Trump Accounts 2026: Turn the $1,000 Baby Bonus Into $191,000 by Age 18

On July 4, 2026, the federal government will hand every newborn in America a $1,000 head start on retirement.

Most parenting blogs are calling it a "baby bonus." That framing is wrong — accept it and you'll leave the most powerful new tax-advantaged investment account in 23 years sitting in default settings.

Trump Accounts 2026 are not a savings account. They're a custodial-style investment vehicle (IRC Section 530A) that auto-invests in S&P 500 index funds, caps fees at 0.10%, and converts to a traditional IRA at the child's 18th birthday. According to the White House Council of Economic Advisers' own modeling, a maxed-out account can grow to roughly $191,400 by age 18 and, if left untouched, over $2.2 million by age 60.

This is the first new federal tax-advantaged account class since the HSA in 2003. And in the noise of policy headlines, almost nobody is doing the math.

Below: how the accounts work, who qualifies, how to file Form 4547, the compounding math, the comparison vs. 529 / Roth / UTMA, three traps, and a FIRE maximization playbook.

Quick note: tax laws can change, the IRS final regulations on a few details (especially partial-withdrawal caps before age 25) are still pending as of May 2026, and this is general information — not personalized financial advice. Confirm specifics with your tax professional before filing.

What Trump Accounts 2026 Actually Are (and Why They're Not Just a Baby Bonus)

A Trump Account is a tax-deferred investment account for minors, created by the One Big Beautiful Bill Act (OBBBA, P.L. 119-21) and codified as IRC Section 530A. It launches July 4, 2026.

Here's the part most articles bury: this is not a savings account. It is forced equity investing. Every dollar must be held in a U.S. equity index fund tracking a broad benchmark like the S&P 500. No cash. No bonds. Just stocks.

That single design choice — combined with a 0.10% fee cap — is what makes this product different. A custodial brokerage account can hold whatever you want, but it has no tax shelter. A 529 has tax-free growth, but only for education. A custodial Roth IRA is incredible, but it requires the child to have earned income, which most newborns don't.

Trump Accounts thread that needle: no earned income requirement, tax-deferred growth, universal eligibility for eligible U.S.-citizen newborns, and a built-in $1,000 federal seed.

The engine inside is just a low-cost S&P 500 index fund — if you're new to index investing, my Investing Made Simple primer is the place to start.

