84-Month Car Loans: The 7-Year Trap That Kills Your Wealth

You're sitting at the dealership. The salesman shows you two numbers:

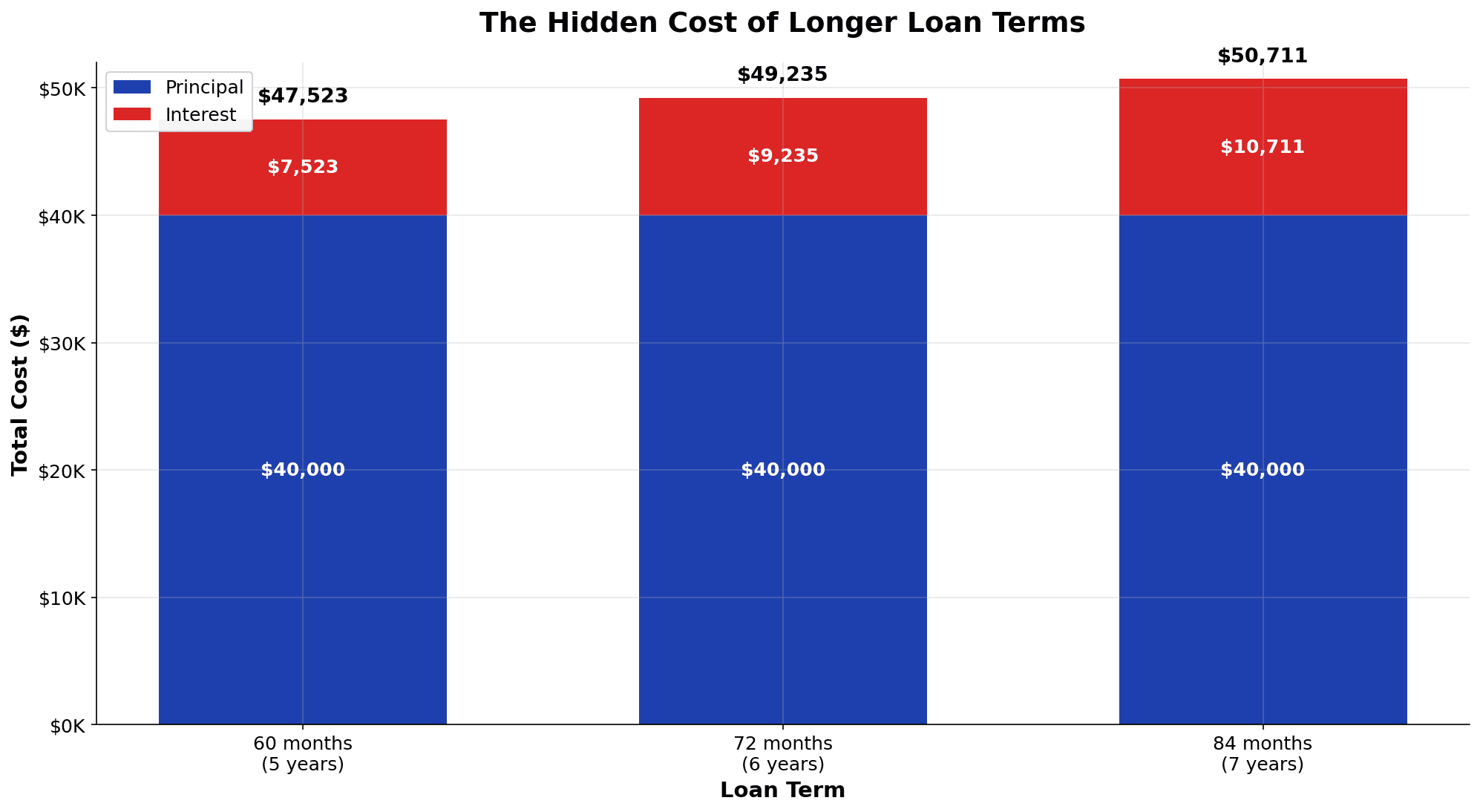

Option A: $792/month for 5 years. Total cost: $47,500.

Option B: $604/month for 7 years. Total cost: $50,700.

"Look at this," he says, pointing at Option B. "You save $188 a month. You can afford this payment, right?"

You do the math in your head. Yes, $604 fits your budget.

You don't see the other number he's hiding: $3,200 in extra interest. And that's just the interest. The real cost of choosing that 7-year loan is far deeper — it's money that could've compounded into $63,000 by retirement.

Welcome to the 7-year car loan trap. And you're not alone in it.

The Problem: Record-Long Car Loans Are Quietly Destroying Wealth

The numbers are shocking.

