Emergency Fund 2026: How Much You Need and How to Build It

TL;DR: 59% of Americans can't cover a $1,000 emergency without borrowing, and 24% have no emergency savings at all (Bankrate's January 2026 report). The right target isn't a universal "3-6 months" — it's 3-12 months of expenses depending on your job security, health, and dependents. Park it in a high-yield savings account at 4-5% APY, where a $10,000 fund earns $400-500 a year instead of $39 in an average checking account. Then build in stages: $500, $1,000, one month of expenses, three months, six.

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Start a Budget — the foundation of money management

- How to Start a Budget — escape paycheck-to-paycheck living

- Financial Levels Step by Step — where emergency funds fit in your strategy

You're scrolling through your phone on a Wednesday afternoon when a notification pops up: your car broke down. The mechanic quotes $1,800 to fix it.

Your paycheck doesn't land until Friday. You have $340 in your account.

You have four options:

- Put it on a credit card at 21% APR and pay $2,100+ total

- Borrow from family and feel the shame

- Take out a personal loan and wait 3-5 days for approval

- Have an emergency fund and handle it calmly

Most Americans are living option 1-3.

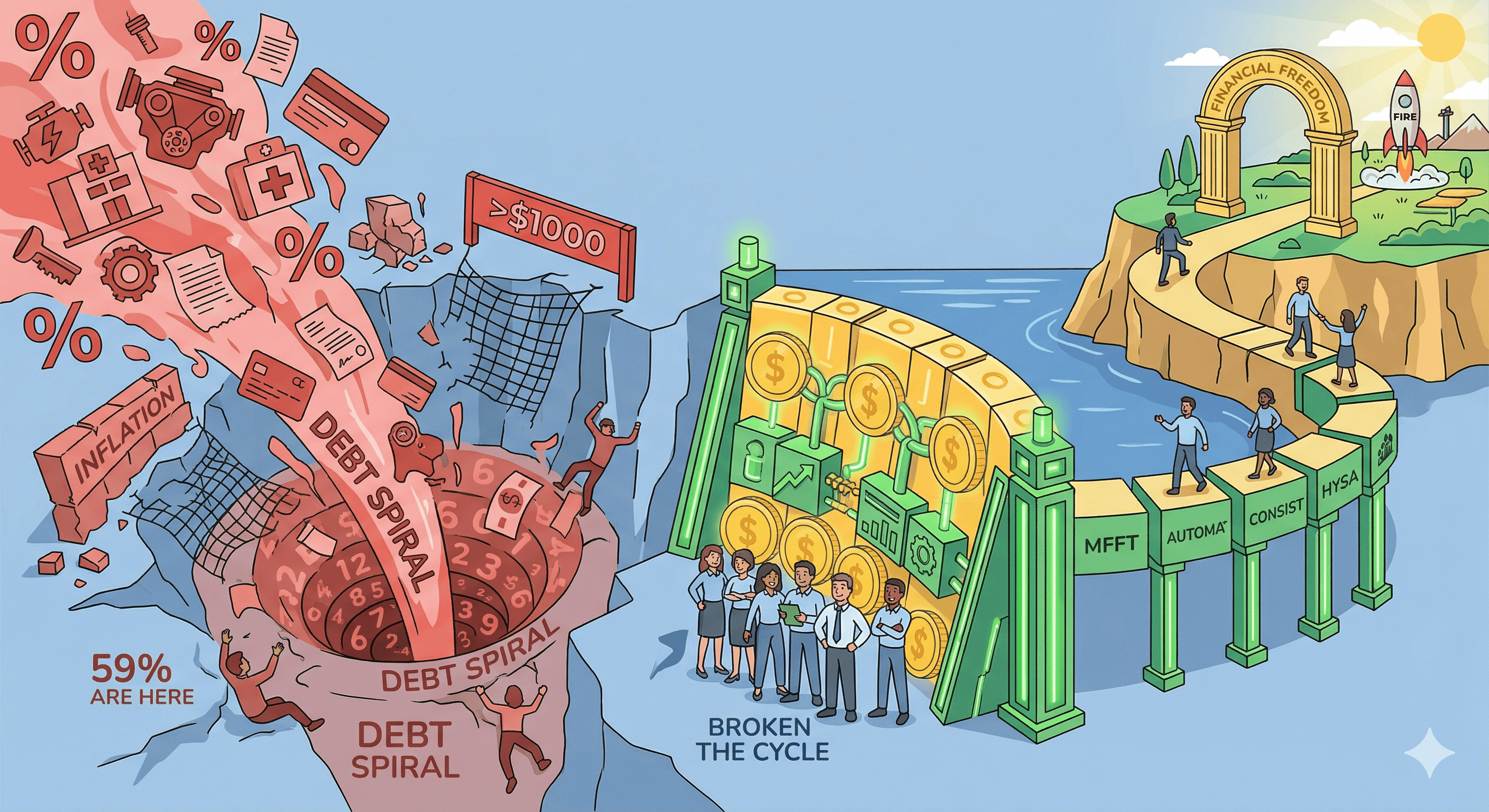

Here's the crisis: 59% of Americans cannot cover a $1,000 emergency without going into debt. Not a $5,000 emergency. Not a $2,000 emergency. A single thousand dollars.

And that's not the worst part. The worst part is that 24% have zero emergency savings at all. They're not building toward a buffer. They're living one car repair away from financial catastrophe.

This article is going to show you the reality of the 2026 emergency fund crisis, why it's happening, and exactly how to break the cycle — no matter where you're starting from.

The 2026 Emergency Fund Reality Check: The Data Behind the Crisis

Let me start with the numbers because they tell a story that goes beyond statistics.

From Bankrate's 2026 Emergency Savings Report (published January 2026; the $1,000-emergency question was surveyed in December 2025):

- 59% of Americans cannot cover a $1,000 emergency without debt

- 24% have zero emergency savings at all

- Only 30% could pay an unexpected $1,000 from savings

- 46% have enough to cover 3 months of expenses

- The median emergency fund balance is $5,000 — down 50% from the previous year

Let that last number sink in. The median person who has an emergency fund has lost half of it in one year.

Why does this matter to you? Because it means the financial system assumes you're trapped. Credit card companies are profitable because they're betting you'll need to borrow. Banks profit from your crisis. The entire financial infrastructure is built on the assumption that you don't have a safety net.

