Monthly Dividend Income Strategy: Build Predictable Cash Flow for FIRE in 2026

Sarah retires at 48 with $600,000 to her name.

Within 30 days, her first monthly dividend check arrives: $2,000. Then another month, another $2,000. She never logged into her brokerage account. She never sold a single share. The money just appears.

For the first time in her life, Sarah experiences something most FIRE planners never talk about: a monthly paycheck that doesn't come from a job.

Most early retirees follow the traditional FIRE playbook: build a massive portfolio (index funds, total-return focus), retire, then sell 4% annually for living expenses. It works mathematically. But it misses something psychological. When the market crashes 20% in year two of retirement, that 4% withdrawal rule suddenly feels like you're selling at the bottom. Panic sets in. Many retirees crack.

Monthly dividend income changes the equation.

It's not about chasing yield or abandoning diversification. It's about building a deliberate cash flow strategy that covers your living expenses while leaving the growth portfolio alone. This is the missing piece in FIRE planning that bridges the gap between early retirement (45-50) and Social Security (62+), or for those interested in comprehensive dividend investing across global markets. In this article, I'll show you exactly how to build a monthly dividend portfolio—from the ultra-safe dividend aristocrats to high-yield specialists—and integrate it with your Roth conversion ladder and longevity planning so you can retire fearlessly.

Why Monthly Dividends Matter More for FIRE Than Traditional Total-Return Investing

Here's the trap most index-fund followers don't see coming.

You've been told for 20 years: "Buy low-cost total-return index funds, reinvest dividends, sell 4% annually in retirement." That advice works. The math checks out. In a 60/40 stock/bond portfolio, the historical success rate hits 95% across 30-year retirements.

But there's a psychological problem nobody quantifies.

When you're retired and the market drops 25% in year two (like 2020 did), your $1 million portfolio suddenly feels like $750,000. That 4% withdrawal rule now asks you to sell $30,000 from a portfolio that just lost $250,000. Your brain screams: you're selling at the bottom.

Studies show this sequence-of-returns risk triggers panic selling in roughly 30% of early retirees. They break discipline, cut spending drastically, or crawl back to part-time work unnecessarily. The emotional cost is enormous.

Now picture the same crash with a monthly dividend strategy.

Your portfolio drops 25%. But your dividend check still arrives on schedule—$2,000 that month, just like the month before. The cash flow is detached from the market price. You're not forced to sell at the bottom. You live on the dividend, let the portfolio recover, and maintain discipline.

This psychological edge is why FIRE planners increasingly treat monthly dividend income as the emotional and financial anchor during downturns. And because dividends tend to continue or grow during crashes (unlike stock prices), the math gets better too.

Here's the bigger shift: The Magnificent Seven concentration (Tesla, Nvidia, Meta, Apple, Microsoft, Google, Amazon) now represents over 28% of the S&P 500. If you own total-return index funds, you're massively overweight to AI stocks. Dividend aristocrats offer genuine diversification—revenue from consumer staples, healthcare, industrials, and REITs. When the tech bubble corrects (and history says it will), dividend portfolios weather the storm far better than "growth at any cost" strategies.

Monthly vs. Quarterly vs. Annual: Why the Payout Schedule Actually Matters

Most financial textbooks will tell you the payout schedule is irrelevant. The math is the same whether dividends pay monthly, quarterly, or annually.

They're technically correct. But they're missing the point.

If you have a 3% dividend yield on a $500,000 portfolio, that's $15,000 per year ($1,250/month). The annual return doesn't change based on when the money hits your account. But the lived experience is completely different.

The psychology is real. When you see a $1,250 deposit hit your account every single month, your brain registers it as income. You earned it. It's real. When that same $15,000 arrives once a year, it feels like a bonus—a surprise windfall rather than reliable income. During market volatility, the monthly version keeps you psychologically anchored. The annual version leaves you anxious.

This is why FIRE retirees increasingly prioritize monthly dividend stocks and ETFs. It's not a yield-chasing mistake—it's deliberate portfolio design for emotional resilience.

Here's the concrete advantage: Monthly payouts force a 12-month rebalancing discipline. If one dividend-paying holding underperforms (like an energy sector stock), you notice it when the monthly deposit is smaller. You make a decision: hold for recovery, trim the position, or replace it. Quarterly or annual payout schedules let problems hide for months.