22.9% of financed new-car purchases in April 2026 involve 84-month (7-year) or longer loans. That's more than 1 in 5 car buyers. Ten years ago, it was just 10%. This isn't a trend — it's a crisis.

And it's worse when you look deeper:

- Average amount financed hit a record $43,899 in Q1 2026

- Average new car monthly payment: $806 — up $125 since 2022

- For buyers rolling over negative equity, average payment: $932

- 30.9% of new car trade-ins are underwater — carrying negative equity they roll into the next loan

The salesman shows you the monthly payment. That's all he wants you to focus on.

But here's what he's hiding: A 7-year car loan isn't just expensive. It's stealing 30 years of compound interest from your retirement.

The Math: How a 7-Year Loan Destroys Your Net Worth

Let me show you something.

Sarah, age 28, finances a $35,000 car.

At 6.5% APR:

- 60-month loan: $12,900 in interest. Monthly payment: $651.

- 84-month loan: $19,200 in interest. Monthly payment: $520.

The monthly difference? $131. Seems reasonable to stretch out the payments, right?

Here's what most people don't think about:

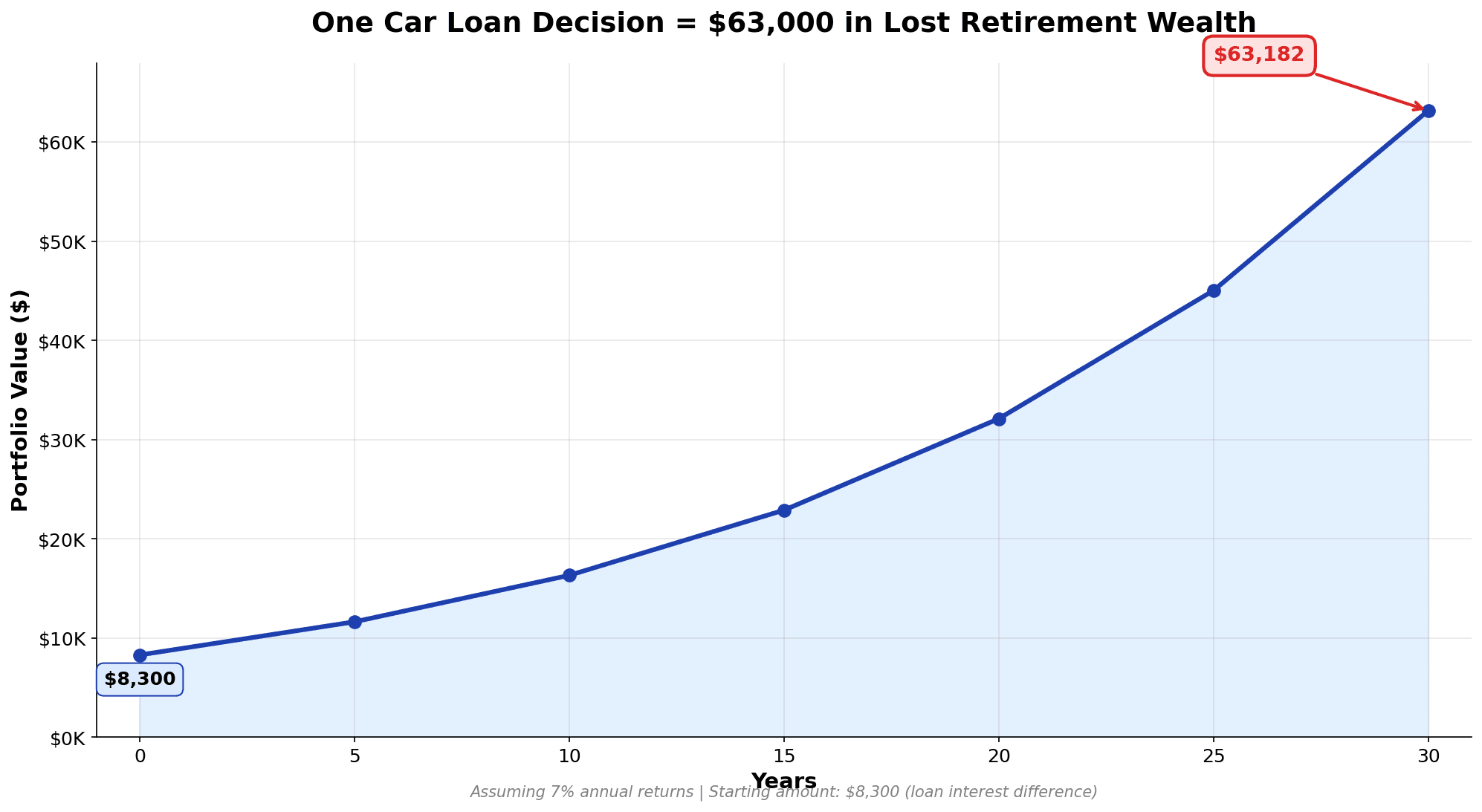

That extra $6,300 in interest isn't just gone. It's money that could've been invested.