An emergency fund isn't boring. An emergency fund is freedom.

It's the difference between:

- A car repair that stresses you for a week vs. one that ruins your month

- A medical bill that's inconvenient vs. one that spirals into debt

- A job loss that's scary vs. one that forces you into desperation

Why Americans Are Raiding Emergency Funds: The Perfect Storm of 2026

The emergency fund crisis isn't random. It's structural.

The Inflation Trap

54% of Americans cite inflation and rising costs as reasons for depleting savings. This isn't lifestyle inflation. This is survival inflation.

Since December 2019, prices have climbed 26% without proportional wage growth. That $10,000 emergency fund you built in 2020? It has the purchasing power of about $8,500 today.

Meanwhile, the median emergency fund balance dropped 50% year-over-year. People aren't choosing to save less. They're being forced to spend what they saved just to keep up with daily expenses.

The Medical Debt Crisis

Here's something nobody talks about enough: 100 million Americans owe $220 billion in medical debt.

One hospital stay. One surgery. One emergency room visit that your insurance doesn't fully cover — and suddenly you're using your emergency fund to pay the bill instead of saving it.

The average family with employer health coverage is facing $8,500–$10,000 in annual premiums. That's before deductibles. Before unexpected procedures.

50% of American adults can't pay an unexpected $500 medical bill out of pocket. Not because they're irresponsible. Because the healthcare system is structured to create debt.

The Credit Card Debt Spiral

Here's the brutal part: 29% of Americans have more credit card debt than emergency savings heading into 2026.

They're not choosing credit card debt over emergency funds. The emergency happened, the emergency fund wasn't big enough, so they put the rest on plastic. Now they're servicing 20%+ interest on their emergency while trying to rebuild savings.

It's a trap designed by interest rates.

The Hidden Psychological Cost: Emergency Fund Shame and Financial Anxiety

This is the part of the crisis that numbers don't capture.

70% of Americans report financial anxiety. But 76% feel isolated in their struggles, as if they're the only ones without a safety net.

When you don't have an emergency fund, you internalize that as personal failure. You think: "Everyone else has this figured out. Why can't I?"

But you're not alone. Nearly 6 in 10 people are in the same position.

The psychological weight of living without a buffer is heavy. You can't sleep as well. You can't take career risks. You can't say no to a bad job because you're one emergency away from disaster.

That psychological cost is real wealth destruction. It affects your mental health, your decision-making, and your ability to think strategically about money.

