Bitcoin in Your 401(k)? What the 2026 DOL Rule Really Means

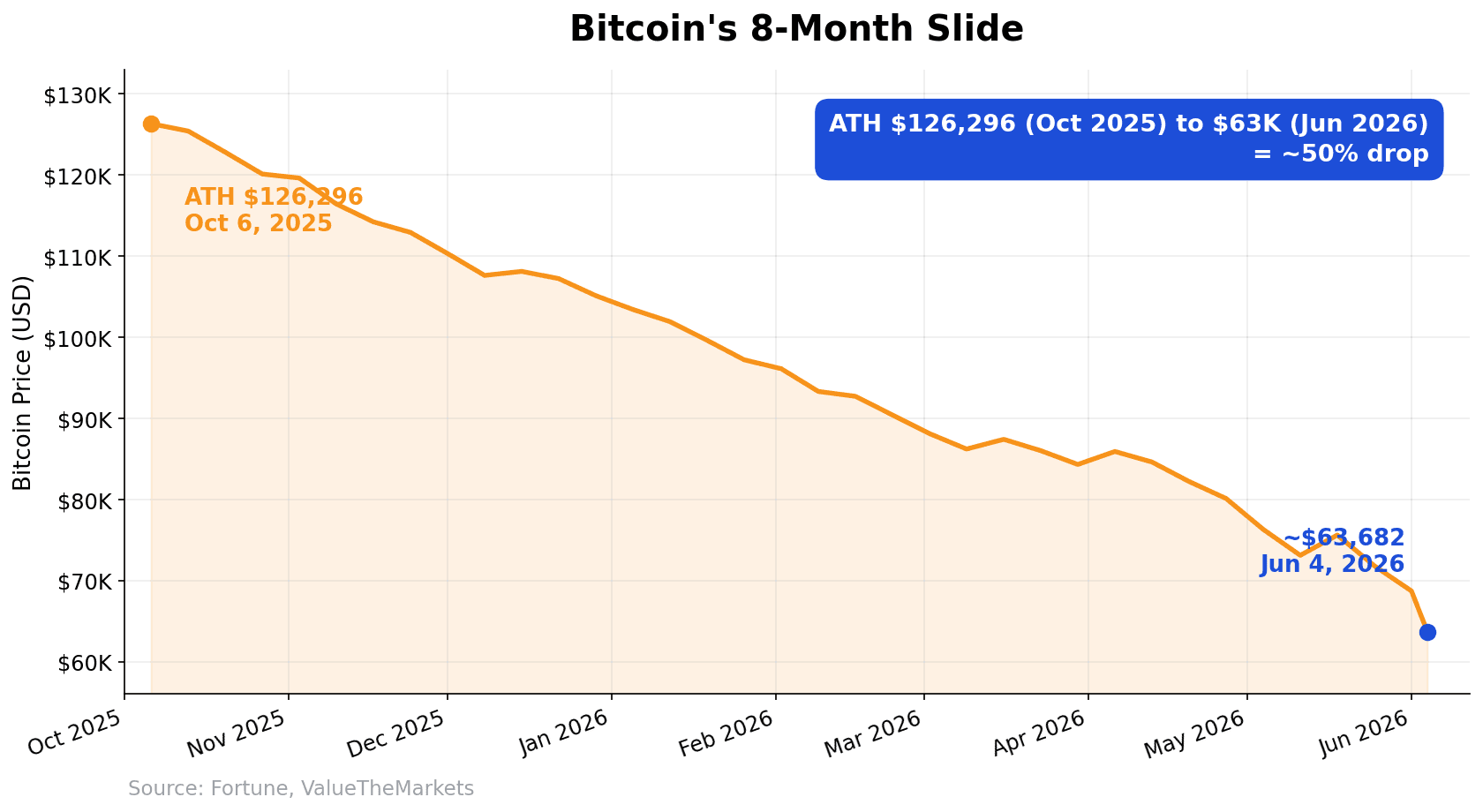

Jake is 58, five years from retirement, and last October he almost did something I would have spent a year talking him out of. Bitcoin had just touched an all-time high of $126,296, the headlines were screaming, and he was eyeing a move of 20% of his 401(k) into crypto. By the time he emailed me this June, Bitcoin was trading near $63,000 — down roughly 50% in eight months. Had he made that move and started drawing on the account, he would have locked in losses he had no time to recover. The question of bitcoin in 401k 2026 plans is suddenly everywhere — so let's slow down and do the math.

