Roth Conversion Ladder: Retire Early, Skip the 10% Penalty

TL;DR: A Roth conversion ladder moves pre-tax 401(k)/IRA money into a Roth IRA in annual chunks; five years after each conversion, that chunk comes out penalty-free — even at age 45. In the worked example below, a couple pulls $945,000 from a $1.2M 401(k) before 59½ at an effective federal tax rate around 7%. The catch: the ladder needs a five-year head start of bridge money, and three hidden cliffs (ACA subsidies, IRMAA, NIIT) can quietly claw back thousands if you convert too much in one year.

New to early retirement and FIRE strategy?

If you're just starting, these three articles give you the foundation this one builds on:

- The FIRE Movement — what financial independence actually means and why it's possible

- What Is Coast FIRE — the lower-effort path to early retirement most people miss

- HSA: The Stealth Retirement Account — the other tax-free vehicle every FIRE saver needs

Sarah retires on her 45th birthday with $1.2 million in her old 401(k) and a homemade cake.

Two days later her husband Jake — who also walked away from his job — opens the spreadsheet they've been building for three years and stares at one number: $120,000.

That's how much penalty they would pay if they tried to withdraw their entire $1.2 million today. The IRS doesn't let you touch tax-deferred retirement money before age 59½ without slapping a 10% early-withdrawal penalty on every dollar — plus charging full ordinary income tax on top of it.

For Sarah and Jake, that's a 14.5-year prison sentence on their own money.

Here's the thing nobody tells you when you start saving for FIRE: building a $1 million 401(k) is the easy part. Getting at it before 59½ — without losing six figures to penalties — is the part the rest of the personal-finance internet quietly skips.

The Roth Conversion Ladder is how the FIRE community escapes. It's the most important tax strategy you've probably never seen explained correctly. Let me walk you through it the way I wish someone had walked me through it: with concrete dollars, 2026 tax brackets, the three hidden cliffs nobody warns you about, and a fully worked example you can swap your own numbers into.

By the end of this article you'll know exactly how Sarah and Jake will withdraw $945,000 from their 401(k) before age 59½ — and pay an effective federal tax rate around 7% along the way.

The Problem: $1.2 Million You Can't Touch

Here's the trap millions of savers walk into without realizing it.

When you contribute to a 401(k), Traditional IRA, 403(b), or 457, you get an immediate tax deduction. The dollars go in pre-tax. They grow tax-deferred. And then — when you withdraw — you pay ordinary income tax on every dollar.

That's the deal. The IRS waited a long time to tax those dollars; they're going to tax them eventually.

The problem for early retirees is the age 59½ rule. Pull out a single dollar before then and you owe:

- Ordinary income tax at your marginal rate (could be anywhere from 10% to 37%)

- A 10% early-withdrawal penalty stacked on top

If you're a 45-year-old retiree with $0 of other income, withdrawing $60,000 would cost you about $3,500 in income tax + $6,000 in penalty = $9,500 in tax friction on $60,000 of spending. That's a 16% haircut you don't get back.

Multiply that across 14.5 years of retirement and the penalty alone burns close to $87,000 of your portfolio. That's roughly the cost of a college education, gone — to the IRS — for the crime of retiring early.

There are exactly four legal ways out of this trap:

- Don't touch the money. Live on taxable + Roth principal until 59½. (Works only if you have an enormous taxable cushion.)

- 72(t) SEPP. Take Substantially Equal Periodic Payments. Rigid, locks for 5 years or until 59½, whichever is later.

- Specific exemptions. First-time home, education, medical bills above 7.5% of AGI, certain birth/adoption costs. Narrow.

- The Roth Conversion Ladder. Convert Traditional → Roth in the year, wait five years, withdraw the converted principal tax-and-penalty-free at any age.

For most FIRE retirees, the ladder is the answer. Let's see why.

What a Roth Conversion Ladder Actually Is (In Plain English)

Here's the trick the strategy exploits.

The IRS treats Roth IRA contributions and conversions differently than Roth IRA earnings:

- Roth contributions can be withdrawn at any time, at any age, with zero tax and zero penalty. (The money was already taxed before it went in.)

- Roth conversions can be withdrawn at any age, with zero tax and zero penalty — but only after a 5-year seasoning period.

- Roth earnings (the growth) can be withdrawn tax-and-penalty-free only after age 59½ AND after the account has been open 5+ years.

The Roth Conversion Ladder uses rule #2.

Each year, you "convert" a chunk of your Traditional 401(k) or Traditional IRA into a Roth IRA. That conversion counts as ordinary income for that year — you owe income tax on it (no 10% penalty though, because it's a conversion, not a withdrawal). Five tax years later, you can withdraw the exact dollar amount you converted, tax-free and penalty-free, at any age.

Run that for five sequential years and you've built a self-replenishing ladder where every year you convert one new "rung" and pull the rung you converted five years ago.

That's the entire mechanic. Everything else in this article is the math, the cliffs, and the worked example.

The Five-Year Rule (Per Conversion, Not Per Account)

Here's the part that trips up almost every first-time reader — and most podcast hosts.

Each conversion has its own 5-year clock. Not the account. The conversion.

