Credit Card Interest at 20%+: The 3-Tier Escape Plan (2026)

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Build Wealth From Zero — the equation that explains wealth multiplication

- How to Start a Budget — escape paycheck-to-paycheck living

- How to Start a Budget — the foundation of money management

You open your credit card app.

You see the balance: $5,000.

Your minimum payment: $120.

You think to yourself: "That's manageable. I can handle that."

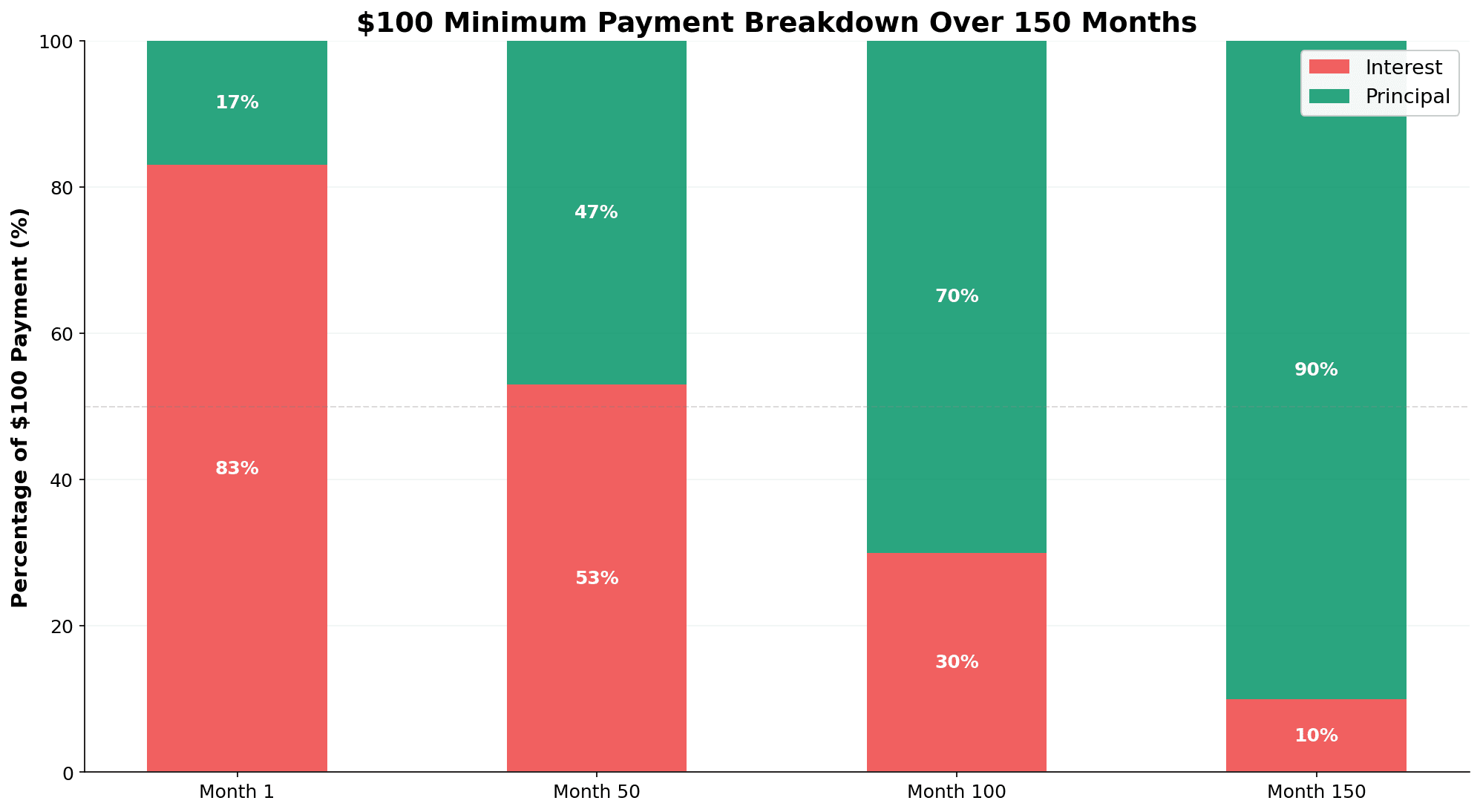

Here's what you don't know: of that $120, roughly $83 goes to interest alone. Only $37 touches your actual debt.

