HSA Retirement Strategy: The Triple Tax Advantage (2026)

You know what no one tells you when you sign up for your health insurance?

That tiny little box for "HSA enrollment" might be the single most powerful retirement account you'll ever have.

More powerful than your 401(k). More tax-efficient than your Roth IRA. More flexible than your brokerage account. And almost nobody uses it correctly.

I didn't either — until I ran the math. Once I did, I realized I'd been leaving tens of thousands of dollars on the table, every single year, by treating my HSA stealth retirement account like a glorified checking account for doctor visits.

If you have access to a Health Savings Account and you're not using it as a stealth retirement vehicle, this article will change the way you think about money. Let's walk through why the HSA is unbeatable, what the 2026 rules mean for you, and exactly how to turn it into a $400,000+ tax-free machine by the time you retire.

The 401(k) Is Not the Best Retirement Account. This One Is.

Here's a sentence that makes most financial advisors uncomfortable:

The HSA is the single most tax-advantaged account in America.

Not the 401(k). Not the Roth IRA. Not any brokerage account, backdoor Roth, or mega backdoor Roth strategy.

The HSA wins on pure tax math — and the FIRE community has known this for a decade. If you're serious about hitting financial independence early, the HSA belongs at the top of your contribution priority list, right after capturing your employer 401(k) match.

So why doesn't everyone know this?

Because the HSA is marketed as a healthcare account. The banks offering HSAs push it as a way to pay for prescriptions. Employers describe it as an alternative to an FSA. Nobody frames it as what it really is: a retirement account with steroids.

That framing costs the average HDHP-eligible American somewhere between $200,000 and $500,000 in missed retirement wealth. Per person. Over a career.

Let's fix that.