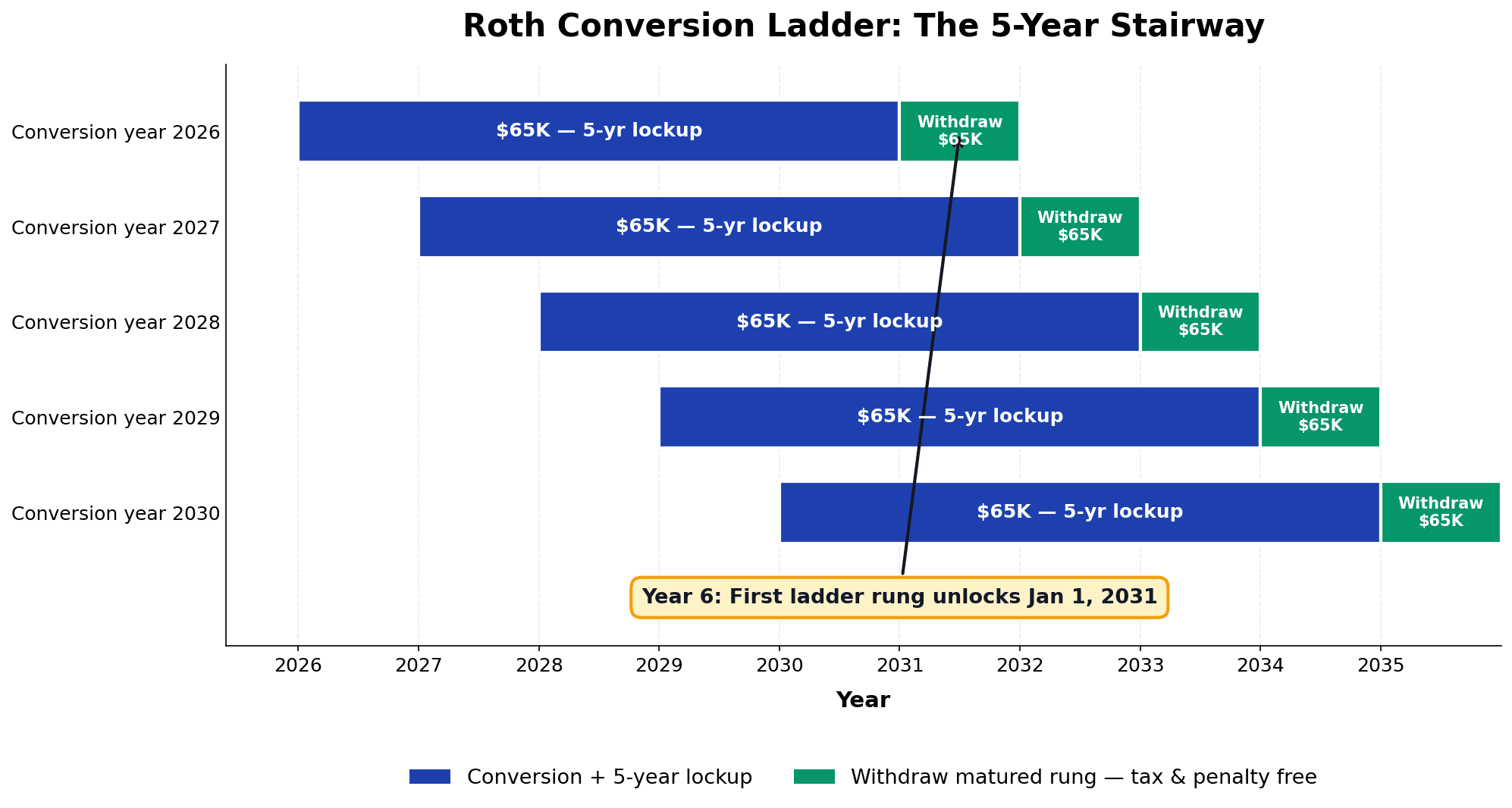

The clock starts on January 1 of the year you do the conversion, regardless of what month you actually executed it. A $65,000 conversion done on December 28, 2026 has the same clock as one done on January 4, 2026 — both mature on January 1, 2031.

So if you convert $65,000 in 2026, $65,000 in 2027, $65,000 in 2028, $65,000 in 2029, and $65,000 in 2030, you have five separate clocks:

- 2026 conversion → withdrawable Jan 1, 2031

- 2027 conversion → withdrawable Jan 1, 2032

- 2028 conversion → withdrawable Jan 1, 2033

- 2029 conversion → withdrawable Jan 1, 2034

- 2030 conversion → withdrawable Jan 1, 2035

Each one is its own thing. If you withdraw the 2026 conversion in 2031, the 2027 conversion's clock is unaffected — it still matures in 2032 as planned. Likewise, if you skipped 2028 (because your income was unexpectedly high that year), the rest of the ladder is fine. You just have a one-year gap to bridge.

Withdrawing converted principal before its individual 5-year clock matures triggers a 10% penalty — the same penalty as a regular early withdrawal. (You don't owe income tax again, because the tax was paid at conversion. But the 10% penalty does apply.)

This per-conversion clock is also why the "first 5 years" of FIRE require careful planning. Your year-1 conversion can't be withdrawn until year 6. Years 1-5 of retirement, you live on something else. We'll cover that in a minute.

Sarah's Ladder: A Year-By-Year Walkthrough

Let's make this fully concrete with a worked example.

Sarah, 45, retires May 2026 with husband Jake, 47 (also retired):

- $1.2M Traditional 401(k) (rolled over to Traditional IRA after separation)

- $300K taxable brokerage in low-cost broad-market ETFs

- $80K of direct Roth IRA contributions accumulated over 15 years (already withdrawable tax-free)

- $0 other income (no rentals, no part-time work, no pensions)

- State: Texas (no state income tax)

Their plan: Spend $60,000/year. Convert $65,000/year from Traditional → Roth. Live off taxable brokerage for years 1-5. Start withdrawing matured ladder rungs in year 6.