And at that rate, you'll spend nearly $12,000 total to pay off that $5,000 balance.

This isn't a personal finance article about "budgeting better." This is about something darker: the mathematical trap designed to keep you poor, and why Americans are spending more on credit card interest than on their mortgages.

The Shock: 40% of Americans Are Trapped in a 20%+ Interest Rate Nightmare

Let me give you the numbers that nobody talks about.

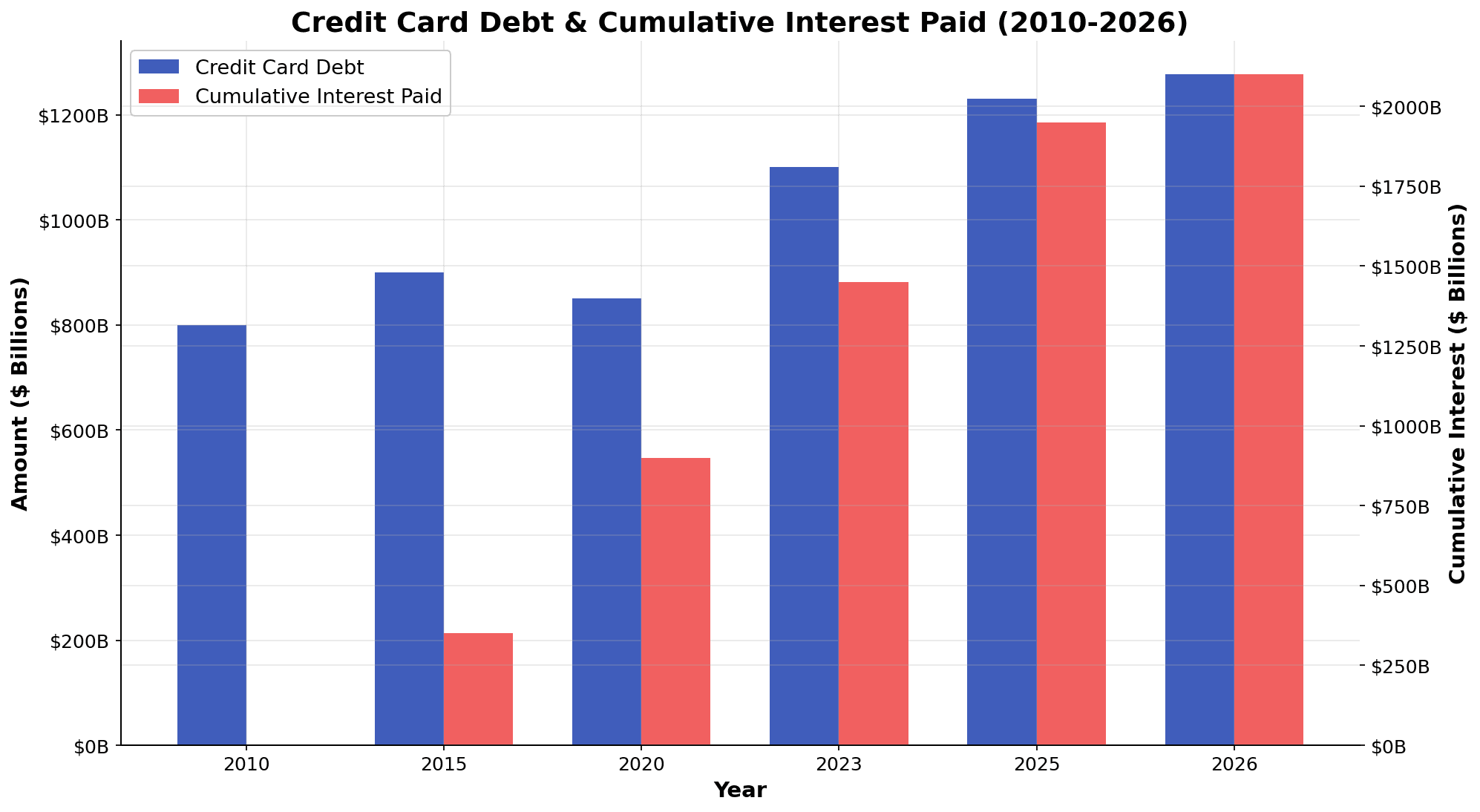

$1.277 trillion. That's the total credit card debt owed by Americans right now. It's the highest amount ever recorded since the Federal Reserve started tracking in 1999.

But here's the part that should terrify you:

Americans have paid $2.1 trillion in credit card interest since 2010. More than auto loans. More than most student loans. Just pure, wasted interest.

Here's what's happening:

- 40% of U.S. adults can't pay off their credit card balances and carry debt month-to-month

- 50.5% of all active cardholders are carrying a balance instead of paying it off each month

- Average balance per cardholder: $6,523 (and climbing)

- Average credit card interest rate in April 2026: 20.97% APR for existing accounts, 22.08% for new offers

- 29% of Americans carry over $10,000 in credit card debt (up from 23% just a year ago)

And maybe the most damning stat: 22% of Americans believe they'll never escape credit card debt. Not financially—psychologically. They've given up.

Let me connect this to you personally.

If you're carrying $6,500 in credit card debt at 21% APR (the average), you're paying $1,365 per year just in interest. That's $114 a month. Money that vanishes. Money that doesn't reduce your debt. Money that goes to a credit card company's profit margin.

