Should You Own Gold in 2026? How Much Belongs in a Normal Investor's Portfolio

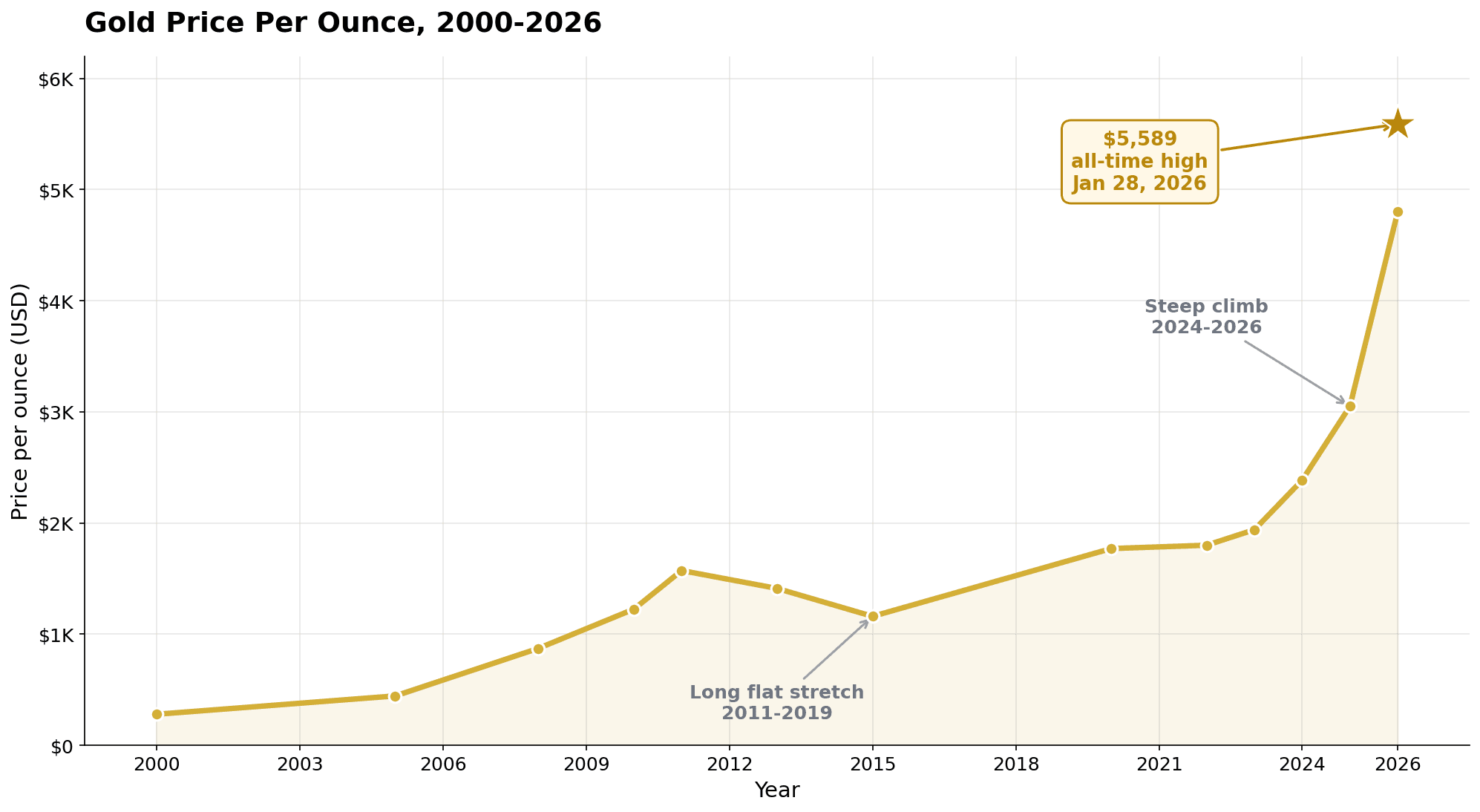

On the morning of January 28, 2026, gold touched $5,589 an ounce — the highest price in human history, after the fastest $1,000 run the metal has ever made. By the time you read this it has cooled to around $4,200, but it's still up roughly 28% over the past year. Suddenly everyone has an opinion: Morgan Stanley is telling clients to put 20% of their portfolio in it, and Reddit can't decide whether you're a genius or a sucker for owning any.

So here's the question I want to answer calmly, with data instead of drama: how much gold should you own — if any — when you're a normal index investor trying to build wealth and maybe retire early? Put differently: what's the right gold portfolio allocation for someone who isn't a trader or a doomsday prepper?

I've watched this movie before — with crypto, with meme stocks, with whatever was hot that quarter. My own rule with crypto is simple and a little blunt: I treat it as money I'm willing to fully lose, so the price swings never run my decisions. I want to bring that same calm to gold — figure out the role it plays before the headline tells me how to feel about it. The headline screams a number, your gut screams fear of missing out, and the worst decisions get made in that gap. This article is the antidote: what's driving the rally, whether gold is really an inflation hedge, the honest allocation range the evidence supports, how to own it without getting fleeced, and the behavioral mistake that turns a diversifier into a regret. No hype, no gold-bug sermons — just arithmetic.

