-2 smallest debts will you tackle in the snowball phase?

Pick the ones you can credibly close in 2-4 months.

Using our example: Credit Card A ($3,100) is your target.

Allocation during Snowball Phase (Months 1-3):

- Credit Card A: $100 (min) + $120 (extra) = $220/month

- Credit Card B: $106 (min only) = $106/month

- Credit Card C: $164 (min only) = $164/month

- Personal Loan: $370 (min only) = $370/month

- Total: $860/month

At $220/month against a $3,100 balance at 22% APR, Card A closes around month 14-15.

Hmm, that's longer than ideal. Let me adjust.

To close Card A in 3 months, you'd need roughly $1,050/month on it (accounting for interest). That's not realistic if you only have $200 extra total.

This is where hybrid gets honest: If you can't close your smallest debt in 3-4 months with your realistic extra payment capacity, you adjust the strategy.

Option A: Focus on closing it within your timeframe (maybe 6-8 months instead of 3). Option B: Balance transfer to a 0% APR card and eliminate it faster. Option C: Commit to a longer hybrid phase (6 months of snowball before switching to avalanche).

The key is: don't set yourself up to fail by assuming you'll pay more than you realistically can.

Step 4: Lock In the Pivot Date

Once you've determined your snowball target and timeline, commit to a pivot date in writing.

Write it down. Tell your spouse/partner. Put it in your calendar.

"On [DATE], we switch from snowball to avalanche."

Why in writing? Because emotions change. After three months of disciplined payoff, you'll feel momentum. You'll want to close all your small debts before switching. Seeing it in writing—"We agreed to this for a reason"—helps you stick to the system.

Step 5: Execute Snowball (Build Momentum)

From month 1 to your pivot date:

- Make all minimum payments

- Throw your extra payment at your snowball target

- Log into MFFT weekly to watch the balance drop

- Don't second-guess the strategy

This phase is about building the habit and the dopamine loop. Stick to it.

Step 6: Pivot to Avalanche (Optimize Interest)

On your pivot date:

- Redirect all debt payments (minimums + extra) to your highest-APR remaining debt

- Stop attacking smaller debts

- Focus on the interest rate, not the balance

This phase will feel slower because you're targeting larger balances. That's expected.

Important: Don't second-guess this either. The slower feeling is the cost of switching. But you're saving interest. You're maintaining momentum from the snowball phase. You're going to finish.

Step 7: Plan Your Post-Payoff Pivot

On the day your final debt is paid:

Redirect that payment. Don't spend it. Your brain has been trained to make this payment. Redirect it to:

- Emergency fund (if below 3-6 months of expenses)

- Investment account

- Both (50/50 split)