Let's walk it.

Year 2026

Income: $0 wages + $65,000 conversion + ~$3,000 dividends + ~$8,000 long-term capital gains from selling some taxable shares to fund spending = ~$76,000 gross.

Tax calculation (married filing jointly):

- Conversion + ordinary income: $65,000 + $3,000 = $68,000 ordinary income

- Long-term capital gains: $8,000 (taxed separately at 0% bracket since combined income is well under $96,700 MFJ threshold)

- Standard deduction: -$32,200

- Taxable ordinary income: $35,800

- Tax: $24,800 × 10% = $2,480 + ($35,800 - $24,800) × 12% = $1,320 → federal tax ≈ $3,800

- Long-term capital gains tax: $0 (0% bracket)

They net: $60,000 from selling taxable shares (cost basis ≈ $52K, gain $8K — taxed at 0%). They live on it. The $65,000 conversion sits in Roth IRA. The 5-year clock starts.

Year 2027

Same playbook. Convert $65,000. Federal tax ≈ $3,800. Live on $60K from taxable brokerage. Roth balance now $130K + growth.

Year 2028

Same. Tax ≈ $3,800. Taxable brokerage drawn down to ~$200K. Roth balance ~$200K + growth.

Year 2029

Same. Tax ≈ $3,800. Taxable brokerage ~$140K.

Year 2030

Same. Tax ≈ $3,800. Taxable brokerage ~$80K — getting low. But the 2026 conversion's clock matures January 1, 2031.

Year 2031 — the first ladder rung unlocks

Sarah is now 50. She withdraws $65,000 from Roth (the 2026 conversion principal). Federal tax: $0. Penalty: $0. She lives on that $65,000 (plus she sells $5K from taxable to keep the same lifestyle).

She also converts another $65,000 from Traditional → Roth that same year. Tax on the new conversion: ~$3,800. The 2031 clock starts.

The ladder is now self-replenishing.

Years 2032-2040: cruise mode

Each year, withdraw the matured rung, convert the next year's rung. Tax stays around $3,800/year.