That is the story behind every breathless headline about bitcoin in 401k 2026 plans. On March 30, 2026, the Department of Labor proposed a new rule, and within hours half the internet decided "Bitcoin is coming to your 401(k)." That is not actually what the rule does. And the real question is not "can I add crypto to my retirement plan?" — you technically always could. It is "should I, and if so, how much?"

This is the calm, numbers-first version I wish landed in everyone's inbox before they touched the buy button. We will demystify the rule, separate the political noise from the mechanics, walk through the three real ways crypto can enter a retirement plan, and finish with a short checklist for deciding how much, if any, belongs in your plan. No hype. No bashing. Just arithmetic.

The Headline vs the Fine Print: What the 2026 DOL Rule Actually Says

Let's kill the biggest myth first. The DOL did not order anyone to put Bitcoin in your 401(k). Nothing is being auto-added to any plan today.

What the DOL actually published on March 30, 2026 is a proposed "process-based safe harbor" for plan fiduciaries. A fiduciary is the person or company legally responsible for choosing the investment options on your 401(k) menu and acting in your best interest. The proposed rule says that if a fiduciary documents a careful evaluation covering six factors — performance history versus comparable options, total fees and cost transparency, liquidity, valuation method, benchmarking, and how understandable the option is for everyday participants — then their judgment is presumed reasonable.

That's it. The rule protects the employer's decision process, not your savings. It makes it easier for plans to offer alternative assets like crypto, private equity, and real estate. It does not make those assets safer for you to hold.

Here is the part almost nobody mentions: alternative investments were never actually banned from 401(k)s. They have always been technically permissible under ERISA, the federal law governing workplace retirement plans. The 60-day public comment period ran until June 1, 2026, which means this is still a proposal — it could change before it is finalized.

Why This Matters: Trillions in Retirement Money, One Procedural Change

If alternatives were always allowed, why does a procedural tweak make news? Because of fear, and the scale of money behind it.

Back in 2022, the DOL issued guidance telling fiduciaries to use "extreme care" before adding crypto to plan menus. That phrase did real work — employers heard "extreme care" and read "lawsuit risk," and most stayed far away. On May 28, 2025, the DOL rescinded that guidance and returned to a neutral stance, neither endorsing nor disapproving crypto. The March 2026 safe harbor goes one step further by giving employers a documented path to say yes without fear of getting sued.

Now the scale. U.S. 401(k) plans held roughly $9.3 trillion as of mid-2025, with about 70 to 72 million active participants. Total U.S. retirement assets sit near $45.8 trillion. A single change to how comfortable employers feel could cascade across thousands of plan menus.

For perspective, the proven tax-advantaged accounts still move more money than any crypto sleeve will. The HSA as a stealth retirement account is a triple-tax-advantaged vehicle most people underuse, and this year's contribution limits and Roth catch-up rules are where the boring, reliable wins live.