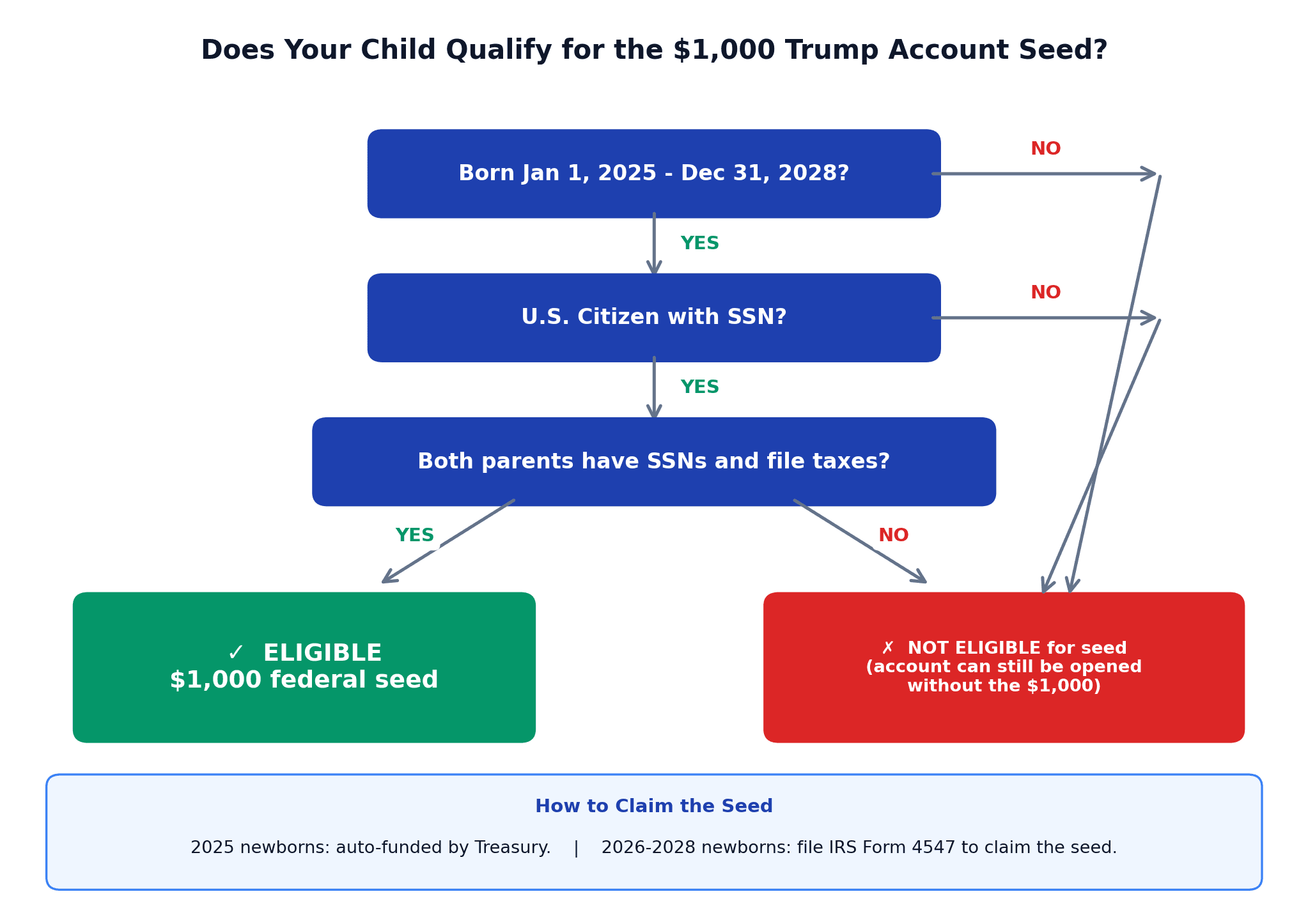

The Free $1,000: Who Qualifies for the Federal Seed

The $1,000 Treasury seed is the headline benefit, and the rules are surprisingly simple.

To qualify, your child must be:

- Born on or after January 1, 2025 and before January 1, 2029 (a four-year pilot window)

- A U.S. citizen at the time of the election

- In possession of a valid Social Security Number

Both parents (or the single filing parent) must also have SSNs and file a federal tax return — ITIN-only filers are excluded. There are no income limits.

For 2025 newborns, Treasury auto-funds the account once your tax return claims the child as a dependent. For 2026, 2027, and 2028 newborns, you have to affirmatively elect by filing IRS Form 4547 ("Trump Account Election(s)"). Three filing options: e-file with your annual tax return (fastest), mail a paper Form 4547, or use form.trumpaccounts.gov.

You can file the election any time before the year your child turns 18, but every year you wait is compounding lost. File as soon as the SSN is issued.

Common questions:

- Twins or triplets? Each child gets their own seed and cap.

- Adopted kids? Yes — domestic and international adoptees qualify, as long as they're U.S. citizens born in the window.

- Green-card holders? No. The child must be a U.S. citizen.

- Kids born before 2025? Account can be opened, but receive no $1,000 seed.

Bonus: the Michael Bonus: the Michael & Susan Dell Foundation has pledged $6.25 billion to add an extra $250 deposit to accounts in qualifying lower-income ZIP codes — automatic if your address qualifies. Susan Dell Foundation has pledged $6.25 billion to add an extra $250 deposit to children.s accounts in qualifying lower-income ZIP codes — automatic if your address qualifies.

The Real 2026 Rules: Contributions, Fees, and Investment Options

Everything beyond the seed follows three numbers: $5,000, $2,500, and 0.10%.

Annual contribution cap: $5,000 per child, combined. Anyone can contribute, but the total across all contributors in a calendar year can't exceed $5,000 for 2026. Indexed for inflation starting 2027.

Employer contribution: up to $2,500/year, tax-free. If your employer sets up a written fringe-benefit plan, the $2,500 is excluded from your gross income — but it counts inside the $5,000 family cap, not on top.

Investment restriction: U.S. equity index funds only. Qualifying investments are mutual funds/ETFs tracking a broad U.S. equity index — VOO, IVV, FXAIX, SPLG. No sector funds. No international. No bonds.