The Triple Tax Advantage: Why the HSA Is Unbeatable

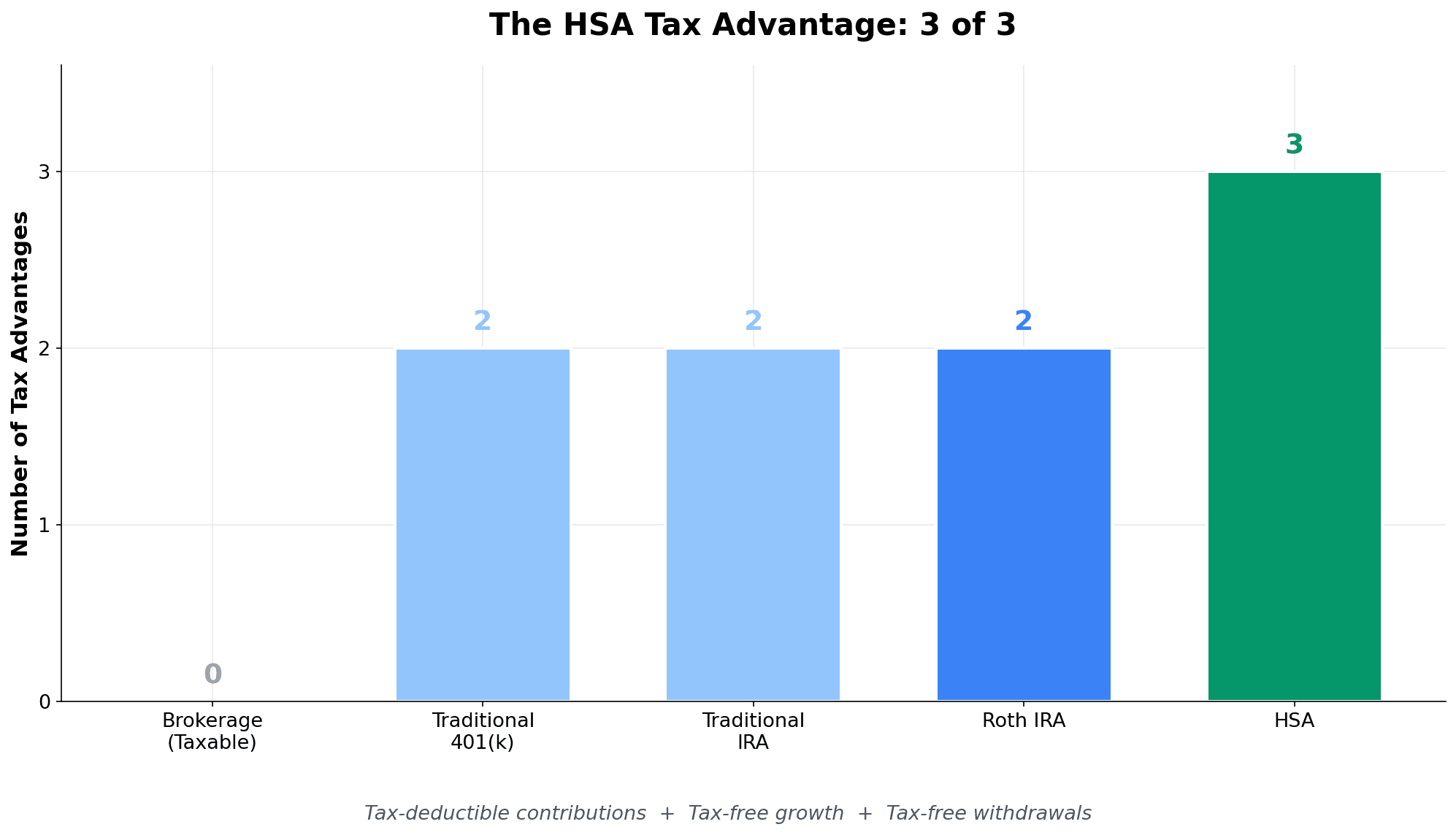

Every retirement account offers some combination of three tax benefits:

- Tax-deductible contributions — you contribute pre-tax dollars

- Tax-free growth — investment gains aren't taxed along the way

- Tax-free withdrawals — you pay nothing when you take the money out

Your 401(k) gives you benefits 1 and 2. Your Roth IRA gives you 2 and 3. Your brokerage account gives you 0 of the 3.

The HSA gives you all three. Every single one.

That's why it's called the "triple tax advantage," and it's why the tax math on an HSA is mathematically superior to every other retirement vehicle in the U.S. tax code.

And there's a bonus fourth advantage most people miss: if you contribute to your HSA through payroll deduction, your contributions also avoid FICA tax. That's another 7.65% in savings — money your 401(k) can never touch.

Run the numbers on a typical dollar:

- Contribute $1 to a 401(k): skip 22% federal tax + 5% state tax. Save 27 cents.

- Contribute $1 to an HSA via payroll: skip federal tax + state tax + 7.65% FICA. Save 34.65 cents.

That's 7.65 cents of extra savings, every single dollar, just for choosing the HSA over the 401(k). On maxing out a family HSA at $8,750, that's an extra $669 of FICA savings per year. Every. Year.