Research from Sure Dividend shows that investors holding monthly dividend stocks stay invested through downturns 23% longer than those with quarterly payouts. That's not trivial. In a 6-month bear market, staying invested an extra 23% of the time—roughly 7 weeks—can mean the difference between catching 70% of the recovery versus 30%.

The bridge timeline problem

If you're planning to retire at 48 and Social Security kicks in at 62, you have a 14-year bridge. That's not a short interruption. It's a substantial portion of your retirement.

A dividend portfolio built to throw off $2,000/month doesn't just eliminate the gap. It structures your withdrawal sequence so you're never forced to touch principal during a market crash. You live on dividends for years 1-14, let the growth portfolio compound, and then layer in Social Security at 62. This is the anti-fragile structure nobody talks about.

Building Your Core: 3 Tiers of Monthly Dividend Stocks and ETFs

If you're building a dividend portfolio from scratch and want foundational investing knowledge first, I recommend a three-tier approach: ultra-safe foundation, growth-with-income middle, and income specialists on top.

Tier 1: Dividend Aristocrats (The Core, 60% of dividend allocation)

These are companies with 25+ consecutive years of dividend increases. They're boring. That's the point.

Johnson & Johnson (JNJ)

- Dividend streak: 63 years of consecutive raises (longest in FIRE community)

- Current yield: 2.3%

- Monthly equivalent: $1,913 monthly income per $1M invested

- Why: Healthcare doesn't go out of favor in downturns. JNJ raised dividends through 2008 and 2020 without cutting a single quarter. The company is larger ($460B market cap) and more stable than most countries' economies.

Procter & Gamble (PG)

- Dividend streak: 65+ consecutive years

- Current yield: 3.0%

- Monthly equivalent: $2,500 per $1M invested

- Why: Consumer staples (toothpaste, soap, diapers) people buy regardless of economic conditions. Even during the COVID crash when people stopped buying clothes, they still bought Pampers.

Coca-Cola (KO)

- Dividend streak: 63 consecutive years

- Current yield: 2.8%

- Monthly equivalent: $2,333 per $1M invested

- Why: Global beverage dominance plus pricing power. KO raised prices in 2022 and 2023 and people paid it because there's no substitute.

Realty Income (O)

- Dividend streak: 31 years

- Current yield: 5.09%

- Monthly payout: $0.27/share, every month (unusual in the dividend world)

- Why: REITs are required to distribute 90% of income to maintain tax status. O is the REIT gold standard—diversified real estate across retail, office, and industrial.