Fee cap: 0.10% expense ratio. A structural advantage — the median active large-cap fund still charges ~0.50%, and many older custodial accounts charge over 1.0%.

Excess contributions: 6% annual excise tax until removed — same penalty as an over-contributed IRA.

How Trump Accounts 2026 compare to the other major child-investment vehicles:

| Account | 2026 Annual Cap | Earned Income? | Tax Treatment |

|---|---|---|---|

| Trump Account | $5,000 family combined | No | Tax-deferred; ordinary income on withdrawal |

| Custodial Roth IRA | $7,500 (or earned income) | Yes | Tax-free growth & qualified withdrawals |

| 529 Plan | No federal cap | No | Tax-free for qualified education |

| UTMA | No cap; $19K/donor gift exclusion | No | Kiddie tax: >$2,700 unearned at parent's rate |

For the full table of adult account limits, see my 2026 Retirement Contribution Rules post.

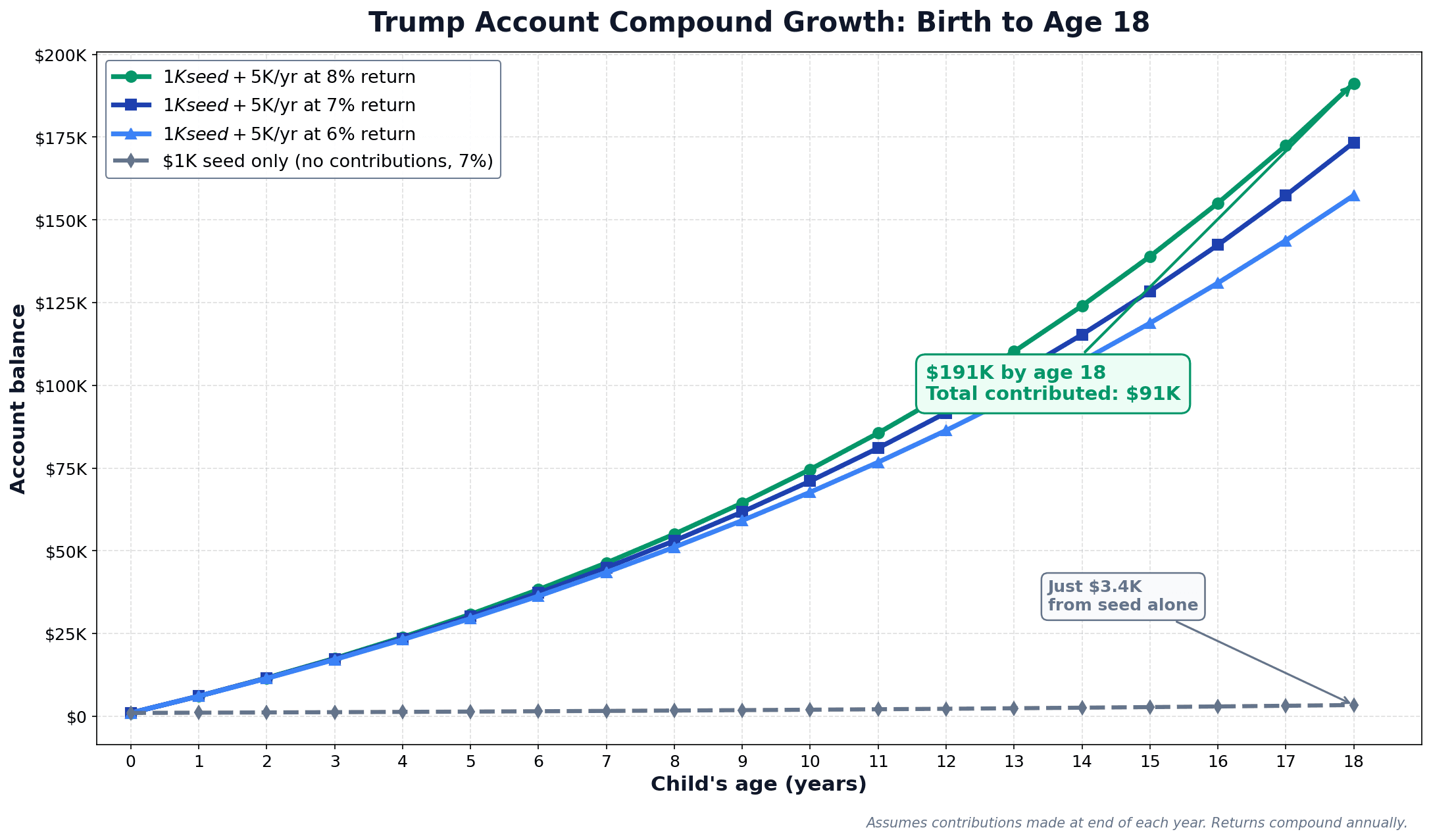

The Compounding Math: $1,000 Today Becomes $191K at 18 and $2.2M at 60

This is where the "baby bonus" framing falls apart completely.

