2026 Retirement Rules Just Changed: New Contribution Limits and the Roth Catch-Up Trap Nobody Warned High Earners About

New to personal finance and investing?

If you're just starting, these three articles will give you the foundation this one builds on:

- How to Start a Budget — where every dollar goes before it hits a retirement account

- The FIRE Movement — why contribution limits matter for early retirement

- Wealth = Time × Money × Discipline — the math behind compounding

Maya opens her pay stub in April 2026 and does a double-take.

Her 401(k) deduction looks normal. But when she logs into her plan portal to bump up the percentage, something has changed. The system is asking her to confirm whether her prior-year wages were above $150,000. She was promoted last November. Her 2025 FICA wages were $151,400.

She clicks "yes." The portal responds: "Based on your compensation, your catch-up contributions in 2026 must be designated as Roth (after-tax)."

She doesn't remember signing up for this. She didn't.

Congress did — back in 2022, buried inside the SECURE 2.0 Act. The provision kicked in quietly on January 1, 2026. Millions of workers will not notice until they open their next statement.

If you're serious about retirement, 2026 is the year to pay attention. The IRS raised nearly every major contribution limit. A new "super catch-up" window just opened for people ages 60–63. And the Roth catch-up mandate has rewritten the rules for anyone earning over $150,000. These changes quietly reshape FIRE timelines, tax bills, and take-home pay for tens of millions of savers.

This article walks through every change, shows you the real dollar math with three character examples, and gives you a clear action plan — whether you're 28 or 62.

What Actually Changed in 2026 (The Short Version)

Before we dig into details, here's the full 2026 picture in one place:

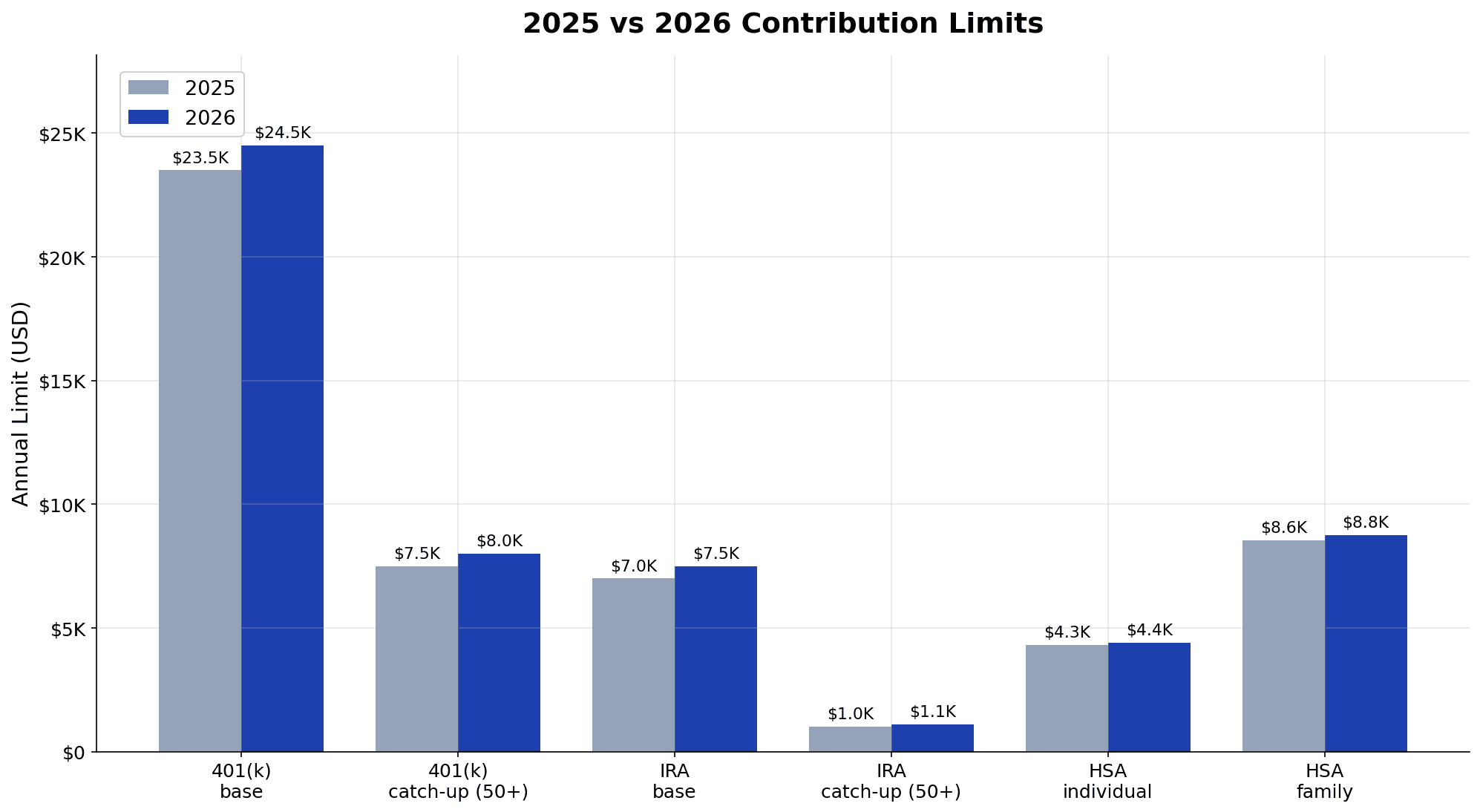

| Account | 2025 Limit | 2026 Limit | Change |

|---|---|---|---|

| 401(k), 403(b), 457, TSP | $23,500 | $24,500 | +$1,000 |

| 401(k) catch-up (age 50+) | $7,500 | $8,000 | +$500 |

| 401(k) super catch-up (age 60–63) | $11,250 | $11,250 | no change |

| Traditional/Roth IRA | $7,000 | $7,500 | +$500 |

| IRA catch-up (age 50+) | $1,000 | $1,100 | +$100 |

| HSA — individual | $4,300 | $4,400 | +$100 |

| HSA — family | $8,550 | $8,750 | +$200 |

| HSA catch-up (age 55+) | $1,000 | $1,000 | no change |

| Roth IRA phase-out (single) | $150K–$165K | $153K–$168K | +$3K |

| Roth IRA phase-out (married) | $236K–$246K | $242K–$252K | +$6K |

Sources: IRS Newsroom, Kiplinger 2026 changes summary.

The biggest practical change isn't a limit going up — it's a rule about how you're allowed to contribute. Let me explain.

The New 2026 Contribution Limits Explained

If you max a 401(k) and an IRA, you can now shelter $32,000/year from taxes as a regular saver under 50 — up from $30,500 in 2025. Add an HSA and it jumps to $36,400 for individuals or $40,750 for families.

That's not a small deal. Over 30 years at a 7% real return, contributing an extra $1,500 every year (the rough increase over 2025 caps) adds $151,700 to a retirement balance. Every dollar of headroom Congress creates is a dollar compounding for decades.

Here's how the three main buckets work:

401(k) / 403(b) / 457 / TSP — $24,500 base limit This is the employee contribution you control. Employer match does not count against this cap. The combined limit (employee + employer + after-tax) is $72,000 for 2026, which matters mostly for mega-backdoor-Roth setups.

Traditional and Roth IRA — $7,500 base limit This limit is combined across both types. You can't put $7,500 in each. Roth IRA eligibility phases out above $153,000 single / $242,000 married — if you're above, you're on the backdoor Roth path or nothing.

HSA — $4,400 individual / $8,750 family HSAs remain the most underrated account in the U.S. tax code. Contributions are deductible, growth is tax-free, and qualified medical withdrawals are tax-free. It's the only triple-tax-advantaged account that exists.

If you have access to all three, the priority order I recommend is straightforward: get the full 401(k) employer match first, then max the HSA if you qualify, then max the IRA (ideally Roth if you're eligible), then top off the 401(k). That sequence captures match dollars first and minimizes tax friction.

The Roth Catch-Up Trap for High Earners

Here is where things get interesting — and where most people will be caught off guard.