Key takeaways

- Gold is a diversifier, not a core holding — it produces no dividends, interest, or earnings.

- 5-10% is the mainstream sweet spot; 0% is completely defensible if you're young and long-horizon, 10-15% reasonable near retirement.

- Gold is a terrible short-term inflation hedge but a real multi-decade store of value (it spent 27 years underwater after its 1980 peak).

- Hold it via a low-cost gold ETF inside a tax-sheltered account to dodge the 28% collectibles tax rate.

- The real edge isn't the metal — it's deciding your number in advance and rebalancing, not chasing the run-up.

Gold Just Had Its Most Dramatic Year in Decades

Let's start with the numbers — they're staggering, and they explain the noise.

In calendar year 2025, gold rose roughly +65% (Visual Capitalist annual-returns data) — its best year since 1979 — then spiked to that $5,589 all-time high in late January 2026 before retracing. Over the trailing twelve months it's up about 28%, quietly outrunning the S&P 500.

The demand side is just as wild: total gold demand in Q1 2026 hit a record $193 billion, up 74% from a year earlier. (Gold trades by the troy ounce — about 31 grams.)

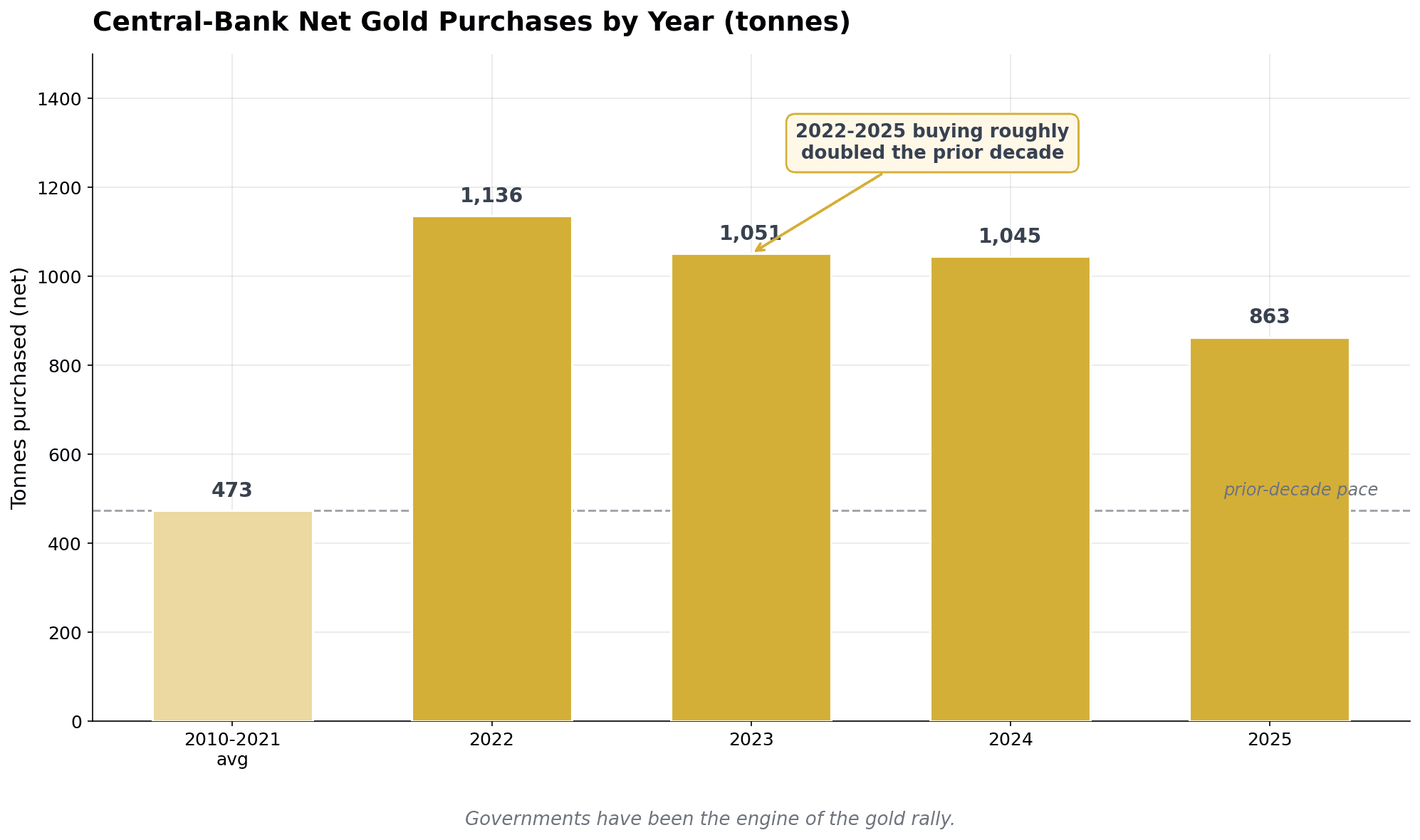

But the most important buyer isn't retail or even Wall Street — it's governments. Central banks bought a net 244 tonnes in Q1 2026 alone and added around 863 tonnes across 2025 — roughly double their average pace in the 2010s (World Gold Council). The buying isn't a straight line — the WGC flagged a visible uptick in selling early in 2026 — but the multi-year direction is unmistakable.