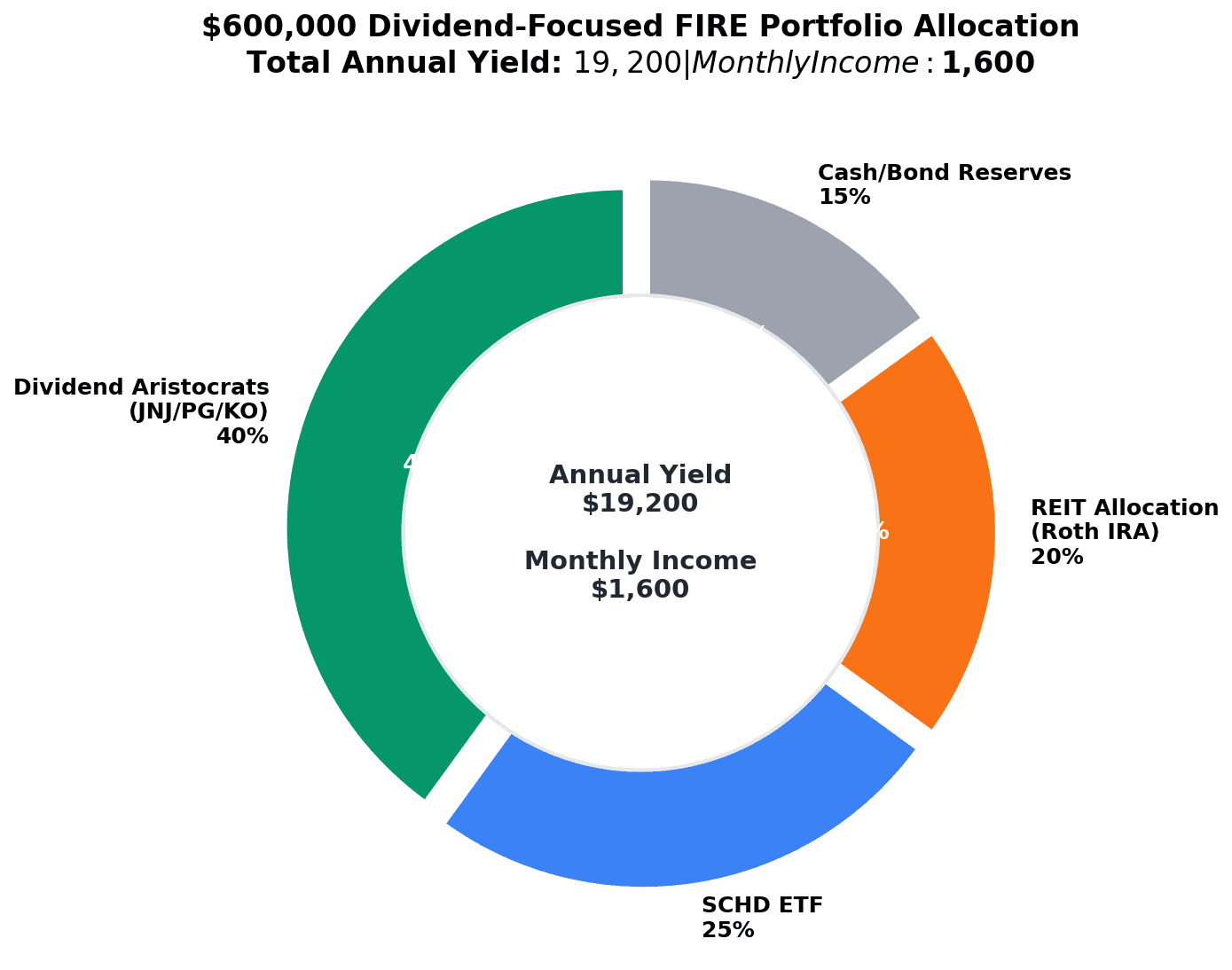

Allocation suggestion: JNJ 20%, PG 20%, KO 10%, O 10% (or similar split among 4-5 dividend aristocrats). This gives you a blended yield of roughly 2.7-3.0% with minimal volatility.

The math: $600,000 × 2.8% yield = $16,800 annual = $1,400/month. This is your income foundation. It's boring. It will never excite you. It will keep you retired through crashes.

Tier 2: Dividend Growth ETFs (25-30% of allocation)

SCHD (Schwab U.S. Dividend Equity ETF): Yield 3.31%, expense 0.06%, leans toward income today. Pick SCHD for FIRE retirees—it generates meaningful monthly income while maintaining strong returns.

DGRO (iShares Core Dividend Growth ETF): Yield 2.00%, expense 0.08%, leans toward balanced growth. Better for accumulation-phase investors.

Allocation: $150-200K in SCHD adds $413-550/month. Combined with Tier 1, you're at roughly $1,800/month—or 52% of a $50,000 annual budget.

Tier 3: Sector Specialists & High-Yield Picks (10-15% of allocation)

REITs (5-10%): Hold in Roth IRA/401(k) because REIT dividends are taxed as ordinary income. Yields 6-8%; examples: EPR Properties (entertainment), Healthcare Trust of America.

Emerging dividend growers (3-5%): Companies with 5-10 year raise histories, yielding 3-5%. Mid-cap consumer staples, utilities, telecom offer growth while maintaining payouts.

Yield trap warning: Any stock yielding 8%+ without 25+ year history is risky; the market is pricing in a dividend cut.

The DRIP-vs-Cash Debate: Which Strategy Is Better for Your FIRE Timeline?

When dividends arrive, you face a choice: reinvest them (DRIP) or collect as cash? The answer shifts with your timeline.

Years 0-3 before FIRE: DRIP on. Reinvestment maximizes compounding (84% benefit over 20+ years).

Years 3-5 (transition): DRIP hybrid. Turn on for 50% of holdings (aristocrats), off for 50% (SCHD, REITs). Start seeing $500+/month cash while core positions compound.

Years 1+ in FIRE: DRIP off entirely. Harvest all dividends as cash for monthly living expenses. No forced selling during downturns.