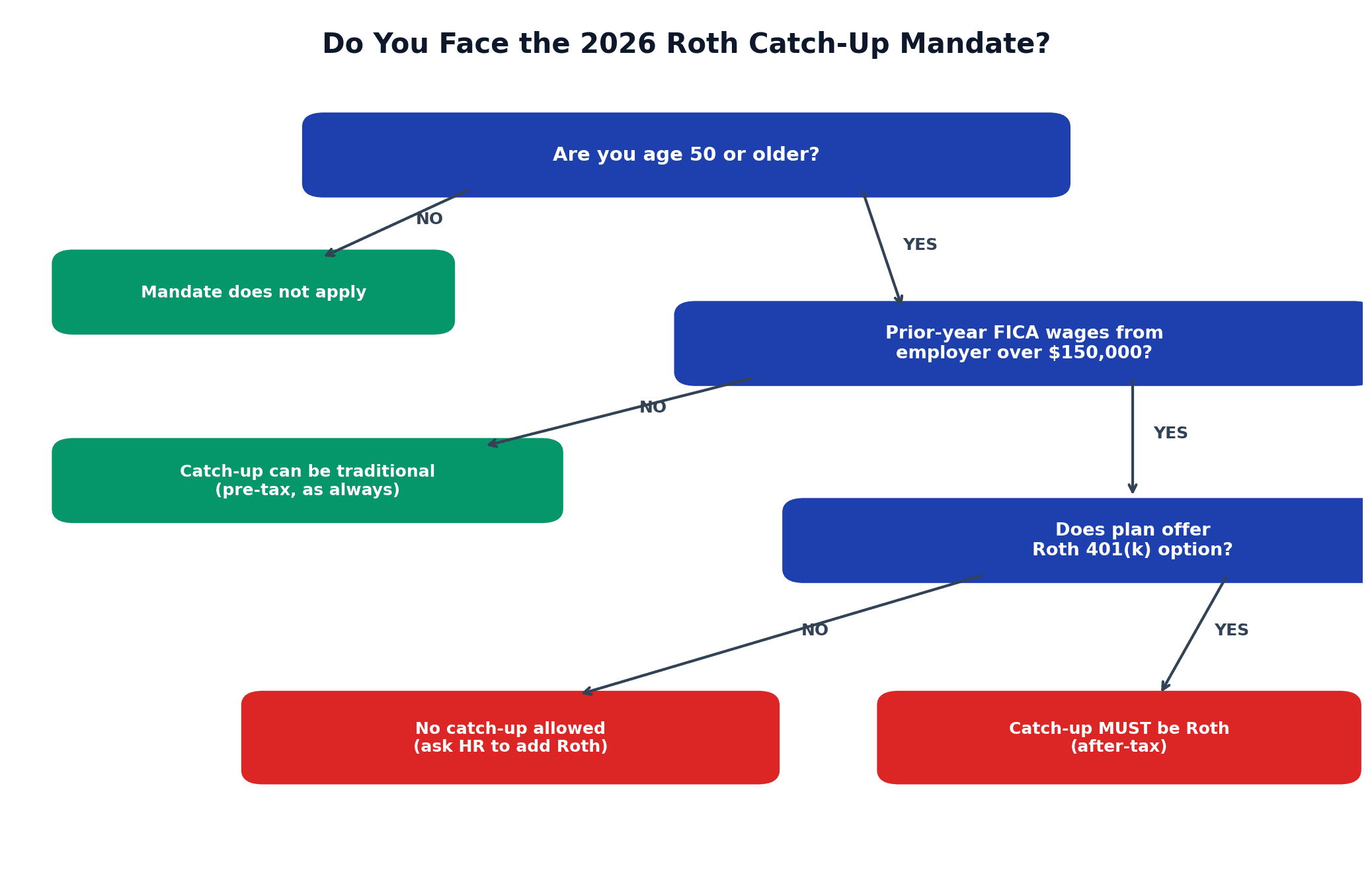

Under SECURE 2.0 Section 603, starting in 2026, anyone who makes catch-up contributions (age 50+) to a workplace plan must designate those contributions as Roth if their prior-year FICA wages from the same employer exceeded $145,000 (indexed to $150,000 for 2025 earnings → affecting 2026 contributions).

Translation into plain English: if you're a 52-year-old earning $160,000 and you want to contribute the extra $8,000 catch-up this year, you can't take the tax deduction anymore. That $8,000 comes out of your paycheck after federal income tax. If you're in the 24% federal bracket, this is equivalent to roughly $1,920 less take-home pay versus the old rules — for the same savings goal.