When the people who literally print money are stockpiling gold, everyone else pays attention.

Why Gold Is Suddenly Everywhere: The 2026 Drivers

A rally this big usually has one cause. This one had three, all pushing the same way — which is why it felt structural.

Driver 1: Central banks are diversifying away from the dollar. The dollar's share of global central-bank reserves has slipped to around 56-58%, down from over 70% in 1999 (IMF COFER). After watching reserves get frozen in recent conflicts, many decided gold — which no foreign government can switch off — looks safer than another country's currency.

Driver 2: Investors piled into gold ETFs. A gold ETF (exchange-traded fund) holds real gold and trades like a share. January 2026 set a single-month record with $18.7 billion of inflows; 2025 saw the largest annual ETF inflows ever, around $89 billion (World Gold Council ETF flows).

Driver 3: Inflation and currency-debasement nerves. With government debt mountains everywhere and the post-pandemic price surge still fresh, plenty of people see gold as insurance against a currency slowly losing value — the deeper story is in my explainer on inflation, the silent wealth killer. J.P. Morgan's base case is roughly $6,000/oz by the end of 2026. I'd take any precise price target — up or down — with a large grain of salt; the same banks were quiet at $2,000 and loud at $5,000. I care less about where someone says gold is going and more about what role, if any, it should play in a plan I can actually stick to.

A quieter fourth driver: when a handful of giant AI names drive most of the index's gains, some investors want ballast. I dug into that fragility in the Magnificent Seven and the AI bubble — gold's popularity is partly a hedge against it.

The Honest Answer: Is Gold Actually an Inflation Hedge?

Here's where I break some bad news. This is the claim gold gets sold on more than any other — and it's only half true.