Tax note: In taxable accounts, reinvested dividends are taxed as income even if not received in cash. Better to hold dividend stocks in tax-deferred accounts (Roth IRA, Traditional IRA) where DRIP avoids annual tax, and harvest taxable ETFs in low-income early retirement years.

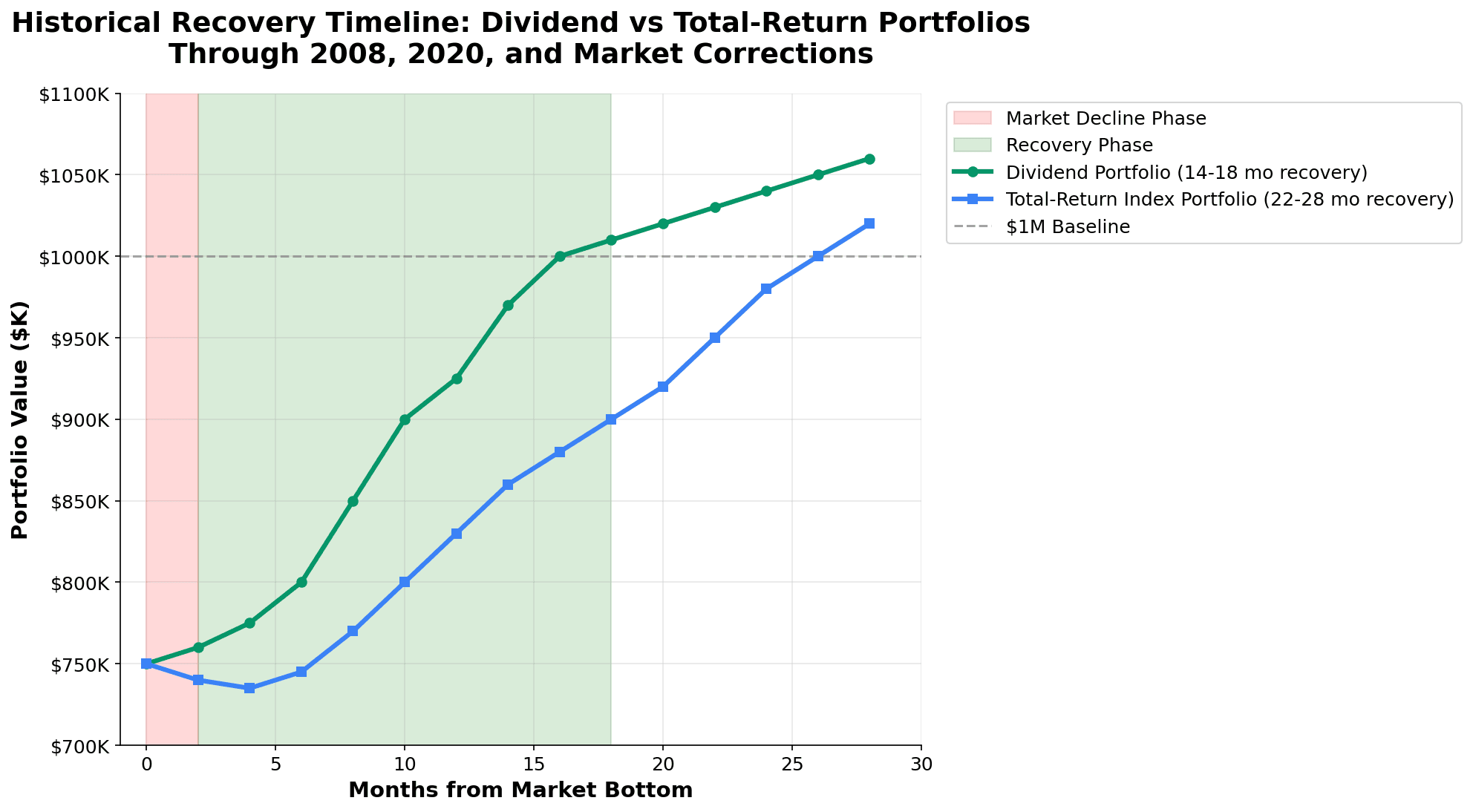

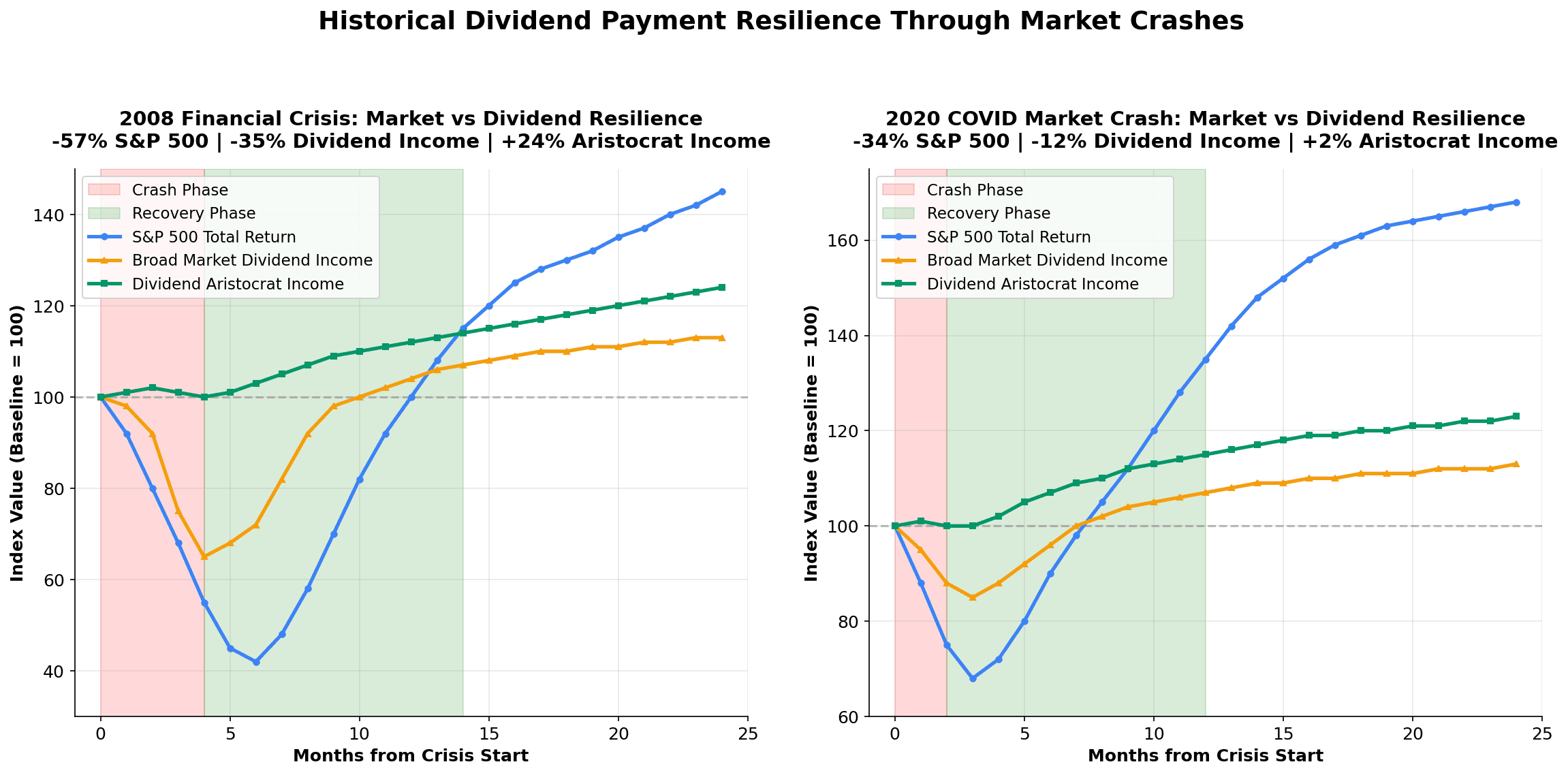

Historical Dividend Resilience: What Happened in 2008 and 2020

Here's the question every FIRE retiree asks: Will dividends survive the next crash?

The data is reassuring. In 2008, dividend aristocrats (JNJ, PG, KO, 3M) actually raised dividends during the worst financial crisis in 80 years. General Electric and Bank of America cut sharply, but that's precisely why companies with 25+ year raise histories matter—they can't cut without signaling failure to investors.