The money grows tax-free and comes out tax-free in retirement, which is genuinely valuable. But for most high earners who are already in a peak tax bracket now and expect to be in a lower one in retirement, losing the upfront deduction is a real hit.

Four nuances most people miss:

-

The threshold is per-employer. If you switched jobs in 2025 and earned $130,000 from your new employer (even though your total was $200,000), the mandate doesn't apply. It looks only at FICA wages from the sponsoring employer.

-

Self-employed catch-ups are unaffected. SEP-IRAs, solo 401(k)s funded through self-employment income, and SIMPLE-IRAs follow different rules. Many solo owners can keep the traditional (pre-tax) catch-up treatment.

-

Your plan has to allow Roth 401(k). If your employer's plan doesn't offer a Roth option, under the final regulations they cannot accept any catch-up contributions from high earners. That's right — no catch-up at all, not even traditional. Call your HR department this month to verify.

-

The threshold adjusts for inflation going forward. The statute sets it at $145,000 in base dollars; indexing pushed it to $150,000 for 2025-wage measurement. Expect it to keep climbing.

Per Fidelity's breakdown, approximately 16% of 401(k) participants make catch-up contributions each year, and roughly one in four of them earn above the threshold. That's millions of workers being quietly shifted into a fundamentally different tax bucket.

The Super Catch-Up for Ages 60–63 (Most People Miss This)

Buried in the same legislation is a gift most people don't know exists: the super catch-up.

If you're between ages 60 and 63 in 2026 and your employer's plan allows it, you can contribute up to $11,250 in catch-up — in place of the standard $8,000. That brings your total 401(k) limit to $35,750 in a single year.

The math on this is genuinely eye-opening.