The 2026 Rules: What's New and What It Means

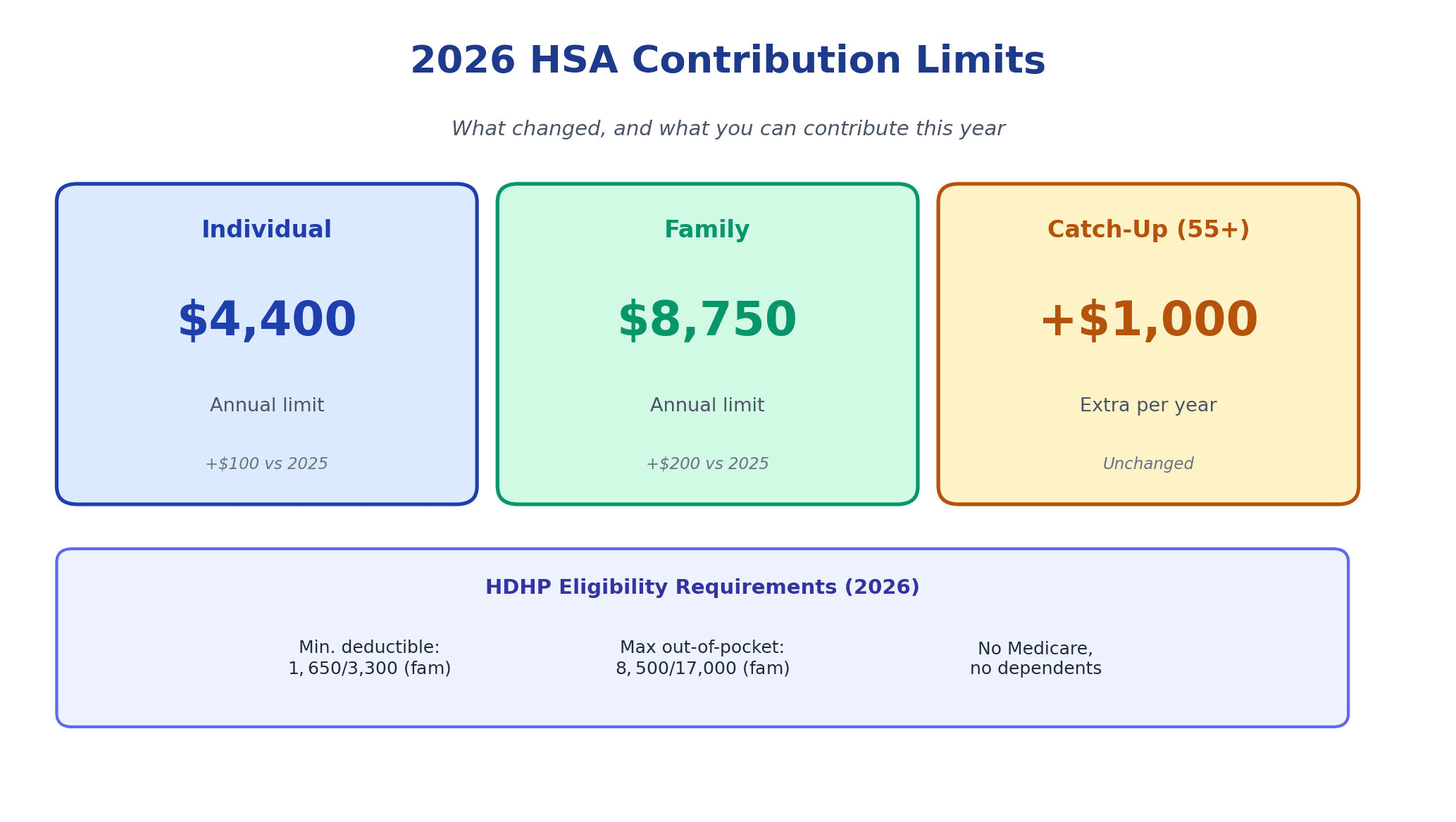

Here are the updated 2026 HSA numbers you need to know:

- Individual contribution limit: $4,400 (up from $4,300 in 2025)

- Family contribution limit: $8,750 (up from $8,550)

- Catch-up contribution age 55+: $1,000 extra per year

- HDHP minimum deductible: $1,650 individual, $3,300 family

- HDHP maximum out-of-pocket: $8,500 individual, $17,000 family

To contribute, you must be enrolled in a qualifying High Deductible Health Plan (HDHP) and not be enrolled in Medicare or claimed as a dependent on someone else's taxes. That's it. There's no income limit. Even high earners can max the HSA — a luxury the Roth IRA denies anyone earning above $161,000 solo or $240,000 married.

If your employer lets you contribute via payroll, do that. If they don't, you can open an HSA yourself with any qualifying provider and deduct contributions on your taxes.

For more on how the 2026 retirement contribution rules interact with each other — especially the Roth catch-up changes for high earners — start with our companion guide.