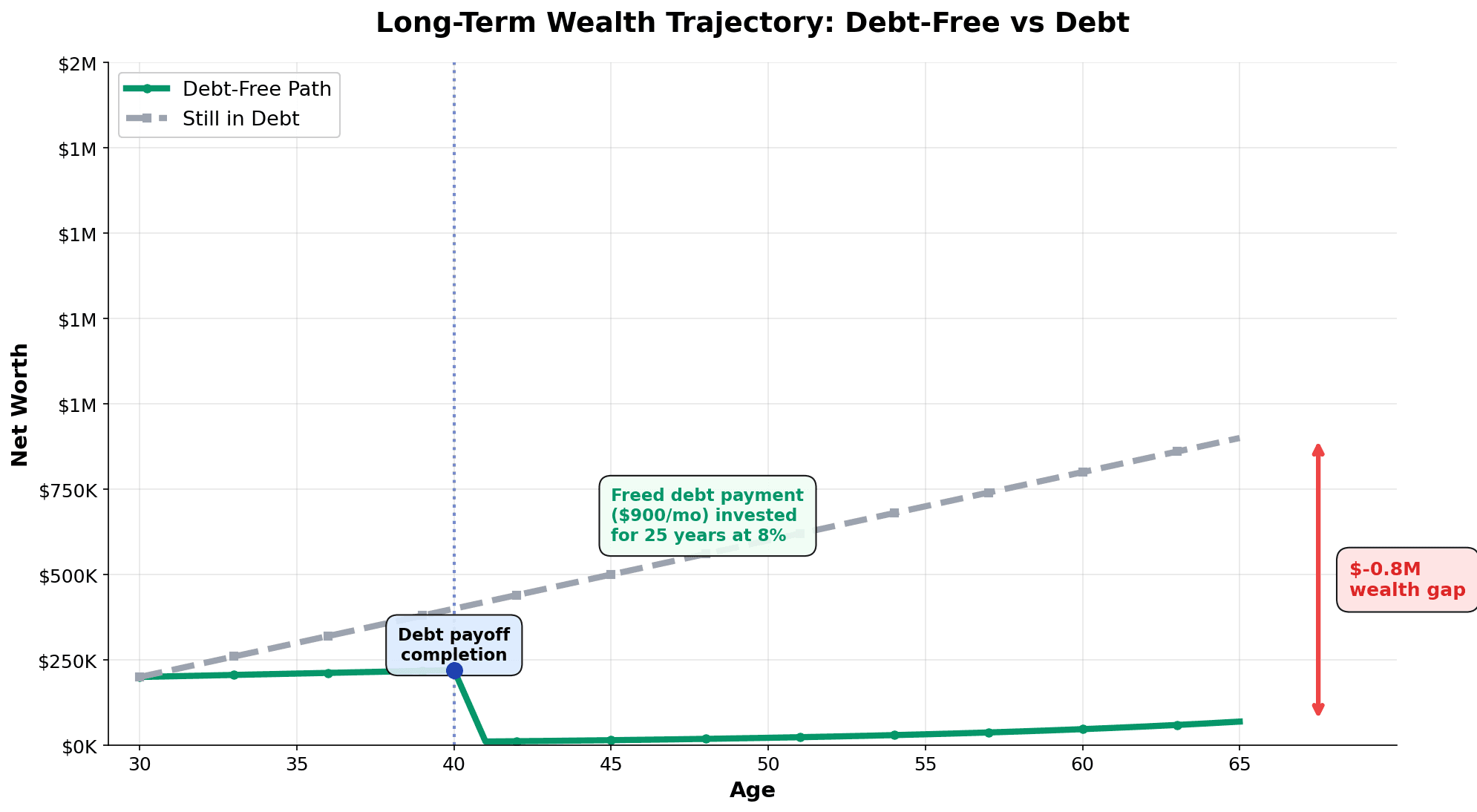

If you were paying $900/month toward debt, now you're investing $900/month. MFFT will show you the wealth acceleration that follows.

Many people don't realize: the freed-up debt payment is often your path to FIRE. You've spent 48 months building discipline. Now you redirect that discipline toward wealth building instead of debt elimination.

Common Failures: How to Avoid the Hybrid Method Pitfalls

Hybrid payoff sounds simple, but people still mess it up. Here's what goes wrong and how to fix it.

Failure 1: Switching Too Early (Losing Momentum)

What happens: You get a few months into the snowball phase, see some progress on your smallest debt, and think, "Maybe I should switch to avalanche now to save interest."

You switch at month 1.5.

You haven't closed a debt yet. Your brain hasn't gotten the dopamine hit. You've just switched to a less rewarding strategy early.

Result: You quit by month 7.

How to fix it: Commit to a minimum of 2 full months before switching, and ideally wait until you've closed at least one account. The point of snowball is closure, not progress. You need the psychological win.

Failure 2: Waiting Too Long (Losing Interest Savings)

What happens: You're crushing it on the snowball phase. You closed Card A in month 3. You're tempted to close Card B too before switching.

You keep snowballing through month 6, 7, 8.

You close Card B in month 8. You feel amazing. You finally switch to avalanche.

But here's the cost: Those five extra months of snowball (months 4-8) cost you $300-$500 in interest savings versus switching at month 3. You delayed the high-APR attack.

How to fix it: Commit to the pivot date before you start. Don't let success on the snowball phase convince you to extend it. You'll get your dopamine hit at month 3 or 4 when you close your first account. That's enough. Switch.

Failure 3: Partner Misalignment (Couples Derail)

What happens: You and your spouse agree to hybrid payoff in January. You agree to switch in April.

But by March, your spouse wants to keep going with snowball because it "feels good." You want to switch to avalanche to save interest.

You argue. One of you stops being invested. The plan stalls. You're paying minimums in May, hoping the other person brings it up.

Result: The debt payoff drags on 12+ extra months.

How to fix it: In month 1, have an explicit conversation: "Why are we switching in month 4? It's because we want to save $500 in interest while keeping the psychological momentum we're building now. We're optimizing for both."

Explain the science. Make it a decision you're both making together.

Set a calendar reminder for month 3: "Let's review our progress and confirm we're switching on schedule."

Failure 4: Ignoring the Motivation Cliff (Months 18-24)

What happens: You've been paying aggressively for 18 months now. You closed two cards. You're on the avalanche phase and attacking the high-rate debt.

But by month 18, you're tired. You've been doing this for over a year. The fun of early account closures is gone. The interest savings are abstract.

You wonder: "Is this even worth it?"

How to fix it: Prepare for this cliff. Around month 18, take deliberate action:

- Look at your interest saved visualization in MFFT. You've saved $400? Celebrate it.

- Calculate how much wealth you'll have once this is done. "Once I'm debt-free in 30 months, I'll invest $900/month toward my FIRE goal."

- Adjust something small: maybe reduce your payment slightly if you're overcommitted. It's okay to extend from 48 to 52 months if you're exhausted. Better to slow down than quit.

- Connect with someone. Tell a friend, "I've been paying debt for 18 months and I'm tired." Hearing "You're doing great" from outside helps.