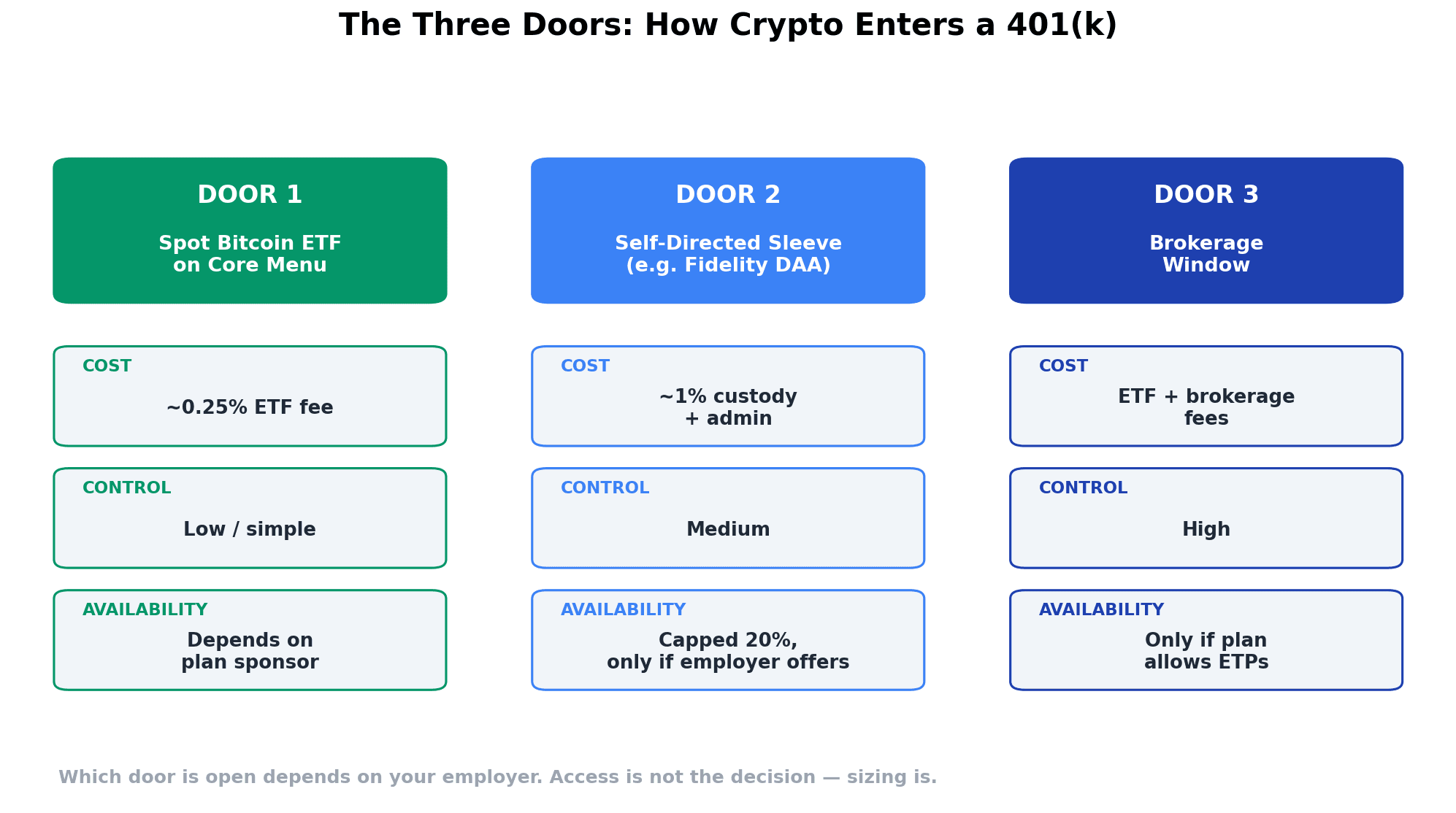

The Three Real Ways to Get Bitcoin in Your 401(k)

When people picture "crypto in 401k," they imagine one thing. There are actually three different doors, with very different costs and control.

Door 1: A spot Bitcoin ETF on the core menu. Your plan sponsor adds a Bitcoin exchange-traded fund as a designated option, right alongside the index funds. A spot Bitcoin ETF holds actual Bitcoin and trades like a stock. This is the simplest route — low effort, ETF-level expense ratio (the iShares Bitcoin Trust, IBIT, charges 0.25%) — but it only exists if your employer chooses to add it.

Door 2: A self-directed or dedicated crypto sleeve. Some providers offer a carved-out account, like Fidelity's Digital Assets Account, which holds Bitcoin plus short-term cash-like investments and caps Bitcoin at no more than 20% of your contributions. More control, more cost — these tend to layer custody and administration fees that can reach around 1% per year.