The Stealth IRA Strategy: Why You Shouldn't Touch Your HSA Now

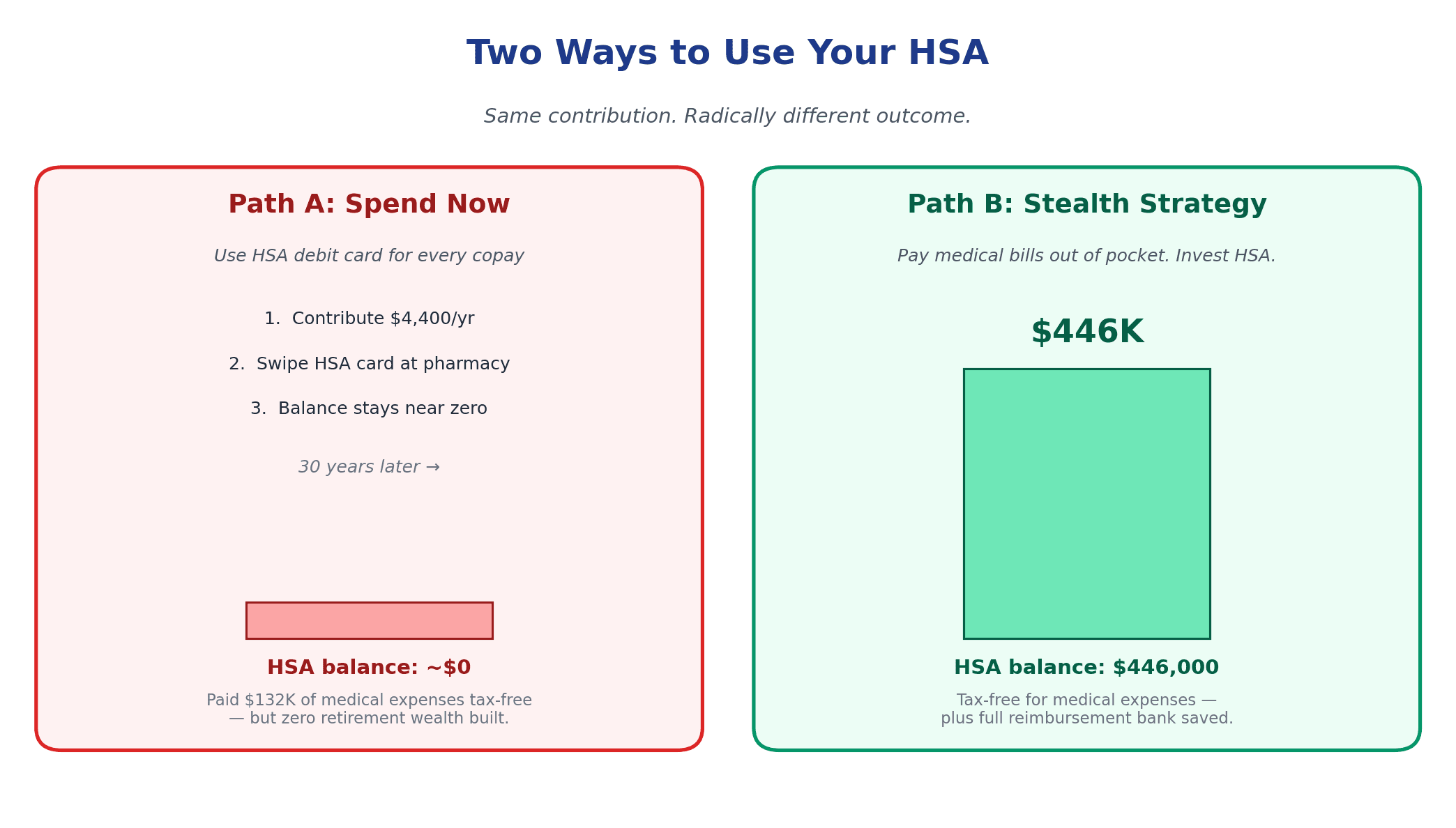

Here's where most people misuse their HSA, and it costs them a fortune:

They fund the HSA. They go to the doctor. They swipe the HSA debit card to pay for the visit. Clean, simple, done.

And wrong.

If you want to turn your HSA into a stealth retirement account, you need to do the counterintuitive thing: don't spend your HSA.

Pay medical bills out of your regular checking account. Let the HSA balance accumulate and invest it in low-cost index funds. Let it grow tax-free for decades.

Then — here's the magical part — you keep every medical receipt. For every visit. For every prescription. For every dental cleaning, pair of glasses, mental health session, surgery, and co-pay.

Why? Because the IRS lets you reimburse yourself from your HSA at any point in the future, for any qualified medical expense incurred after your HSA was opened. There's no deadline. No statute of limitations. No "use it or lose it."

You can accumulate $50,000 of out-of-pocket medical expenses over 20 years, let your HSA compound into $300,000 during that same stretch, and then pull $50,000 out of the HSA — tax-free — as "reimbursement" whenever you want. Your HSA essentially becomes a tax-free piggy bank with a bottomless fill line.

