How to Start Investing: A Plain-English Beginner’s Guide

You've heard about investing. You know you should probably be doing it. But every time you try to learn, you hit a wall of jargon and complicated advice.

Sound familiar?

Let's fix that — in plain English.

This is the guide for how to start investing as a complete beginner — the basics in simple, human terms. No jargon, no unnecessary complexity. Just what you actually need to know to get started.

What Investing Is NOT

Let's start with the important stuff: investing is not getting rich quick. Don't expect overnight miracles, secret tricks, or "sure tips."

Investing is a long-term game. It requires patience, discipline, and the ability to suppress your ego today so you can enjoy freedom tomorrow. It's not for everyone — but for those who stick with it, it can be extremely rewarding.

So What IS Investing?

Simply put: Investing means buying a piece of something you believe will grow and prosper long-term.

The goal is for your money's value to grow over time — in other words, "making your money work for you."

In the past, this mainly meant individual companies. But today, you have access to a wide range of tools that let you invest:

- around the world (USA, Europe, Asia, the whole globe),

- in various sectors (technology, industry, agriculture, etc.),

- without having to pick anything complicated yourself.

Three Approaches to Investing

Personally, I divide investing into three basic categories:

-

"Better Savings Account" (Passive Investing) Global funds, ETFs (Exchange-Traded Funds — basically baskets of many stocks bundled together), companies with long histories

-

Active Investing - Buying individual company stocks

-

"Gambling" - Crypto and short-term speculation on company rises or falls

Everything has its place, but I personally invest most of my money passively — into the Better Savings Account.

Better Savings Account - Passive Investing

This is the foundation for most of us.

It's about long-term investing (5-10+ years) where you:

- invest regularly (e.g., every month),

- into a broadly diversified, low-risk portfolio,

- without constantly watching news and charts — you basically "forget about it."

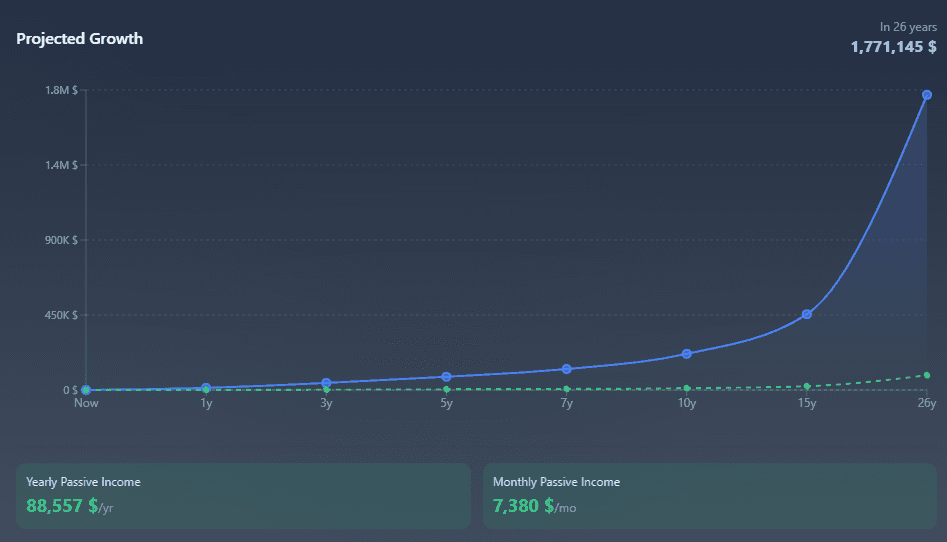

Example: Every month from your paycheck, you send $1,000 into global funds. You don't worry about whether the market is rising or falling. You just invest and move on.

After 25 years, you look back and find you have roughly $1.4 million (based on historical market numbers). Without complicated decisions, stress, or chasing the "best investment."

If you put the same money in a regular savings account, you'd have about $300,000. The difference is... dramatic.