Door 3: The brokerage window. A self-directed brokerage window lets you buy a wider menu of investments — including Bitcoin ETFs — inside your 401(k). Highest control, but you pay ETF plus brokerage fees, and only if your plan permits exchange-traded products in the window.

The takeaway: which door is even open to you depends entirely on your employer. Access is not the decision. Sizing is.

The Political Fight: Blockchain Association vs Warren and Sanders

This rule did not appear in a vacuum, and the fight around it tells you why the final version could still shift.

The proposal flows from President Trump's August 7, 2025 Executive Order 14330, "Democratizing Access to Alternative Assets for 401(k) Investors," which gave the DOL 180 days to re-examine its guidance. On the for side, BlackRock CEO Larry Fink argues that modernized retirement structures are the main way more Americans — including the roughly 40% with no market exposure — can share in economic growth, and the Blockchain Association says savers should not be blocked from an asset class simply because it is crypto.

On the against side, Senators Elizabeth Warren and Bernie Sanders, with Representative Bobby Scott, sent a June 1, 2026 letter urging the Labor Department to withdraw the rule, arguing it weakens retirement protections and exposes savings to assets that are "riskier, more expensive, and less transparent." The Economic Policy Institute echoes the concern.

Both sides have a point — which is why the safe harbor is ultimately a fight about access and process, while your decision is about position sizing. Different problems.

The Real Risks Nobody Puts in the Brochure

Here is where being honest matters more than being optimistic. Three risks deserve your full attention.