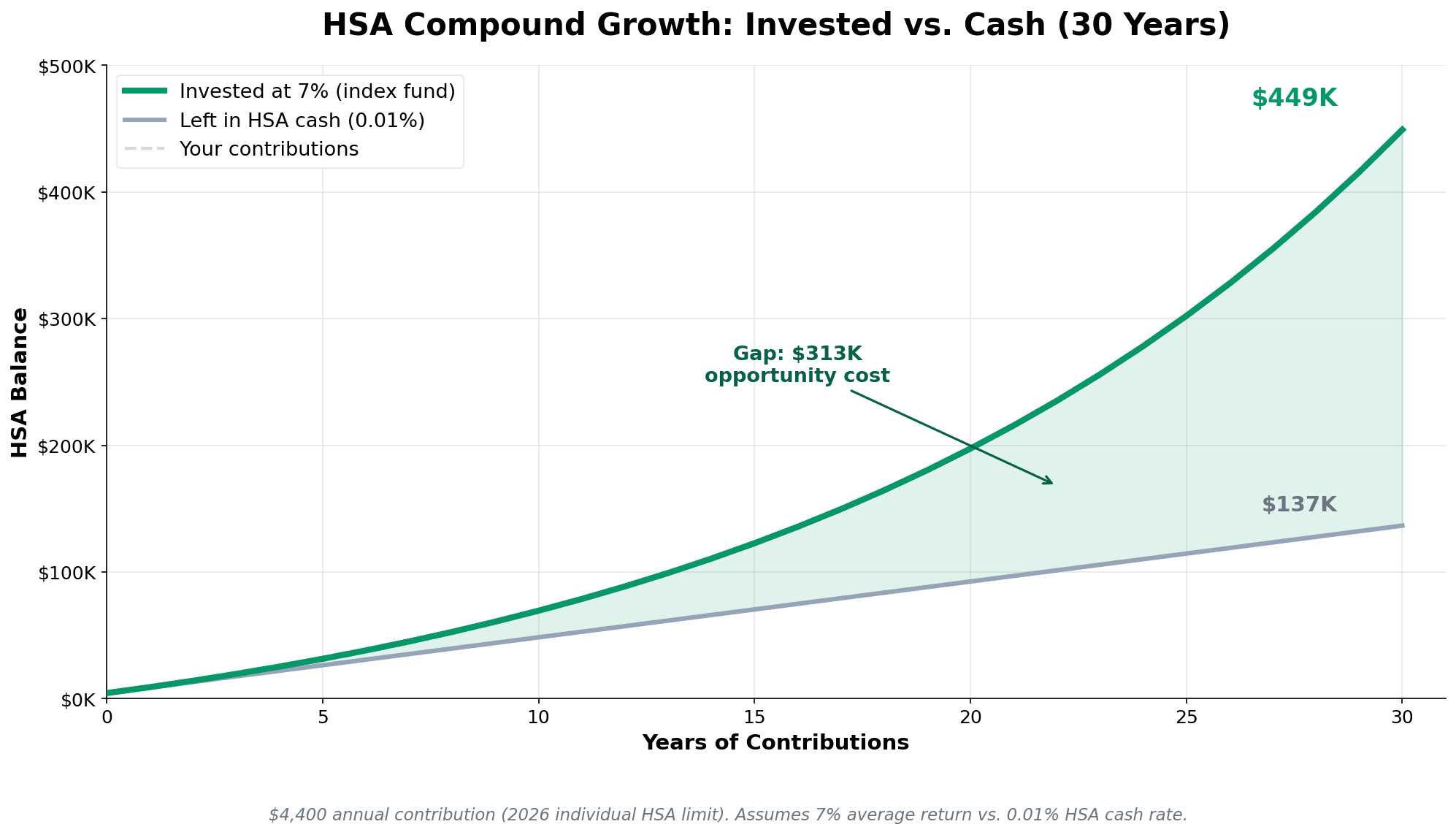

The 30-Year Compound Math: What Your HSA Could Be Worth

Let's make this concrete. Here's what happens if a 35-year-old maxes out their HSA every year for 30 years, invests the money in a low-cost index fund averaging 7% annual returns, and never touches it.

- Annual contribution: $4,400 (individual limit)

- Time horizon: 30 years

- Assumed return: 7% per year

- Final balance: ~$446,000

And that entire balance is tax-free for medical expenses — including all the receipts you've accumulated over the past 30 years.

For a family maxing out the $8,750 family limit at the same 7% return, the final balance clears $888,000. That's near-millionaire status from a single retirement account that most people use as a debit card.

Compare that to leaving the money in the HSA cash account at 0.01% interest (the default for most HSA providers, and the reason most HSAs never grow):

The difference between investing your HSA and leaving it in cash is $314,000. Over 30 years. For the same contributions. That's not a rounding error. That's a life-changing number hiding inside a decision most people don't even realize they're making.