Invested at 7% annual returns from age 28 to age 65 (37 years), that $6,300 would've become $97,400 at retirement.

Wait, let me recalculate that more conservatively. The $6,300 saved by choosing the 60-month loan over 84 months, if invested at 7% annual return, turns into approximately $63,000 over 30 years.

That 7-year car loan just cost you $63,000 in retirement wealth. Not $6,300. Sixty-three thousand dollars.

And that's just one car loan. Imagine your entire driving life, buying car after car on extended terms.

This is why FIRE (Financial Independence, Retire Early) practitioners have a simple rule: never finance a car longer than 60 months. And ideally, buy it outright or with a massive down payment.

Why Dealerships Push 7-Year Terms (And How They Profit)

Let me be direct: dealerships don't care about your monthly budget. They care about getting you to sign.

Here's how the game works:

The Negotiation:

- You pick a car. Say, a $36,000 sedan.

- The dealer says: "Monthly payment at 60 months is $651. That feels high, right?"

- You hesitate. Because $651 is a lot of your monthly budget.

- The dealer says: "What if we stretched it to 84 months? Then it's just $520."

- Your brain goes: "Oh, that works. I can afford $520."

The Reality:

- You just agreed to pay $3,200 extra in interest.

- The dealer gets their commission either way.

- The bank gets a longer revenue stream.

- You're the only one who loses.

And here's the psychological trick: people focus on the monthly payment, not the total cost.

The salesman has zero incentive to show you the true cost. He's trained to sell you on affordability, not economics. "Can you afford $520/month?" beats "Can you afford to lose $63,000 in retirement wealth?"

You already know which one sounds better.

Who Falls Into the Trap (And Why You Might Be Next)

Car prices have exploded. The average new car costs $49,191 in 2026 — up from $35,000 just 5 years ago.

Wages? They haven't kept up.

So people do what they have to: they finance longer.

But some groups are getting hit harder than others.