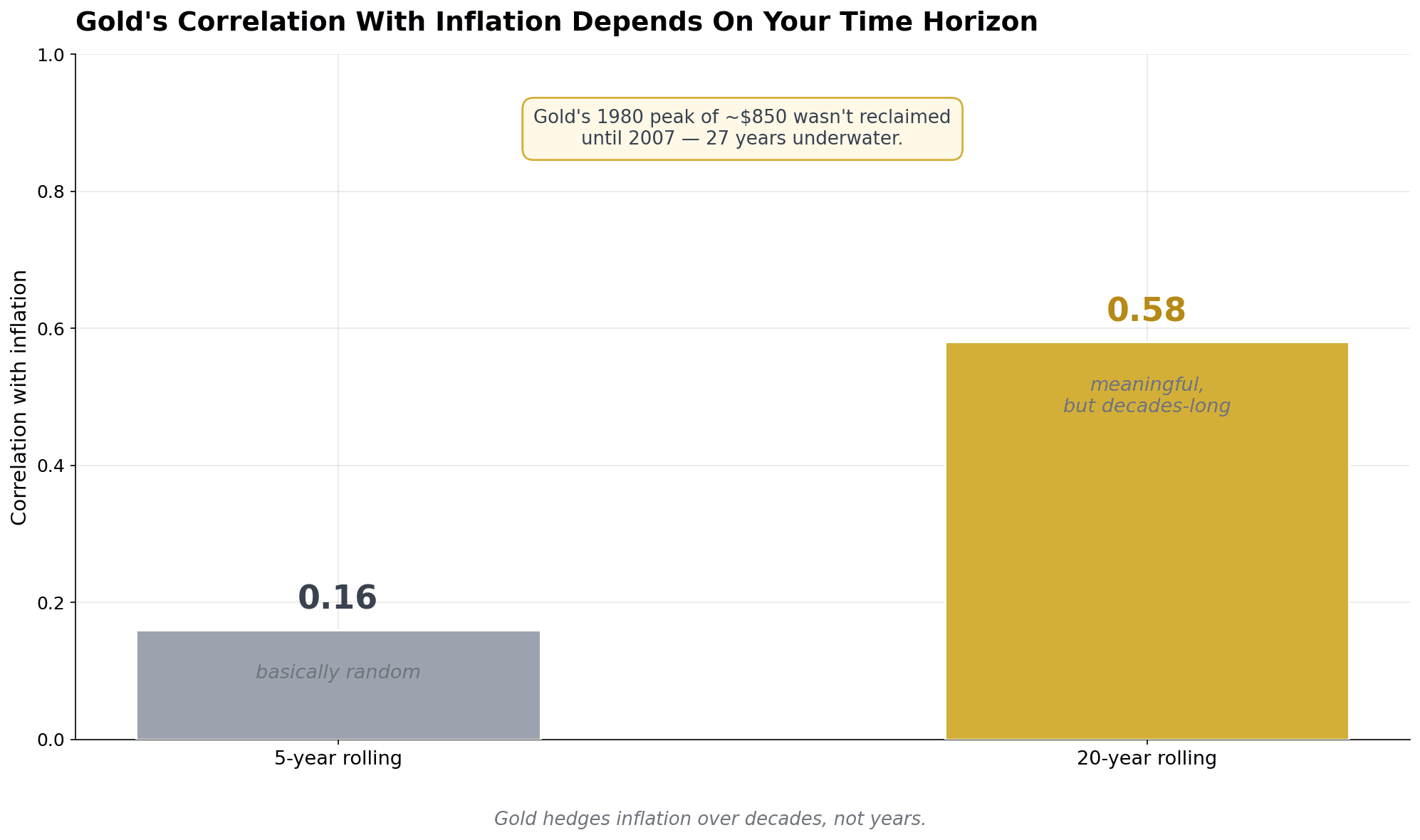

Yes, over very long stretches, gold has roughly kept pace with the cost of living: from 1971 to 2023 it compounded at about 8% a year against U.S. inflation near 4%. Across a lifetime, it has preserved purchasing power. That's real, and it matters.

But here's the part the sales pitch skips: gold is a terrible short-term inflation hedge. Its correlation with inflation is only about 0.16 over rolling five-year periods — close to random — tightening to roughly 0.58 over twenty-year windows (CFA Institute / LBMA data). Gold's inflation protection is a multi-decade promise, not a year-to-year one, and it can lag rising prices for a decade or more.

Gold hit about $850 an ounce in January 1980, then entered a brutal drought — near $270 by 2000, and it didn't reclaim that 1980 high until February 2007. Anyone who bought gold "to beat inflation" in 1980 spent 27 years underwater. That's the best rebuttal to "gold always protects you."

So set expectations honestly: gold is a long-horizon store of value that tests your patience — not a shield against next year's grocery bill.

What Gold Does in a Portfolio (and What It Doesn't)

If gold isn't a dependable inflation hedge, why own any? Its real job is diversification: gold tends to have low or even negative correlation with stocks and bonds, so it often holds up — or rises — exactly when your other assets are falling. That ballast cushions the blow in a crash. It's portfolio insurance, not a growth engine.

And you have to be clear-eyed about the trade-off — it's the heart of the skeptic's case. Gold produces nothing — no dividends, no interest, no earnings. A stock pays you to own it, a bond pays interest, a rental pays rent. Gold just sits there.

Warren Buffett has hammered this for decades, calling gold one of the "assets that will never produce anything" — you only profit if someone later wants it more than you did. The Bogleheads, the index community built around Jack Bogle's philosophy, agree: the classic three-fund portfolio holds zero gold, on the logic that swapping any of stocks, bonds, or international for gold tends to lower long-run returns.

They're not wrong. Over the 30 years through late 2025, the S&P 500 compounded at about 10.7% a year versus gold's 8% (Visual Capitalist), and stocks have beaten gold in most years since the mid-1970s. If your horizon is decades and your stomach is strong, a 0% gold allocation is completely defensible.

So why land above zero? Because "stocks win on average" hides terrifying stretches — like the lost decade for U.S. equities in the 2000s — where a little gold would have saved your sanity. Gold is the asset you hope you never need: a satellite, never the core.

How Much Gold Should You Own? Setting Your Gold Portfolio Allocation

Here's the question you came for. The honest answer is a range, not a magic number — it depends on who you are. Here are the camps, from skeptic to true believer:

| Allocation | Who recommends it | What it means |

|---|---|---|

| 0% | Bogleheads, Buffett | "Gold produces nothing; I'll take equities and bonds." |

| 2-5% | BlackRock's allocation team | A small dusting of insurance. |

| 5-10% | Most advisors, World Gold Council | The mainstream "diversifier" sweet spot. |