Research shows that financial anxiety actually prevents people from building wealth. The stress makes you less rational. It makes you more likely to make impulsive decisions. It makes you less likely to invest or plan long-term.

An emergency fund doesn't just protect you financially. It protects your mental health. And that's worth more than the numbers suggest.

How Much Emergency Fund Do You Actually Need? (The Real Answer)

Here's where conventional wisdom gets it wrong.

You've probably heard: "Build 3-6 months of expenses."

That's not bad advice, but it's incomplete. It doesn't account for your actual risk.

Dave Ramsey recommends 6 months of expenses. Ramit Sethi recommends up to 12 months. Suze Orman says 8-12 months.

They're all right, and they're all wrong — because the right number depends on you, not on a universal rule.

The Real Framework: Calculate Your Emergency Fund Amount by Age and Risk

Step 1: What are your monthly expenses?

Not your income. Not what you spend on extras. Your actual monthly expenses: rent/mortgage, utilities, food, insurance, transportation, minimum debt payments.

Let's say it's $3,000/month.

Step 2: Assess your job security.

- Stable career, in-demand skills: 3-4 months

- Some volatility (freelance, commission, small business): 6-9 months

- High volatility (contract work, gig economy, startup): 9-12 months

Step 3: Factor in health and dependents.

- Single, healthy, no dependents: Lower end of your range

- Chronic health conditions or dependents: Upper end of your range

Step 4: Calculate your target

Example: $3,000/month × 6 months = $18,000

That's your target emergency fund. It's your financial peace of mind.

For someone making $60,000/year, that's not tiny, but it's achievable in 2-3 years of focused saving.

The real answer is this: your emergency fund should be enough that you can breathe if something goes wrong. If that's $5,000, it's $5,000. If it's $25,000, it's $25,000.

The number doesn't matter. The security does.

The High-Yield Savings + Emergency Fund Hack: Make Your Buffer Earn in 2026

Here's something that infuriates me: people keep their emergency funds in checking accounts earning 0.01% APY.

That's leaving money on the table.

The Math Is Ridiculous

High-yield savings accounts are currently earning 4-5% APY (as of April 2026):

- Varo Money: Up to 5.00% APY

- Axos Bank: Up to 4.21% APY

- Wealthfront: Up to 4.20% APY

Compare that to the national average checking account at 0.39% APY.

On a $10,000 emergency fund:

- Traditional bank: $39/year

- High-yield savings: $400-500/year

That's $361–461 per year doing absolutely nothing. No additional risk. No additional work. Just moving your money.

For someone who builds their emergency fund over two years, getting to $10,000:

Year 1: $5,000 earning 4.5% = $225 interest Year 2: $10,000 earning 4.5% = $450 interest

You literally earn back the interest costs while building the fund.

Why This Matters

Emergency funds are supposed to be boring. Safe. Accessible.

High-yield savings accounts are all three, plus they earn interest while you're not using them.

When an emergency happens and you need to tap the fund, you're not losing months of interest. You're tapping into money that was already working for you.

This is a no-brainer optimization that most people don't do.

Building Your Emergency Fund From Zero: A No-Shame Roadmap (Even If You're Broke)

Okay, you're starting from zero. Or close to it. Maybe you have $200. Maybe you have $0.

The goal isn't to judge yourself. The goal is to build momentum.

Stage 1: The First $500 (Psychological Win)

This is your "system is working" milestone. It's not a full emergency fund. It's proof that you can save.

Where it goes: High-yield savings account. This is non-negotiable. Moving your money to an HYSA makes it feel real.

How long: Depends on your situation. If you earn $2,000/month and can spare $100, that's 5 months. If you can spare $20, that's 25 months.

The timeline doesn't matter. Consistency does.

How to find the money:

- Cut one subscription ($10-15)

- Reduce one category by 10% (dining, entertainment, groceries)

- Add one small side income ($200-500)

- Redirect a tax refund

- Skip one major purchase

Once you hit $500, celebrate. Tell someone. Let yourself feel the momentum.

Stage 2: The First $1,000 (Crisis Buffer)

This is your "I can handle a car repair or minor emergency" fund.

Time to get here: Another 5 months at $100/month, or whatever pace you set in Stage 1.

Why this matters: At $1,000, you're no longer helpless. You're no longer forced to use credit cards for a medical bill or a broken phone.

This is the first real taste of financial breathing room.

Stage 3: 1 Month of Expenses (Real Safety)

Once you know your monthly expenses, your next target is 1 month worth.