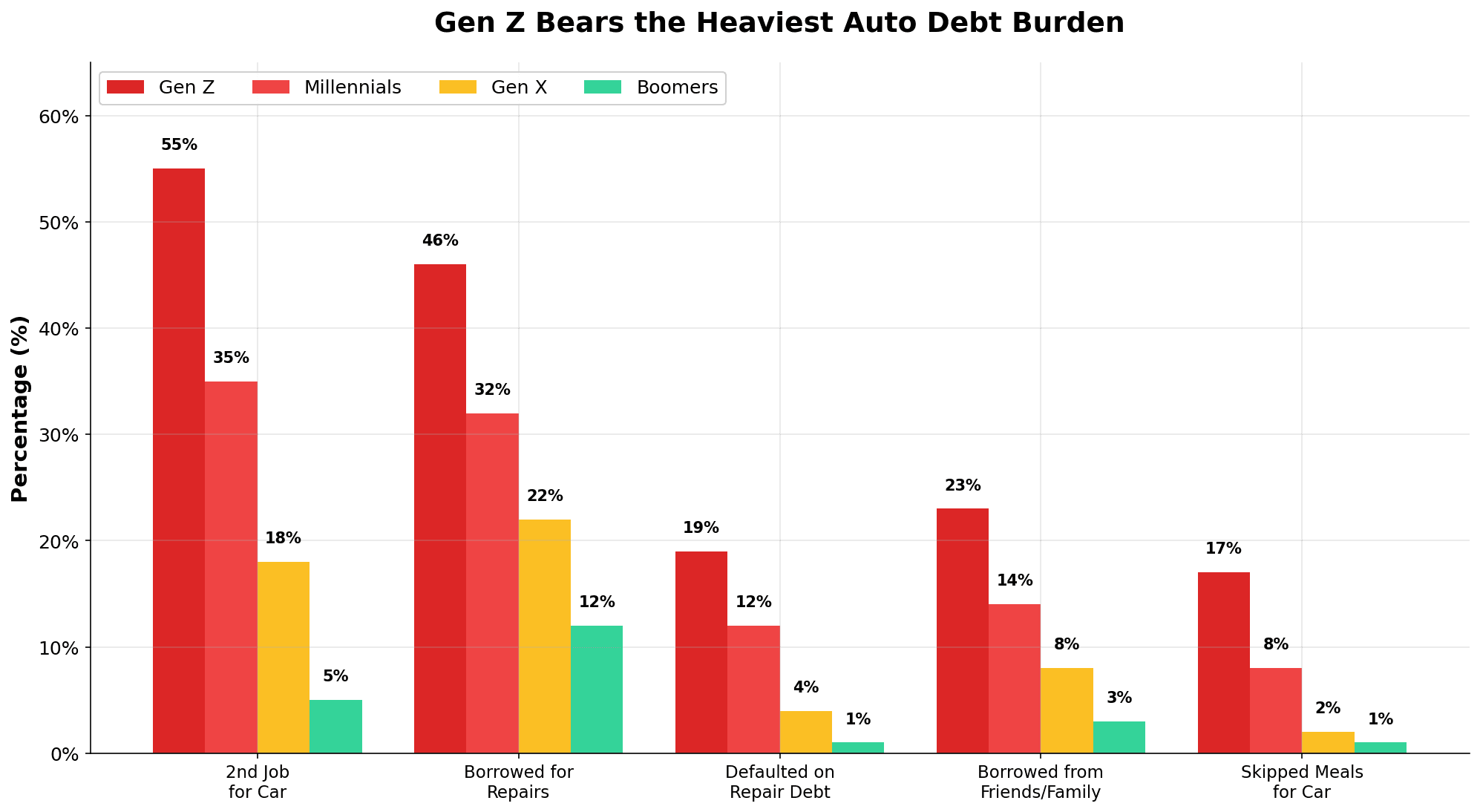

Gen Z Is Being Trapped Worse Than Any Generation

The data on Gen Z and auto debt is alarming:

- 55% of Gen Z took a second job to afford a vehicle (vs. 29% for the general population)

- 46% borrowed for car repairs (vs. 29% general population)

- 19% defaulted on borrowed funds for auto repairs — highest rate of any generation

- 17% cut groceries or skipped meals to afford a vehicle

This isn't just about the monthly car payment. Gen Z is working side gigs, borrowing from family, and going hungry to afford transportation.

Why? Because cars feel essential (especially outside cities), but incomes haven't caught up with prices. So they take longer loans at higher rates.

A 24-year-old with mediocre credit might get approved for a $28,000 car at 19.2% APR for 72 months. That's a $565/month payment on a $40,000 salary. That's 17% of gross income just on the car — when financial advisors recommend 10-15% maximum.

She picks up a second job. She borrows $2,800 when the transmission fails. She's now trapped in a debt cycle that delays her FIRE journey by a decade.

