Tariff Impact on Household Budgets: $570-$1,050 in 2026

TL;DR: Tariffs cost the average U.S. household $570-$1,050 in 2026, with the overall tariff rate at 11% — the highest since 1943 (Yale Budget Lab). The burden is regressive: the bottom 20% of earners lose about 0.8% of income versus 0.3% for the top 20%. Tariffs hit goods, not services — so the strongest defenses are shifting spending toward services, extending product lifecycles, and bulk-buying strategic items before the July 24, 2026 Section 122 expiry.

You're scanning your grocery receipt and notice the total went up 8% since last month — even though you bought the same items. You're looking at a new car and the dealership adds an extra $6,200 to the quote. You're thinking about replacing your aging refrigerator and can't believe the new price tag. This isn't just inflation anymore. Tariffs are hitting your household budget right now, and the impact is real.

I'm Dennis Vymer, and I've spent the last few months studying how tariffs affect everyday Americans. Here's what I found: the average U.S. household faces $570–$1,050 in annual tariff costs in 2026. But the real story isn't in the average—it's in how brutally these costs hit lower-income families hardest.

What Is a Tariff and Why It Matters to Your Budget

Let's start with plain English, not economics jargon.

A tariff is a tax on imported goods. When goods arrive at U.S. ports, the government says: "That shirt from Vietnam? That's 21% more expensive now. That car from Mexico? Add 12%."

Manufacturers face these tariffs, and they pass the costs forward. Your favorite clothing brand pays more for fabric—so your jeans cost more. Toyota pays more for parts—so your next car costs more.

Here's the key: tariffs hit goods, not services. Your haircut, doctor visit, or plumber's rate? Nearly untouched. But that refrigerator, car, laptop, winter coat, or furniture? All vulnerable.