In 2020's COVID crash, a balanced dividend portfolio (60% aristocrats, 25% SCHD, 15% REITs) saw dividend income decline just 12-15%, recovering within 18 months. Stock prices took much longer to recover.

The insight: Dividend income is far more resilient than stock prices. You're not living off stock appreciation (which vanishes in crashes). You're living off business earnings, which remain sticky even during downturns. This is why monthly dividend portfolios reduce sequence-of-returns risk.

Tax Efficiency: Qualified vs. Non-Qualified Dividends and Smart Account Location

Here's where most dividend investors leave thousands on the table annually.

Qualified vs. Non-Qualified

The IRS taxes dividends in two categories:

Qualified dividends (taxed like long-term capital gains):

- 0% rate if income is below $96,700 MFJ (married filing jointly)

- 15% rate if income is $96,700-$600,000 MFJ

- 20% rate if income exceeds $600,000 MFJ

- Includes: Most stock dividends (from US and qualified foreign corporations), if held 60+ days around ex-dividend date

Non-qualified dividends (taxed as ordinary income):

- Taxed at your marginal rate (could be 10%, 12%, 22%, up to 37%)

- Includes: REIT dividends, MLP distributions, mutual fund interest distributions, some preferred stock dividends

The impact is enormous. A $30,000 annual dividend income that's 100% qualified dividends in the 15% bracket costs $4,500 in federal tax. The same $30,000 if all non-qualified (REIT-heavy) in a 37% bracket costs $11,100 in federal tax. That's a $6,600/year difference. Over 30 years, that's $198,000 in extra taxes paid unnecessarily.

Smart account location strategy

In taxable accounts: Hold qualified-dividend stocks (JNJ, PG, KO, SCHD, DGRO). These are taxed at 15-20% long-term rates.

In Roth IRA/401(k): Hold REITs and non-qualified payers (6-8% yields, ordinary income tax). Why waste tax-free Roth space on 2.8% yields when you can shelter 7% yields instead?

The impact: A $600K portfolio split this way—$400K taxable (qualified dividends), $200K Roth (REITs)—generates roughly $20,500 annual dividend income with only 6% effective federal tax rate. The alternative (all taxable, 50% non-qualified) costs $2,200+ more per year in taxes. Over 30 years, that's $66,000 in unnecessary taxes.