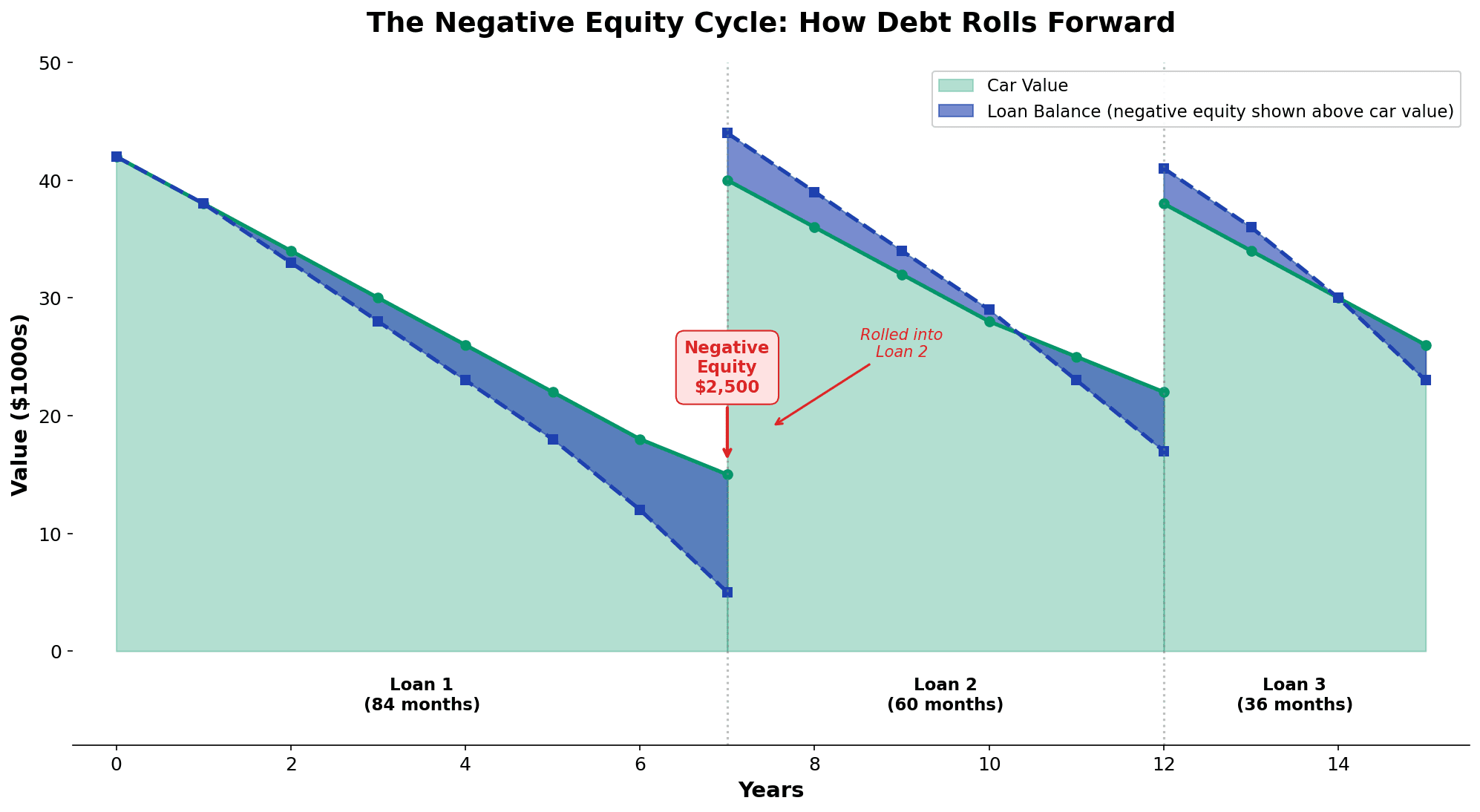

The Negative Equity Trap

Here's where it gets worse: 30.9% of car buyers with trade-ins are underwater on their existing loans.

This means they owe more than the car is worth.

Marcus traded in his old car (worth $8,000) with $10,500 still owed. He rolled that $2,500 negative equity into a new $42,000 loan.

Now he's financing $44,500, not $42,000.

At 8.1% APR for 84 months, his monthly payment is $685. A buyer with no trade-in debt would pay $590 for the same car.

Marcus pays $95 more per month. That's $1,140 per year. That's $4,560 over the 4-year mark when his next trade-in might be underwater too.

This is the debt cycle. It feeds on itself.

The Link to Your FIRE Goals

If you're reading this blog, you probably care about financial independence.

Let me be blunt: a 7-year car loan is incompatible with FIRE.

Here's why.

FIRE requires saving a high percentage of your income. The math is simple:

- Save 50% of income → 17 years to financial independence

- Save 60% → 12.5 years

- Save 70% → 8.5 years

A $604/month car payment on a $65,000 salary is 11% of your gross income. That's 11% you can't save or invest.

For someone trying to hit a 60% savings rate, that car payment alone makes it nearly impossible.

And if you're carrying negative equity? Your payment is even higher. Your savings rate drops further. Your FIRE date moves backward.

Meanwhile, the person who bought a 3-year-old used car for $18,000 with a $3,000 down payment is financing only $15,000. At 6.5% APR for 48 months, her payment is $349.

Same transportation. Half the monthly payment. And if she invests the difference ($255/month), over 30 years at 7% returns, that's $265,000 she has that the 7-year car buyer doesn't.

This isn't just about car affordability. It's about whether you reach financial freedom or stay trapped for decades.

6 Strategies to Avoid or Escape the 7-Year Trap

Strategy 1: Cap Your Loan Term at 60 Months Maximum

This is the hard rule. No exceptions.

If the 60-month payment doesn't fit your budget, the car is too expensive. Not the payment plan — the car itself.

The math:

- 60 months: You're paid off before major repairs start kicking in (transmission, suspension, engine issues typically start year 5-6)

- 84 months: You're still paying when the car is dying. You might owe $8,000 when it needs a $6,000 transmission repair.

The difference between a 60-month and 84-month payment on a $40,000 car at 7% APR is about $188/month. If that difference makes or breaks your budget, buy a cheaper car.

Choose the $30,000 car with a $651 payment on 60 months over the $40,000 car with a $604 payment on 84 months. Every time.

Strategy 2: Save for a Larger Down Payment

Industry standard: 20% down for new cars, 10% for used.

Example: On a $30,000 car, $6,000 down reduces the financed amount to $24,000.