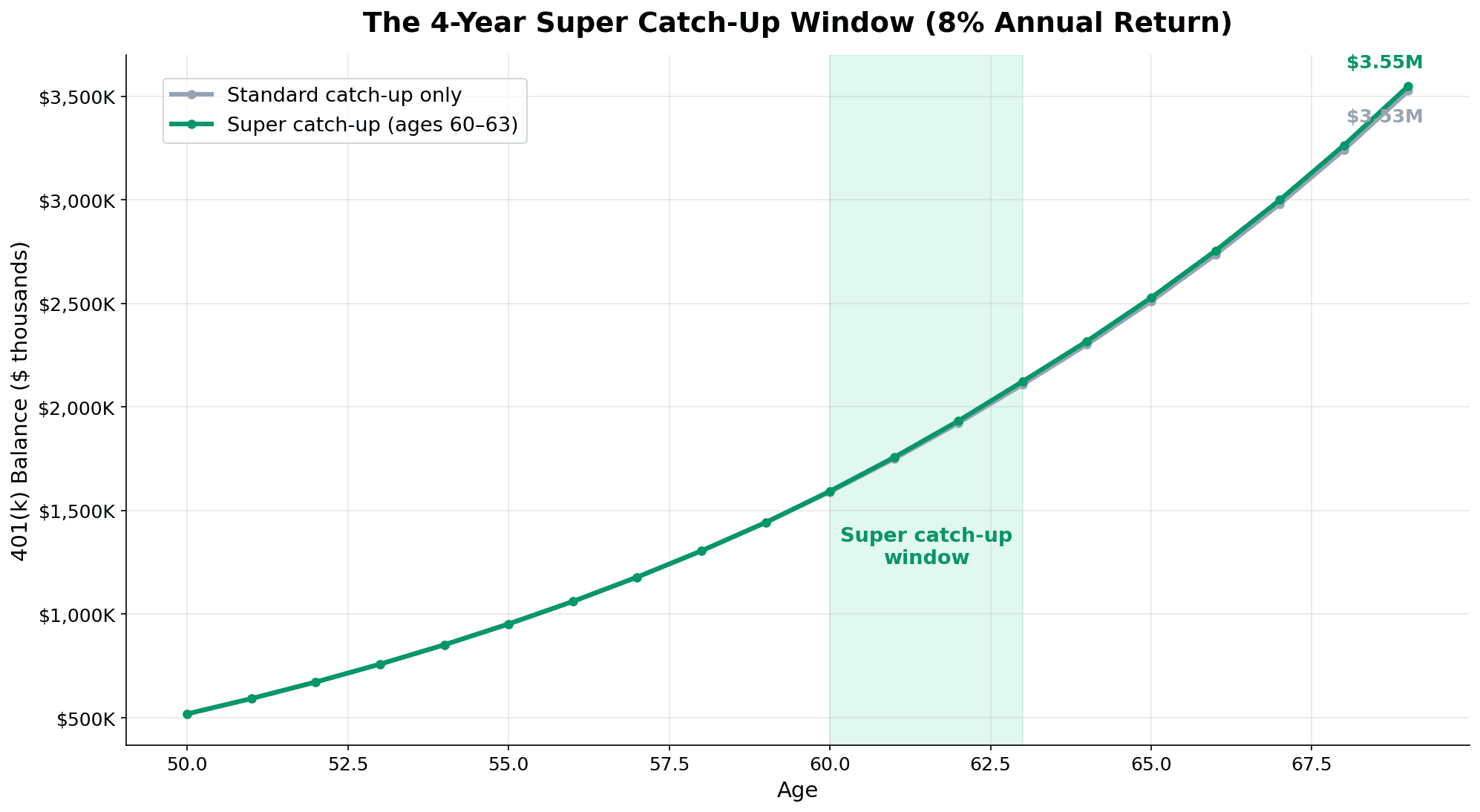

Meet Jordan. He's 60 in 2026, earns $140,000, and already has $900,000 in his 401(k). He's been contributing $32,500/year (limit plus regular catch-up) since age 50.

If Jordan uses the super catch-up for four years (2026–2029), he puts in $35,750/year instead of the standard $32,500. At 8% annual returns, here's how those four years compare:

| Strategy | Years 60–63 Contributions | Balance at 64 |

|---|---|---|

| Standard catch-up only | $130,000 total | ~$1.38M |

| Super catch-up | $143,000 total | ~$1.41M |

| Super catch-up + working 5 more years | $143K + compounding | ~$2.31M |

The direct contribution difference is modest ($13,000 over four years). The compounding difference is what matters — especially if Jordan keeps working and contributing through 65+. The super catch-up window is small, but it lands at the most powerful compounding age in anyone's career.

One catch: because Jordan earns over $150,000, those super catch-ups must still be Roth. He loses the pre-tax deduction but gains four decades of tax-free growth on every dollar.