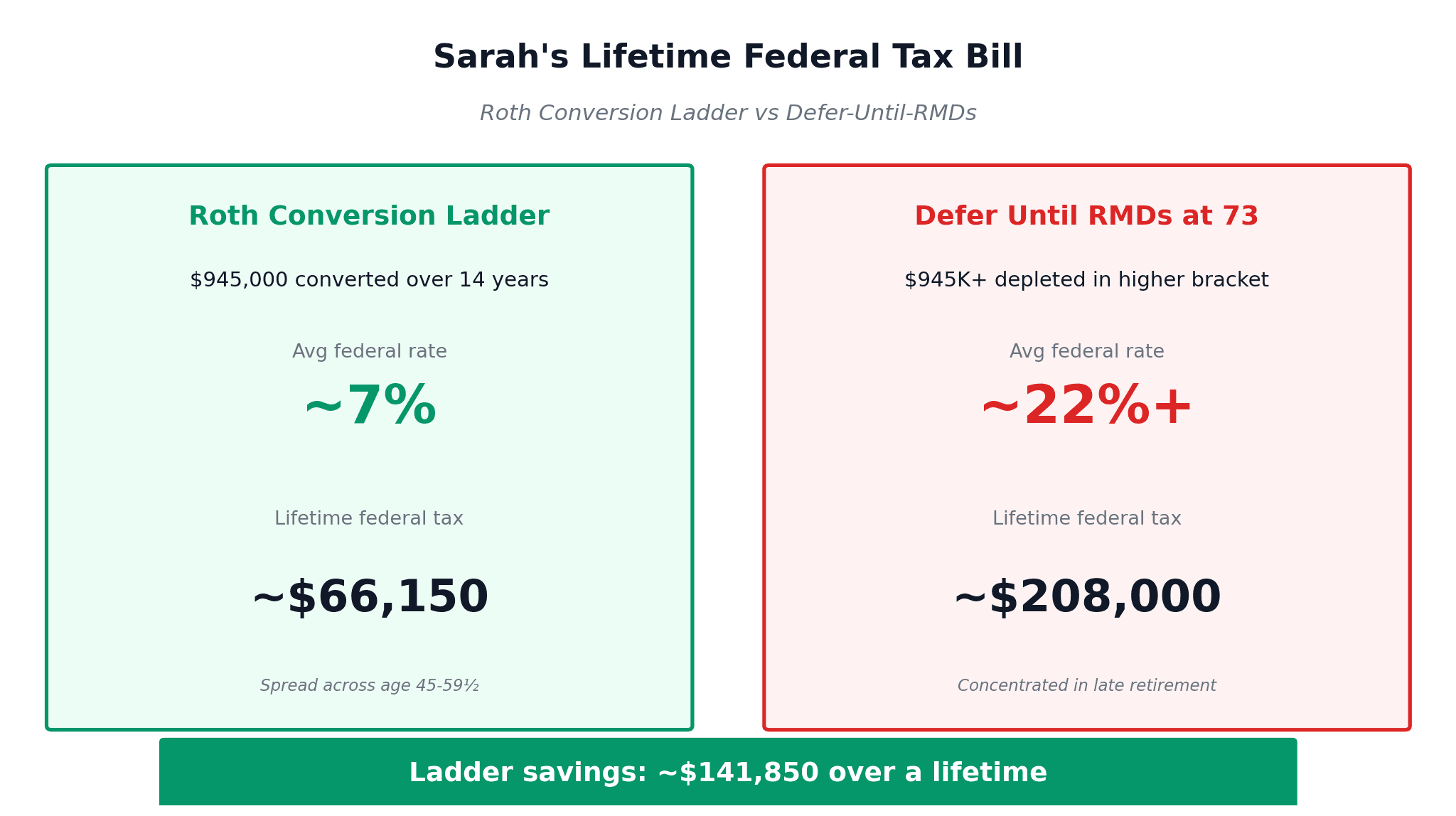

By age 59½, Sarah has converted ~$945,000 from Traditional → Roth. Average federal tax rate: roughly 7%. Had she let those dollars sit in Traditional and triggered RMDs in her 70s at the (likely 22%+) marginal bracket, the lifetime tax bill would have been $80,000+ higher.

That's the magic. Early retirement isn't just about quitting work. It's about exploiting the years when your income is low to convert tax-deferred dollars into permanently tax-free dollars.

The Math: How Much To Convert Each Year (2026 Brackets)

Here are the actual 2026 federal income tax brackets you need to plan around. The OBBBA (One Big Beautiful Bill Act, passed in 2025) made the TCJA brackets permanent, so these numbers are stable for the foreseeable future.

2026 Standard Deduction

- Single: $16,100

- MFJ: $32,200

- Head of Household: $23,625

2026 Federal Income Tax Brackets (MFJ)

| Marginal Rate | Income Range (MFJ) |

|---|---|

| 10% | $0 – $24,800 |

| 12% | $24,800 – $100,400 |

| 22% | $100,400 – $206,800 |

| 24% | $206,800 – $403,550 |

| 32% | $403,550 – $512,450 |

| 35% | $512,450 – $768,700 |

| 37% | $768,700+ |

(The single-filer brackets are roughly half these thresholds.)

The key planning question: what conversion size should you target?

The answer most FIRE bloggers give — "fill up the 12% bracket" — is correct for most early retirees in most situations. Here's why:

Your future RMDs will likely push you into the 22% bracket or higher. Converting at 12% today and avoiding 22% later is a permanent 10-percentage-point arbitrage. Multiplied over decades and seven figures, that's worth six-figure dollars.

