What to Do When Markets Crash (And Why Not to Sell)

You open your app, check your investments, and see -20%. Your heart skips a beat. Your mind races:

"I need to sell before I lose everything."

Stop. This is exactly the moment when most people make the biggest financial mistake of their lives.

What Does It Mean When "Markets Crash"?

When we say the "market is crashing," we mean that stock and fund prices are falling. Investors categorize these drops by size:

| Name | Drop | What It Means |

|---|---|---|

| Dip | up to -10% | Normal, happens several times a year |

| Correction | -10% to -20% | Uncomfortable but normal |

| Bear market | -20% or more | Bigger drop, can last months |

| Crash | -30% or more, rapidly | Panic, news about the end of the world |

The important thing to understand:

All of these situations are a normal part of investing. They've always happened and always will.

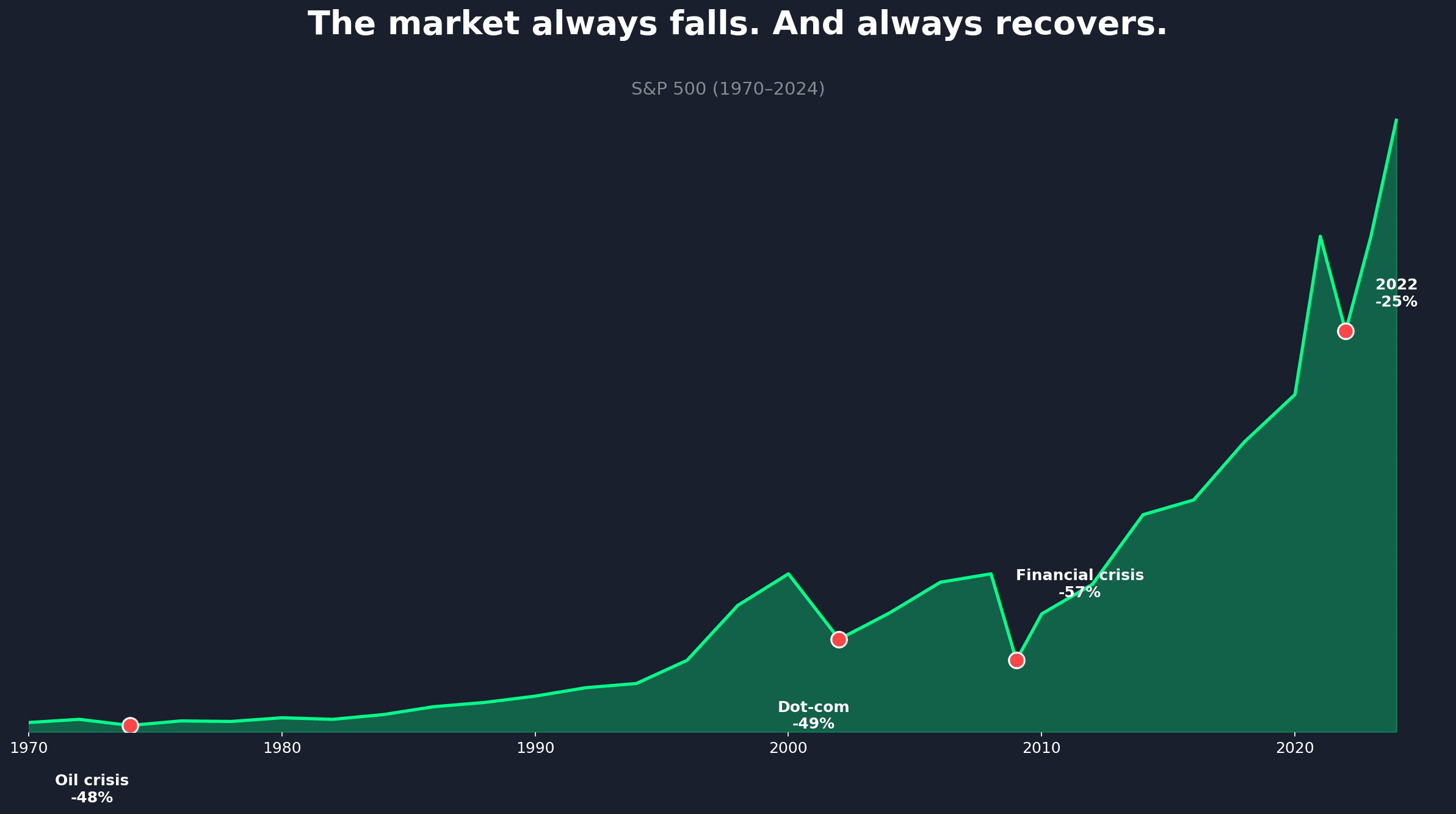

How Often Do Markets Actually Fall?