This is the same compound math behind the Coast FIRE strategy, where you front-load retirement savings early and let compounding do the heavy lifting. The HSA is one of the highest-leverage accounts to do that with, because every dollar avoids three layers of tax along the way.

The Receipt Reimbursement Hack

If you're going to follow the stealth IRA strategy, you need a bulletproof system for tracking medical receipts. Here's the setup that works:

1. Create a dedicated cloud folder. Name it something like "HSA Receipts" in Google Drive, Dropbox, or iCloud.

2. For every medical expense, save:

- The receipt or Explanation of Benefits (EOB)

- The date of service

- The amount you paid out of pocket

- The provider's name

- A short description

3. Log it in a simple spreadsheet. Columns: Date, Provider, Service, Amount, Receipt Link. Keep a running total. This is your "reimbursement bank."

4. Back it up. Keep a second copy somewhere redundant. You don't want to lose $20,000 of reimbursement eligibility because Google Drive had a bad week.

5. Reimburse yourself strategically. When you need the money (say, you hit a rough patch, or you want to fund a kid's college, or you're ready to retire early), pull the HSA funds out and attribute them to accumulated receipts. Tax-free. Every dollar.

This sounds like a hassle. It's not. It's 30 seconds per expense, and it's building you a six-figure tax-free asset.

You can track these contributions alongside your net worth and retirement projections in My Financial Freedom Tracker — our tool pulls your HSA balance into your full financial picture, so you can see how the stealth IRA fits into your broader FIRE path.

After Age 65: The HSA Becomes a Traditional IRA

Here's the closing magic trick that makes the HSA genuinely unbeatable.

Until age 65, HSA withdrawals must be for qualified medical expenses — otherwise you pay income tax plus a 20% penalty. That's the one "catch" people usually cite when they say the HSA is too restrictive.

But once you turn 65, that penalty disappears entirely. Non-medical withdrawals after 65 are taxed exactly like a traditional IRA — ordinary income, no penalty.

Which means your HSA at age 65 effectively gives you three options:

- Withdraw for qualified medical expenses: tax-free. Forever.

- Withdraw for reimbursement of past medical expenses: tax-free (if you kept receipts).

- Withdraw for anything else: taxed as ordinary income — same as a 401(k) would be.

That third option is what makes the HSA function as a "stealth IRA." Even if you're somehow blessed with a lifetime of zero medical expenses (statistically impossible), the HSA is still at least as good as a traditional IRA after 65. And in the vast majority of cases, because you'll have some medical expenses in retirement, it's meaningfully better.

Fidelity estimates the average 65-year-old retired couple will spend around $165,000 on healthcare through retirement. That's a lot of tax-free HSA withdrawals you'll naturally use. The rest? Treat it like a 401(k).

Common Mistakes That Destroy the HSA Advantage

I've watched smart people make these five HSA mistakes over and over. Don't be one of them:

1. Leaving the HSA in cash.

Most HSA providers default your contributions into a 0.01% interest account. You have to manually opt into the investment option. If you don't, you're earning nothing while inflation eats your contributions. A $4,400 contribution growing at 0.01% for 30 years is worth about $4,413. At 7%, it's worth $33,500. Check your HSA today — is it invested?

2. Paying medical bills from the HSA.

Every time you swipe the HSA card for a $30 copay, you're robbing your future self of the compounded growth that $30 could have generated. If cash flow allows, pay out of pocket and let the HSA keep compounding.

3. Failing to save receipts.

Without receipts, the stealth IRA strategy collapses. You can only reimburse yourself tax-free for expenses you can document. Start saving receipts today, even if you haven't been. Going forward is better than never.

4. Picking the wrong HSA provider.

Not all HSAs are created equal. Some charge monthly fees that eat your returns. Some have terrible investment options. Look for an HSA provider with low fees, low-cost index fund options, and a strong digital interface. Fidelity, Lively, and HSA Bank are popular choices in the FIRE community.

5. Skipping the HDHP when it would save you money.

Many people reflexively pick the "gold" PPO plan at open enrollment because it feels safer. But run the math. For young healthy individuals and families with moderate healthcare usage, the HDHP is frequently the cheaper option — especially when you factor in the HSA tax savings on top.

Who Should NOT Use an HSA

The HSA isn't for everyone. Let's be honest about the exceptions.