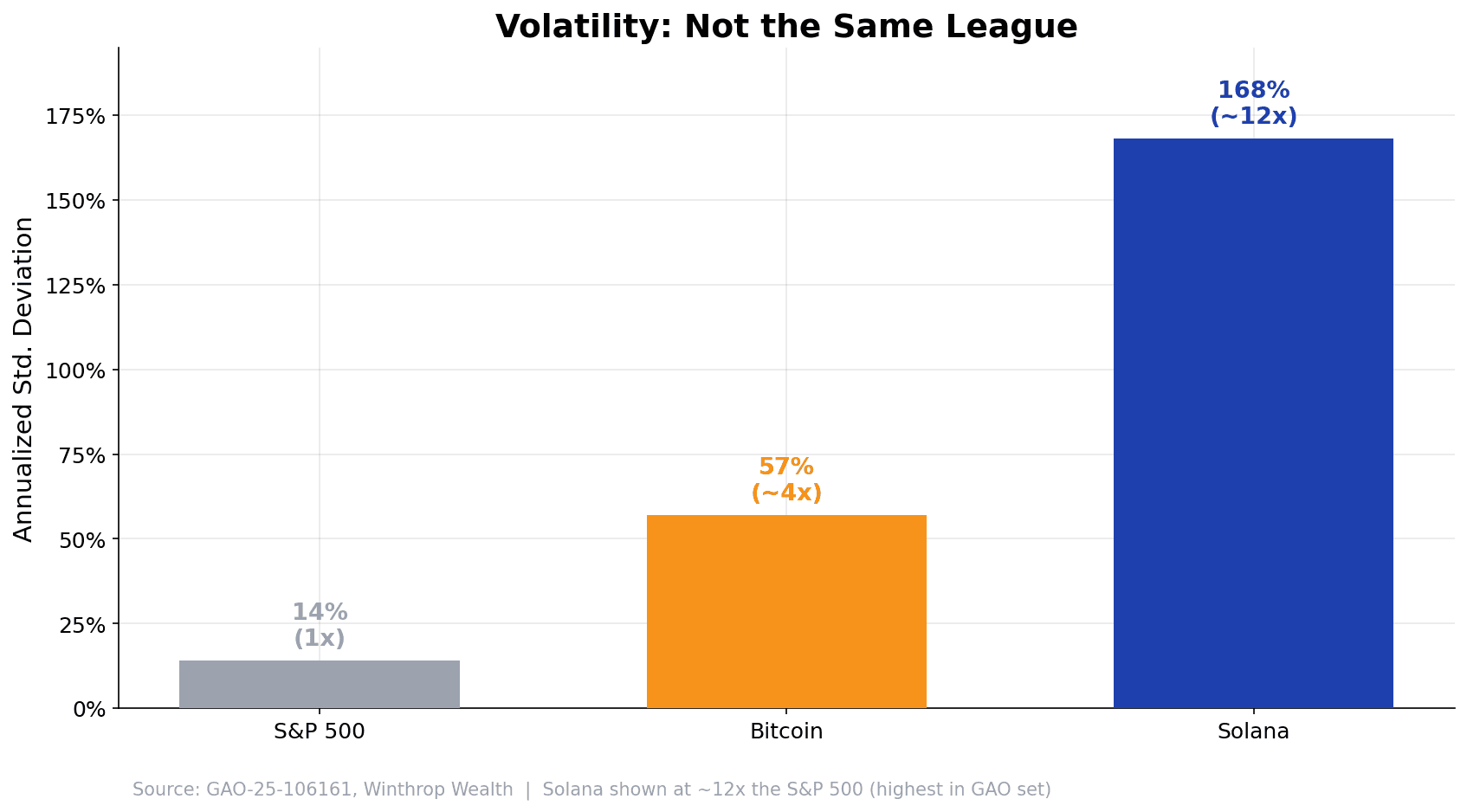

Risk 1: Volatility that is genuinely in a different league. A 2024 GAO study found the crypto assets available to 401(k) plans ranged from 4x as volatile as the S&P 500 (Bitcoin) to 12x (Solana). Bitcoin's annualized standard deviation runs around 54 to 60%, against roughly 13 to 15% for the S&P 500. Crypto has stayed under 1% of all defined-contribution plan investments — for good reason.

Risk 2: Drawdowns that can erase most of your stake. Bitcoin's three largest historical drops average around 80%, with individual crashes hitting 77% (2022), 86% (2018), 85% (2015), and 93.5% (2011). The S&P 500's worst drawdown in that modern era was just under 34%. A 50% slide, like the one we just watched from October 2025 to June 2026, is not an anomaly for Bitcoin. It is Tuesday.

Risk 3: Sequence-of-returns risk for anyone near retirement. This is the one Jake nearly walked into. Sequence-of-returns risk is the danger that a big loss early in retirement — while you are withdrawing — does permanent damage, because you are selling assets at depressed prices and never give them time to recover. Crypto's swings amplify this enormously, and I dug into the mechanics in the sequence-of-returns risk playbook — the key context for anyone within a decade of retirement.