All scenarios assume end-of-year contributions and the 0.10% fee netted out. Returns aren't guaranteed; the S&P 500 has averaged ~9.8% nominal CAGR since 1926, but any 18-year window can land higher or lower.

Scenario A — Seed only ($1,000), no contributions, 18 years:

| Return | Balance at 18 |

|---|---|

| 6% | $2,854 |

| 7% | $3,380 |

| 8% | $3,996 |

| 10% | $5,560 |

Scenario B — $1,000 seed + $5,000/year for 18 years:

| Return | Balance at 18 |

|---|---|

| 6% | $157,383 |

| 7% | $173,375 |

| 8% | $191,247 |

| 10% | $233,556 |

That $191,247 is where the headline comes from — the White House Council of Economic Advisers' model arrived at ~$191,400.

Scenario C — That $191K balance at 18, no further contributions, compounded to age 60:

| Return | Balance at 60 |

|---|---|

| 6% | $2,207,393 |

| 7% | $3,274,553 |

| 8% | $4,839,841 |

| 10% | $10,459,867 |

Read that table again. At a conservative 6% real return, a maxed Trump Account turns into a $2.2 million retirement balance by age 60 — without your child contributing a single additional dollar after age 18. That's a complete Coast FIRE plan funded in the first 18 years of life — my What Is Coast FIRE explainer covers the framework.