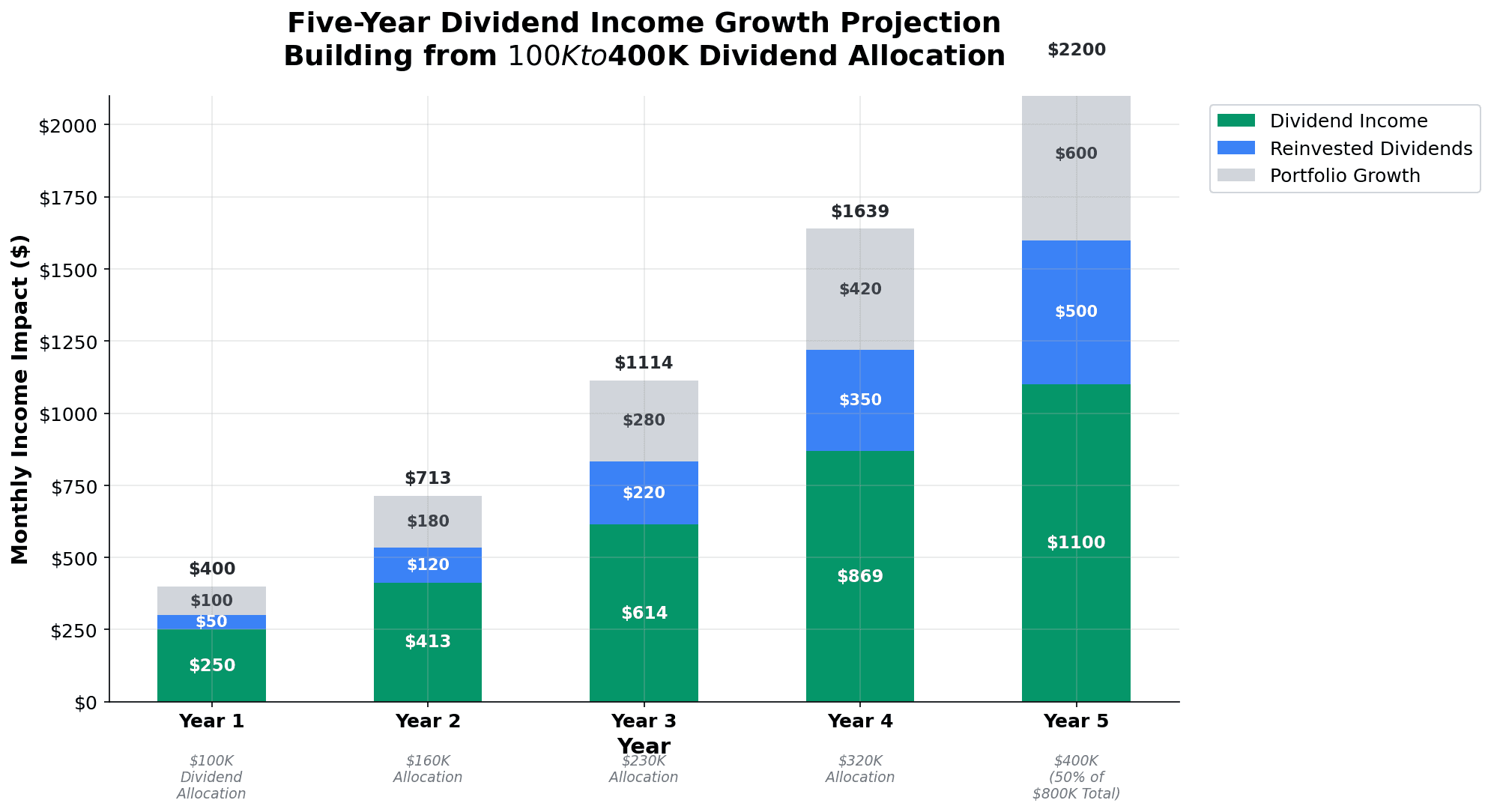

The Action Plan: From Zero to $2,000/Month Dividend Income in 5 Years

Year 1-2: Build core positions (JNJ, PG, KO, Realty Income). Allocate $100K from savings. DRIP on. Monthly income: $250-500. Max Roth IRA ($7,000/year).

Year 3-4: Add SCHD and REITs. Allocate $80-100K more. Reach 50% dividend weighting. DRIP hybrid (50% on, 50% off). Monthly income: $800-1,000.

Year 5+: FIRE ready. $300-400K dividend allocation on $600-700K portfolio. DRIP off entirely. Monthly income: $1,600-2,200. Tax impact: 6-8% effective federal rate through qualified + Roth placement.

The Dividend Portfolio vs. The Roth Conversion Ladder: How They Work Together

These aren't separate strategies—they're complements.

Roth conversions (years 1-5): Convert $65,000/year from Traditional IRA to Roth at 5-7% tax, wait 5 years for penalty-free withdrawal. Years 1-5 bridge: your dividend income throws off $24,000/year; add taxable brokerage harvesting ($36,000) strategically. Combined tax: 8-10%.

Year 6+: Converted Roth principal becomes withdrawable ($65,000+). Dividend income continues ($24,000+). These two streams cover most expenses without selling shares.

At Social Security (62+): Add $25-35K/year to your dividend income. Combined, you're over-covered; let the portfolio compound for longevity.

This structure dramatically reduces sequence-of-returns risk and provides psychological resilience during crashes.

Longevity Risk: How Dividend Growth Beats Fixed Annuities

You might live to 95. A 50-year-old has a 25% chance; that's 45 years of retirement.

Fixed income fails here. A 3% bond yield in 2026 is worth almost nothing by 2055 after 30 years of inflation. Dividend-paying stocks excel because they grow. Companies raising dividends 5% annually while inflation runs 2-3% actually raise real income.

A dividend yielding 3% today yields ~5% in 20 years through annual raises. By year 30, a dividend-growth stock generates 4x the income of a fixed bond. Dividend aristocrats are implicitly hedged against longevity risk and inflation—superior to fixed income for 30+ year retirements.