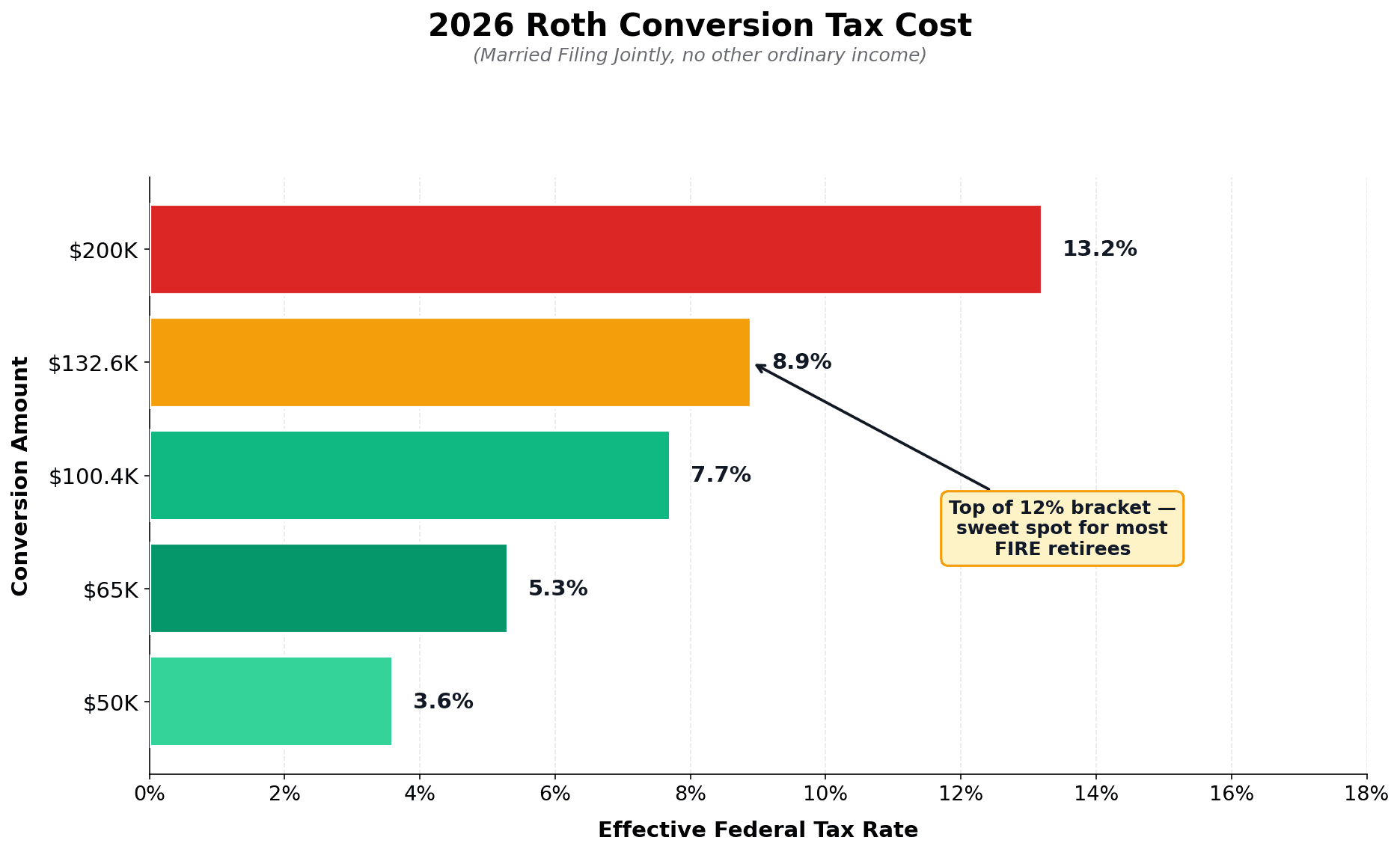

For an MFJ couple with no other ordinary income, the 12% bracket caps out at $100,400 of taxable income. Adding back the $32,200 standard deduction means you can convert up to $132,600 per year while staying entirely within the 10%-12% brackets.

Here's a quick reference table for what each conversion size actually costs in federal tax (MFJ, no other ordinary income):

| Convert | Standard Deduction | Taxable | Federal Tax | Effective Rate |

|---|---|---|---|---|

| $50,000 | $32,200 | $17,800 | $1,780 | 3.6% |

| $65,000 | $32,200 | $32,800 | $3,440 | 5.3% |

| $100,400 | $32,200 | $68,200 | $7,724 | 7.7% |

| $132,600 | $32,200 | $100,400 | $11,792 | 8.9% |

| $200,000 | $32,200 | $167,800 | $26,422 | 13.2% |

The Mad Fientist (the FIRE community blogger who popularized this strategy) recommends conversions up to the top of the 12% bracket as the "sweet spot" — high enough to make meaningful progress in 5 years, low enough that the marginal rate stays well below your future RMD bracket.

But — and this is the part most articles skip — that's not the whole story. Three other constraints can lower the maximum conversion amount well below the 12% ceiling.

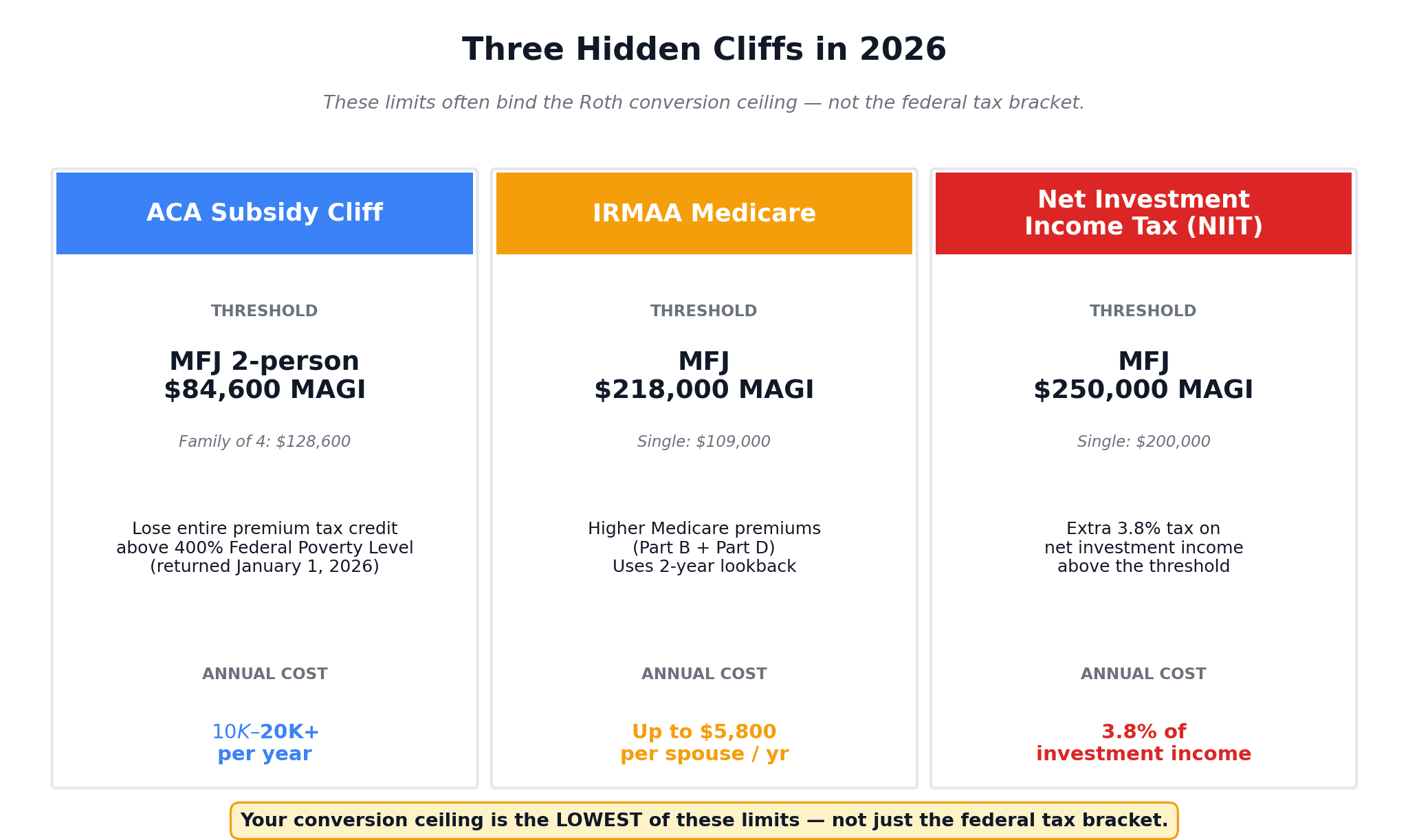

Three Hidden Cliffs That Wreck The Ladder (ACA, IRMAA, NIIT)

If your only constraint were the federal income tax bracket, planning would be simple. It isn't. Three other thresholds quietly bind the conversion size for most early retirees:

Cliff #1: The ACA Subsidy Cliff (returned January 1, 2026)

If you retire before age 65, you need health insurance. Most FIRE retirees get it through the ACA Marketplace and rely on Premium Tax Credits to make premiums affordable.