| 10-15% | Ray Dalio | "A well-diversified portfolio has 10-15% in gold." |

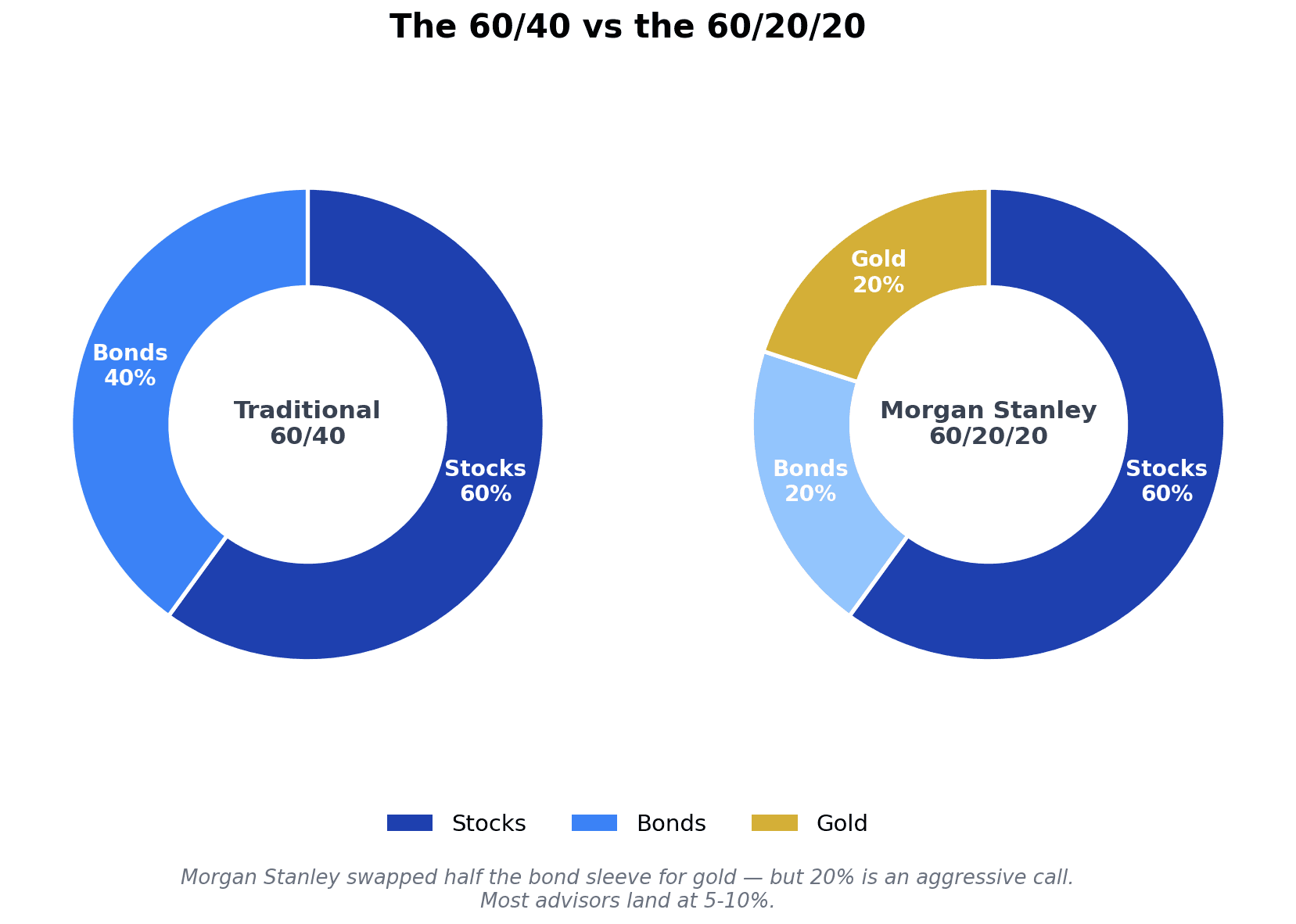

| 20% | Morgan Stanley (60/20/20) | Gold as a co-anchor, replacing half your bonds. |

| 25% | Harry Browne's Permanent Portfolio | Equal-weight bet across four assets. |

The center of gravity in that table — and the figure I'd anchor to for a normal investor — is 5-10%. Below that you barely move the needle; above it you're betting gold will outperform, not just diversify. Morgan Stanley's headline 60/20/20 swaps half the classic 60/40's bonds for 20% gold — striking, but a minority view; that's a lot to bet on something that pays nothing.

For what it's worth, my own portfolio sits at the low end of that range. I'm a simplicity person — a couple of low-cost global ETFs do most of the heavy lifting, and I'd rather not add a second moving part I have to babysit unless it clearly earns its place. So I treat gold as a small, optional dusting of insurance, not a pillar. That's my bias talking, not gospel — if a larger sleeve genuinely helps you stay invested through a crash, that's a perfectly good reason to hold more.

Here's a simple framework to pick your number:

- Young, long horizon, high risk tolerance: 0-5%. Time is your hedge. You can skip gold entirely and put that energy into a low-cost global stock fund — the core that gold would, at most, merely complement. (Here's my breakdown of the best world ETFs.)

- Mid-career, balancing growth and protection: 5-10%, the classic diversifier band.

- Near or in retirement, worried about a bad early market: 10-15%, where gold earns its keep as a sequence-of-returns cushion.