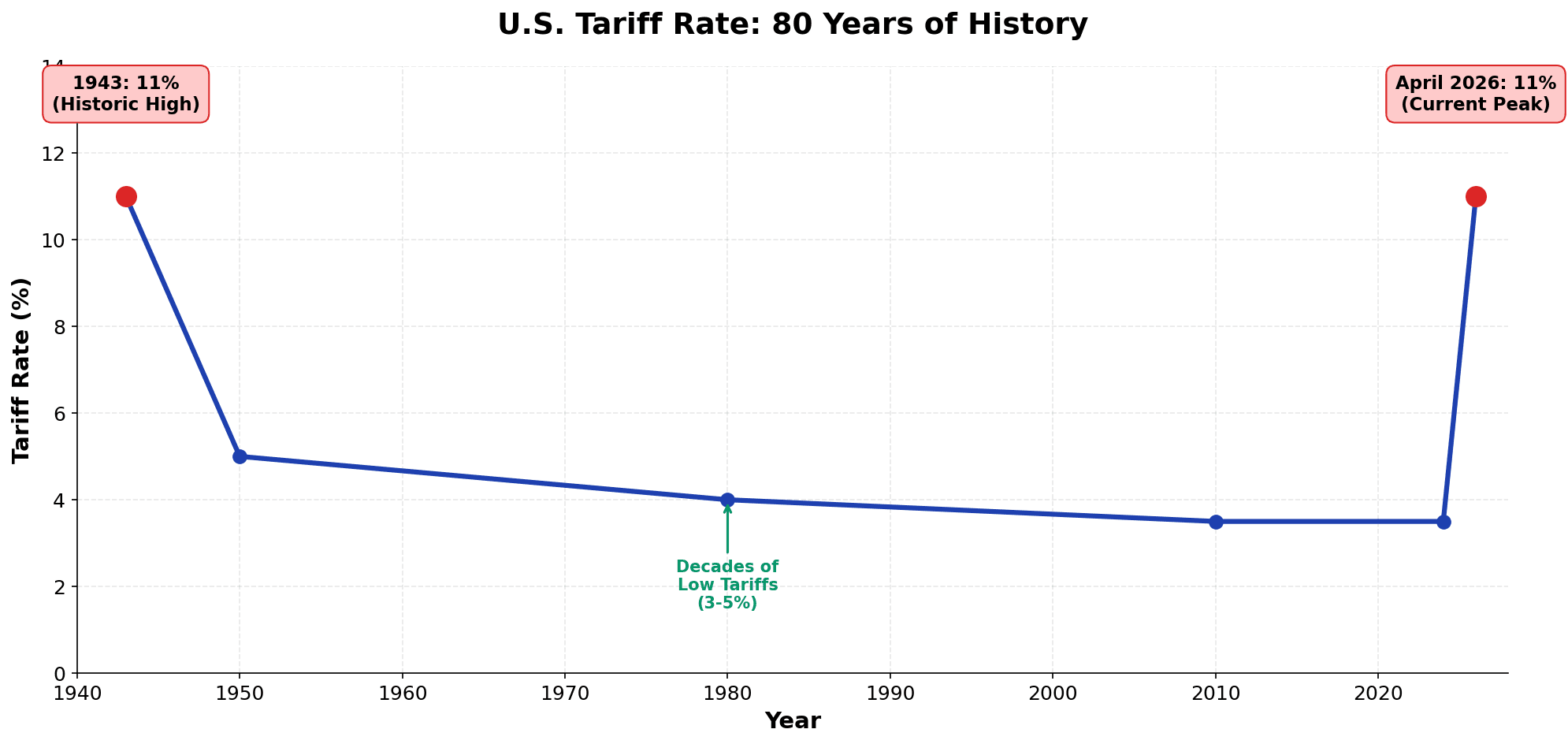

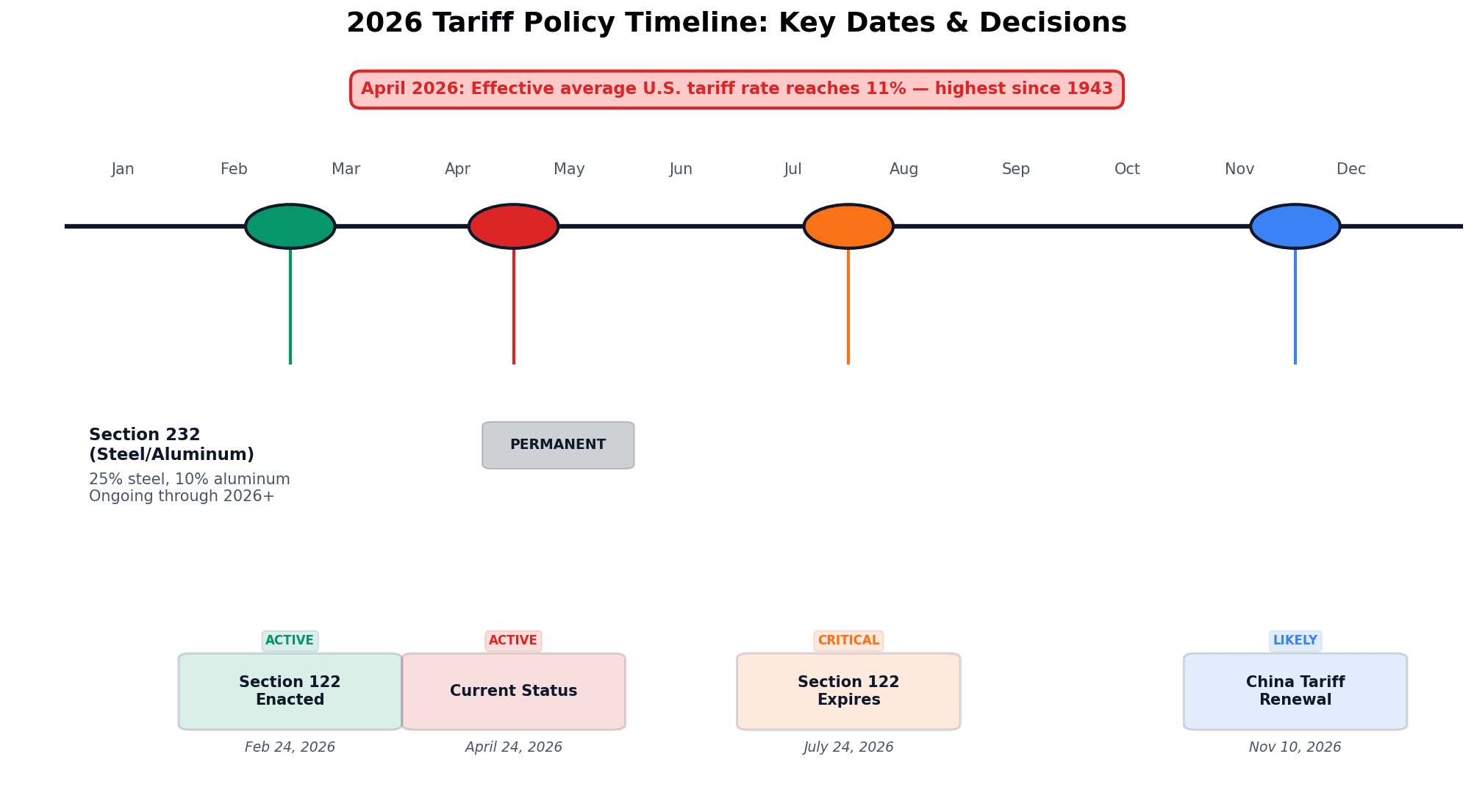

The U.S. tariff rate in April 2026 reached 11%, the highest since 1943. Section 122 tariffs (the main ones) expire July 24, 2026—three months from now—but policy uncertainty means households should plan for continued pressure.

The Real Cost: $570–$1,050 Per Household in 2026

Let me show you the uncomfortable truth with actual data from the Yale Budget Lab.