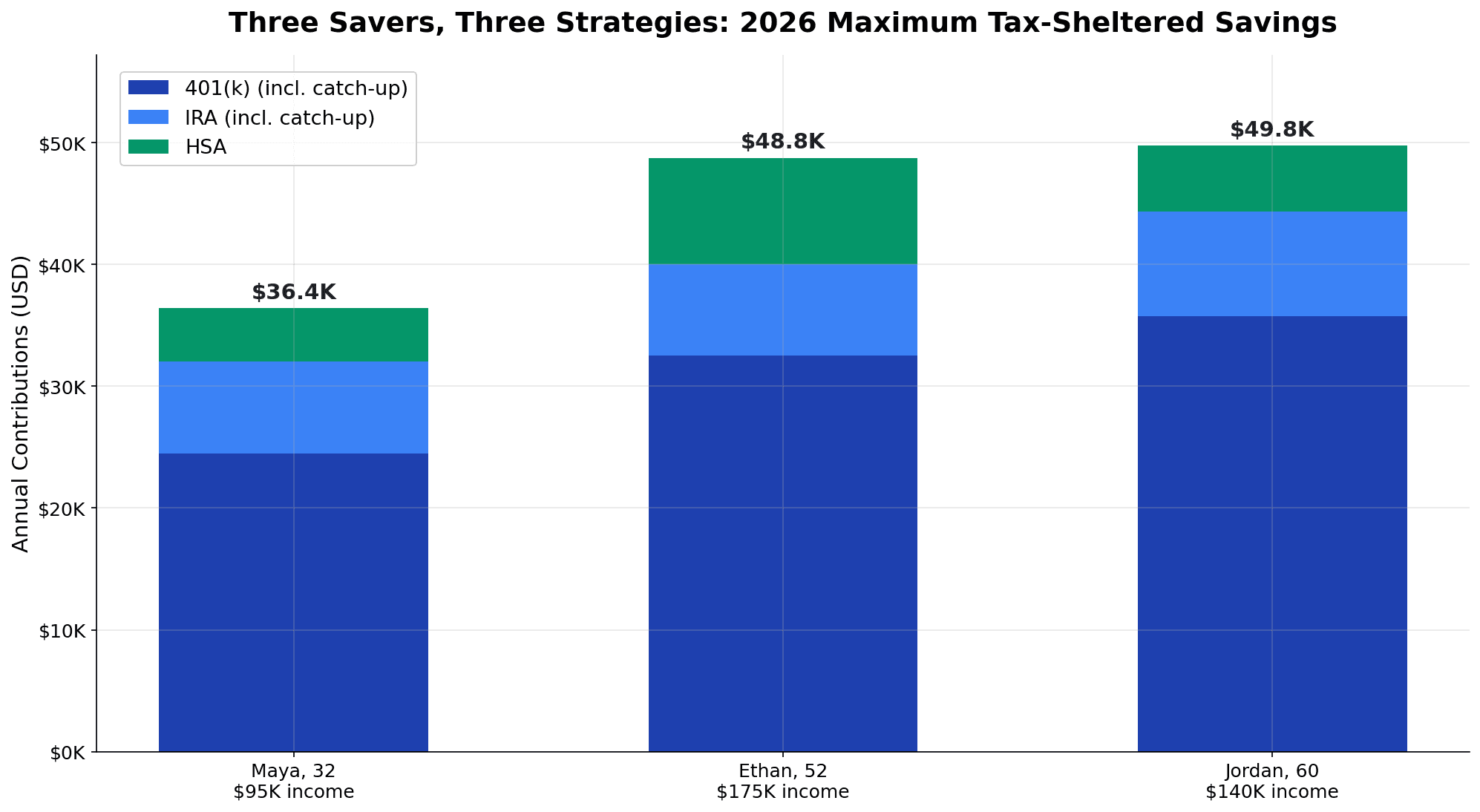

The Real Dollar Impact: Three Character Stories

Let me show you what this looks like in three different lives.

Maya, 32, earning $95,000

Maya is under 50, so no catch-ups apply. She's below the Roth IRA phase-out. Her 2026 plan:

- 401(k): $24,500 (traditional, for the deduction now)

- Roth IRA: $7,500

- HSA: $4,400

Total sheltered: $36,400/year → 38% of gross. Over 25 years at 7% real returns, that compounds to roughly $2.3 million. Maya doesn't think about herself as on the FIRE path, but she's on a trajectory to hit Coast FIRE well before 45.

Ethan, 52, earning $175,000

Ethan gets the worst of the new rules and needs to adjust. His 2026 plan:

- 401(k): $24,500 base (traditional, if plan allows) + $8,000 catch-up (Roth, mandatory)

- Roth IRA: disqualified (income too high) → uses backdoor Roth strategy for $7,500

- HSA: $8,750 (family coverage)

His effective tax hit from the Roth mandate: ~$1,920 in additional taxes this year (24% bracket × $8,000). Annoying, but the trade-off is tax-free growth on $8,000/year from now to age 75 — roughly $46,000 of tax-free compounded money at 7% returns. Over time, it's closer to a wash.

Jordan, 60, earning $140,000

Below the Roth mandate threshold (barely), Jordan can still contribute traditional catch-up. His plan offers super catch-up. His 2026 plan:

- 401(k): $24,500 + $11,250 super catch-up (traditional)

- Roth IRA: $7,500 + $1,100 catch-up

- HSA: $4,400 + $1,000 catch-up

Total sheltered: $49,750/year for the next four years — the biggest savings window of his life. If he didn't know about super catch-up, he'd leave $3,250/year on the table for four years. That's $13,000 of direct contributions plus decades of growth on money he'll never get the window for again.

What This Means for Your FIRE Timeline

Higher contribution limits are quietly one of the most FIRE-friendly policy changes in a decade. Here's why.