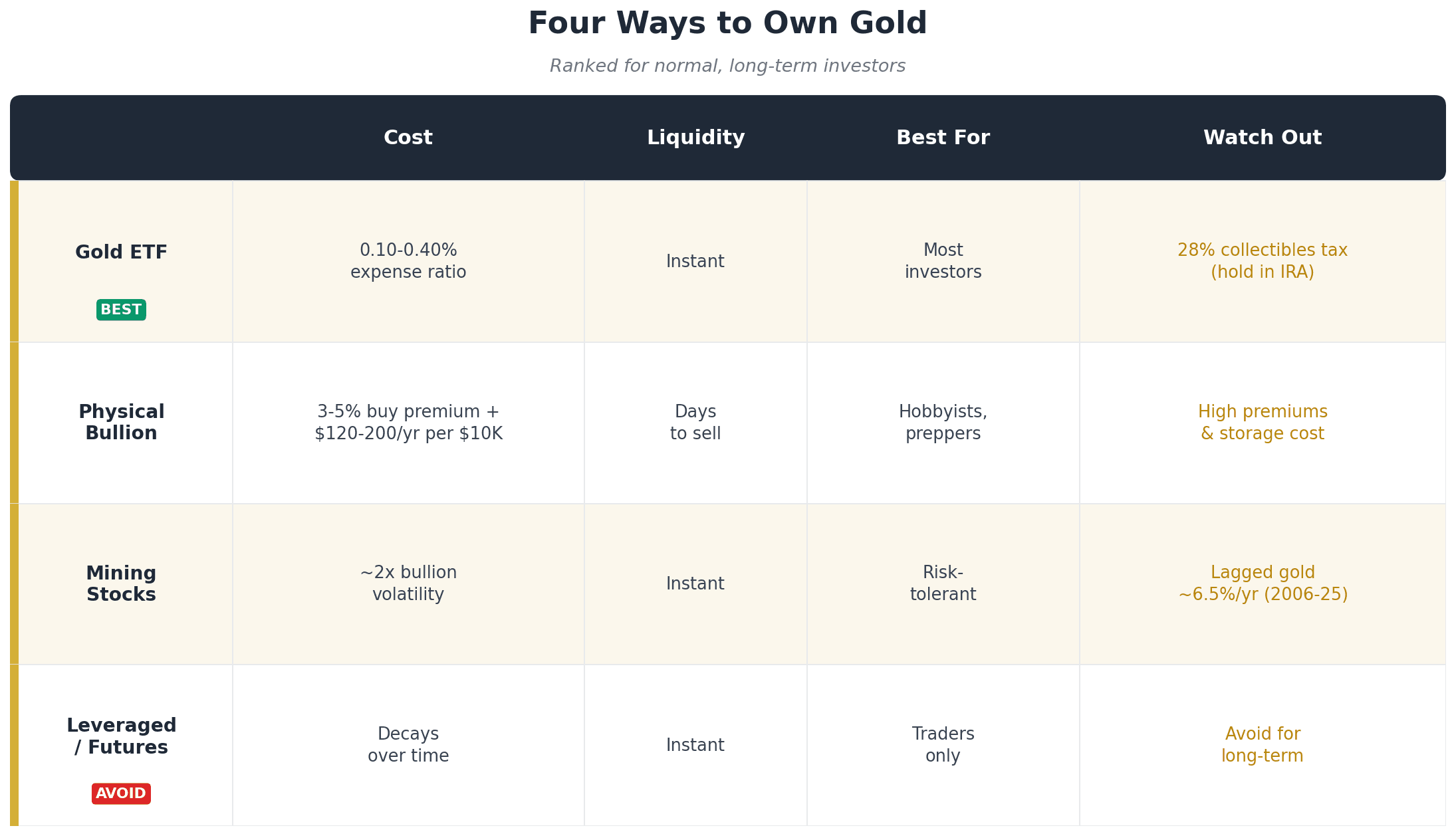

Four Ways to Own Gold (Ranked for Normal Investors)

Decided on a number? How you hold gold matters almost as much; some routes quietly bleed you with fees, spreads, and taxes.

1. Gold ETFs — the default for most people. A gold ETF holds real bullion and trades like a stock: lowest-friction, most liquid, tiny fees. Expense ratios run from about 0.10% (GLDM) up to 0.40% (GLD); for a long-term holder the cheaper funds win. One critical tax wrinkle: the IRS taxes physically-backed gold ETFs as collectibles at a top long-term rate of 28% (versus 20% for stocks) — so hold gold in an IRA or Roth if you can.

2. Physical bullion and coins — satisfying, but costly. There's real comfort in holding a coin you own, but the friction is brutal: 3-5% premiums to buy, a 1-3% spread to sell, and $120-200 a year to store and insure every $10,000. Liquidating takes days. For most investors it's a hobby with a return attached, not an efficient way to get exposure.

3. Gold mining stocks and funds — a leveraged bet, not a clean proxy. Miners (or a fund like GDX) give you leverage to the gold price, but also equity risk — management, mining costs, debt. GDX has been roughly twice as volatile as bullion and underperformed it by around 6.5% a year over 2006-2025.

4. Leveraged and futures products — a trap. Anything promising "2x daily gold" or built on futures is built for short-term trading and decays over time. For a long-term investor, the answer is simply a low-cost gold ETF held in a tax-sheltered account — simple, liquid, cheap.

The Mistake Almost Everyone Makes: Chasing the Run-Up

This is the most important section, so slow down. After a 28% year, the most common mistake isn't owning gold or skipping it — it's buying it for the wrong reason at the wrong time. Performance-chasing is hardwired into us: we see something rising, feel the FOMO, and pile in near the top — buying insurance after the fire.

Picture Sarah, 32, with a clean three-fund portfolio. She sees gold up 28% and gets ready to dump in a lump sum. That's textbook chasing — buying a rally that central banks created, not ballast she planned for. If she genuinely wants gold, the disciplined move is to pick a small target (say 5%) and dollar-cost-average in — a fixed amount each month over several months — instead of betting it all at a record high.