Over 10 years, that's $13,650 in pure waste.

The Math Nobody Explains: How Daily Compounding Traps You

This is where I need to show you exactly how you get trapped.

Credit card interest isn't simple. It's compound daily. That matters more than you think.

Let's use a real example: $5,000 balance at 20% APR.

Here's what the minimum payment looks like:

| Month | Balance | Min Payment | Interest Charge | Principal Paid | New Balance |

|---|---|---|---|---|---|

| 1 | $5,000 | $100 | $83 | $17 | $4,983 |

| 2 | $4,983 | $100 | $83 | $17 | $4,966 |

| 12 | $4,800 | $100 | $80 | $20 | $4,780 |

| 24 | $4,500 | $100 | $75 | $25 | $4,475 |

| 60 | $3,200 | $100 | $53 | $47 | $3,153 |

Do you see what's happening?

After 60 months of payments (5 years), you've paid $6,000 into a $5,000 debt, and you still owe $3,153. You've made zero progress. You've been servicing interest, not debt.

At a $100/month minimum payment, this $5,000 debt doesn't actually disappear until you've paid roughly $12,500 total — roughly 2.5x the original amount.

And here's the cruel part: once you hit month 70 or 80, your minimum payment stops decreasing because the card issuer's algorithm keeps you on a slow burn. You feel like progress is happening. It's not.

This is called the minimum payment trap, and it's the primary weapon credit card companies use to keep you enslaved.

Why Rates Climbed to 20%+ (And Why Fed Cuts Won't Save You)

This is the part where the Fed's policy matters, but not in the way you think.