And what about risk? Look, it's always there. My personal philosophy is this: If something like a global index crashes, everything will go down anyway...

Compound Interest: The Real Magic

The reason investing works so well is called compound interest — the phenomenon where your earnings generate their own earnings, creating a snowball effect over time.

"Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn't, pays it." — Albert Einstein

At the beginning, it looks slow. Almost like you just have money sitting in an account. But over time, growth accelerates — and after 20-30 years, the difference is enormous.

* The numbers used correspond to the historical average of global stock markets (~11% per year, $1.000/month). If you want to play with your own numbers, try a compound interest calculator.

Active Investing

This part of investing is:

- riskier,

- more time-consuming.

This includes buying individual company stocks. You can make a lot — but also lose a lot.

Personally, I recommend that before investing, you don't just read articles from random internet personalities, but also look at books written by the best to understand long-term concepts. As a good starting point, I can recommend: "The Intelligent Investor" by Benjamin Graham.

Gambling

I used a name that's emotionally charged at first glance. This type of investing has already cost many people, simply put, everything.

This includes Options — contracts that give you the right (but not the obligation) to buy or sell a stock at a predetermined price by a certain date. You can speculate on rises (call options) or falls (put options) with leverage — small investment, big potential profit, but also losing your entire stake.

The general rule is: Only invest money here that you can afford to lose.

I use a simple "Campfire Test":

If I lit this money on fire right now and roasted marshmallows over it, would it affect my life?

- If yes → don't gamble, I can't afford to lose it

- If no → go ahead and play, I accept the risk

Passive Income

I believe investing is the key to financial freedom and independence. When you start early and invest regularly, you can build passive income.

What Is Passive Income from Investing?

Passive income is cash flow that:

- comes regularly,

- doesn't require your daily work.

Typically this means:

- dividends,

- withdrawals from an investment portfolio.

Note: Renting property is not passive income — it always requires time, headaches, and management.

Traditional Retirement vs. Self-Investing

Traditional Retirement System

The average American contributes roughly $450/month to Social Security. Over 40 years, that's approximately $216,000.

In return, they receive about $1,500/month in retirement.

Better Savings Account

Now imagine investing the same $450/month.

- duration: 40 years

- average return: 11% per year

Result: approximately $3.15 million.

If you withdraw 4% annually from this amount (conservative rule):

- you get about $10,500/month in passive income.

And additionally:

- the capital remains,

- it can pass to your children.

Conclusion

Investing in the form of a Better Savings Account can fundamentally improve your future quality of life.

Every dollar you invest in your twenties and thirties has much greater value than one you earn in your fifties.

The math is simple. The hardest part is discipline, patience, and starting.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Learn To Invest

Learn To InvestLump Sum vs Dollar-Cost Averaging: What I Did With a Windfall in 2026

I had a lump sum and the market was at its 24th record high of 2026, so I froze for six weeks. Here's what the data actually says about lump sum vs dollar-cost averaging, and why the entry method matters far less than whether you press the button at all.

Learn To Invest

Learn To InvestBitcoin in Your 401(k)? What the 2026 DOL Rule Really Means

The 2026 DOL rule doesn’t put Bitcoin in your 401(k) by itself. The real risks, three ways crypto can enter your plan, and how much (if any) to hold.

