The Anti-Influence Movement: Why Smart People Are Rejecting FinTok Hype (And Building Real Wealth Instead)

I watched a TikTok last week. A 24-year-old creator with 2.3M followers showing off her net worth: "$50K invested by 24, and I'm just getting started." The comments were ecstatic. "OMG this is goals." "How do I do this?" "I'm inspired."

Nobody asked the obvious question: Is this sustainable? Or is this the algorithmic equivalent of survivorship bias?

That question is what this entire article is about.

Welcome to the anti-influence movement — a growing, quiet revolt against the performative, algorithmically-amplified version of personal finance that dominates social media. This isn't about rejecting financial education. It's about rejecting hype. And it's winning.

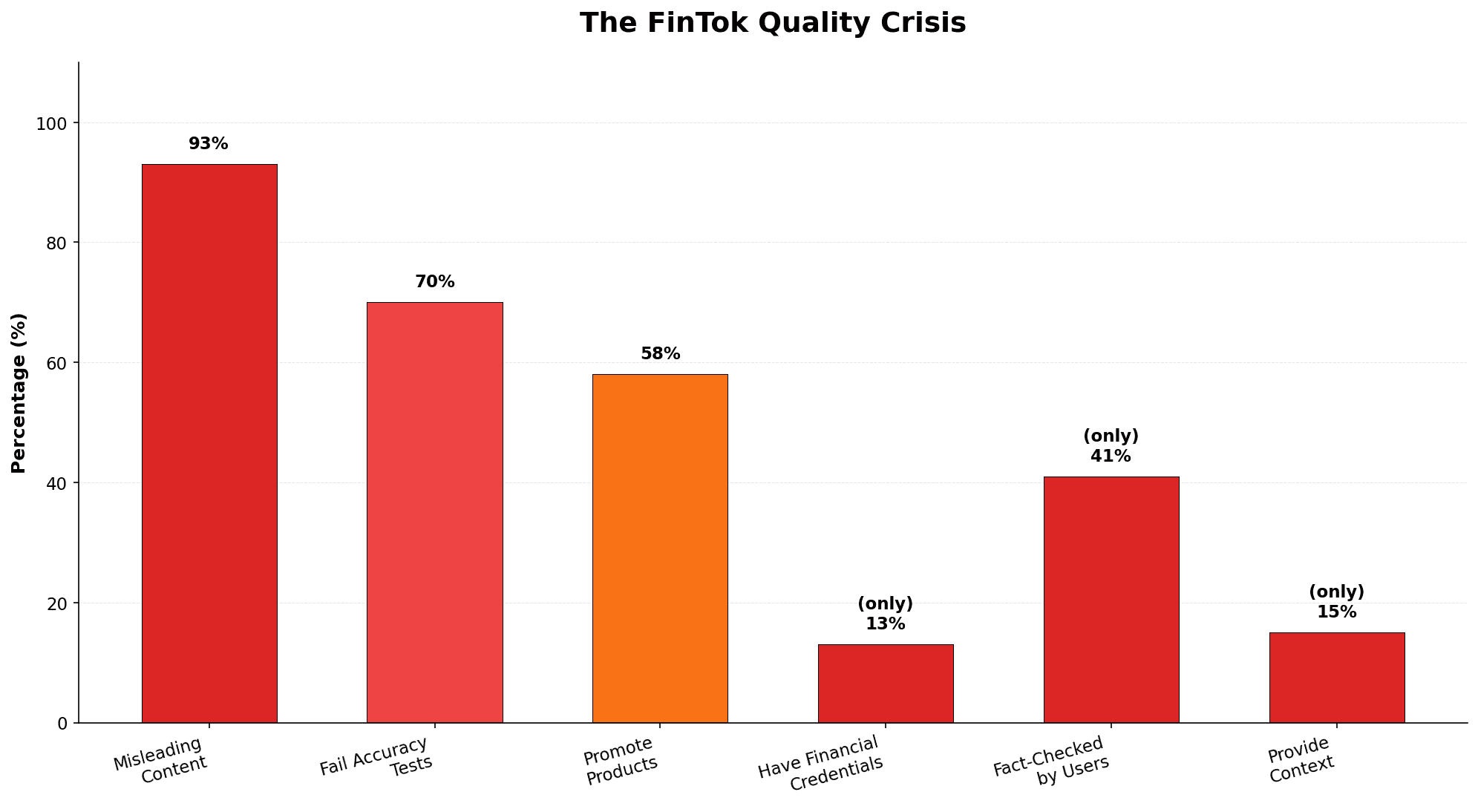

Here's what the data shows: 93% of viral trading videos contain misleading content. 72% of day traders lose money. Yet 39% of Gen Z now say they'll never trust social media finance advice again. Meanwhile, the people actually building wealth are doing something radically different: they're being boring, staying quiet, and compounding silently while the rest of the internet argues about shortcuts and get-rich-quick schemes.

Let me show you why boring is winning, and how to reject the noise without rejecting financial growth.

The Hype Trap: Why Viral Money Advice Is Engineered to Fail

Here's something that matters: algorithms reward drama, not returns.

A TikTok creator showing a 7% index fund return doesn't go viral. It's boring. It's not engaging. It has no emotional hook. Nobody feels FOMO about consistent, compounding returns.

But a creator claiming they turned $5K into $50K through day trading? That gets 400K views. The algorithm loves it because it triggers excitement, envy, and urgency. The fact that 72% of day traders lose money is completely irrelevant to the algorithm. The algorithm doesn't care about outcomes. It cares about engagement.

This creates a systematic bias: the financial advice you see online is disproportionately likely to be dramatic, risky, and wrong. The platform actively suppresses boring but effective advice while amplifying false but exciting advice.

The Data on Viral Finance Content

Let me be specific about what's happening with FinTok:

- 93% of viral trading videos contain potentially misleading or harmful content — they cherry-pick winners and hide losers

- 70% of viral finance TikToks fail basic accuracy tests — the claims don't hold up to scrutiny