The real magic, though, is rebalancing — what separates investors from gamblers. Here's how it works. Say you decide on 7% gold and set a band: trim back if it drifts above ~9% of your portfolio, top up if it falls below ~5%. When gold spiked in January 2026, that rule forced anyone using it to sell into strength and rotate into stocks; when gold lags, it makes you buy cheap. You're mechanically selling high and buying low — the opposite of what panic does.

That discipline is why a volatile, no-yield asset can still improve a portfolio — not because gold rises, but because rebalancing harvests its swings. It's the calm-in-the-chaos principle from what to do when markets crash: the winners set their rules before the emotion hit, then followed them.

Gold vs Bitcoin vs Just Holding Index Funds

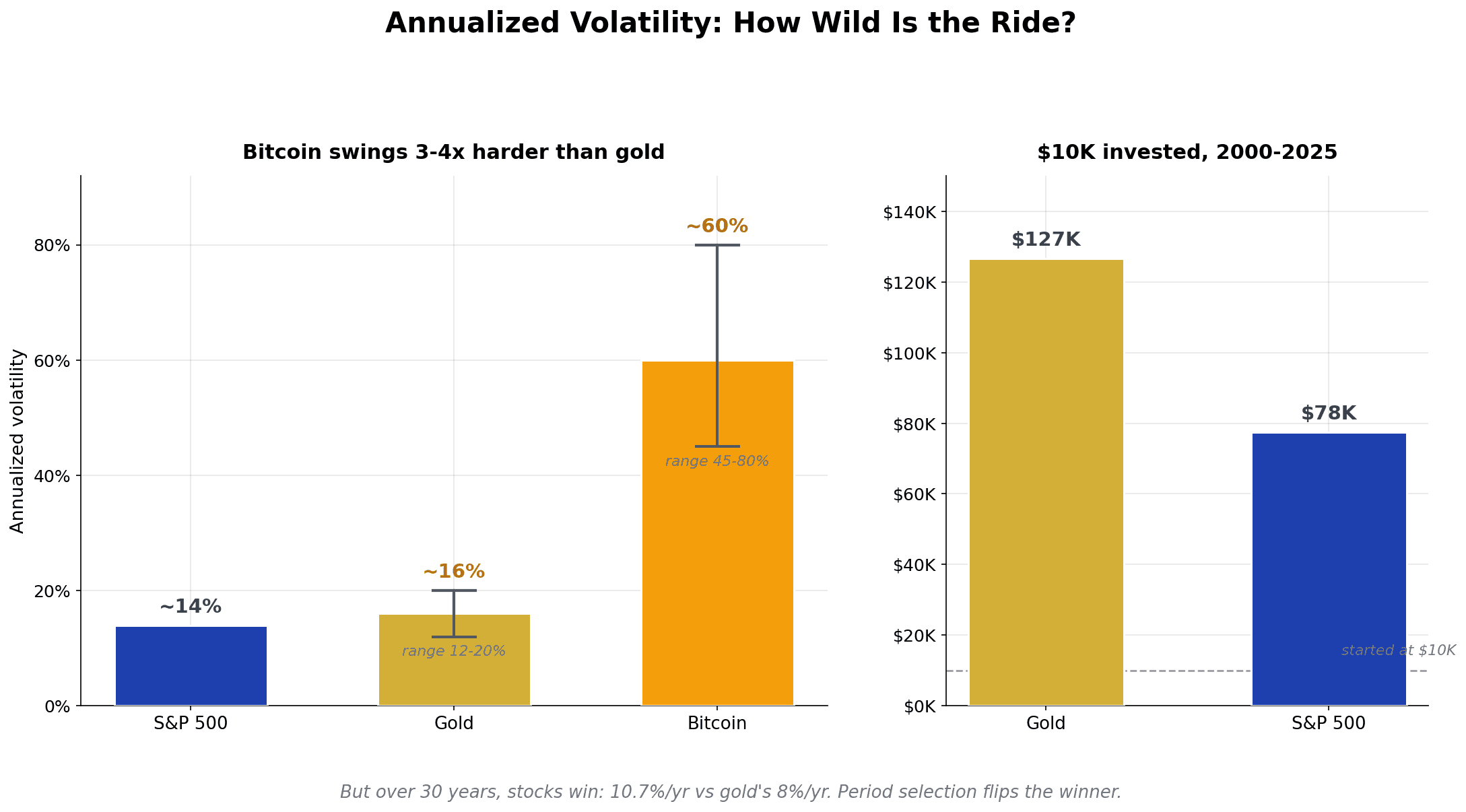

No 2026 gold article is complete without the "digital gold" debate. Bitcoin and gold get pitched as cousins — both "hard money," both scarce, both for currency-debasement worriers. But they behave very differently. Gold's annualized volatility runs around 12-20%; Bitcoin's is 45-80% — three to four times as jumpy. Gold has a multi-millennium track record; Bitcoin has about 15 years, and the two have moved against each other at times, so they're not interchangeable hedges. I went deep on the crypto side in Bitcoin in your 401(k).