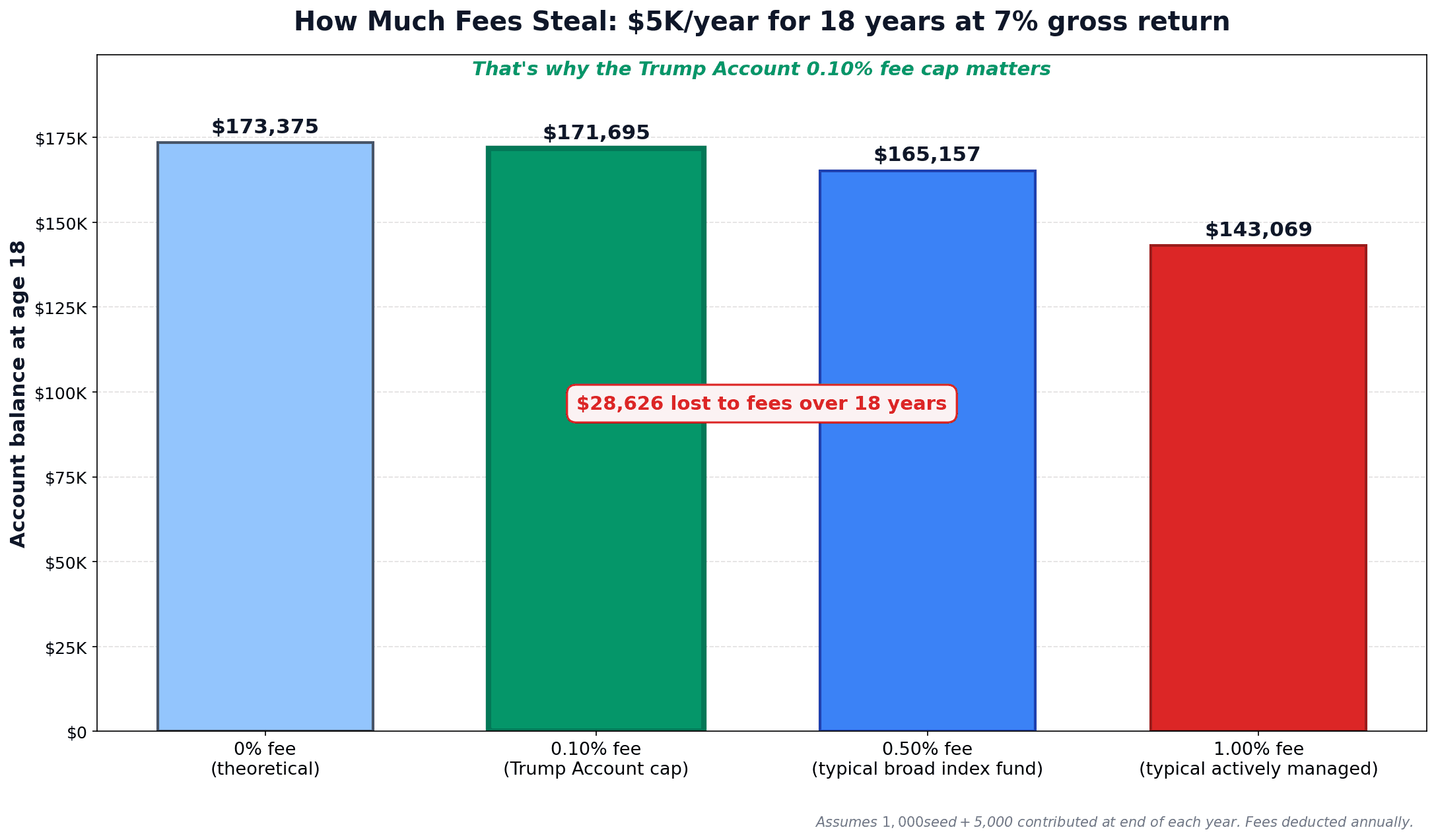

A quick word on why the 0.10% fee cap matters more than it appears:

| Net Return | Final Balance (18 yrs) | Loss vs. 0% Fee |

|---|---|---|

| 7.0% (no fee) | $173,375 | — |

| 6.9% (0.10% fee) | $171,695 | -$1,680 |

| 6.5% (0.50% fee) | $165,157 | -$8,218 |

| 5.0% (1.0% load fund) | $143,069 | -$30,306 |

The 0.10% cap saves roughly $30,000 over 18 years versus the 1% fees common in older legacy custodial accounts.

Trump Account vs. 529 vs. Roth IRA for Kids vs. UTMA: The Decision Tree

The most-asked question since OBBBA was signed: "Do I open this instead of my 529, or in addition to?" Short answer: in addition to. Side-by-side:

| Feature | Trump Account | 529 Plan | Custodial Roth IRA | UTMA |

|---|---|---|---|---|

| Annual cap | $5,000 family | No federal cap | $7,500 / earned income | $19K gift exclusion |

| Earned income required? | No | No | Yes | No |

| Federal seed | $1,000 (one-time) | None | None | None |

| Investments | U.S. index, < =0.10% fee | Age-based, ETFs | Anything | Anything |

| Tax on growth | Tax-deferred | Tax-free if qualified | Tax-free | Kiddie tax >$2,700 |

| Tax on withdrawal | Ordinary income | Tax-free for qualified ed | Earnings 59 1/2 | LTCG rates |

| Withdrawal lockup | Until age 18 | None for qualified ed | Earnings until 59 1/2 | Age of majority |

| FAFSA impact | TBD; likely student | Parent asset (5.64%) | Not on FAFSA | Student asset (20%) |

For a deeper dive into stealth tax-advantaged accounts, my HSA: The Stealth Retirement Account post covers the bucket Trump Accounts now join.

The decision tree I'd give my own family:

- U.S.-citizen child born 2025-2028 with an SSN? Yes → open the Trump Account first, capture the free $1,000 seed. There is no scenario where skipping a free $1,000 makes sense.

- Saving for college? The 529 should still be your primary education vehicle.

- Child has earned income? Max the custodial Roth IRA next.

- Already maxing the 529 and the Roth? Ramp Trump Account contributions toward the $5,000 cap.

- Need flexibility for non-education, non-retirement spending? Use a UTMA (with awareness that it crushes financial aid).