- 58% actively promote financial products — trading courses, proprietary "systems," premium memberships — the creator profits directly from your compliance

- Only 15% of FinTok trading videos provide meaningful context — about how results were achieved, what risks were taken, whether outcomes are repeatable

- Only 13% of FinTok creators have actual financial credentials — CFP, CFA, FINRA licenses, anything suggesting they know what they're talking about

- Only 41% of FinTok users fact-check the advice — roughly 6 in 10 people are consuming financial advice with zero verification

That's not education. That's exposure.

Three Viral Trends That Illustrate the Problem

The "I Turned $5K Into $50K" posts: You see a screenshot of a brokerage account, a dramatic story about the trade, thousands of likes and amazed comments. What you don't see: the $15K account that went to $500, the 16 failed trades, the six months of emotional torture. You're watching the one win out of 20 attempts. That's not inspiration. That's statistics being weaponized.

The "I'm 25 With $1M Net Worth" flex: These posts explode. Everyone wants the secret. The reality? Usually inherited money, a company that succeeded by luck, or real estate equity in a hot market (included in net worth but illiquid). The "secret" isn't replicable. But the algorithm doesn't care — it got your attention and engagement.

The "Get-Rich-Quick Side Hustle" pitch: "Make $5K/month in your spare time," "I quit my job to do this," "This business model changed my life." According to my research, the median side hustle earns $200/month. But median doesn't sell courses. Outliers do. The people earning $5K/month are the 1%, not the rule. These creators are selling a fantasy, not a system.

Why Your Brain Falls for It (Even Though You Know Better)

There's a psychological mechanism called availability bias. If something is easy to recall because you've seen it viral 47 times, your brain assumes it's common. You've seen seventeen posts about people making money day trading. Therefore, your brain concludes, day trading must be reliable.

It's not. But the algorithm has made it feel inevitable.

Combine this with social proof — "if thousands of people like this post, it must be legitimate" — and fear of missing out. You're not choosing whether to day trade. You're choosing whether to miss out on wealth that everyone else apparently claims is available.

The algorithm stacked the deck.