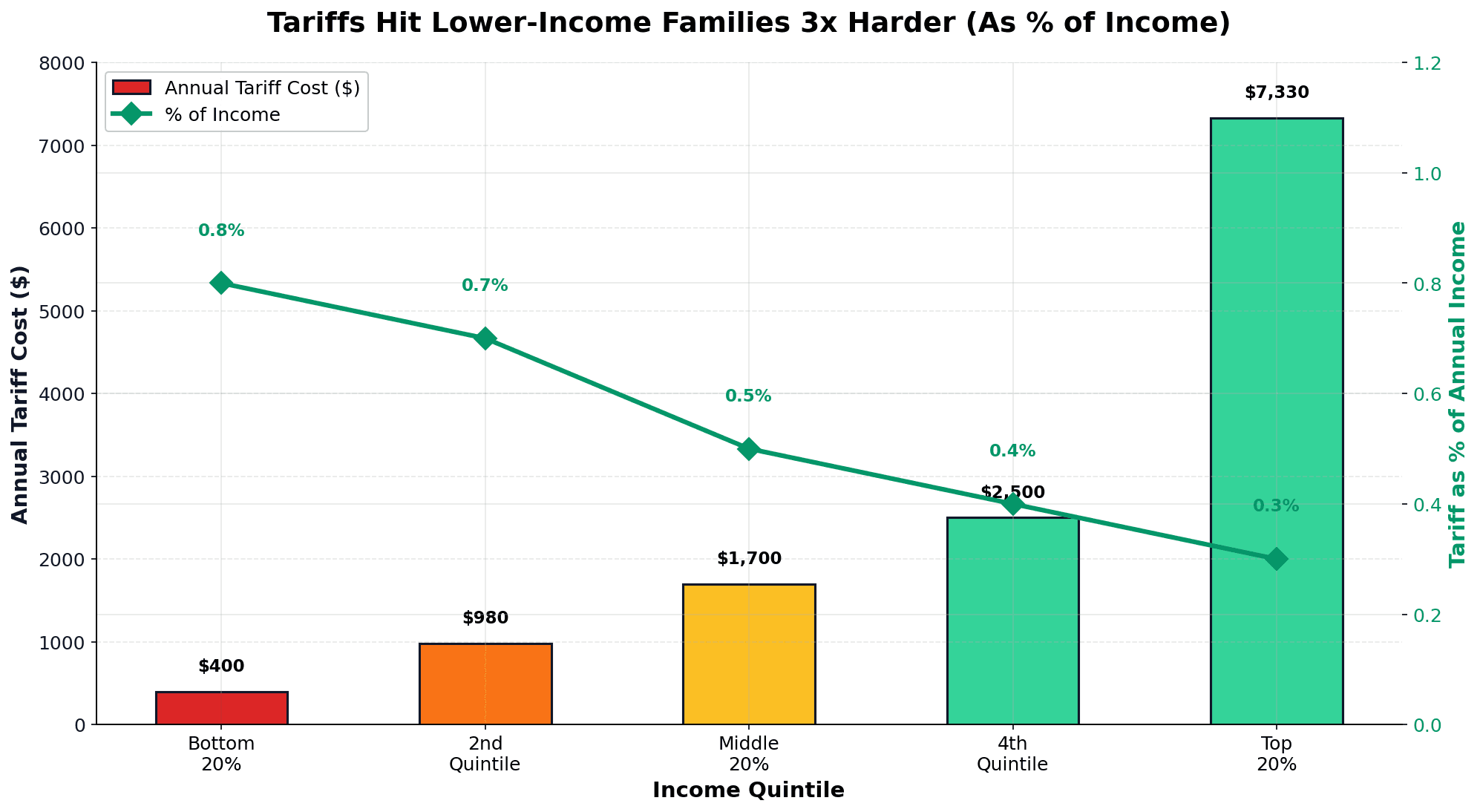

The average household pays between $570 and $1,050 in tariff costs this year. But "average" is misleading because tariffs are regressive—they hit the poor harder, as a percentage of income.

Here's the breakdown by income quintile:

| Income Level | Annual Tariff Cost | Percent of Income | What This Means |

|---|---|---|---|

| Bottom 20% | $400 | 0.8% | Nearly 1 of every 125 dollars |

| 2nd Quintile | $980 | 0.7% | Still above 0.5% |

| Middle 20% | $1,700 | 0.5% | More than half a percent |

| 4th Quintile | $2,500 | 0.4% | Lower pressure relative to income |

| Top 20% | $7,330 | 0.3% | Lowest burden as % of income |

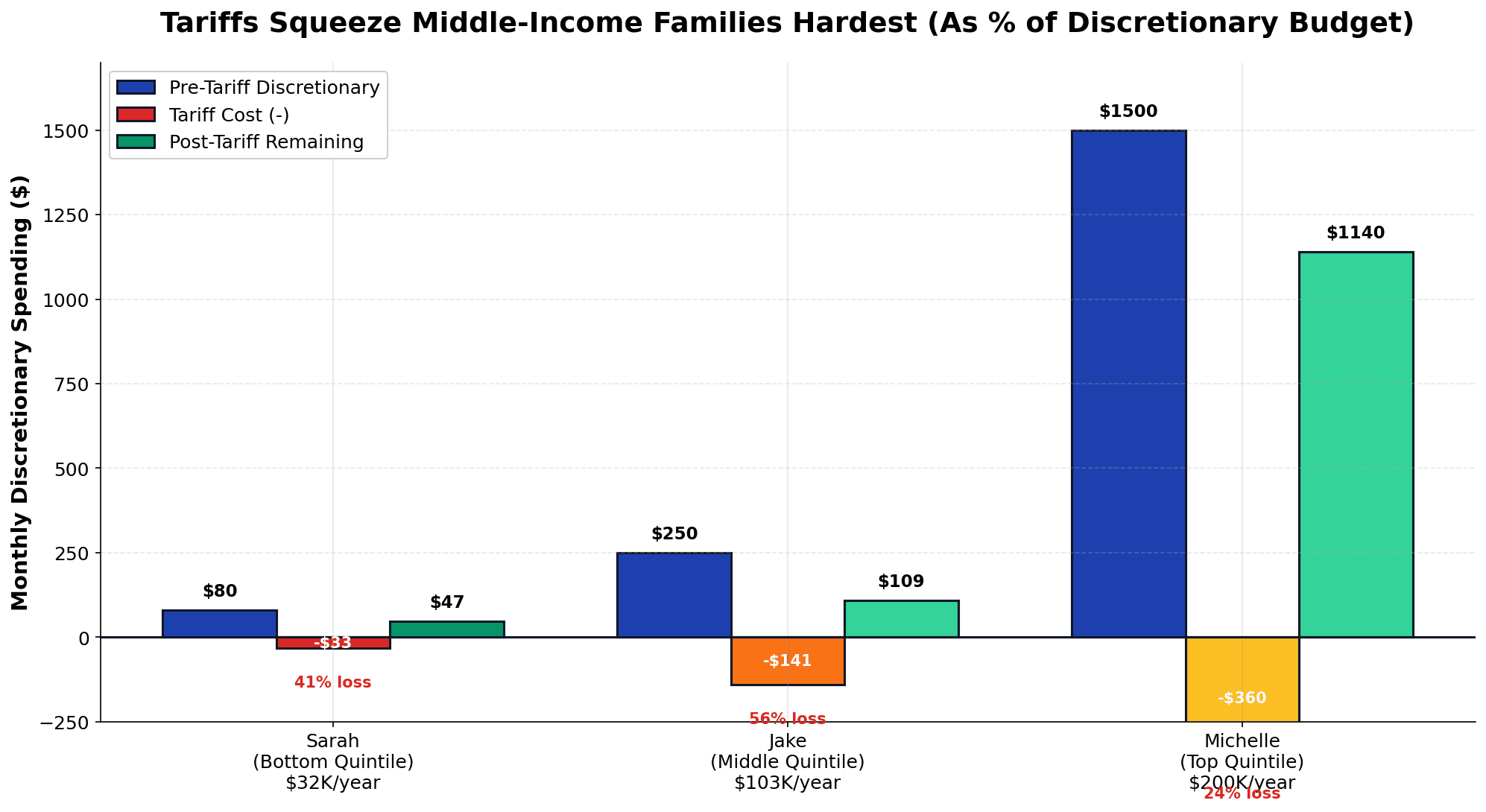

The inequality is stark. A single parent earning $32,000 loses 0.8% of income to tariffs ($33/month). A software engineer earning $200,000 loses 0.3% ($28/month proportionally). Same percentage burden? No. Sarah loses $33; Michelle loses far less relative to her wealth.

This is why financial experts like Ramit Sethi call tariffs "directly a tax on the poor and middle class."

Which Product Categories Are Hit Hardest

Not all tariffs are created equal. Some hit your budget immediately. Others catch you when you least expect them.