Three Traps Most Parents Will Miss with Trump Accounts 2026

The rules have sharp edges. Three places I expect well-intentioned parents to lose money.

Trap 1: No withdrawals before age 18. Period.

Unlike a 529 (qualified ed expenses anytime) or a UTMA (custodian discretion), Trump Account funds are completely locked until the child's 18th birthday. No tuition. No orthodontia. No medical emergency. The only pre-18 exits: death of the beneficiary, ABLE rollover for a disabled child, or removal of an excess contribution.

Rigid by design. If you're depending on this money for college, use a 529 instead.

Trap 2: After age 18, it becomes a traditional IRA — not a Roth.

When the account converts at 18, it follows traditional-IRA rules. Withdrawals before 59 1/2 generally trigger a 10% penalty plus ordinary income tax. Earnings, the federal seed, and employer contributions are taxed as ordinary income on withdrawal. Only after-tax family contributions come out tax-free.

Ordinary income at the child's adult marginal rate could easily be 22-32% — versus 0-15% LTCG. If you're funding college, a 529 wins. If the plan is retirement (the right move), the IRA conversion is fine — eventual withdrawals are still 41+ years of tax-deferred compounding.

For ideas on what to do with the converted IRA in adulthood, my Monthly Dividend FIRE Strategy 2026 post walks through how to turn a tax-deferred account into monthly cash flow.

Trap 3: Contribution stacking silently kills your headroom.

Multiple contributors share the same $5,000 cap. If you're on auto-deposit at $5,000/year and Grandma writes a $3,000 birthday check, you've triggered the 6% annual excise tax until you remove the excess.

Worse, the $2,500 employer contribution counts inside the $5,000 family cap. So "employer + family" caps parent contributions at $2,500 — not $7,500. Coordinate with grandparents and employer plans before each calendar year.

One uncertainty to flag: Early policy analyses (Morningstar, Tax Foundation) suggest a partial-withdrawal cap may apply between ages 18-25. The IRS final regulations are still pending as of May 2026, so confirm current rules with a tax professional.

How to Open and Fund a Trump Account in 2026 (Step-by-Step)

The practical workflow from "newborn at home" to "first dollar invested."

Step 1: Get the SSN. Apply at the hospital with the birth registration, or file SSA Form SS-5 within the first few weeks. No SSN, no election.

Step 2: 2025 newborns — do nothing. Treasury auto-funds the account once your tax return claims the child as a dependent.

Step 3: 2026-2028 newborns — file IRS Form 4547. E-file with your annual tax return is fastest (TurboTax, H&R Block, FreeTaxUSA all support it). Or paper Form 4547. Or the online portal at form.trumpaccounts.gov.

Step 4: Pick a custodian. Expected at launch: Fidelity, Schwab, Vanguard, JPMorgan Chase, Bank of America. Treasury opens a default account when the seed is issued; transfer afterward if you prefer.

Step 5: Select the index fund. VOO (0.03%), IVV (0.03%), FXAIX (0.015%), SPLG (0.02%) — all track the S&P 500 within a basis point.

Step 6: Auto-contribute. $416.67/month maxes the $5,000 cap, $208.33/month does half. Even $25-50/month adds up over 18 years.

Step 7: Track it alongside your other goals so the compounding curve stays visible.

The FIRE-Style Maximization Playbook

The maximization stack: $1,000 federal seed + $5,000/year from family for 18 years = $90,000 total cash out.

Balance at age 18: $158K (6%), $173K (7%), $191K (8%), $234K (10%).

If left untouched until 60: $1.83M (6%), $2.96M (7%), $4.83M (8%), $10.5M (10%).

That second number should rearrange how you think about retirement planning for your kids. At a conservative 7% return, a maxed Trump Account funded entirely in your child's first 18 years is roughly a $3 million retirement portfolio for them at 60, with zero contributions needed in adulthood.

Compare with the set-and-forget plan — take the $1,000 seed, never contribute another dollar. At 18 (7%): $3,380. At 60 (7%): $57,946. Doing nothing produces $58K for the cost of filing one form. That's the floor; maxed is the ceiling.