If you spend $2,500/month, that's $2,500. If you spend $4,000, that's $4,000.

What this does: It means if you lose your job, you have 30 days to find a new one without panic. That 30 days changes your negotiating power. It changes the job you'll accept.

Time to get here: 6-12 months from Stage 2, depending on your savings rate.

Stage 4: 3 Months of Expenses (Peace of Mind)

This is the "I'm getting serious" milestone.

You can handle a job loss. A major car repair. A health issue. Multiple emergencies in the same year.

Time to get here: 6-18 months from Stage 3.

By now you've been building for 1-2 years. The momentum is real.

Stage 5: 6 Months of Expenses (The Goal)

This is where most financial advisors recommend you land. Full breathing room. Real security.

Time to get here: 6-12 months from 3 months.

The timeline: If you start from zero and save $200/month, you hit 6 months of expenses in 18-24 months. If you save $500/month, you get there in 12-15 months.

That's not forever. That's the next year or two of disciplined action.

The Automation Secret

Here's what makes it actually work: automation.

The best emergency fund is one you don't think about.

Set up an automatic transfer the day after payday:

- To your high-yield savings account

- A small amount you won't miss ($50-200)

- Every single month

You'll be shocked how quickly it grows when you're not watching.

Emergency Fund vs. Investing: The False Choice (And Why FIRE Folk Get This Wrong)

Here's the tension that confuses a lot of people:

"Should I build an emergency fund or should I invest? The stock market returns 10% annually. An emergency fund earns 4.5%. Why would I choose the lower return?"

The person asking this question is making a logical error.

The False Choice

You're comparing:

- Emergency fund: guaranteed 4.5%, absolute safety, no risk

- Stock market: average 10%, but sometimes -30%, requires 20+ years for reliability

That's not a fair comparison because they're serving different purposes.

An emergency fund is insurance. It's not an investment. It's protection against forced selling.

Here's the hidden math that most people don't see:

If you have an emergency fund, you can invest aggressively. You can handle a market crash because you're not forced to sell.

But if you don't have an emergency fund and the market drops 30%, what happens? You panic. You sell at the bottom. You turn a paper loss into a permanent loss.

The person without an emergency fund who invests might have a higher average return on paper. But they actually end up with less money because they sell at the worst time.

The Real Framework

Think of your financial strategy in layers:

Layer 1 (Foundation): Emergency Fund (3-6 months of expenses)

- Absolute safety, HYSA, non-negotiable

- This enables everything else

Layer 2 (Growth): Retirement Accounts (401k, IRA, tax-advantaged)

- Medium risk, long-term, tax benefits

- Max out the match first

Layer 3 (Acceleration): Taxable Investments (brokerage accounts)

- Full market exposure, for wealth beyond retirement needs

- Build this only after Layers 1-2 are solid

Most people try to build Layer 3 before Layer 1 is done. Then an emergency happens, they raid their investments, and they're back to square one.

The FIRE Perspective

If you're working toward FIRE (financial independence), an emergency fund is even more critical.

Here's why: FIRE requires discipline and consistency over 15-20 years. One financial shock — unexpected medical bill, job loss, car replacement — can derail that entire timeline.

An emergency fund removes the possibility of a derailment.

You won't need to tap your investments. You won't need to change your plan. You just tap the buffer and keep moving forward.

That consistency compounds into freedom.

I've seen too many FIRE-focused people skip the emergency fund to be aggressive about investing. Then something breaks, they raid their portfolio, and they lose 3-5 years of progress because they had to restart.

Build the emergency fund first. Then invest like your life depends on it. That's the winning strategy.

The Gen Z Exception: Why Young Adults Are Winning at Emergency Funds

Here's something hopeful in the data: Gen Z (ages 18-24) is actually winning.

65% of Gen Zers have emergency savings. That's the highest of any age group.

Meanwhile:

- Millennials (25-34): 40% comfortable with savings

- Gen X: 31% comfortable (the least comfortable)

- Boomers: Have higher median balances ($2,000+)

Why is Gen Z ahead? I think it's a combination of factors:

-

They grew up during the 2008 financial crisis. They saw their parents' financial insecurity. It's baked into their expectations.

-

Social media and peer accountability. The "loud budgeting" movement is real for Gen Z. They talk openly about savings goals in ways older generations didn't.

-

Financial literacy access. Gen Z has access to free financial education (YouTube, TikTok, blogs) that earlier generations didn't have.