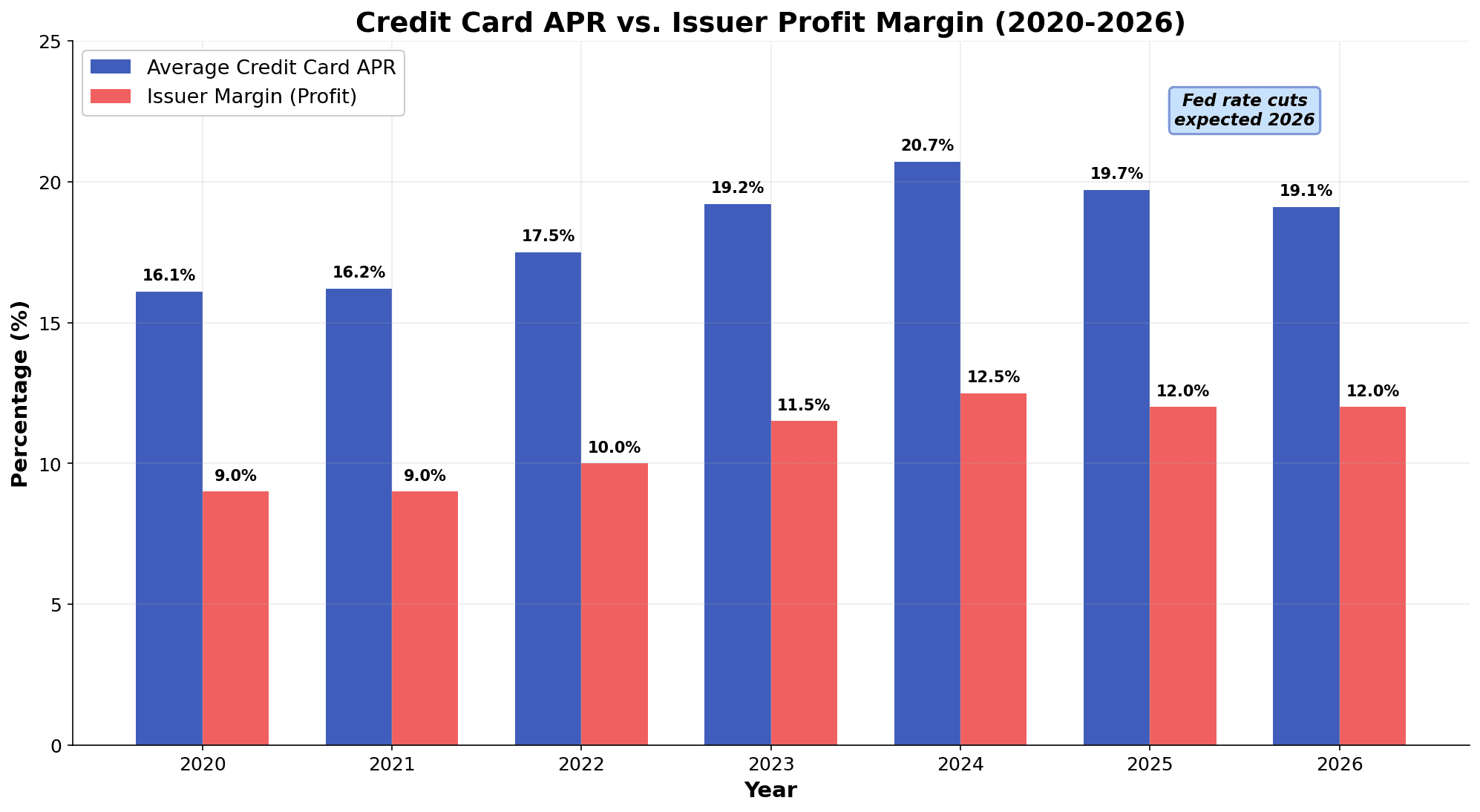

In 2020-2021, credit card rates hovered around 16% APR. They were bad, but manageable.

Then the Federal Reserve started hiking rates aggressively to fight inflation. Credit card rates climbed: 17% → 19% → 20% → 21% → hitting an all-time high of 20.7% in August 2024.

Here's what you need to know: credit card companies have chosen not to pass through Fed rate cuts.

The Fed is expected to cut rates 3 times in 2026 — roughly 0.75 percentage points total. But industry analysts project credit card rates will only fall to around 19.1% by year-end.

Why the disconnect?

Because credit card companies expanded their profit margins during the rate hike cycle, and they're keeping those extra profits instead of passing cuts to borrowers.

Before 2022, the card issuer's margin (their profit on every dollar of APR) was around 9%. By 2024, it had expanded to 12%+. As of 2026, margins have stayed at 12%, not shrunk back.

This means: even if the Federal Reserve cuts rates, your APR won't fall proportionally.