The Reddit Wake-Up Call: Communities Are Calling Out the Lie

Here's what's interesting: the people who know the most about building wealth are actively rejecting the narratives that dominate social media.

Reddit communities dedicated to financial independence have exploded in size. r/FIRE has 871K members. r/Bogleheads has 628K. These communities grew 30x in five years, and the conversation has shifted dramatically.

Instead of celebrating wealth, they're questioning it. Instead of sharing wins, they're interrogating the cost. There's a wisdom in these spaces that social media suppresses.

The Sentiment Shift

Go to r/FIRE and sort by recent posts. You'll see conversations like:

- "I hit my FIRE number at 40 and I'm miserable. Nobody tells you that."

- "The bragging is out of control. Let's talk about actual fulfillment."

- "Why does achieving the goal feel empty?"

- "I'm rich but also exhausted and burned out. This wasn't supposed to feel like this."

This isn't cynicism. It's wisdom. These are people who followed the playbook, hit the numbers, and discovered that hitting the numbers isn't the same as being happy.

The meta-awareness is real: the movement itself has become what it was reacting against. FIRE started as a rebellion against consumerism, comparison, and the rat race. Now, in its most visible form (Instagram, TikTok, YouTube), it's become another status competition. People flex their net worth instead of their salary.

But the people actually building wealth aren't flexing anything. They're quiet.

The Data on Trust Collapse

What I've noticed is a growing pattern:

- 39% of Gen Z now say they will never take financial advice from social media again — they've been burned

- 33% of millennials say the same thing — even older Gen Z has learned this lesson

- Yet 63% of Gen Z still use social media for financial information — the contradiction shows the trap. People know it's unreliable, but the pull is strong

The Reddit communities are where the actual conversation is shifting. People are increasingly focused on:

- Boring, consistent wealth-building (index funds, dollar-cost averaging)

- Questioning the hype of get-rich-quick strategies

- Discussing the emotional and psychological costs of optimization culture

- Building wealth privately, without an audience

This is the counter-movement crystallizing.

The Boring Path Actually Works (And It's Winning)

Let me show you some actual data on what builds wealth.

The most boring wealth-building strategies in the world are also the most reliable.