-

FIRE movement adoption. Gen Z is building emergency funds not as a burden but as a step toward independence.

The median emergency fund balance for a Gen Z saver is only $400 (vs. $5,000+ for older generations), but the percentage with savings is highest.

They're starting earlier. And starting earlier, with compound interest, wins.

If you're Gen Z: keep doing what you're doing. If you're older: Gen Z isn't smarter or more disciplined. They're just starting a habit earlier. You can start the same habit today.

Track and Rebuild: Using MFFT to Monitor Your Emergency Fund Progress

Here's where tracking becomes powerful.

Most people build emergency funds in a void. They don't see progress. They don't celebrate milestones. So they quit.

My Financial Freedom Tracker (MFFT) changes this by making your emergency fund progress visible.

How it works:

1. Set a Goal

- Define your target (3 months, 6 months, specific dollar amount)

- Track in a dedicated "emergency fund" goal category

- MFFT calculates how far you are from the target

2. Watch It Grow

- Every deposit updates your progress

- Visual progress bar shows movement toward your goal

- You see the compound interest being added (from the HYSA)

3. Celebrate Milestones

- Hit $500? MFFT notices.

- Hit your 3-month target? Celebration moment.

- These psychological wins keep you motivated.

4. Understand Tradeoffs

- See how increasing your emergency fund competes with other goals

- Decide: Do I prioritize emergency fund or investing this month?

- Make intentional choices instead of random ones

The difference between an emergency fund you never see growing and one you watch grow is the difference between a habit that sticks and one that fails.

Visibility drives behavior. Behavior drives results.

The Bottom Line: Your Emergency Fund Is Your FIRE Foundation

Let me connect this to the larger picture.

If you're interested in financial independence, wealth building, or early retirement, an emergency fund isn't optional. It's foundational.

It's not exciting. It doesn't get Instagram likes. It doesn't fit the narrative of "get rich quick."

But it's the thing that separates people who reach financial freedom from people who almost reach it and then get knocked back by a single emergency.

The statistics are bleak: 59% can't cover a $1,000 emergency. But that also means 41% can. And you can be in that 41%.

It takes time. It takes discipline. It takes automation and tracking and the willingness to say no to things you want.

But it takes less time than you think.

If you earn $60,000/year and can save $300/month, you hit a 6-month emergency fund ($30,000 in expenses = $15,000 buffer) in about 50 months. That's just over 4 years.

4 years from now, you could have the security that 59% of Americans don't have. You could sleep at night. You could take career risks. You could handle emergencies without going into debt.

That's not small.

Your 7-Day Action Plan

You don't need to be perfect. You just need to start.

Day 1: Calculate your monthly expenses (not budget — actual monthly outflow)

Day 2: Decide your target emergency fund ($500? $1,000? 3 months of expenses?)

Day 3: Open a high-yield savings account or CD ladder earning 4%+

Day 4: Make your first deposit (even $20 counts)

Day 5: Set up automatic monthly transfers (smallest amount that won't break your budget)

Day 6: Track it in MFFT or a spreadsheet so you see the growth

Day 7: Tell someone. Accountability works.

The momentum builds from there.

Conclusion: Your Emergency Fund Is Your Superpower

59% of Americans are one emergency away from financial disaster.

That's not a character flaw. That's a systemic problem. It's inflation outpacing wages. It's healthcare costs. It's a job market that doesn't offer security.

But you don't have to be part of that statistic.

An emergency fund is the single most powerful tool for financial security. It's not flashy. It won't make you rich. But it will make you free.

Free from panic. Free from debt spirals. Free from forced decisions.

And from that freedom, everything else becomes possible.

Start building your emergency fund today. Use MFFT to track progress. Watch it grow. Celebrate milestones.

In 12-24 months, you'll have security. In 3-4 years, you'll have peace of mind.

That's not forever. That's the next few years of intentional action.

The question is: will you start now or will you be part of the 59% next year?

The answer you give yourself today determines the freedom you have (or don't have) in 5 years.

Make it count.

📩 Have questions about building your emergency fund or how to track it? Email me at dennis.vymer@myfinancialfreedomtracker.com.

For better tracking of your emergency fund and overall financial progress, use MFFT's budgeting and goal-tracking dashboard to see exactly how far you've come and how close you are to financial security. Visibility is the first step to building wealth. If you're struggling with debt that prevents saving, learn how to escape the credit card trap — the strategy is similar to building an emergency fund, just in reverse.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.