Banks are choosing higher profits over customer relief. And unless legislation changes, this is the new normal.

Why You Can't Escape: The Psychological Trap

Here's something credit card companies understand better than you do: math is easier to ignore than feelings.

The minimum payment feels manageable. It's low enough that you don't feel the full weight of your debt. Your brain tricks you into thinking you're making progress when you're barely moving.

This is called anchoring bias. The minimum payment becomes your psychological anchor. As long as you can make it, you feel okay.

But here's the trap within the trap:

Every time you make that minimum payment, your brain releases a dopamine hit. You paid. You did the right thing. Everything is fine.

Except it's not fine. You're one of 40% of Americans stuck in revolving debt, paying $83 in interest for every $17 that reduces your debt.

And then there's the shame spiral. You know intellectually that your situation isn't good. But admitting it means confronting reality. So instead, you avoid looking at your statements. You avoid doing the math. You avoid being honest about the timeline—that you won't escape this debt until you're 55 or 60 years old.

55% of Americans are now using credit cards for basic necessities — groceries, rent, utilities. This isn't choice. This is survival. When your paycheck doesn't cover your living expenses, the credit card becomes a bridge loan. And once you're on the bridge, compound interest keeps you trapped.

Add to this: only 48% of people carrying credit card debt have an actual plan to pay it off. The other 52%? They're hoping something changes. They're not taking action.

Here's the truth nobody wants to say: you're more likely to escape poverty by taking deliberate action than by waiting for circumstances to change.

The Real Cost: How Credit Card Debt Delays Your Financial Freedom by a Decade

Let me connect this to the core mission of this site.

If you're interested in financial independence or early retirement (FIRE), credit card debt is your #1 obstacle. Not housing. Not student loans. Credit card debt, because of the compounding interest and the psychological toll.

Let me show you with a real scenario.