If you have chronic high medical expenses, the HDHP required to be HSA-eligible may expose you to too much out-of-pocket risk. If your household income is low and your marginal tax rate is already near zero, the triple tax advantage gives you less benefit than it gives high earners. If you're juggling too much debt or don't have an emergency fund, prioritize those first — paying down a 20% credit card balance beats almost any investment return, HSA included.

This is the classic financial levels step-by-step question: the right move depends on where you are. For most middle-class and upper-middle-class households eligible for an HSA, though, it's one of the most powerful moves on the board.

How to Start Your HSA Stealth IRA Strategy Today

Ready to turn your HSA into a retirement powerhouse? Here's your action plan:

Step 1 — Confirm HDHP eligibility. Check your health plan's summary. Does it meet the 2026 deductible thresholds ($1,650 individual / $3,300 family)? Are you not enrolled in Medicare? Are you not claimed as a dependent? If yes to all, you're eligible.

Step 2 — Open or upgrade your HSA. If you have one through your employer, confirm you can invest the balance in index funds. If not, consider rolling it to a better provider (Fidelity, Lively, HSA Bank are common picks). You can roll employer HSAs to personal HSAs without tax consequence.

Step 3 — Set contributions. If you can afford it, max the HSA ($4,400 individual / $8,750 family in 2026). If not, at minimum contribute enough to capture any employer HSA match and to cover your actual annual medical spend.

Step 4 — Invest the balance. The HSA is not a savings account. Pick a low-cost total market or world index fund. If you're new to investing, start with our Investing Made Simple guide, and consider the options in our roundup of the best world ETFs.

Step 5 — Pay medical bills out of pocket. Treat your HSA like a Roth IRA you can't touch. Cash flow permitting, cover medical expenses from your regular checking account and let the HSA compound.

Step 6 — Build your receipt system. Cloud folder + spreadsheet. Date, provider, amount, receipt link. Start now, and keep it forever.

Step 7 — Track it in your financial picture. Whether you use a spreadsheet or a tool like My Financial Freedom Tracker, make sure your HSA balance is showing up in your net worth and retirement projections. An asset you don't see is an asset you don't use.

If you're already on the FIRE movement path, the HSA might be the single highest-leverage upgrade you can make in the next 12 months. And if you're not on that path yet, it's one of the easiest places to start.

The Bottom Line

The HSA is the most tax-efficient retirement account in America, and most people never use it as one. If you're eligible — and millions of Americans are — treating your HSA as a stealth retirement vehicle can add hundreds of thousands of dollars to your future net worth for no additional risk and almost no additional effort.

Fund it. Invest it. Don't touch it. Save the receipts.

That's the entire strategy. Three decades from now, your older self will thank you.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Learn To Invest

Learn To InvestLump Sum vs Dollar-Cost Averaging: What I Did With a Windfall in 2026

I had a lump sum and the market was at its 24th record high of 2026, so I froze for six weeks. Here's what the data actually says about lump sum vs dollar-cost averaging, and why the entry method matters far less than whether you press the button at all.

Learn To Invest

Learn To InvestBitcoin in Your 401(k)? What the 2026 DOL Rule Really Means

The 2026 DOL rule doesn’t put Bitcoin in your 401(k) by itself. The real risks, three ways crypto can enter your plan, and how much (if any) to hold.

Learn To Invest

Learn To InvestTrump Accounts 2026: Turn the $1,000 Baby Bonus Into $191,000 by Age 18

Trump Accounts 2026 launch July 4 with a free $1,000 seed for every U.S. newborn. The math: maxed out, $191K by age 18 and $2.2M by 60. Plus the IRS Form 4547 walkthrough, three traps, and how it compares to 529s and custodial Roths.

Learn To Invest

Learn To InvestMonthly Dividend Income Strategy: Build Predictable Cash Flow for FIRE in 2026

Monthly dividend income strategy builds predictable cash flow for early retirees, covering 40-60% of living expenses before Social Security while reducing sequence-of-returns risk. Three-tier approach: dividend aristocrats (60%), dividend ETFs like SCHD (25%), and high-yield specialists (15%) generate $1,600-$2,500/month on a $600K portfolio.

Learn To Invest

Learn To InvestPay Off Mortgage or Invest? The Math vs. the Psychology

Pay off the mortgage or invest the difference? The math favors stocks; psychology favors the house — homeowner net worth is $400K vs $10K for renters.