The core FIRE math is that your savings rate drives how quickly you reach financial independence. The classic table: a 25% savings rate = ~32 years to FI; 50% = ~17 years; 70% = ~8.5 years. When Congress raises the cap on tax-advantaged accounts, they're letting you shield a bigger absolute dollar amount — which raises the ceiling on how much you can plausibly save while still having normal take-home.

For someone earning $100,000:

- 2025 max-everything savings: $30,500 (30.5% rate before employer match)

- 2026 max-everything savings: $32,000 (32% rate before employer match)

That's not life-changing on its own. But the super catch-up can shave years off a late-career FIRE push. If you're 58 and looking at retiring at 65, those four super-catch-up years hit during peak-earning, peak-compounding time.

If you're not sure what your actual FI number looks like, the framework in the FIRE movement article walks through the 25× rule and withdrawal math. For younger readers, Gen Z's phased retirement approach shows how to stretch modest incomes into early freedom.

The Roth vs Traditional Decision (2026 Edition)

With the new mandate, many high earners no longer get to choose — their catch-ups are Roth now. But for everyone else, the Roth vs traditional decision still matters, and 2026 has nudged the math.

Choose Roth when:

- You're early in your career with low current income (you'll be in a higher bracket later)

- You expect Congress to raise tax rates in the future (a safe bet given the deficit trajectory)

- You want flexibility — Roth contributions (not earnings) can be withdrawn anytime tax-and-penalty-free

- You're aiming for FIRE with a large Roth conversion ladder strategy

Choose Traditional when:

- You're in your peak earning years (usually 40s–50s)

- Your state currently taxes income but won't where you plan to retire

- You expect to spend less in retirement than you earn now

- You need the deduction to actually afford maxing contributions

There's no universally correct answer. The most sophisticated savers often do both — partly for tax diversification, partly because nobody knows what tax rates will look like in 2050.

Your 2026 Action Plan

Regardless of age or income, here's a concrete checklist for April through December:

This month (April 2026):

- Log into your 401(k) portal and confirm your contribution rate hits the new $24,500 limit by December (or the appropriate catch-up amount if you're 50+)

- If you're a high earner, call HR and confirm your plan offers a Roth 401(k) option. If it doesn't, push them to add one — otherwise your catch-ups simply aren't allowed

- If you turn 60, 61, 62, or 63 this year, verify your plan supports the super catch-up (it's optional for employers)

- Make your 2025 IRA contribution before the April 15 tax deadline if you haven't — that's a separate last chance

Mid-year (June–September 2026):

- Review whether you're on pace to hit the new limits

- Consider a Roth conversion if the market takes a dip (converting when values are depressed = tax savings)

- If your income will push you over the Roth IRA phase-out, start the backdoor Roth process now

End of year (October–December 2026):

- Front-load the remaining balance into Q4 if you got a raise, bonus, or side income

- Check your HSA contribution (many employers under-contribute to meet the full $4,400/$8,750)

- Harvest tax losses in taxable accounts to offset anything else

If the act of tracking all of this feels overwhelming, this is exactly the kind of situation a proper budgeting and net worth system solves — you want every dollar categorized and every account monitored in one place so you're not guessing in December.

The Real Story of 2026

The headline numbers — $24,500, $7,500, $4,400 — are the kind of thing personal finance articles will tell you by rote. The real story is subtler:

Congress made saving easier for people under 50 (slightly higher caps), harder for high earners (forced Roth), and dramatically more generous for people in their early 60s (super catch-up). It's a redistribution of tax treatment, not a simple inflation adjustment.

If you're 32 and on autopilot, the 2026 changes are a small bonus. If you're 52 and earn six figures, they demand an active decision — especially if your plan doesn't currently offer Roth. If you're 60, they represent the single biggest short-window savings opportunity you'll ever get.

Whatever age you are, the worst thing you can do is nothing. The deductions and growth you don't capture in 2026 are gone forever.

Open your plan portal. Check your contribution rate. Confirm your Roth options. The rules changed. Your strategy should too.

Next week: A deep dive on the mega-backdoor Roth strategy — how to get up to $72,000/year into tax-advantaged accounts if your plan supports the after-tax bucket. If you want early access when it drops, bookmark the MFFT blog.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.