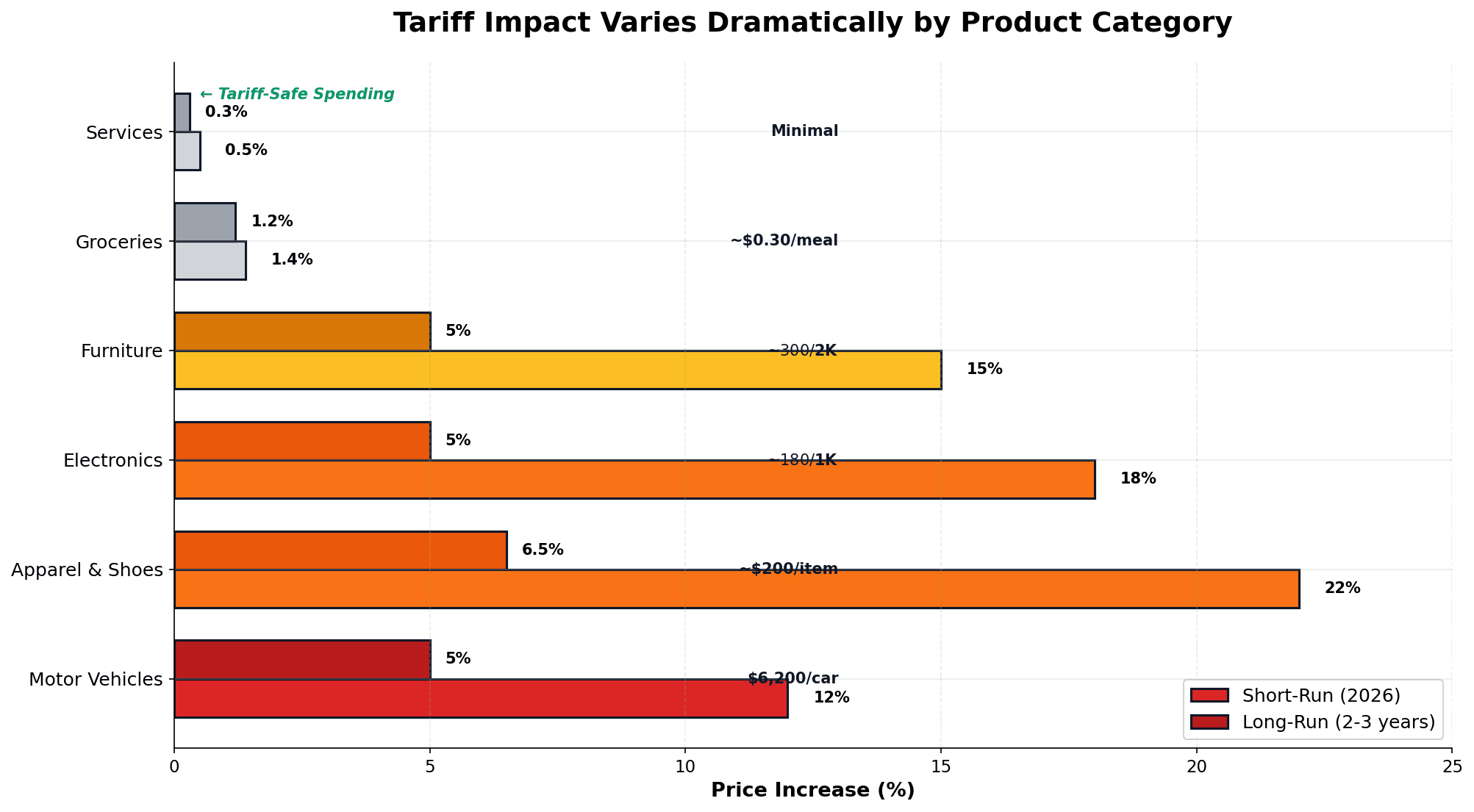

Here's what Yale Budget Lab data shows for short-run price increases (2026):

| Product Category | Short-Run Price Increase | Long-Run Increase | Real Impact |

|---|---|---|---|

| Motor Vehicles | 12% | 5% | $6,200 per new car purchase |

| Apparel & Shoes | 21–23% | 6–7% | Children's clothes, winter jackets |

| Electronics | 18% | 5% | Laptops, phones, appliances |

| Furniture | ~15% | ~5% | Sofas, beds, office equipment |

| Groceries | 1.4% | 1.2% | Minimal but steady creep |

| Services | < 1% | < 1% | Your budget's safest bet |

What's the difference between short-run and long-run? In the short term (2026), prices spike as tariffs apply immediately. Over 2–3 years, some manufacturers absorb costs into margins, some pass full costs through, and some shift supply chains—so the long-run impact stabilizes but doesn't disappear.

The takeaway? Motor vehicles and clothing are your biggest exposure. If you're a single parent buying your kids new shoes every 6 months, tariffs compound. If you're planning a vehicle replacement, you're looking at thousands of dollars in tariff taxes.

The Tariff Trap: Why Services Are Safer Than Goods

Here's a strategy many people miss.

Tariffs almost exclusively hit tangible goods—things you can touch. Services—which you pay for but don't physically carry home—face minimal tariff pressure.

Think about your budget:

- Goods exposure (tariff-vulnerable): groceries, clothing, electronics, furniture, vehicles, appliances, tools, toys

- Services exposure (tariff-safe): haircuts, gym memberships, health care, car repairs, consulting, streaming, pet grooming, tutoring

A household spending 60% on goods and 40% on services absorbs tariff costs across a larger surface area. A household spending 75% on goods (lower-income families often must) faces concentrated pain.

This is why redirecting discretionary spending toward services—instead of buying more stuff—becomes a conscious budgeting strategy in 2026. Instead of a $300 exercise bike, take a $200 gym membership. Instead of a $400 home office gadget, hire a virtual assistant for four hours ($200).

You're not depriving yourself. You're pivoting away from tariff-heavy spending into resilient categories.

Tariff Calculators and Tools: What Will It Cost You?

Before you panic, you can estimate your personal tariff burden.

The Tax Foundation Tariff Tracker (taxfoundation.org) breaks down tariff rates by product category. The Yale Budget Lab publishes detailed income-level analysis.