Here's the trap: Premium Tax Credits cut off entirely above 400% of the Federal Poverty Level. The "ARPA smoothing" that softened this cliff from 2021 through 2025 expired on January 1, 2026.

For 2026, the 400% FPL thresholds are:

- 1-person household: $62,600

- 2-person household: $84,600

- 3-person household: $106,600

- Family of 4: $128,600

Earn $1 over the cliff and you lose the entire subsidy. That can mean a $10,000-$20,000+ swing in annual healthcare costs. For Sarah and Jake, the 2-person 400% FPL cap of $84,600 is the real constraint — well below the $132,600 federal-tax-only ceiling.

Practical implication: if you're pre-65 and using the Marketplace, your conversion target is whatever keeps total Modified Adjusted Gross Income (MAGI) below the 400% FPL line for your household size. For Sarah's couple, that's a conversion ceiling closer to $80,000 — not $132,600. Their $65,000 plan leaves comfortable headroom.

Cliff #2: IRMAA (Medicare Income Threshold)

Once you hit Medicare at 65, your Part B and Part D premiums are calculated based on your income from two years ago. That's the IRMAA lookback.

For 2026, IRMAA surcharges kick in above:

- Single: $109,000 MAGI

- MFJ: $218,000 MAGI

Cross those thresholds even by $1 and your Medicare premiums climb in tiers, with the top IRMAA bracket adding about $480/month per spouse to Medicare premiums.

Practical implication: if you're 63 or 64, you're now planning conversions that affect your Medicare premiums two years out. Most FIRE retirees stay well below IRMAA naturally — but high-balance converters trying to "front-load" before RMDs can accidentally trigger surcharges. Plan accordingly.

Cliff #3: NIIT (Net Investment Income Tax)

Above MAGI of $250,000 MFJ ($200,000 single), an additional 3.8% NIIT is assessed on investment income. For high-balance converters trying to do $200K+ years, this becomes a real cost.

Most early retirees never come close. But it's worth knowing the line is there.