Boring Strategy #1: Consistent Saving + Index Funds

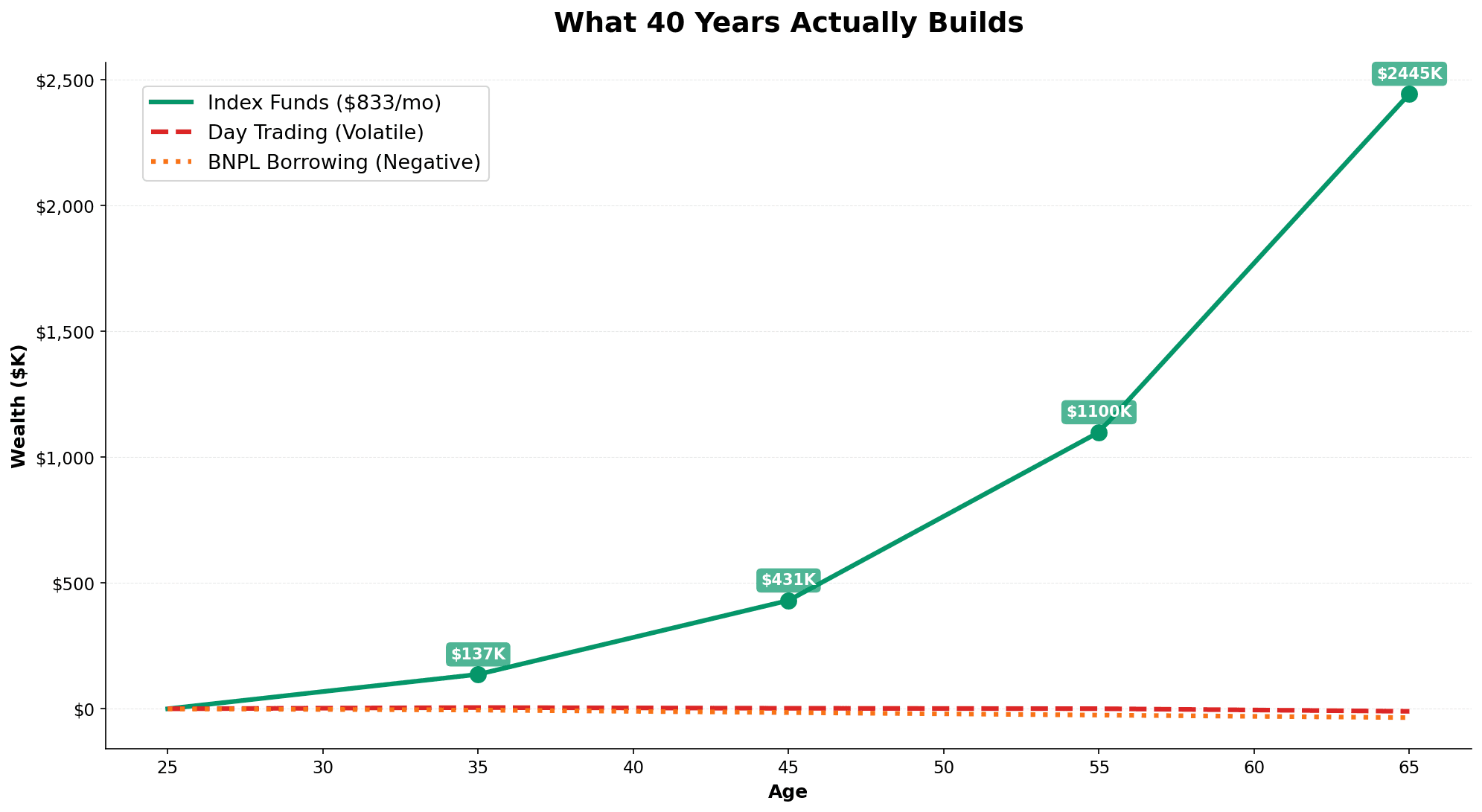

Take a 25-year-old with a $50K salary who saves 20% ($10K per year, $833/month) and invests it in a total market index fund earning 7% annually (the historical average). They don't try to time the market. They don't pick individual stocks. They just invest it mechanically, every month, regardless of what the market is doing.

At 35: $136,876 At 45: $430,721 At 55: $1,099,566 At 65: $2,444,633

That's $2.4M from a mechanical, zero-skill-required process. No timing. No picking winners. No cryptocurrency. Just consistent contribution and patience.

Now, what if this person actually tried to beat the market? Started day trading, thought they'd found an edge, took on more risk?

According to FINRA data, here's the realistic outcome:

- Year 1: 85% of active traders lose money

- Year 2: Only 13% of day traders maintain profitability

- 5-year horizon: Less than 1% are profitable

The person who stayed boring is now $2.4M richer. The person who tried to beat the market is probably broke and exhausted.

This is the most important comparison I can make: boring wins. Consistently. Over decades.

Boring Strategy #2: Debt Payoff + Wage Growth

Maria starts at $45K salary, age 30, with $18K in student debt. She commits to staying in her job and requesting annual raises (realistic: 3-4% per year). She pays off her debt in 5 years through consistent payments. Then she invests the freed-up payment ($400/month) into retirement accounts.

By age 40, her debt is gone. By age 60, she's accumulated $385K just from that single redirect. Meanwhile, her salary has grown 35%, giving her more capacity to save for other goals.

Again: boring. Unglamorous. Nobody makes a TikTok about it. But it works.

Boring Strategy #3: BNPL Avoidance

Wealth-building isn't just about what you do. It's about what you don't do.