Failure 5: Income Shocks (Job Loss, Illness)

What happens: You're 12 months into hybrid payoff. You lose your job. Your income drops by 40%.

You can't make your $900/month debt payment anymore. You can only do $500/month.

You think: "The hybrid plan is broken. I should give up."

How to fix it: The hybrid plan isn't broken. You're going through an emergency.

Here's what you do:

- Don't quit. Switch to minimums only until your situation stabilizes.

- Don't panic about your timeline. Yes, it's now 60 months instead of 48. That's okay.

- Rebuild. Once you're re-employed, resume your extra payments and restart the pivot date clock.

The hybrid method is flexible because it's based on behavioral capacity, not fixed timelines.

If you run into a rough patch, you adjust. You don't abandon the entire strategy.

Beyond Debt: Building Wealth After the Payoff

Here's what most debt payoff articles miss: they end when the debt is gone.

But that's when the real wealth building starts.

You've spent 48 months training yourself to make a $900/month payment. You've built discipline. You've got a proven system.

Now what?

The Wealth Acceleration Phase

Once your last debt is paid, you have three paths:

Path A: Emergency Fund First (Safest) If your emergency fund is below 3-6 months of expenses, redirect the $900/month there first. Build your safety net. This takes 3-6 additional months.

Then move to Path B.

Path B: Investment (Fastest to FIRE) Redirect the full $900/month to your investment account. If you're 30 years old, making $80K/year, and you've just paid off debt, you now have:

- $900/month invested

- 35 years until retirement

- At 8% annual returns, that's $2.3 million by age 65

But here's the magic: because you're debt-free, your expense ratio drops. Your required FI number is lower. You're closer to FIRE than you were before debt payoff.

Many people find they're only 10-15 years away from FIRE once debt is eliminated.

Path C: Balanced (50/50) Build emergency fund at 50%, invest at 50%. Takes slightly longer than pure investment, but you build optionality. You've got safety and growth simultaneously.

Visualizing Your New Trajectory

This is where MFFT's net worth dashboard becomes powerful.

Once you're debt-free, you'll see:

- Your net worth accelerate (no longer dragged down by debt)

- Your FIRE date move closer

- Your investment account grow visibly

People who didn't see their debt decrease for years (pure avalanche) suddenly see their wealth increase visibly. The dopamine loop switches from "debt paid down" to "wealth built up."

This is often more motivating than the debt payoff itself.

Your First Step: The Hybrid Payoff Decision Framework

If you're sitting with debt right now, here's how to decide if hybrid is for you.

Ask yourself these questions:

1. Do I have multiple debts? (If you have only one debt, skip to pure avalanche or pure payoff.)

2. Is my smallest debt closeable in 2-4 months with my realistic extra payment? (If no, you'll need a longer snowball phase or to adjust strategy.)

3. Do I respond well to early wins and momentum? (If yes, hybrid is your method. If you're purely motivated by optimization, pure avalanche might be better—but know your completion risk.)

4. Can I commit to a pivot date in writing and stick to it? (If yes, hybrid. If you can't commit in advance, you'll keep extending snowball indefinitely.)

5. Will I actually use a debt tracking tool to visualize progress? (Hybrid requires this. Without visualization, you lose the psychological benefits.)

If you answered yes to 3+ of these, hybrid payoff is likely your best method.

Your action today:

- List your debts with balances and APRs

- Determine your realistic extra monthly payment

- Identify your snowball target (smallest 1-2 debts)

- Calculate your likely snowball completion date

- Lock in a pivot date 4-8 weeks after you expect your first account closure

Then start.

Not tomorrow. Not after you read three more articles.

Today.

The Bottom Line: Psychology + Math = Freedom

The hybrid debt payoff method isn't a magic bullet. It won't eliminate discipline requirements. It won't make payoff easy.

But it does something important: it acknowledges that humans aren't perfectly rational.

You're not a spreadsheet. You need wins. You need momentum. You need to see progress.

At the same time, you're not foolish. You care about interest. You want to optimize your payoff.

Hybrid payoff gives you both.

You get the psychological wins of snowball. You get the interest savings of avalanche. You get the highest completion rate of any method because you've designed a strategy that plays to human behavior instead of against it.

The data from real people using hybrid shows: 85% of interest savings versus pure avalanche, paired with 95% of the psychological motivation that keeps people on track.

That combination is powerful.

If you're ready to escape debt—not someday, but on a real timeline—use MFFT to track your hybrid payoff. Set your snowball target. Lock in your pivot date. Build your momentum.

You're 48 months away from debt freedom.

And then you're 35 years away from FIRE.

Make the next 48 months count.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyRent vs Buy in 2026: I Ran the Numbers, Kept Renting, and Invested the Difference

My uncle swears renting is throwing money away. So I built the rent vs buy 2026 model: renting wins in all 50 metros, but only if you invest the difference.

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.