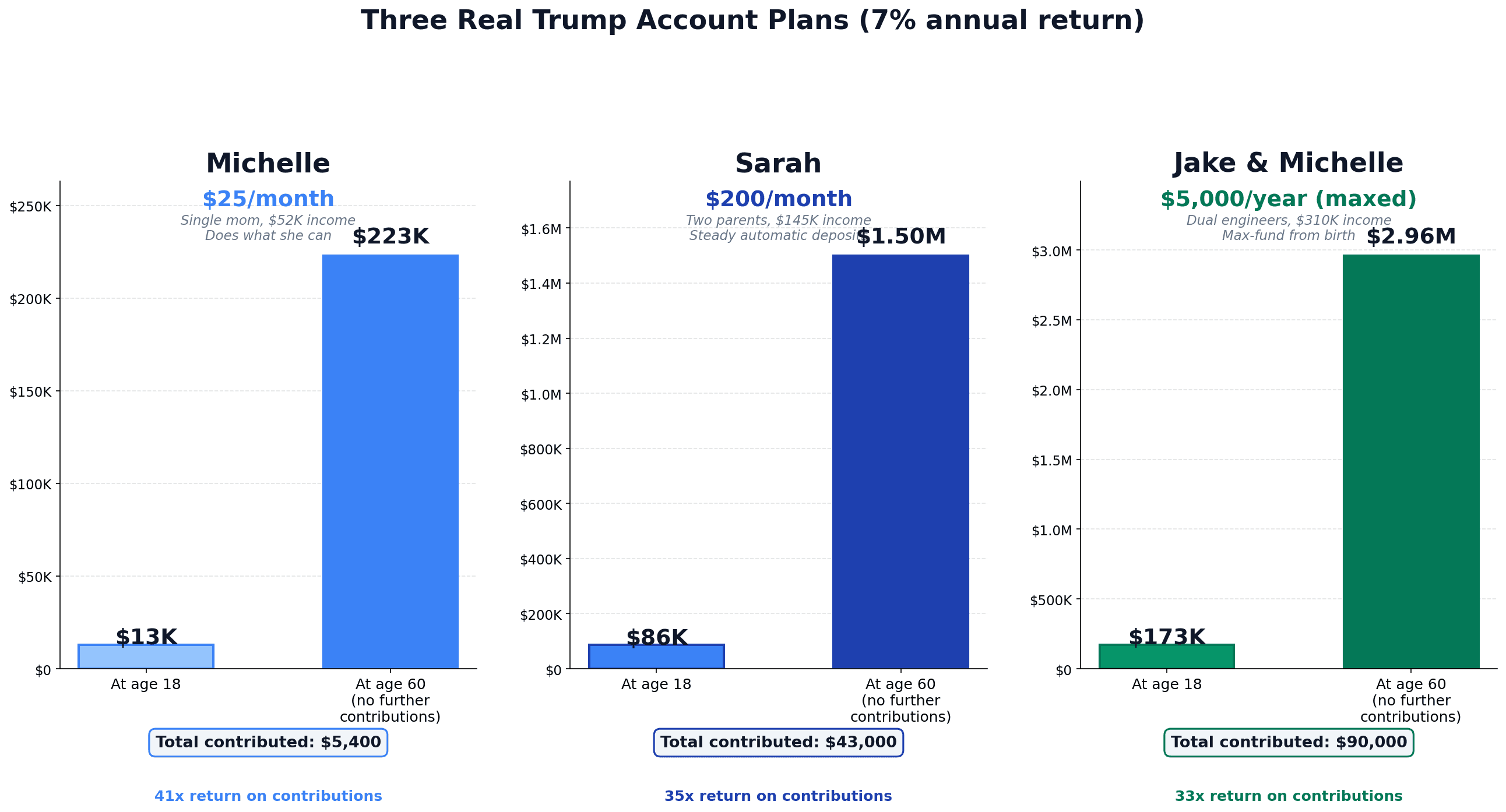

Three real-world examples:

Sarah, teacher, $58K, Columbus OH. Son born March 2026. Sets $200/month into VOO. At 18 (7%): $86,000. Untouched until 60: $1.5M.

Jake & Michelle, dual engineers, $310K, Austin TX. Twins born November 2026. Both accounts max-funded at $5,000/year. Each: $173K at 18, $2.96M each at 60 — nearly $6M combined.