But for a quick personal estimate:

- Pull 3 months of your bank and credit card statements.

- Categorize spending: groceries, clothing, vehicles, electronics, furniture, services, rent/mortgage, utilities.

- Calculate your "goods-heavy" spending as a percentage of total.

- Apply the tariff rates from the table above.

Example: Jake spends $2,000/month. Breakdown: $600 groceries (1.4% tariff cost = $8), $200 clothing ($42 at 21%), $0 vehicles (planning replacement next year), $300 electronics/household ($54), $800 services/utilities ($0 tariff). His monthly tariff impact: $104/month = $1,248/year.

Not every purchase faces tariff pressure, so your real burden is likely lower than the headline numbers suggest. But if you're buying a car, replacing major appliances, or refreshing a wardrobe in 2026, you'll feel it.

7 Budget-Hardening Strategies to Offset Tariff Costs

The question isn't "Can I avoid tariffs?" (You can't—they're baked into prices.) The question is: "How do I offset them?" Here are seven concrete tactics.

1. Shift Spending to Services (Your #1 Defense)

Services face minimal tariff exposure. Redirect discretionary spending from goods to services:

- Replace a $400 smart home device with a $150/month home cleaning service

- Skip the $300 office gadget; hire freelance help instead

- Choose a $50 gym membership over a $500 home equipment purchase

Monthly impact: $100–200 savings if you consciously redirect just 20% of discretionary goods spending.

2. Extend Product Lifecycles Through Preventive Maintenance

A $100 car transmission fluid service now saves $1,500 in emergency repairs later. A $200 appliance repair prevents a $600 replacement purchase.

The math: Replacing your car costs $6,200 more (12% tariff). Extending its life by 18 months through maintenance avoids that cost entirely.

Monthly impact: Budget $50–100/month for preventive maintenance (oil changes, appliance servicing, HVAC checkups). This saves 10–20x that amount in deferred replacement costs.

3. Bulk-Buy Strategic Items Before July 24, 2026

Section 122 tariffs expire July 24, 2026. In-stock goods at current tariff-adjusted prices will be your highest-priced option.

Strategic categories to pre-buy (if you have cash flow):

- Winter clothing (buy now for fall)

- Large appliances (fridge, washer, dryer)

- Tires and car maintenance supplies

- Furniture you've been considering

Important: This only works if you have savings to absorb the purchase timing. Don't go into debt to buy early.

Potential savings: $200–500 per household depending on planned purchases.

4. Source Alternative Products and Cheaper Retailers

Not all products face equal tariff pressure. Domestic brands and products with lower import exposure face lower tariff costs.

- Seeking American-made furniture? You'll pay tariff tax on imports, but domestic production costs less.

- Looking for clothing? Fast-fashion retailers often take tariff hits harder than premium brands with diversified supply chains.

- Electronics? Consider refurbished models (tariffs apply to new goods, not resale).

Monthly impact: 5–10% savings by consciously choosing lower-tariff alternatives.

5. Eliminate Discretionary Goods Spending

This is the nuclear option—but it works.

Cut non-essential goods purchases for 6 months:

- Pause clothing beyond basics

- Skip new electronics (use your phone/laptop longer)

- Defer furniture purchases

- Eliminate home décor shopping

Simultaneously, redirect that money to either emergency savings or offset income boosts (see #7).

Monthly impact: $200–500 depending on your current discretionary goods spending.

6. Build a Dedicated "Tariff Buffer Fund"

Separate from your emergency fund, create a savings account specifically for tariff-driven price shocks.

Target: $200/month into a high-yield savings account (currently earning 4–5% APY).

Why separate? Your emergency fund should remain untouched for true emergencies. Your tariff buffer fund is for planned purchases that will arrive at higher tariff-adjusted prices.

Monthly impact: $200/month = $2,400/year, enough to absorb tariff taxes on a vehicle purchase or major appliances.

7. Boost Income to Directly Offset Tariff Burden

The most powerful strategy: earn more. A $150/month side gig (freelance work, gig economy) directly compensates for tariff burden without requiring lifestyle cuts.

How this ties to MFFT: Redirect 100% of side income to either your tariff buffer fund or direct investment. This keeps your lifestyle spending intact while building wealth.

Link for deeper strategy: Check out our guide on Salary Negotiation Data Driven 2026—the same strategies that work for raises work for side income negotiation.

Monthly impact: +$150/month side income = fully offset tariffs for many households.

Using MFFT to Track and Offset Tariff Impact

This is where it gets practical.

The MFFT budgeting framework (zero-based budgeting) is perfect for tariff-era planning because it forces you to assign every dollar to a category. That visibility reveals your tariff exposure instantly.

Here's how to use MFFT to model tariff scenarios:

- Set up a "Tariff Impact" tracking category in your monthly budget. Log purchases in tariff-heavy categories separately.

- Create a "Tariff Buffer" savings goal ($200–300/month). Watch it grow alongside your emergency fund.