Look at that chart. Over the past 50 years, the market dropped -48%, -49%, -57%, -34%... And every single time, it recovered and grew even higher.

Drops aren't exceptions. They're a normal part of the game.

When you see -20% on your account, remember this image. The red dot is uncomfortable — but the green line always continues upward.

Why We Feel the Urge to Sell

Our Brain Doesn't Help

Evolution programmed us for survival. When you see danger, your brain triggers the "run!" response.

The problem? Your brain doesn't distinguish between a tiger and a red number in an app. It sees -25% and screams: "Save yourself! Sell!"

Losses Hurt More

Psychologists found that losing $1,000 hurts roughly twice as much as gaining $1,000 feels good. This is called loss aversion — we simply hate losing.

That's why when the market drops 20%, you feel it much more intensely than when it rises 20%. And that's why you have such a strong urge to "stop the pain."

What Happens When You Sell

Example: John and Mike

Both invested $10,000 in an ETF in January 2020. In March, COVID hit and the market dropped 34%. Both saw -$3,400.

John panicked and sold. Mike also didn't feel great, but he did nothing.

End of 2020? John has $6,600. Mike has $11,800.

Same investment, same drop. A $5,200 difference — just because of one decision.

Why Such a Big Difference?

As long as you don't sell, you haven't lost anything. That -$3,400 is just a number on the screen — it's called a paper loss. You still own the same number of shares.

The moment you sell, the paper loss becomes a real loss. The money is gone and won't come back.

Warren Buffett puts it perfectly:

"I lost half only on paper. I didn't sell anything."

What TO DO When Markets Crash

1. Nothing (Seriously)

The best strategy is often to do absolutely nothing.

If you have automatic investing set up, let it run. You're actually buying cheaper now.

2. Close the App

The less you look, the better you sleep. In turbulent times, I recommend checking your portfolio at most once a month.

3. Remember Your Plan

Are you investing for retirement 30 years away? Saving for a house in 10 years?

None of that has changed just because the market dropped this month. Your horizon is years, not days.

4. Maybe Buy More

When something goes on sale and you believe in it long-term, it's an opportunity.

Imagine an iPhone priced at $1,000. Suddenly there's a 30% discount. Do you say "great, I'll buy" or "something's wrong, I'll wait until it gets more expensive"?

With stocks, people do the second thing. Which doesn't make sense.

Conclusion

Crashes are scary. But here's the truth:

The investor's biggest enemy isn't the market crash. It's their own panic.

People who profit long-term aren't the smartest ones. They're the ones who can sit and do nothing while everyone around them is panicking.

When you see red numbers, remember:

- As long as you don't sell, you haven't lost anything

- Markets have always recovered

- Your horizon is years, not days

Then close the app and go live your life.

Have questions? Reach out at dennis.vymer@myfinancialfreedomtracker.com.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Learn To Invest

Learn To InvestLump Sum vs Dollar-Cost Averaging: What I Did With a Windfall in 2026

I had a lump sum and the market was at its 24th record high of 2026, so I froze for six weeks. Here's what the data actually says about lump sum vs dollar-cost averaging, and why the entry method matters far less than whether you press the button at all.

Learn To Invest

Learn To InvestBitcoin in Your 401(k)? What the 2026 DOL Rule Really Means

The 2026 DOL rule doesn’t put Bitcoin in your 401(k) by itself. The real risks, three ways crypto can enter your plan, and how much (if any) to hold.

Learn To Invest

Learn To InvestTrump Accounts 2026: Turn the $1,000 Baby Bonus Into $191,000 by Age 18

Trump Accounts 2026 launch July 4 with a free $1,000 seed for every U.S. newborn. The math: maxed out, $191K by age 18 and $2.2M by 60. Plus the IRS Form 4547 walkthrough, three traps, and how it compares to 529s and custodial Roths.

Learn To Invest

Learn To InvestMonthly Dividend Income Strategy: Build Predictable Cash Flow for FIRE in 2026

Monthly dividend income strategy builds predictable cash flow for early retirees, covering 40-60% of living expenses before Social Security while reducing sequence-of-returns risk. Three-tier approach: dividend aristocrats (60%), dividend ETFs like SCHD (25%), and high-yield specialists (15%) generate $1,600-$2,500/month on a $600K portfolio.

Learn To Invest

Learn To InvestHSA Retirement Strategy: The Triple Tax Advantage (2026)

The HSA is America’s only triple-tax-advantaged account. How FIRE savers turn it into a stealth retirement fund — 2026 limits, the receipt hack, 65+ rules.