Buy Now, Pay Later (BNPL) is a great example. FinTok promoted it heavily as "liberating," as a "smarter way to shop." The reality:

- 47% of BNPL users paid late on a BNPL loan in the past year — they're missing payments

- 25% of BNPL users now use it for groceries — essential purchases, meaning they're borrowing for survival

- 34-41% report at least one late payment — despite claims that BNPL is easier and more manageable

The people building real wealth aren't using BNPL at all. They're not using it because it's a wealth destroyer. It removes the friction that creates good financial decisions. When you feel the sting of paying immediately, you're more thoughtful. When that friction disappears, you spend more, save less, and end up in a debt cycle.

The anti-influence approach is simple: pay for things when you can afford them. Don't borrow. If you can't afford it immediately, don't buy it.

That kills virality. It also kills debt.

How to Build Financial Confidence Without an Audience

Here's the thing about the people who actually build wealth: nobody knows about it.

Your neighbor who's a millionaire by 50? You have no idea. She's driving a 2015 Toyota, wearing Target clothes, grocery shopping at Aldi. She doesn't post about her wins. She doesn't need validation.

Meanwhile, the person posting net worth updates and flexing their portfolio? They're seeking something — validation, probably. Or engagement. Or they're selling a course.

The irony is that privacy is a wealth-building advantage. The less visible your money is, the less you feel compelled to spend it maintaining an image. And the more it compounds.

Redefining Wealth (Privately)

Most wealth-building advice asks you comparative questions: "What's your net worth?" "What's your savings rate?" "How much do you have invested?"

These are comparative metrics. They only make sense in relation to other people, which immediately puts you in a comparison trap.

The anti-influence approach asks different questions:

"Can I cover an emergency without panic?" Not "Do I have $50K?"

"Am I saving consistently without stress?" Not "Am I saving 40%?"

"Does my spending align with my actual values?" Not "Is my spending optimal?"

These are private metrics. You don't need anyone else to know them. Better if nobody does.

The research backs this up: social comparison leads to poorer and riskier financial decision-making, regardless of how often you encounter it. And 45% of Americans now define wealth in terms of happiness rather than net worth. Another 37% define it in terms of physical health.

The old definition (net worth flex) is losing. The new definition (private security, health, autonomy) is winning.