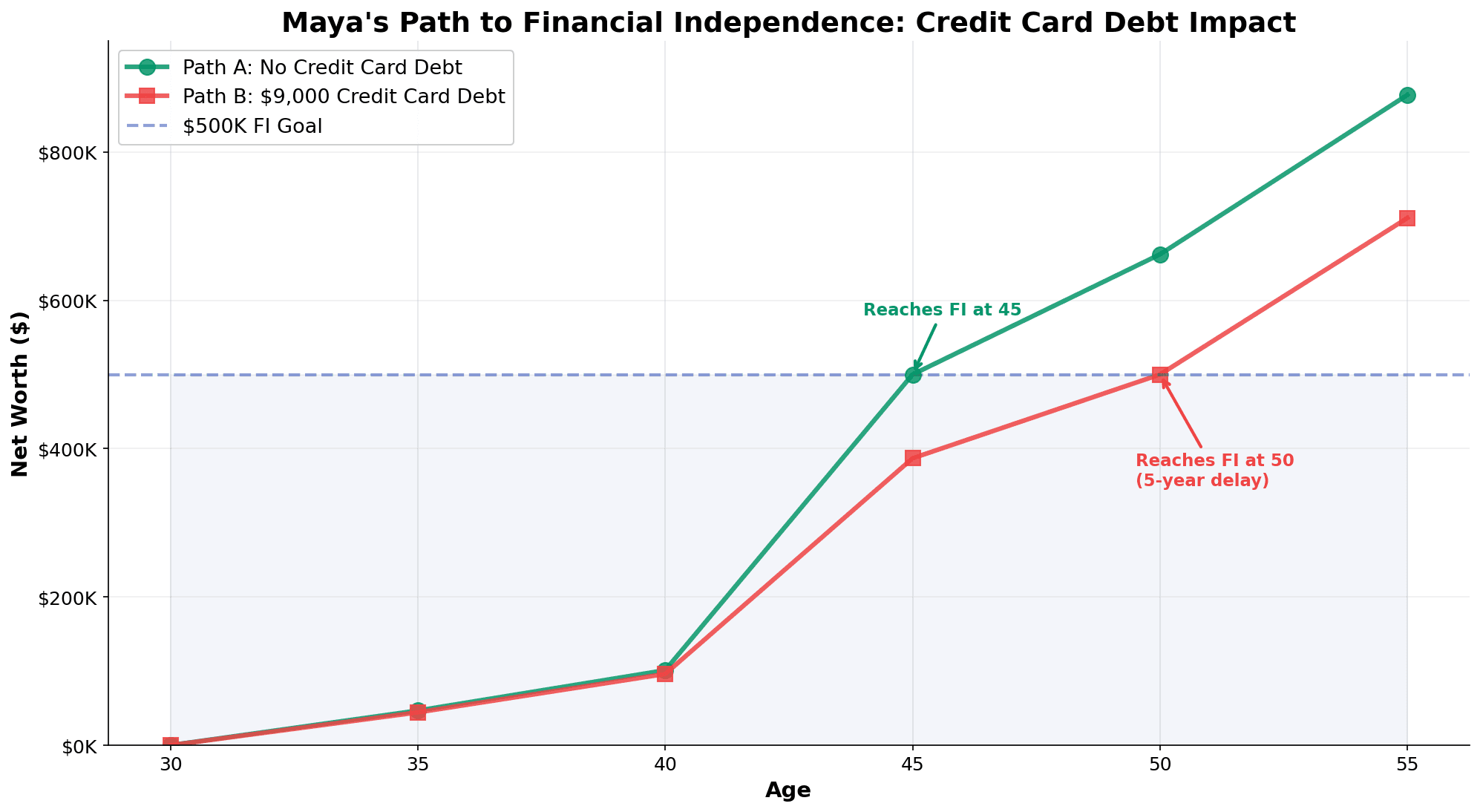

Meet Maya. Age 30.

- Income: $80,000/year

- Debt: $9,000 in credit card balances at 19% APR

- Goal: Retire by age 45

- Planned savings rate: 37.5% ($30,000/year invested)

Without credit card debt, investing $30,000/year at an 8% annual return for 15 years, Maya reaches her $500,000 FI number by age 45.

But with the $9,000 credit card debt:

- Minimum payment: $200/month ($2,400/year)

- Interest cost: ~$1,710/year (year 1), declining slightly each year

- Available for investing: Only $27,600/year instead of $30,000/year

That $2,400/year difference, compounded at 8% over 15 years, equals $68,000 in lost wealth.

But it's worse than that. The psychological weight of debt slows her down. She gets demotivated. She cuts her savings rate to 30% instead of 37.5%. Now she's losing even more.

Maya's actual FIRE date? Age 50, not 45. The $9,000 in credit card debt just cost her 5 years of freedom.

And that's assuming she doesn't face another emergency that increases her debt during those 15 years. If she does, she's now looking at age 55 or 60.

The equation we've talked about before is: Wealth = Income × Discipline × Time

Credit card debt poisons all three:

- It reduces your available income (interest payments)

- It erodes your discipline (debt fatigue)

- It steals your time (years of payoff)

The Three-Tier Escape Plan: From Trapped to Debt-Free

Okay, the bad news is clear. Here's the good news: you can escape this.

But it requires a strategic approach, not hope.

Tier 1: Emergency Actions (Week 1-2)

If you're carrying credit card debt right now, do this today:

Step 1: Audit Your Debt

List every credit card. Write down:

- Balance

- APR

- Minimum payment

See it all at once. Face the number.

Step 2: Calculate the True Cost

Use a credit card payoff calculator (or do it manually). Find out: How much will I pay total if I only make minimum payments for 5 years?

A $5,000 balance at 20%? You'll pay $12,500 total. Nearly 3x the original amount.

Most people haven't done this math. It's shocking. Use that shock as motivation.

Step 3: Apply for a Balance Transfer Card

This is your fastest escape route if you qualify.

Cards like Citi Diamond Preferred (21 months at 0% APR, 3% transfer fee) or Wells Fargo Reflect (21 months at 0% APR, 5% transfer fee) exist specifically for this.

If you transfer $5,000 to a 21-month 0% card with a 5% fee ($250), your cost is $250 + whatever you pay in 21 months.