I'll be honest about my own bias here. I hold a little crypto, but only with the same loss-it-all rule I mentioned up top — I find it interesting and I understand the appeal, I just don't see the value-add for the boring job of building wealth. Gold at least has a few thousand years of people agreeing it's worth something. But neither one is the engine. For me they sit in the same mental bucket: small, optional, and never allowed to distract from the low-cost index core that's actually doing the compounding.

And the uncomfortable reminder that frames the whole decision: over most long periods, a low-cost global stock index has out-compounded both gold and Bitcoin. Both are optional satellites; a diversified equity portfolio is the core. The 2000-2025 window favored gold ($10,000 grew to ~$126,600 versus ~$77,500 in the S&P 500), but that's an accident of where you start the clock — over 30 years, stocks win comfortably.

So the framing isn't "gold or Bitcoin or stocks." Build your diversified core first, then maybe add a small, deliberate gold sleeve as ballast if it helps you sleep. The hedge is the side dish, never the meal.

Your 2026 Gold Decision Checklist

Here's the checklist I'd give a friend — run through it before you buy a single ounce.

- Is your foundation built first? Emergency fund funded, employer match captured, low-cost index core in place. Gold comes last.

- Have you decided your target percentage in advance? Pick a number in the 0-10% range based on your age and nerves, and write down why — most people land at 5-10%, or 0% if you're young with a strong stomach.

- Did you choose a low-friction vehicle? For nearly everyone, a low-cost gold ETF (GLDM, SGOL, or IAU), ideally inside a tax-advantaged account to dodge the 28% collectibles rate.

- Are you buying gradually, not chasing? Dollar-cost-average over several months rather than lump-summing a record high.

- Have you set a rebalancing band? A target weight plus trim/add triggers, written down before you buy — not improvised mid-spike.

- Did you write down why you own it? So you neither panic-sell the next drawdown nor panic-buy the next record high.

Notice almost every item is about behavior, not gold. The asset is the easy part; discipline is everything.

One last tip before you buy: X-ray what you already own. Plenty of "diversified" investors discover hidden commodity or miner exposure inside their funds. The MFFT portfolio analysis and breakdown tool shows your real, consolidated allocation in one place, so you can slot a gold sleeve into its band and watch it drift instead of guessing.

The Bottom Line on Gold in 2026

So — should you own gold in 2026, and how much gold should you own? Here's my honest, non-dogmatic take.

Gold can be a small, deliberate diversifier — a sensible 5-10% for many investors, 0% completely defensible if you're young and long-horizon, 10-15% reasonable if you're near retirement and want crisis ballast. What it is not: a core holding, a reliable short-term inflation hedge, an income producer, or a substitute for a low-cost global stock portfolio. It lives or dies on price alone — Buffett and the Bogleheads are right about that, even if a modest sleeve still earns its place.

The record price and the 28% run are exactly why you should be more careful, not less. Investors who get hurt chase the headline; those who do well decide their number in advance and let rebalancing harvest the swings.

And if you're young, keep the whole gold question in proportion. The single biggest advantage you have isn't a clever hedge — it's time, and the quiet compounding that comes with it. Honestly, in your twenties the highest-return 'asset' is usually yourself: the skills and earning power you build there tend to pay back many times what any commodity will. Sort that out first, let compounding do the heavy lifting, and gold stays what it should be — a small footnote, not the headline.

Pick your gold portfolio allocation on purpose, hold it cheaply in the right account, and rebalance with discipline. Then get back to the boring, quiet work of building wealth — that's the part that actually gets you free.

One honest disclaimer: I'm a founder and fellow investor sharing what the evidence says, not a licensed financial advisor — nothing here is personalized advice. When in doubt, talk to a professional who can see your full picture.

📩 Weighing a gold sleeve and want a second set of eyes? Email me at dennis.vymer@myfinancialfreedomtracker.com — I read every reply. Decide your number, write down why, then let rebalancing do the talking.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Invest Smart

Invest SmartDo You Actually Know What You Own? This Tool Reveals the Truth About Your Portfolio in 30 Seconds

You bought 3 ETFs and think you're diversified? Think again. Turns out 30% of your money might be sitting in the same 6 stocks — and you had no idea. This tool X-rays your portfolio in 30 seconds, exposes hidden overlaps, and even calculates exactly when you'll be financially free. No sign-up required. Just the truth about what you actually own.

Invest Smart

Invest SmartMagnificent Seven: Will AI Make You Rich, or Are You Buying the Decade's Most Expensive Bubble?

Seven tech giants now drive the entire market, promising an AI revolution that will change the world — but their valuations remind us of 2000. Is this the beginning of a new era, or just an extremely expensive bet on the future? This article breaks down the hard data, historical parallels, and what this debate means for the average investor.

Invest Smart

Invest SmartBest World ETFs (And Why Investing Is Like Marriage)

Choosing an ETF is like choosing a life partner — and most people do it completely wrong. I'll tell you why a "boring" ETF is the best choice and which funds I recommend (I own one of them). Spoiler: sexy investments will ruin you.