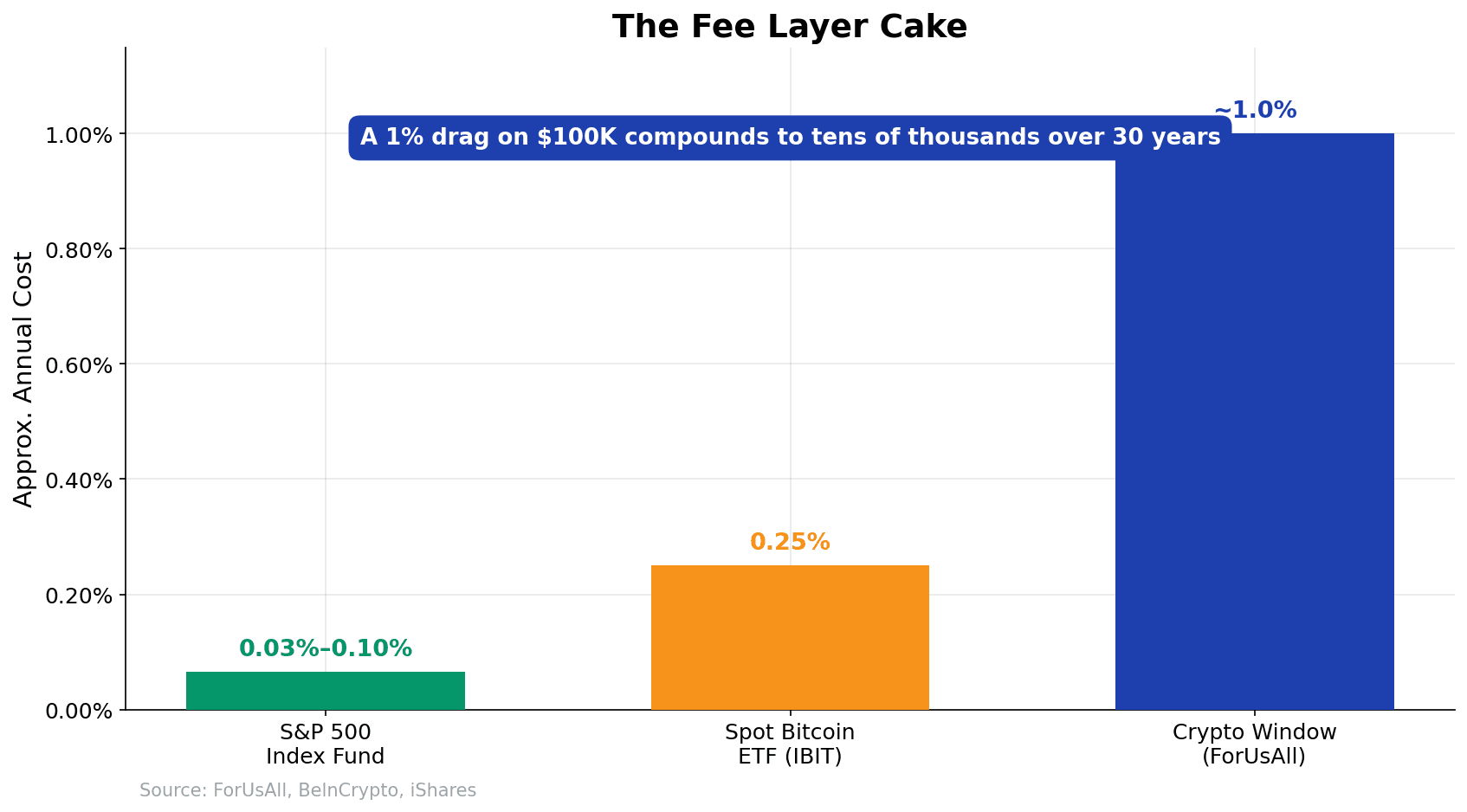

And then there are the fees. A typical S&P 500 index fund in a 401(k) charges 0.03% to 0.10% a year. Crypto options layer custody, administration, and execution costs on top — ForUsAll's crypto window runs about 1% annualized; even a spot Bitcoin ETF like IBIT charges 0.25%. A 1% annual fee difference on a $100,000 balance can quietly erode tens of thousands of dollars over a 30-year career.

The Honest Case For a Small Allocation

I promised balance, so here is the genuine argument for a small sleeve — presented fairly.