Single mom, $42K, Phoenix AZ. Daughter born February 2027. $25/month. At 18 (7%): $13,000. Untouched until 60: $223,000.

The pattern: the seed is significant on its own. Any contribution is a multiplier. The account is forgiving of inconsistent funding.

Common Questions: Twins, Adopted Children, Stacking with 529s

Rapid-fire FAQ:

- Can I have a Trump Account and a 529 and a custodial Roth and a UTMA? Yes. There's no cross-account conflict. Stacking them is the right move for high-saving households.

- What if my child doesn't need the money at 18? The account auto-converts to a traditional IRA. Leaving it untouched is the most tax-efficient path; partial withdrawals before age 25 are capped at half the 18th-birthday balance (pending final IRS confirmation).

- Can grandparents open the account directly? No — only a parent or legal guardian can establish it, but anyone can contribute (within the shared $5K cap).

- What if I file Form 4547 late, when my kid is 5? The seed is still deposited (assuming eligibility), but you've lost 5 years of compounding.

- Are contributions tax-deductible? No. Family contributions go in with after-tax dollars. Only the employer's $2,500 portion is tax-deductible to the employer and tax-free to the employee.

- Is the seed taxable income to the child? No, the $1,000 seed is not taxable when received. It's taxed as ordinary income later when withdrawn.

Bottom Line on Trump Accounts 2026: Open One the Day It Launches

The verdict is genuinely simple, with a few qualifications.

For any U.S.-citizen child born 2025-2028: yes, open it. The $1,000 seed is essentially free government-funded compounding. The cost is one IRS form. Not opening means leaving money on the table.

For higher-income parents already maxing 529s and Roths: open it for the seed, then prioritize tax-free vehicles (529 for education, Roth IRA for retirement) before piling more into the Trump Account. It becomes your tier-three tax-advantaged bucket.

For lower- and middle-income families: the $1,000 seed alone, untouched at 7%, becomes ~$58,000 by age 60. That's a meaningful gift. Don't stress about the $5K cap.

For FIRE-minded parents: maxing this from birth is the single highest-leverage retirement-funding move you can make for your child. They'll have a Coast-FIRE-funded retirement before they finish high school.

Trump Accounts 2026 are the first new federal tax-advantaged account class in 23 years. Whatever you think of the politics, the financial mechanics are too good to ignore for any eligible family. Get the seed. Pick the cheapest qualifying index fund. Set an auto-deposit you can sustain. Then let compounding do its job for 18 years.

If you want to track the new account alongside your FIRE goal, your 529, your HSA, and the rest of your financial picture in one place, that's what My Financial Freedom Tracker is built for. Add it as a custodial sub-goal the moment you file Form 4547.

The $1,000 baby bonus is the headline. The $191,000 by 18 — and $2.2 million by 60 — is the real story. Go file the form.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Learn To Invest

Learn To InvestBitcoin in Your 401(k)? What the 2026 DOL Rule Really Means

The 2026 DOL rule doesn’t put Bitcoin in your 401(k) by itself. The real risks, three ways crypto can enter your plan, and how much (if any) to hold.

Learn To Invest

Learn To InvestMonthly Dividend Income Strategy: Build Predictable Cash Flow for FIRE in 2026

Monthly dividend income strategy builds predictable cash flow for early retirees, covering 40-60% of living expenses before Social Security while reducing sequence-of-returns risk. Three-tier approach: dividend aristocrats (60%), dividend ETFs like SCHD (25%), and high-yield specialists (15%) generate $1,600-$2,500/month on a $600K portfolio.

Learn To Invest

Learn To InvestHSA Retirement Strategy: The Triple Tax Advantage (2026)

The HSA is America’s only triple-tax-advantaged account. How FIRE savers turn it into a stealth retirement fund — 2026 limits, the receipt hack, 65+ rules.

Learn To Invest

Learn To InvestPay Off Mortgage or Invest? The Math vs. the Psychology

Pay off the mortgage or invest the difference? The math favors stocks; psychology favors the house — homeowner net worth is $400K vs $10K for renters.

Learn To Invest

Learn To InvestDo Stocks Always Go Up? The Truth That Will Surprise You

Same market. Same stocks. The only difference? How long you looked. See why 95% of investors who hold for 10+ years never lose money — and why those who panicked in 2020 lost hundreds of thousands.