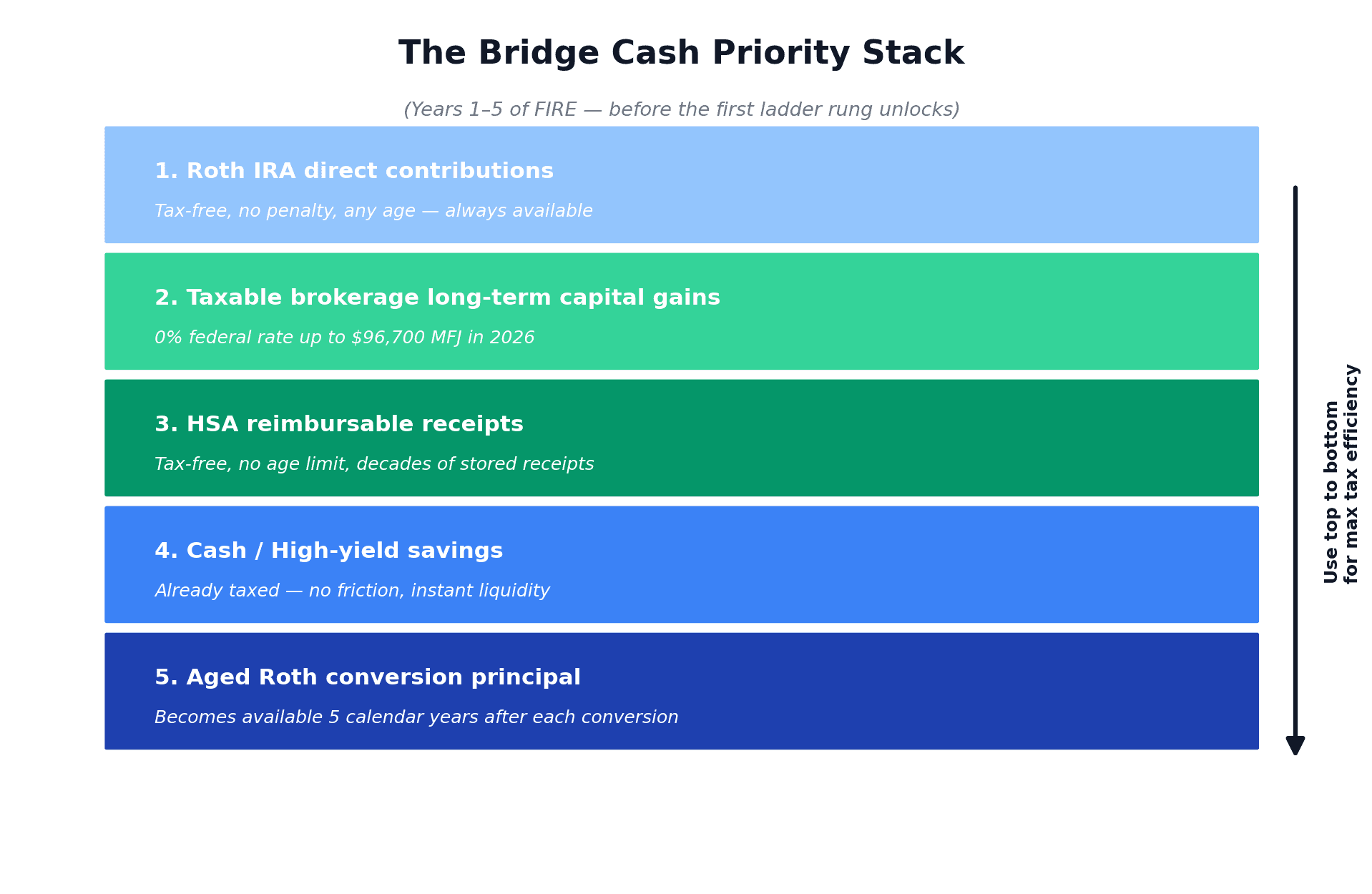

Bridging the Gap: Where Sarah's $300K of Spending Comes From

The ladder takes 5 years to start delivering withdrawable cash. So years 1-5 of retirement, you have to live on something else.

Here's the priority stack I recommend, in tax-efficiency order:

1. Existing direct Roth IRA contributions (always tax-and-penalty-free at any age) 2. Taxable brokerage long-term capital gains (0% federal rate up to $96,700 MFJ in 2026) 3. HSA reimbursable medical receipts (tax-free, no age restriction — see HSA: The Stealth Retirement Account for the full receipt-banking strategy) 4. Cash / high-yield savings (already taxed, so no friction) 5. Roth principal of any earlier conversions that have already aged 5+ years

For Sarah, that's $300K taxable + $80K direct Roth = $380K of bridge cash. At $60K/year of spending net of conversion taxes, that's just over 6 years of bridge — enough to get her past the 5-year ladder gap with a small buffer.

If your bridge cash is thin, you have three options:

- Convert less, work part-time. A 2-day-per-week consulting gig that pays $30K/year stretches a thin bridge dramatically. It's also why "BaristaFIRE" exists — see Time Freedom Over Retirement for why partial work in early retirement isn't failure.

- Combine with 72(t) SEPP for years 1-5 only. Run SEPP just long enough to get to year 6 of the ladder, then turn it off (the 5-year minimum applies — plan accordingly).

- Delay retirement by 1-2 years. Build a thicker taxable buffer and start converting before quitting if your salary still leaves headroom in the 12% bracket.

Roth Conversion Ladder vs 72(t) SEPP: Which Is Right For You?

You'll see these two strategies presented as competitors. They're not — they're complements. But the ladder is preferred for almost everyone with a meaningful taxable cushion.

| Roth Conversion Ladder | 72(t) SEPP | |

|---|---|---|

| Setup | Convert annually; track 5-year clocks | Calculate fixed annual payment; lock in |

| Flexibility | High — skip a year if income spikes | None — modify and pay back-penalties on everything |

| Modification penalty | None | 10% penalty on ALL prior payments + interest |

| Years until first dollar | 5 | Immediate |

| Lock duration | None | 5 years OR until 59½, whichever is longer |

| Best for | Retirees with 5+ years of bridge cash | Retirees who need income immediately |

| Tax efficiency | High — sized to your bracket each year | Mediocre — fixed amount regardless of bracket |

The ladder wins on flexibility, tax efficiency, and recovery from mistakes. SEPP wins on immediate cash flow if you don't have enough bridge.

Many retirees use both: SEPP to bridge years 1-5, ladder taking over in year 6. The combined approach is more complex but optimal when bridge cash is tight.

Common Mistakes That Cost Retirees Five Figures

I've watched thousands of FIRE-aspiring savers approach the ladder. The same five mistakes show up over and over.

Mistake #1: Withholding tax from the conversion. When you convert $65,000, you owe roughly $3,800 in federal tax. If you tell the custodian to withhold the $3,800 from the conversion itself (rather than paying it from outside funds), the IRS treats the withheld $3,800 as an early withdrawal — and slaps a 10% penalty on it. Always pay conversion tax from non-retirement funds.

Mistake #2: Forgetting the 5-year clock is per-conversion. "I converted in 2026, so my account is 'open' for 5 years" — wrong. Each conversion has its own clock. Withdraw a 2028 conversion in 2030 and you owe a 10% penalty even though your first conversion was in 2026.

Mistake #3: Ignoring state income tax. Sarah's example uses Texas (no state tax). If she lived in California, she'd owe an additional 9.3%-13.3% state tax on every conversion dollar. That moves the optimal conversion size down, sometimes meaningfully. States with no income tax (TX, FL, NV, WA, TN, SD, AK, WY) make the ladder dramatically more attractive — and a few FIRE retirees specifically relocate before retiring to capture this.

Mistake #4: Forgetting other ordinary income. Rental income, pensions, interest, side-hustle profits, even unemployment all count as ordinary income and stack with the conversion. If you have $20K of rental net income, your conversion ceiling drops by $20K. Run the calculation in late November after your year's actual income is mostly known, then size the December conversion precisely.