- Run "what-if" scenarios. "If I buy a car in July, how does that impact my annual savings target?" MFFT's zero-based framework makes this instant.

- Audit your discretionary goods spending. Which $100/month purchases are services (safe) vs. goods (tariff-exposed)? Shift deliberately.

- Track side income separately. If you earn $150/month from freelance work, direct it to investments instead of lifestyle creep. MFFT's automation helps.

Getting started with budgeting? Our guide How to Start a Budget walks you through zero-based budgeting fundamentals. Apply those principles with tariff-era discipline.

Emergency fund expansion: Standard advice was 3–6 months. Tariff volatility pushes that to 9–12 months, especially for single-income households or gig workers. Link: Emergency Fund Crisis 2026—tariff-specific guidance on why larger buffers now make sense.

Tariffs and Inflation: Understanding the Difference

People ask: "Is this just inflation?"

No. Tariffs are a specific, policy-driven form of inflation affecting goods disproportionately. Inflation is general—everything rises. Tariffs are targeted—goods spike, services stay flat.

Here's the data from the Federal Reserve: tariffs explain 3.1% of core goods inflation since January 2025. That's measurable, distinct, and policy-reversible (when tariffs expire, prices should stabilize).

General inflation rose 2.8% in 2025. Tariff inflation adds another 0.6–0.9% on top, but mainly in goods categories.

The distinction matters for your budget because:

- General inflation hits everything; you budget for it everywhere.

- Tariff inflation is goods-concentrated; you can pivot strategically toward services.

Read more: Inflation for a deeper dive into inflation dynamics and purchasing power erosion.

Political and Economic Outlook: How Long Will Tariffs Last?

Here's what you need to know for planning purposes.

July 24, 2026: Section 122 tariffs are set to expire unless extended. That's 90 days away. Congressional outlook is uncertain, but many economists expect some form of extension or renegotiation.

Key regulatory dates:

- April–May 2026: Ongoing investigations into pharmaceutical and medical device tariffs (potential new tariffs)

- July 24, 2026: Section 122 expiration (critical pivot point)

- November 2026: China tariff agreement renewal (possibility of escalation)

- Ongoing: Section 232 (steel, aluminum, copper) tariffs remain permanent

The bottom line for your household: Plan for tariffs to stick around through at least July 2026, with possibility of extension or new tariff waves. Don't assume relief; plan conservatively. If tariffs expire on schedule, July–August 2026 could be a window for planned purchases (appliances, vehicles) before prices normalize downward—or before tariffs return in new form.

Counterarguments: Do Producers Absorb Some Costs?

I want to give balanced perspective here.

Producers do absorb some tariff costs. Federal Reserve economists note that roughly 32% of manufacturers absorb costs into profit margins while 42% combine price increases with margin compression. Some tariff burden falls on companies, not consumers—just not all of it.

However, the pass-through remains high. A 2025 Federal Reserve study found that tariff inflation passes through to consumer prices faster in essentials (groceries, utilities) than in discretionary goods (electronics, furniture). This means lower-income families—who spend more on essentials—face faster price pressure.

Long-term supply chain reshoring is a real argument from tariff proponents. If U.S. domestic production ramps up (steel plants being built, auto production rising to 54.4% domestic), long-term tariff dependence could decrease. But that takes 1–3 years to realize, offering no comfort to households paying tariff taxes today.

Fiscal benefits are also real: Tariffs collected ~$77 billion in 2024 and are projected to collect $421 billion in 2027. That revenue could fund deficit reduction or infrastructure. But that's a government-level benefit, not a household-level offset.

The honest truth: Some costs are absorbed, but most reach consumers. Reshoring is real but slow. Fiscal benefits exist but don't help your wallet today. Plan for the burden you'll face now while hoping for long-term relief.

Wealth-Building Through Tariff Discipline

Here's the opportunity hidden in constraint.