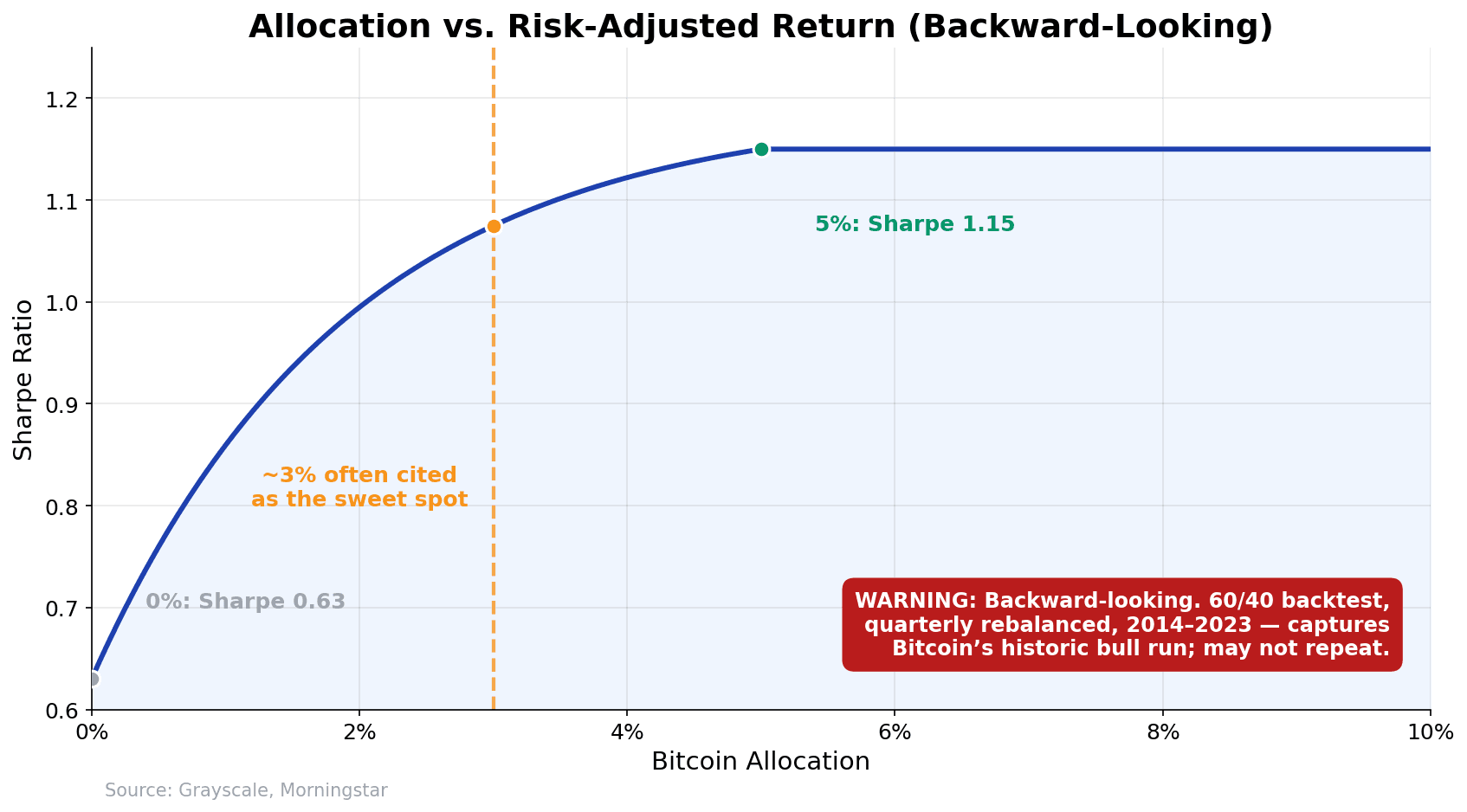

Bitcoin has had a low historical correlation to stocks and bonds, and historically high returns. Combine those and a tiny allocation can, in backtests, improve a portfolio's risk-adjusted return — its Sharpe ratio, which measures return per unit of risk. Research from Grayscale and Morningstar finds the Sharpe ratio tends to rise as a Bitcoin allocation moves from 0% toward roughly 5%, then plateaus, with about 3% often cited as the sweet spot. One industry backtest showed a 5% Bitcoin allocation with quarterly rebalancing lifted a 60/40 portfolio's Sharpe ratio from 0.63 to 1.15 over 2014 to 2023.

There is also the asymmetric-upside argument: you can only lose what you put in, but the upside is uncapped.

Read that backtest with both eyes open, though. It captures Bitcoin's extraordinary historic bull run, and the past does not have to repeat. This is the case for, and even the case for lands on "small." Morgan Stanley's Global Investment Committee and most advisors cap crypto at 5 to 10% of the overall portfolio, and many suggest 1 to 3% for conservative investors. Whatever the number, it sits on top of a boring, diversified core that does the real work — here is a model for the best world ETFs to build that part.

Your Decision Checklist: Should You Put Bitcoin in Your 401(k)?

Run yourself through these seven questions. If you cannot answer "yes" to the first four, the honest answer is "not yet."