Learn To Invest

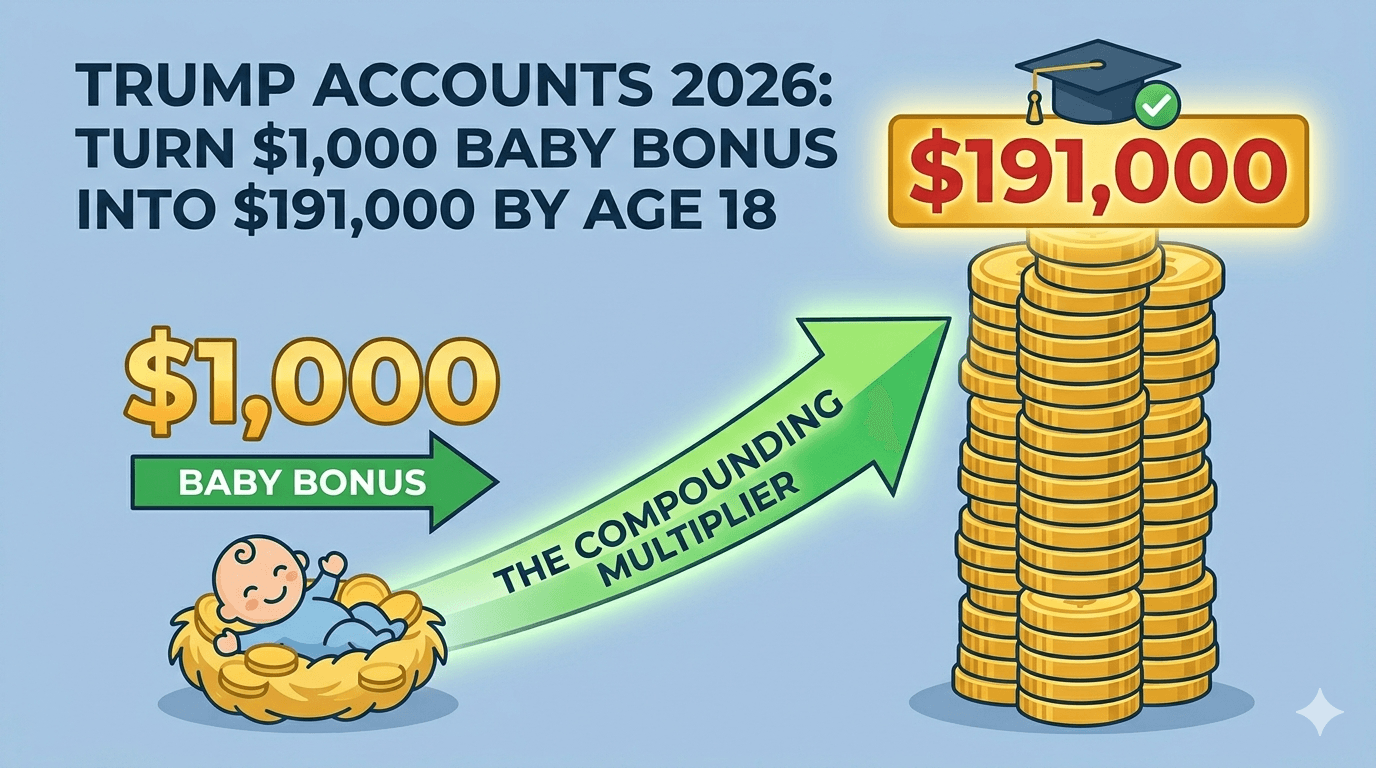

Learn To InvestTrump Accounts 2026: Turn the $1,000 Baby Bonus Into $191,000 by Age 18

Trump Accounts 2026 launch July 4 with a free $1,000 seed for every U.S. newborn. The math: maxed out, $191K by age 18 and $2.2M by 60. Plus the IRS Form 4547 walkthrough, three traps, and how it compares to 529s and custodial Roths.

Learn To Invest

Learn To InvestMonthly Dividend Income Strategy: Build Predictable Cash Flow for FIRE in 2026

Monthly dividend income strategy builds predictable cash flow for early retirees, covering 40-60% of living expenses before Social Security while reducing sequence-of-returns risk. Three-tier approach: dividend aristocrats (60%), dividend ETFs like SCHD (25%), and high-yield specialists (15%) generate $1,600-$2,500/month on a $600K portfolio.

Learn To Invest

Learn To InvestHSA Retirement Strategy: The Triple Tax Advantage (2026)

The HSA is America’s only triple-tax-advantaged account. How FIRE savers turn it into a stealth retirement fund — 2026 limits, the receipt hack, 65+ rules.