If you pay $238/month, you eliminate the debt in 21 months with $0 in interest.

Compare that to minimum payments where you pay $12,500 total. The balance transfer card saves you $12,000+.

Requirement: You need decent credit (670+) to qualify. If your credit is worse, move to Tier 2.

Tier 2: Strategic Payoff (Month 1-12)

If a balance transfer card doesn't work, here are two proven methods:

Option A: Debt Avalanche (Mathematically Optimal)

This saves the most interest.

- Make minimum payments on all cards

- Take any extra money and throw it at the highest APR card first

- Once the highest APR card is gone, roll that payment to the next-highest APR

- Repeat

Example: Three cards at 21%, 20%, and 18% APR. Attack the 21% card aggressively. Once it's gone, combine those payments toward the 20% card. This saves you roughly $1,366 more than other methods on a $15,000 debt.

Option B: Debt Snowball (Psychologically Optimal)

This is slower mathematically, but gives you quick wins.

- Make minimum payments on all cards

- Throw extra money at the smallest balance first

- Once it's gone, roll that payment to the next card

- The momentum builds — your "snowball" grows

Example: Three $5,000 balances. Attack one aggressively. Pay it off in month 8. You get the dopamine hit of a zero balance. That motivation often keeps people going where Avalanche advocates quit.

(Can't choose between the two? There's a hybrid method that captures most of both benefits. And if you're hunting for the "extra money" itself, hourly workers got a new source in 2026 — the No Tax on Overtime deduction can return up to $4,000 at tax time, found money that belongs on your highest-APR card.)

Which should you choose? If you're mathematically motivated, use Avalanche. If you need psychological wins to stay motivated, use Snowball. The difference in total interest is real, but not paying at all is worse.

Option C: Personal Loan Consolidation

If you don't qualify for balance transfer cards, a personal loan at 12% APR (for qualified borrowers) saves money versus 22% credit card rates.

Example: $10,000 at 22% credit card APR costs you $4,100 in interest over 4 years.

Same $10,000 at 12% personal loan APR costs you $1,200 in interest.

Savings: $2,900. Yes, there's usually a 5% origination fee ($500), but you still come out way ahead.

Tier 3: Prevention (Month 4-12+)

Once you're on the escape plan, prevent relapse:

Build a $1,000 Emergency Fund

Put this in a high-yield savings account earning 4.5-5% APY. The point isn't returns. It's that the next emergency (car repair, medical bill, job loss) doesn't force you back onto credit cards.

Without this emergency fund, you're one crisis away from re-entering the debt spiral.

Track Your Spending

Use a budgeting tool to understand where lifestyle inflation happened. Was it restaurants? Subscriptions? Impulse shopping? Know your trigger.

Switch to Cash for Daily Spending

This sounds old-fashioned, but it works: paying with physical cash feels different than swiping a card. Psychologically, you'll spend less and avoid the "I didn't really spend that" effect.

Only Invest After Debt is Gone

This is important: paying 20% interest on credit card debt while investing at 8% returns is a losing strategy. Your guaranteed 20% savings from eliminating debt beats your uncertain 8% gains from the market.

Close the loop first. Then invest.

Warning Signs You're in the Trap (And What to Do Now)

Do you recognize yourself in any of these?

Sign 1: Your balance never shrinks month-to-month

You make your payment. Next month, the balance is almost the same. You're servicing interest, not principal.

Sign 2: You only pay the minimum

The minimum payment is the maximum you can afford. This is Tier 1 territory.

Sign 3: You're using credit cards for essentials

Groceries, gas, utilities. You don't have a choice anymore. Emergency fund time.

Sign 4: You're only paying interest, not principal

Example: Your minimum payment is $150, and you can see that $130 of it is interest. The other $20 barely touches debt.

Sign 5: You've stopped looking at your statements

Avoidance. The debt is real. You just don't want to face it.

Sign 6: You're carrying balances across multiple cards

This is complexity + interest multiplication. This is priority #1 to fix.