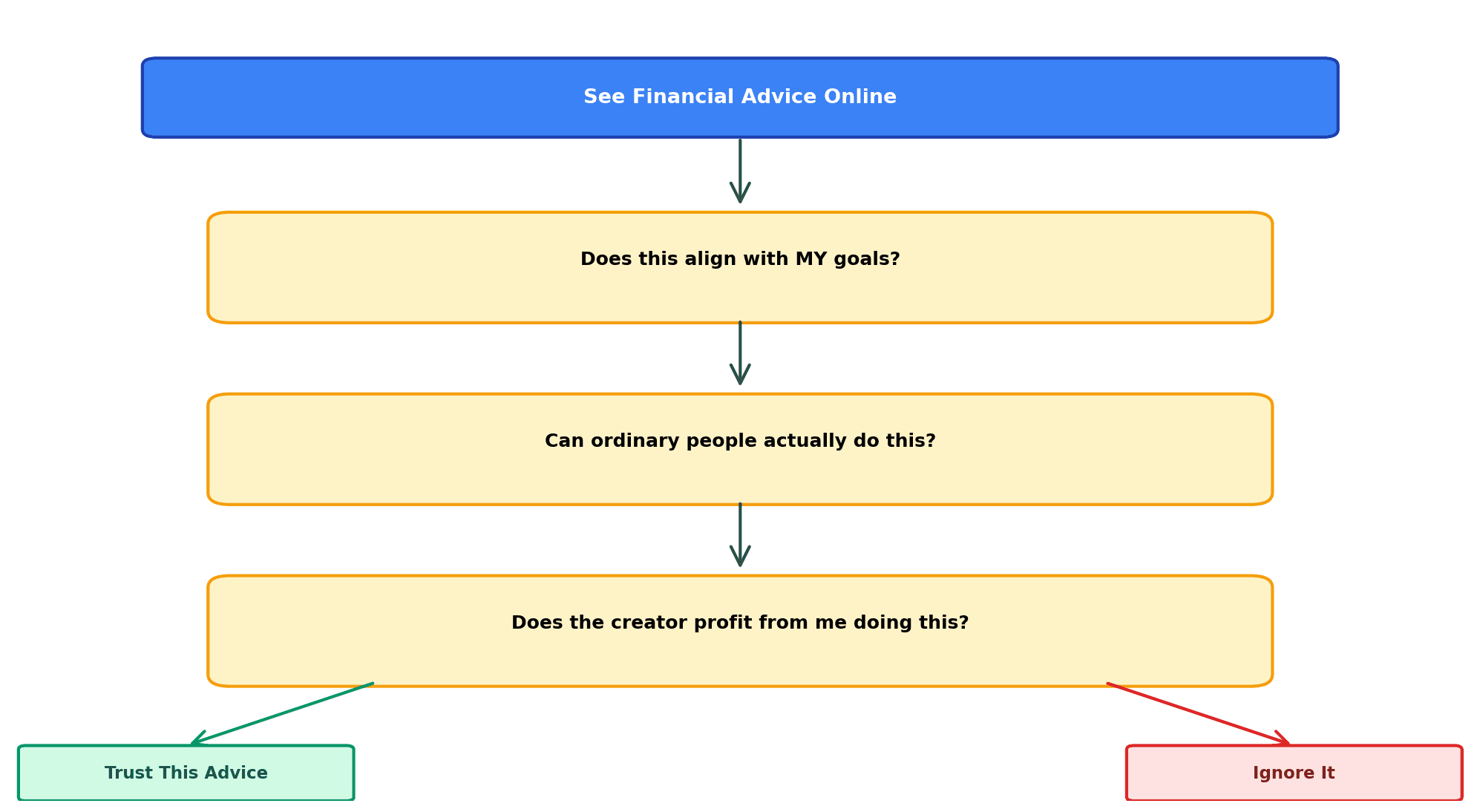

The 3-Question Filter

When you see financial advice online, ask yourself three critical questions:

Question 1: Does this align with MY goals? Not the creator's. Not the viral narrative. Your goals.

If your goal is financial security and time with family, and the advice is "maximize side hustles to work 60-hour weeks," the answer is no. Ignore it.

Question 2: Can ordinary people actually do this? This filters out 80% of misleading advice.

"I turned $5K into $50K" — can an ordinary person do this consistently? No. 99% fail. The statement is technically true but not replicable.

Question 3: Does the creator profit from me following this? If their profit is more lucrative than you actually succeeding, the advice is suspect.

Apply these three questions. You'll disqualify most advice immediately.