Mistake #5: Not coordinating with ACA subsidies. This is the most expensive mistake on the list. Crossing the 400% FPL line by $1,000 doesn't cost you a little subsidy — it costs you the entire subsidy. For most early retirees this is a $5,000-$15,000+ annual hit. Always model the ACA subsidy alongside the conversion; for most pre-65 FIRE retirees, ACA is the binding constraint, not the federal tax bracket.

How to Plan This in 30 Minutes With the Right Tools

You don't need a CPA to plan a Roth conversion ladder. You need four numbers and a system to track them.

The four inputs:

- Current Traditional balance. How much is in your 401(k), Traditional IRA, and any rolled-over pre-tax money.

- Current taxable brokerage + direct Roth contribution balance. Your bridge cash.

- Target annual retirement spend. Most FIRE planners use $40K-$80K per couple.

- Target retirement age. This sets the conversion start year and the ladder length needed before age 59½.

The system:

For most savers I work with, the workflow looks something like this. Track your three buckets — Traditional, Roth, Taxable — separately in a tool that tells you when your bridge cash is enough to cover 5 years of spending. Project the ladder forward using your expected return assumptions. Once retired, run the conversion calculation each November based on actual current-year income.

If you want a one-stop place to track all of this, MFFT's net worth tracker was built for exactly this kind of scenario. You can categorize accounts as Traditional, Roth, or Taxable, see the bucket balances at a glance, and watch your bridge cash grow as you accumulate it. Combine it with the FIRE planning math from the FIRE Movement guide and you've got the whole picture without a CPA bill.

The tool isn't doing anything magic. The math itself is straightforward. What it does is make the buckets visible — which is what 95% of pre-retirees never bother to do, and which is exactly why most people are blindsided by the ladder problem at age 50.

What If The 2026 Rules Change?

A reasonable question. Tax rules change. The OBBBA made the TCJA permanent, but "permanent" in tax law means "until Congress decides otherwise."

A few specific risks worth knowing:

- The 5-year per-conversion rule is in IRC §408A(d)(3)(F). Repealing it would require explicit legislation. There's no current proposal on either side of the aisle to do so.

- The 10% early-withdrawal penalty is in IRC §72(t). Same — stable for the foreseeable future.

- ACA subsidies and IRMAA brackets change annually for inflation. The 400% FPL cliff is the real political wildcard — a future Congress could re-enable the ARPA smoothing, raise the threshold, or eliminate the cliff entirely.

- State tax rates change every legislative session. If you're in a high-tax state, monitor your state's treatment of conversions.

The strategy itself has been stable since 1997 (the Roth IRA's introduction) and rests on tax mechanics that have survived four major tax reforms. It's about as solid a long-term plan as personal finance offers.

If anything, the 2026 retirement rule changes — particularly the higher Traditional 401(k) contribution limits and the Roth catch-up mandate for high earners — make the ladder more relevant, not less. High earners forced into Roth catch-ups are accidentally building a bigger Roth basis in their 50s. That's a bigger ladder waiting to be run when they retire.

The Bottom Line: Why Every FIRE Saver Should Plan The Ladder

Most personal-finance articles end with a soft CTA. Let me end with a sharper claim.

If you're aiming for financial independence before age 60 and you don't know how the Roth Conversion Ladder works, you don't yet have a real plan.

That's not gatekeeping — it's just the math. You can save 50% of your income for 15 years, hit your FI number at 45, walk away from work, and watch the IRS take $87,000 out of your portfolio in penalties because you didn't think through the bridge.

Or you can spend 30 minutes today modeling the ladder. Identify whether your current allocation skews too heavily toward Traditional (most FIRE savers do — they chase the deduction). Adjust your contribution mix to build a thicker taxable cushion. By the time you retire, the ladder is already pre-funded and the bridge problem disappears.

This is also why the 3-bucket allocation — Traditional, Roth, Taxable — matters more than the headline savings rate. A 30% saver with a balanced 3-bucket allocation will reach FI faster than a 35% saver with everything in Traditional, because the Traditional-heavy saver loses years of progress to penalty bridges they can't fund.

Plan the ladder. Build the bridge. Model the cliffs.

The ladder isn't optional knowledge if you're serious about financial independence before age 60. It's the difference between a portfolio you've earned and a portfolio you can actually use.

📩 Have questions about modeling your own Roth conversion ladder, the ACA cliff, or the bridge math? Email me at dennis.vymer@myfinancialfreedomtracker.com.

For tracking your three retirement buckets and seeing exactly how big your bridge cash needs to be, use MFFT's net worth tracker — no signup required, and built for exactly this kind of scenario. If you want the parallel tax-free vehicle most FIRE savers underuse, read our companion guide: HSA: The Stealth Retirement Account. And if you're earlier in the journey and not sure if FIRE is even realistic for you, start with What Is Coast FIRE — a lower-effort version of the same strategy.

The penalty isn't paid by people who don't have $1.2 million. It's paid by people who do — and didn't plan how to use it.

Make sure that's not you.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyStablecoin Savings Accounts: Is 8% Yield Worth the Risk in 2026?

My savings rate slid to 2.4% and an app dangled 7.2%. I almost bit. Here's where a stablecoin savings account's yield in 2026 really comes from, what the ads hide, and the math that stopped me.

Master Your Money

Master Your MoneyRent vs Buy in 2026: I Ran the Numbers, Kept Renting, and Invested the Difference

My uncle swears renting is throwing money away. So I built the rent vs buy 2026 model: renting wins in all 50 metros, but only if you invest the difference.

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.