Sign 7: Your credit score is dropping

High balances relative to limits, or missed payments due to not being able to pay. This feedback loop makes everything worse.

If you see yourself here — in any of these signs — the time is now. Not next month. Now.

Use our budgeting tool to understand exactly where you are. Knowledge is the first step to escape.

The 12-Month Action Plan: Your Escape Timeline

Here's a month-by-month plan to get you from trapped to free:

Month 1: Audit & Realize

- List all debts, balances, APRs

- Calculate total payoff cost if minimum payments only

- Set a specific payoff target date

Month 2: Apply for Solutions

- If you qualify: apply for balance transfer card or personal loan

- Approval usually takes 1-3 business days

- Transfer highest-APR balances immediately

Month 3-8: Aggressive Payoff

- Execute your chosen method (Avalanche or Snowball)

- Set aggressive monthly payment target (ideally 2-3x the minimum)

- Track progress weekly to maintain motivation

Month 9-10: First Victory

- Your first card/balance should be paid off

- Roll that payment amount to the next debt

- Celebrate the win (but don't increase spending)

Month 11-12: Build Prevention

- Open high-yield savings account, start $1,000 emergency fund

- Review your budget to prevent relapse

- Identify spending triggers and set boundaries

Beyond Month 12: Freedom

- Debt paid. Emergency fund in place. Ready to invest properly.

- Monitor statements to prevent future balance-carrying

- Redirect that former credit card payment amount to investments

This isn't theoretical. This is the timeline that works.

What People Get Wrong About Escape

Myth 1: "I'll wait for Fed rate cuts"

We already addressed this. Credit card rates will stay elevated even as Fed cuts roll out. Don't wait. Action now saves you thousands.

Myth 2: "I should use a personal loan for my emergency"

No. A personal loan should only be for debt consolidation/refinancing, not new emergencies. Once you're out, build cash reserves.

Myth 3: "I need to cut up my credit cards"

Wrong. You need to stop using them, not destroy them. Cards paid off and unused are actually good for credit score. Unused cards with $0 balances show credit discipline.

Myth 4: "This will take 5+ years"

Only if you keep making minimum payments. With an aggressive payoff plan and a balance transfer card, $6,000 in debt vanishes in 18-24 months, not 5+ years.

Myth 5: "I should invest instead of paying off debt"

No. Guaranteed 20% return (from eliminating 20% interest) beats uncertain 8% market returns. Close the debt loop first.

The Bigger Picture: Why This Matters for Your Future

Credit card debt isn't just a financial problem. It's a freedom problem.

Every dollar going to credit card interest is a dollar that can't go to:

- An emergency fund (so you don't face another crisis)

- Investing (so you can escape the paycheck-to-paycheck cycle)

- Time freedom (every year of minimum payments is a year you can't pursue FIRE)

- Your actual life (because you're stressed about money)

The Federal Reserve, credit card companies, and inflation have conspired to create a situation where 40% of Americans are trapped. But you don't have to be part of that statistic.

You can escape. It takes focus, strategy, and about 12-18 months of deliberate action. But the alternative — spending the next 10-20 years servicing interest — isn't acceptable.

The math is clear. The strategy is clear. What's left is your decision.

Are you going to keep making minimum payments?

Or are you going to take back control?

Conclusion: Your Choice, Starting Today

You now know:

- The math: How $5,000 becomes $12,500 through compound interest

- The timeline: Why you're not making progress on minimum payments

- The escape routes: Balance transfer, Avalanche/Snowball, consolidation loans

- The prevention: Emergency fund + budgeting + awareness

What you do next is the only thing that matters.

Credit card debt doesn't go away on its own. It compounds against you every single day at 20%+ interest.

But it also doesn't require perfection to escape. It requires:

- Honest math (face the number)

- Strategic choice (which method)

- Consistent action (stick to the plan)

- Time (12-24 months usually)

You have the tools. You have the knowledge.

The only question is: are you ready to stop being poor so credit card companies can be rich?

📩 Have questions about your specific situation? Email me at dennis.vymer@myfinancialfreedomtracker.com

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.