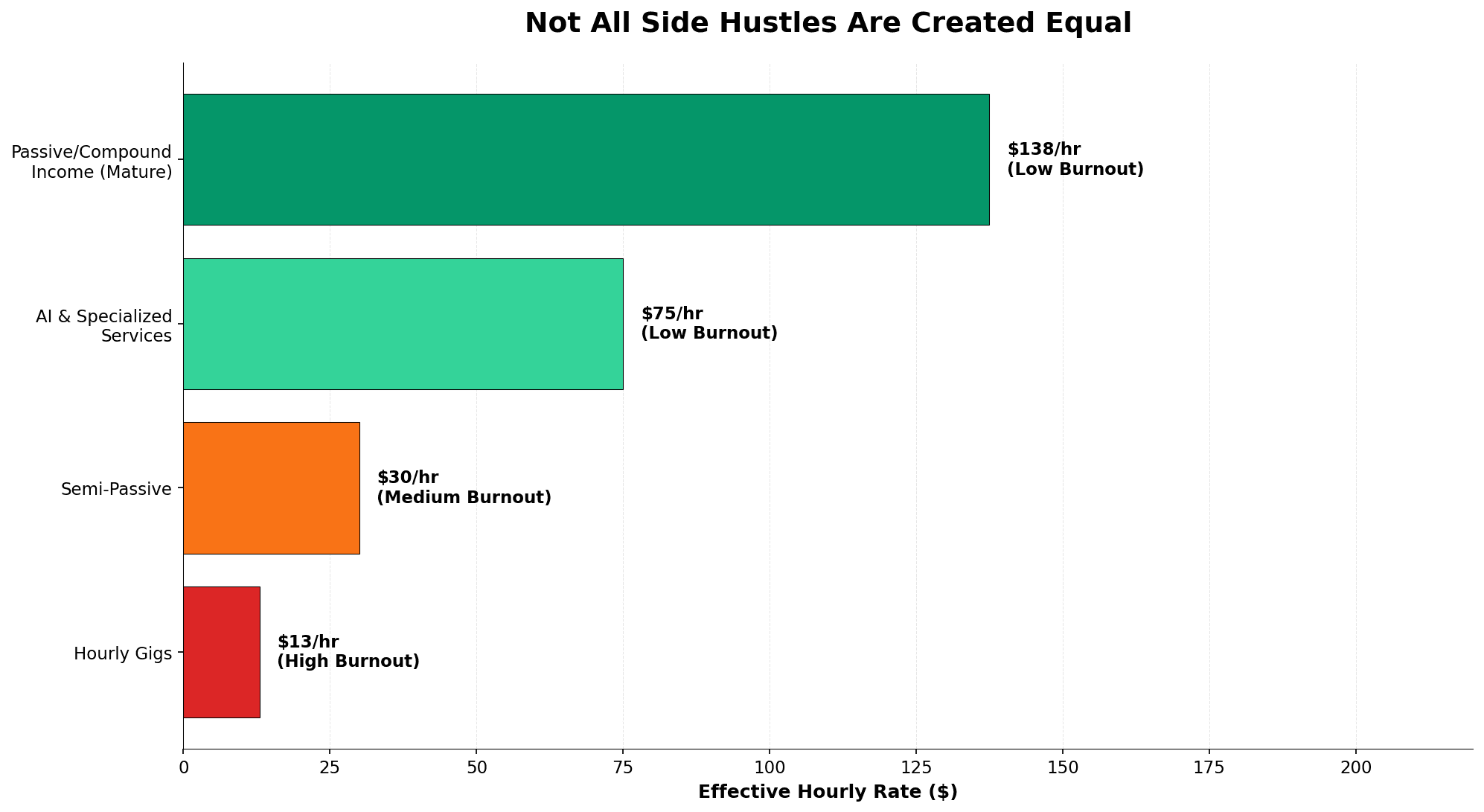

The Side Hustle Reality Check

You've probably seen posts claiming side hustles are the path to wealth. But there's a spectrum of side hustle effectiveness that matters. Some drain your time and energy. Others actually compound.

The key is: not all income sources are created equal. A side hustle that requires 15 hours a week at $15/hour is worse than minimum wage when you account for taxes. But a side hustle that generates $500/month with just 5 hours of setup and 2 hours of monthly maintenance? That compounds into real wealth.

This is where most FinTok advice fails. It doesn't distinguish between time-for-money hustle (which exhausts you) and genuine secondary income streams (which build wealth).

Your Next Move

If you're ready to build real wealth without the hype, start with fundamentals: a simple budget, consistent saving, boring index funds.

My Financial Freedom Tracker is private — no social media integration, just you and your actual numbers. It's the anti-influencer version of tracking.

Then read these foundational pieces:

- How to Start a Budget — the unsexy foundation that actually works

- The Complete Guide to FIRE — unglamorous, reliable, realistic

- Understanding the BNPL Trap — what the algorithm won't show you

Your wealth doesn't need an audience. It just needs consistency, discipline, and time.

Let's build something boring. Something that actually works.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.

Master Your Money

Master Your MoneyAI Scams Stole $21 Billion: How to Protect Yourself in 2026

AI scams hit a record $20.9B and could reach $40B by 2027. Scammers clone a loved one's voice from 3 seconds of audio. Here's the calm, free, afternoon-long defense playbook to protect your money in 2026.

Master Your Money

Master Your MoneyPrediction Markets: Why 69% of Polymarket Users Lose

69% of Polymarket users lose money and the top 1% take 76.5% of profits. The math, why Gen Z is targeted, and a 30-day reset plan.