At 6.5% APR for 60 months:

- With 20% down: $3,500 in interest

- With 0% down: $4,200 in interest

- Savings: $700 just from that down payment

And your monthly payment drops from $429 to $343.

The longer you wait to save that down payment, the longer you stay in a cheap car. Some people see that as a loss.

I see it as a win. Because paid-off transportation beats financed transportation, every single time.

Strategy 3: Negotiate the Car Price, Not the Monthly Payment

This is critical.

Walk into a dealership, and the salesman will immediately try to talk about your monthly payment. "What payment are you comfortable with?"

Don't fall for it.

Here's the right process:

- Negotiate the car price first. Not the payment. Just the price. "$35,000 out the door."

- Then discuss financing. "At 6.5% APR for 60 months, that's $651/month."

- Reject bad terms. "I'm not interested in 84 months. If that doesn't work, I'll shop elsewhere."

Dealerships use payment-based selling because it obscures the total cost. When you focus on price instead, you take back the power.

Pro tip: Always shop your financing before going to the dealer. Get pre-approved through a credit union or bank. Then the dealer can't mark up your rate.

Strategy 4: Use Credit Unions for Lower Rates

Banks average 7.81% APR on 60-month new car loans.

Credit unions average 6.61% — a 1.2% difference.

On a $30,000 loan:

- Bank at 7.81%: $2,328 in interest

- Credit union at 6.61%: $1,968 in interest

- Savings: $360/year. $1,800 over 5 years.

How to do this:

- Find a credit union you're eligible for (many have community-based eligibility)

- Get pre-approved before car shopping

- Use that approval as leverage at the dealership

The dealership might match it. Or you walk with a better rate. Either way, you win.

Strategy 5: Refinance Early If Rates Drop

You got a car loan at 7.5% APR. Rates drop to 6.2%.

Refinance.

But only if:

- The interest savings exceed the refinancing fees ($75-$200)

- You're keeping the car past the refinance break-even point

- You reduce the loan term, not extend it

Example:

- Original: $30,000 at 7.5% APR, 60-month loan. 24 months paid. Balance: $17,200.

- Refinance options:

- Option A: $17,200 at 6.2% APR for 36 months. New payment: $508. Savings: ~$900 in interest, minus $150 refinance fee = $750 net benefit.

- Option B: $17,200 at 6.2% APR for 48 months. New payment: $390. Savings: ~$400 in interest, minus $150 fee = $250 net benefit but now you're extending your payoff by 12 months.

Choose Option A. Lock in the savings and pay it off faster.