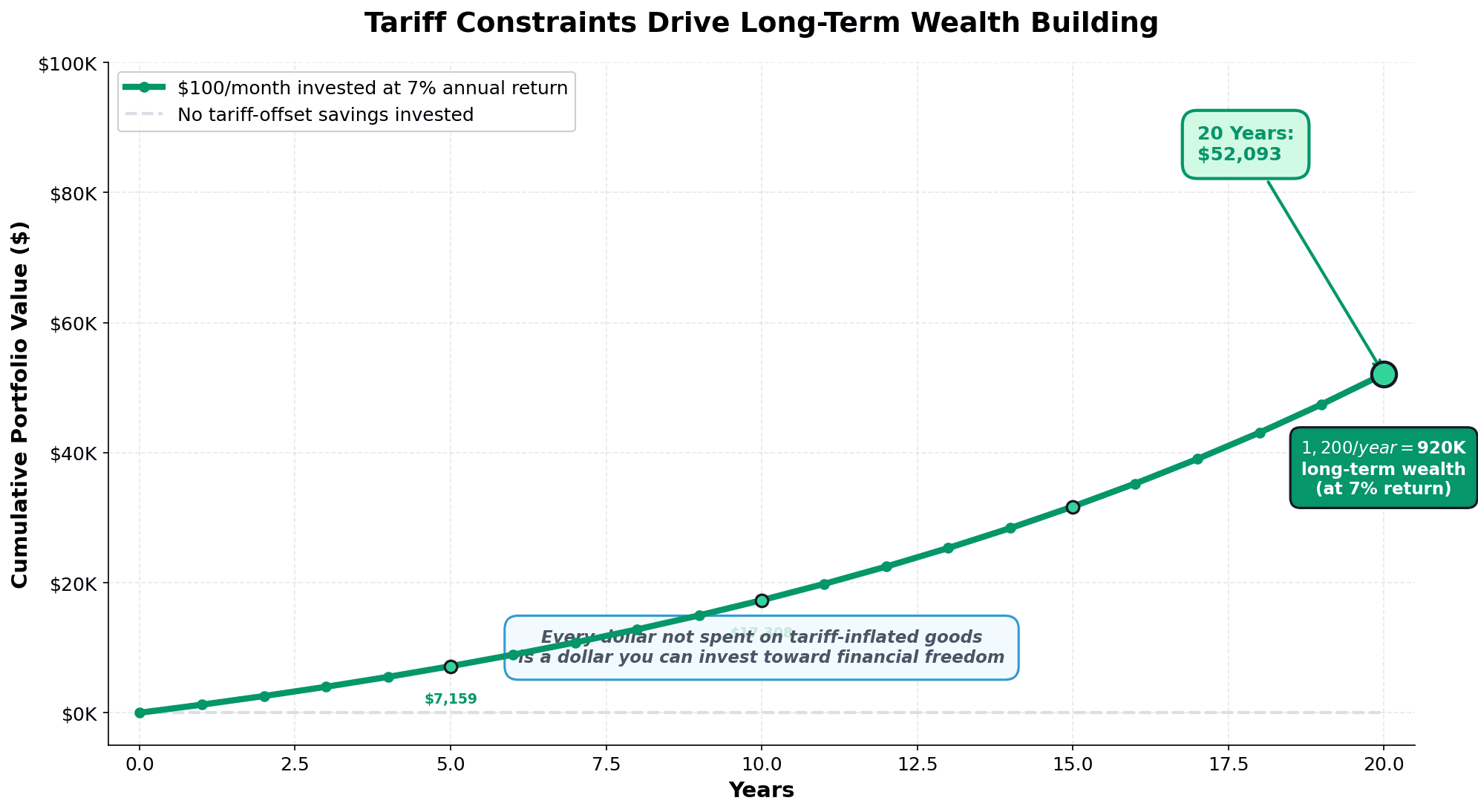

When you're forced to think carefully about goods purchases, you naturally shift toward asset-building instead of consumption. That $100/month you cut from discretionary goods? Invest it.

The math over 20 years:

- $100/month invested at 7% annual return = $77,000

- $1,200/year tariff-offset savings redirected to index funds = $920,000 total portfolio impact

You're not being squeezed into poverty. You're being squeezed into disciplined wealth-building.

This connects directly to our guide on Wealth, Time, and Money Discipline—the idea that constraints force better choices and long-term wealth accumulation beats short-term consumption every time.

Action Plan for April 2026

Here's what you should do this week:

- Pull 3 months of statements. Categorize spending by tariff exposure (groceries, clothing, vehicles, electronics vs. services).

- Estimate your personal tariff burden. Use the tables in this article. Is it $400/year or $2,000/year?

- Identify your three biggest tariff exposures. For most households: vehicles, clothing, electronics, furniture.

- Make a decision on any planned major purchases. Before July 24: buy now (tariff-adjusted prices locked). After July 24: wait for potential relief.

- Set up a tariff buffer fund. $200/month into a high-yield savings account, separate from your emergency fund.

- Audit discretionary goods spending. What $100–200/month can you redirect to services or investments?

- Set up tariff tracking in MFFT. Create a category so you see real impact month-to-month.

Final Thought: Tariffs as a Budget Discipline Tool

I started writing this article worried about messaging. Tariffs do hurt. The regressive impact on lower-income families is real. Sarah (earning $32,000) loses $33/month. That's real money.

But I also realized something: The households that will thrive through tariff cycles are those that respond strategically—not those that panic.

You can't avoid tariffs. But you can:

- Pivot toward services

- Plan major purchases strategically

- Invest the money you save through discipline

- Build emergency buffers before the next shock

That's what MFFT is about. It's not about earning more (though that helps). It's about seeing exactly where your money goes, making intentional choices, and building long-term wealth through discipline.

Tariffs are a short-term shock. MFFT discipline is forever.

Log into MFFT today. Start tracking your tariff exposure. Build your buffer fund. And remember: every dollar you don't spend on tariff-inflated goods is a dollar you can invest toward the financial freedom you actually want.

You've got this.

Dennis Vymer My Financial Freedom Tracker April 2026

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.