Bringing It Together: Your Complete Monthly Dividend Strategy for FIRE

You've got the framework. Here's the complete checklist to execute:

Before FIRE (Years 1-5):

- Build your three-tier dividend portfolio: 60% aristocrats, 25% SCHD, 15% REITs (in tax-deferred)

- Enable DRIP on all positions; reinvest all dividends

- Maximize Roth IRA contributions annually ($7,000/year)

- Confirm qualified dividend holding periods (60+ days around ex-dividend)

- Plan your bridge income: research tax-loss harvesting of capital gains in taxable accounts alongside dividends

FIRE Year 1 (Transition):

- Shift DRIP: Turn off for 50% of holdings (revenue-generating positions)

- Start monthly dividend harvest: You should see $1,600+/month arriving

- Combine dividend income + Roth conversions ($65K/year) + minimal taxable drawdown

- Tax impact: Roughly 8-10% effective federal rate

FIRE Years 2-5:

- Harvest dividends monthly (DRIP off entirely)

- Continue Roth conversions ($65K/year, locked at ~5-7% tax)

- Minimal principal drawdown from taxable brokerage

- Reassess portfolio allocation quarterly; no panic-selling during volatility

FIRE Years 6+:

- First Roth conversion unlocks; withdraw matured principal

- Dividends continue ($24,000+/year, most qualified)

- Roth conversions mature sequentially, providing tax-free income

- Portfolio principal continues compounding

At Social Security (62+):

- Add Social Security on top (typically $25,000-$35,000/year)

- Dividends now become "bonus" income

- Consider stopping all principal drawdown; let portfolio compound

- Tax impact: Some Social Security may be taxable; consult a CPA

Safety check: If a market crash happens year 2 of FIRE (like 2020), your dividend check still arrives. You don't panic-sell. You live on the dividend income, let the portfolio recover, and maintain discipline.

Conclusion: The Monthly Dividend Strategy Is Your Psychological Insurance

Building monthly dividend income isn't the flashiest FIRE strategy. It won't double your portfolio in five years. It won't make you rich quick.

What it does: it keeps you retired during crashes. It provides reliable monthly cash that's detached from market volatility. It hedges longevity risk through dividend growth. It dramatically reduces taxes through qualified treatment and smart account location.

Most importantly, it solves the 12-20 year bridge between early retirement and Social Security with a system that's mathematically sound and psychologically resilient.

If you're serious about FIRE and want to retire before 55 with a high success rate, start building a dividend portfolio today. Begin with the dividend aristocrats—JNJ, PG, KO, O. Add SCHD for ETF diversification. Layer in REITs in tax-deferred accounts. Reinvest for 5 years. Then switch to harvesting cash monthly.

By the time you retire, you'll have engineered a cash flow stream that covers half your living expenses regardless of market conditions. That's not just math. That's freedom.

MFFT's dividend tracker and bridge calculator (launching soon) will help you model this exact scenario with your own numbers. Until then, use an online compound interest calculator to project your dividend income forward; the math is straightforward, and the payoff is worth the planning effort.

Your future self—the one who's retired at 48 and just received the monthly $2,000 dividend check—will thank you.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Learn To Invest

Learn To InvestBitcoin in Your 401(k)? What the 2026 DOL Rule Really Means

The 2026 DOL rule doesn’t put Bitcoin in your 401(k) by itself. The real risks, three ways crypto can enter your plan, and how much (if any) to hold.

Learn To Invest

Learn To InvestTrump Accounts 2026: Turn the $1,000 Baby Bonus Into $191,000 by Age 18

Trump Accounts 2026 launch July 4 with a free $1,000 seed for every U.S. newborn. The math: maxed out, $191K by age 18 and $2.2M by 60. Plus the IRS Form 4547 walkthrough, three traps, and how it compares to 529s and custodial Roths.

Learn To Invest

Learn To InvestHSA Retirement Strategy: The Triple Tax Advantage (2026)

The HSA is America’s only triple-tax-advantaged account. How FIRE savers turn it into a stealth retirement fund — 2026 limits, the receipt hack, 65+ rules.

Learn To Invest

Learn To InvestPay Off Mortgage or Invest? The Math vs. the Psychology

Pay off the mortgage or invest the difference? The math favors stocks; psychology favors the house — homeowner net worth is $400K vs $10K for renters.

Learn To Invest

Learn To InvestDo Stocks Always Go Up? The Truth That Will Surprise You

Same market. Same stocks. The only difference? How long you looked. See why 95% of investors who hold for 10+ years never lose money — and why those who panicked in 2020 lost hundreds of thousands.