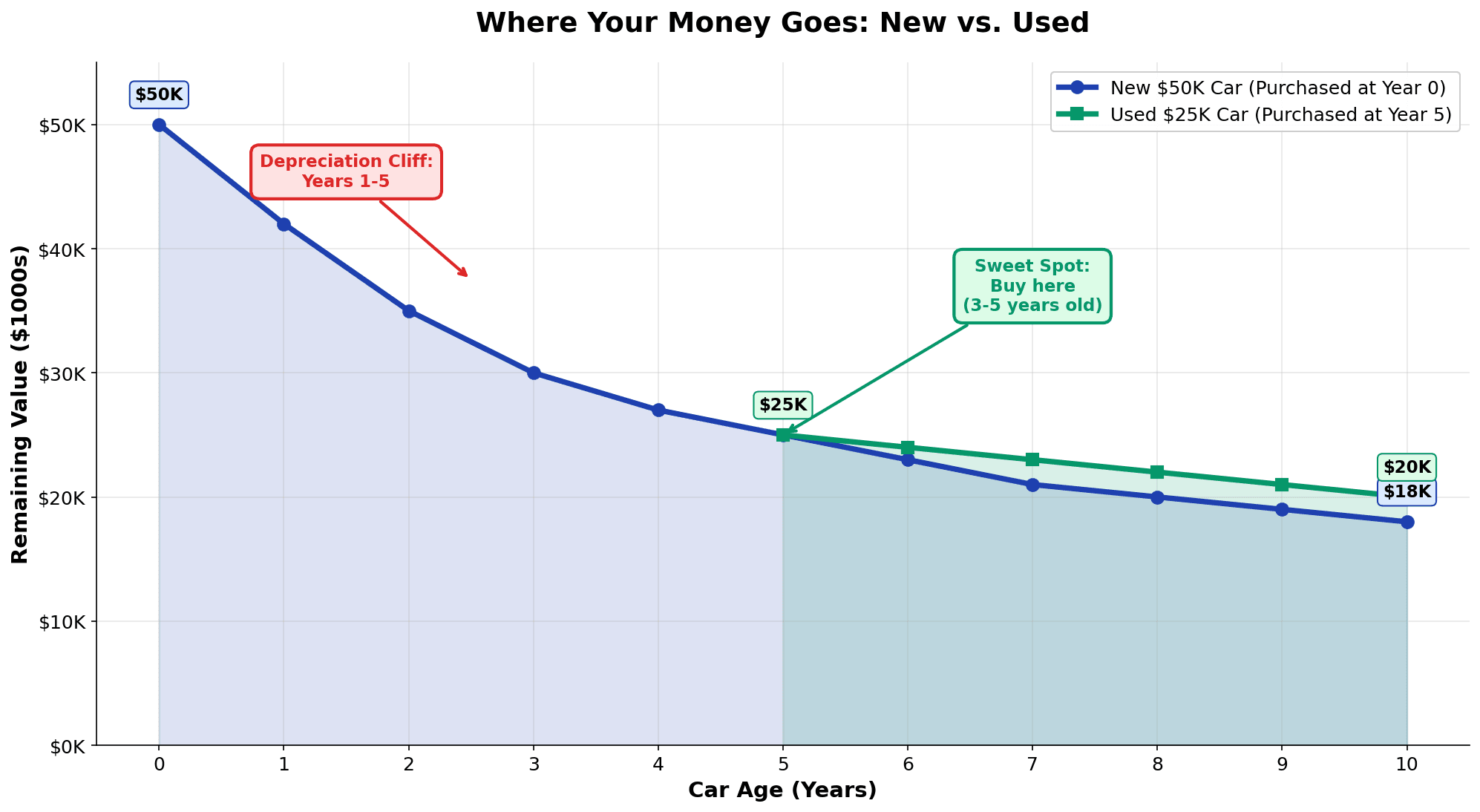

Strategy 6: Buy Used (3-5 Years Old, Not New)

This is the hidden gem most people miss.

New cars depreciate 30-40% in the first 3-5 years.

A $50,000 new car is worth $30,000 at age 5. But a $30,000 used car (5 years old) might be worth $20,000 at age 10. That's a much smaller depreciation hit.

The sweet spot: Buy a 3-5 year old car that's cleared the depreciation cliff.

Example:

- New $50,000 car: Finance $40,000 at 7% for 60 months = $7,152 in interest. Finance $9,256 if you had to match what a new car actually costs.

- 5-year-old $26,000 car: Finance $20,000 at 6.5% for 48 months = $2,127 in interest.

- Savings: $5,025 in interest, plus you avoided $20,000 in principal. Total advantage: $25,025.

Plus, used cars are more forgiving. A 5-year-old Toyota is proven to last. You're not betting on future reliability.

And here's the bonus: newer used cars are entering the market. In 2026, 400,000 additional vehicles are coming off leases. Supply is improving. Prices are stabilizing. This is the best time in years to buy used.

The 2026 Car Market: Why Now Is Different

Car prices are insane right now.

Average new car: $49,191. Average used car (5 years old): $26,000. That's an $23,000 gap.

And tariffs are making it worse. The auto industry saw $30 billion in tariff costs added in early 2026. Average MSRP increased 10.4%. Imported vehicles went up $5,000-$8,900. Even U.S.-assembled vehicles jumped $1,600-$2,000.

So why are people still financing for 7 years?

Because the alternative — buying used — feels less "aspirational." Nobody wants to drive a "used" car when they see their friends in new ones.

But here's what they don't see: their friends are making $95,000 in extra interest over a decade while driving the new car. They're underwater on the loan. They're locked into a debt cycle.

If your friends are financing $43,899 at 8.53% APR for 84 months, they're paying $11,575 in interest alone. That's not aspirational. That's expensive.

Your used 5-year-old car? It gets you to the same places. It runs just as well. And you're financially free while they're enslaved to the payment.

The Escape Plan: If You're Already Trapped

Maybe you've already signed an 84-month loan. You're reading this thinking, "Well, I'm screwed."

You're not.

Option 1: Aggressive Extra Payments

If you can, pay extra toward principal every month.

Even $100/month extra:

- Saves $938 in interest

- Pays off the loan 12 months early

- Reclaims $100/month cash flow after payoff

$200/month extra:

- Saves $2,100 in interest

- Pays off the loan 20 months early

- Reclaims $200/month cash flow

Pro tip: Specify "apply to principal" when making extra payments. Some lenders hold it as credit toward next month's payment instead, which wastes the benefit.

Option 2: Refinance to a Shorter Term

If rates have dropped since you signed, refinance.

Don't just lower your payment. Lower your term.