- Is your emergency fund fully funded? Speculation comes after safety, never before.

- Are you capturing your full employer match? That match is an instant 50 to 100% return no crypto can promise. Get it first.

- Are your proven tax-advantaged accounts on track? HSA, Roth and traditional 401(k) and IRA, all funded toward your targets.

- Is your time horizon 10-plus years? If you are near or in retirement, sequence risk should pull you toward zero.

- Have you checked the fees? Compare the crypto option's all-in cost against your 0.03 to 0.10% index funds, and accept that the gap compounds.

- Can you stomach an 80% drop without touching your core? If not, the sleeve is too big — shrink it until you can.

- Do you have a rebalancing plan? A target weight and a band, written down before you buy, not improvised during a bull run.

Seven yeses and a 1 to 5% sleeve sized to your age can make sense. Anything less than seven, and the responsible move is to wait and build the foundation.

X-Ray Your True Crypto Exposure With MFFT

One last trap, because it is the one that quietly burns careful people.

Michelle, 41, was about to add Bitcoin to her 401(k). Before she did, she totaled her exposure across every account — and discovered she already owned a spot Bitcoin ETF in her brokerage and held crypto-correlated positions through her employer's stock fund. Across all accounts she was already sitting at 4% crypto. She decided not to add more. The 401(k) addition would have pushed her past her own comfort line without her ever noticing.

That is the real risk for organized savers: not one account, but the total across 401(k), IRA, brokerage ETFs, and employer stock. This is exactly what the MFFT portfolio analysis breakdown tool is built for — it lets you X-ray your real, consolidated crypto exposure so you can keep any allocation inside its target band over time, instead of double-counting or overshooting.

So here is the whole article in one breath. The 2026 DOL rule did not put bitcoin in 401k 2026 menus by force — it gave employers an easier yes, nothing more. Crypto is roughly 4x as volatile as the market, prone to 80% drawdowns, fee-heavy inside plans, and especially dangerous near retirement. If you still want in, the disciplined answer is a small, intentional, optional sleeve of 1 to 5%, funded only after the boring wins are locked, sized down by age, and rebalanced with bands. Access is not the decision. Position sizing is.

If you are weighing this for your own plan and want a second set of eyes, email me at dennis.vymer@myfinancialfreedomtracker.com — I read every reply. And before you touch the buy button, X-ray your total exposure first. Most people are more invested than they think.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Learn To Invest

Learn To InvestLump Sum vs Dollar-Cost Averaging: What I Did With a Windfall in 2026

I had a lump sum and the market was at its 24th record high of 2026, so I froze for six weeks. Here's what the data actually says about lump sum vs dollar-cost averaging, and why the entry method matters far less than whether you press the button at all.

Learn To Invest

Learn To InvestTrump Accounts 2026: Turn the $1,000 Baby Bonus Into $191,000 by Age 18

Trump Accounts 2026 launch July 4 with a free $1,000 seed for every U.S. newborn. The math: maxed out, $191K by age 18 and $2.2M by 60. Plus the IRS Form 4547 walkthrough, three traps, and how it compares to 529s and custodial Roths.

Learn To Invest

Learn To InvestMonthly Dividend Income Strategy: Build Predictable Cash Flow for FIRE in 2026

Monthly dividend income strategy builds predictable cash flow for early retirees, covering 40-60% of living expenses before Social Security while reducing sequence-of-returns risk. Three-tier approach: dividend aristocrats (60%), dividend ETFs like SCHD (25%), and high-yield specialists (15%) generate $1,600-$2,500/month on a $600K portfolio.

Learn To Invest

Learn To InvestHSA Retirement Strategy: The Triple Tax Advantage (2026)

The HSA is America’s only triple-tax-advantaged account. How FIRE savers turn it into a stealth retirement fund — 2026 limits, the receipt hack, 65+ rules.

Learn To Invest

Learn To InvestPay Off Mortgage or Invest? The Math vs. the Psychology

Pay off the mortgage or invest the difference? The math favors stocks; psychology favors the house — homeowner net worth is $400K vs $10K for renters.