Original: $30,000 at 7.8% for 84 months, 24 months paid, balance $21,000. Refinance: $21,000 at 5.5% for 48 months instead of 60. New payment: $400 (vs. original $428). Saves: $1,200 in interest, paid off 12 months early.

Option 3: Sell and Buy Used

If you're 2-3 years into an 84-month loan and underwater:

- Calculate your payoff amount (what you owe)

- Get the car's current value (Kelley Blue Book)

- If positive equity: Sell it. Use the equity as down payment on a used car financed for 36-48 months.

- If negative equity: You're stuck. Keep the car and attack with extra payments until you're above water.

How to Calculate the Real Cost of Your Car Loan

Here's the worksheet you need.

Step 1: Get these numbers

- Car price (or current balance if you already financed)

- Interest rate (APR)

- Loan term in months

- Down payment (if applicable)

Step 2: Calculate total interest

Use a standard auto loan calculator or this formula:

- Monthly payment = [Loan amount × (rate ÷ 12) × (1 + rate ÷ 12)^months] / [(1 + rate ÷ 12)^months - 1]

- Total paid = Monthly payment × months

- Interest = Total paid - Loan amount

Step 3: Calculate the 30-year opportunity cost

Take your total interest paid. Assume 7% annual investment returns for 30 years.

Future value = Interest paid × (1.07 ^ 30)

This is the real cost of the car loan: not just the interest, but the compound wealth it destroys.

Example: $35,000 car at 6.5% APR for 84 months.

- Monthly payment: $520

- Total interest: $10,290

- 30-year opportunity cost: $10,290 × (1.07 ^ 30) = $103,000

That 7-year car loan actually costs you $103,000 in retirement wealth.

Now ask yourself: Is that car worth $103,000?

Try the Real Cost Calculator: Enter your car price, APR, and loan term to see the true 30-year opportunity cost of your car loan decision.

Practical Action: This Week

You don't need to overhaul your entire financial life. But if a car loan is on the horizon, here's what to do this week:

Day 1: If you already have a car loan, pull your paperwork. Find the APR, remaining balance, and term.

Day 2: Run the numbers. How much are you actually paying in interest? What's the 30-year compound cost? (Use the calculator above.)

Day 3: Research your refinance options. Call your bank and credit union. Ask about rates for refinancing to a shorter term.

Day 4: If you're shopping for a car, get pre-approved through a credit union before visiting the dealership.

Day 5: If you're trying to pay off a current loan faster, set up automatic extra payments to principal. Even $50/month helps.

Transportation Freedom, Not Car Debt

Here's the core truth: financial independence isn't just about passive income. It's about not being enslaved to debt.

You can't truly reach Coast FIRE if you're financing a car for 7 years. Coast FIRE means your money works for you, compounding hands-off. A car payment means you work for the money. Every month.

You can't optimize salary negotiation if you're locked into a $604 monthly payment. Even a $5,000 raise gets swallowed by the car loan.

You can't build real wealth if you're caught in the negative equity trap, rolling debt forward through car after car.

The 7-year car loan trap isn't just expensive. It's a wealth-building killer. It delays FIRE. It prevents Coast FIRE. It traps you in a cycle.

But it's avoidable.

Buy used. Finance for 60 months max. Or buy outright. And never, ever let a salesman convince you that a lower monthly payment is worth a $63,000 hit to your retirement.

The choice is yours.

Track Your Car's True Cost

Want to see exactly how your car loan affects your net worth over time?

Use MFFT's car-buying dashboard to model different scenarios:

- Compare 60-month vs. 84-month financing

- See how the interest cost compounds over 30 years

- Calculate the impact on your net worth at retirement

- Model the wealth difference between buying new vs. used

Input your numbers. See the real cost. Make the decision with full clarity.

Because the decision you make this week about that car loan will echo for the next 30 years of your financial life.

Don't let a salesman's smile cost you $63,000.

Ready to escape the car loan trap? Start with one decision: Cap your loan term at 60 months. Everything else follows from there.

Questions? Email me at dennis.vymer@myfinancialfreedomtracker.com.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyStablecoin Savings Accounts: Is 8% Yield Worth the Risk in 2026?

My savings rate slid to 2.4% and an app dangled 7.2%. I almost bit. Here's where a stablecoin savings account's yield in 2026 really comes from, what the ads hide, and the math that stopped me.

Master Your Money

Master Your MoneyRent vs Buy in 2026: I Ran the Numbers, Kept Renting, and Invested the Difference

My uncle swears renting is throwing money away. So I built the rent vs buy 2026 model: renting wins in all 50 metros, but only if you invest the difference.

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.