Women & Investing: Close the $500K Wealth Gap in 5 Steps

New to investing or personal finance? If you're just getting started, I recommend checking out Investing Made Simple: What It Is and Why to Start — the fundamentals of index funds and market investing. Or dive into How to Build Wealth From Zero: The Equation That Works for Everyone — the wealth-building equation that applies to anyone. And if you're trying to escape the paycheck cycle first, start with How to Take Control of Your Finances (And Stop Living Paycheck to Paycheck).

Here's a stat that should hit you hard: 64% of women have never invested. Meanwhile, 47% of men haven't.

That 17-point gap doesn't sound like much. But over a lifetime, it compounds into roughly $500,000 in lost wealth per woman.

This isn't about intelligence. It's not about math ability. I'm going to walk you through the data, and you'll see something interesting: women investors who do participate actually outperform men on risk-adjusted returns. The issue is psychology and access, not capability.

Gen Z women are dominating FinTok, talking openly about money, and breaking generational shame cycles. That's real progress. But while they're building community on social media, 64% of women are still sitting on the sidelines — watching compound growth happen to other people.

This article breaks the psychology barrier, dispels the dangerous myths, and gives you a 5-step roadmap to close the gap fast. Not through extreme sacrifice or get-rich-quick schemes. Through math, discipline, and time.

The $500K Question: What Women Are Missing Out On

Let me start with a concrete example.

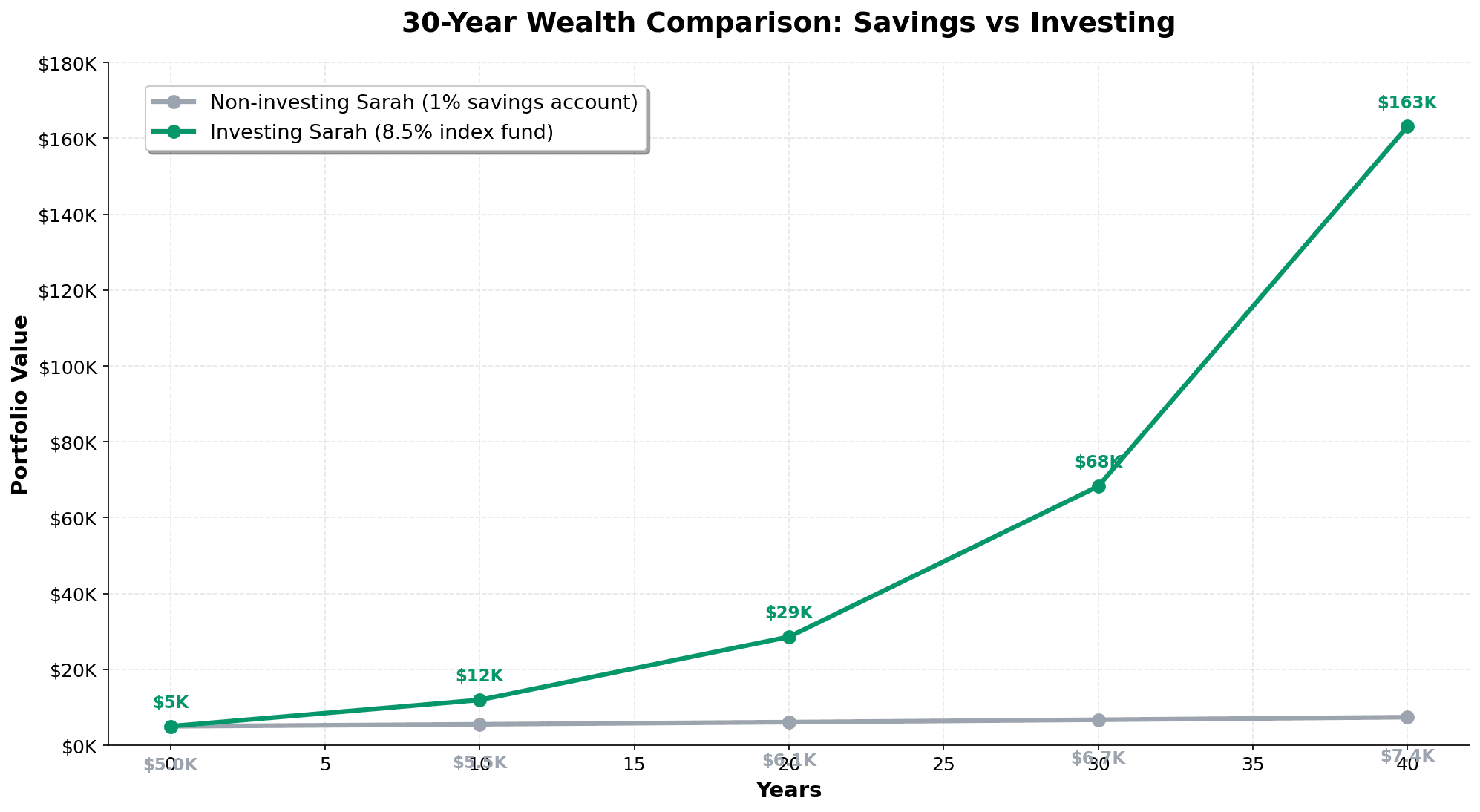

Sarah is 25 years old. She has $5,000 in a savings account earning 1% annually. She keeps her money "safe" — no investments, no risk. She plans to keep this pattern for 40 years until retirement at 65.

Her $5,000 grows to about $8,200. The interest earned: $3,200. Forty years of caution = barely keeping up with inflation.

Now imagine a different Sarah — same age, same $5,000 starting balance.

She invests it in a total stock market index fund. Average historical returns: 8.5% annually. She's not picking stocks. She's not paying an advisor. She's buying the whole market and holding it.

That same $5,000 at 8.5% annual returns becomes $171,500 by age 65.

The difference: $163,300 from a single decision.

Now add $100 per month invested:

Non-investing Sarah: $8,200 (savings at 1%) Investing Sarah: $377,400 (at 8.5% returns)

The gap widens to $369,200.

And this is before accounting for the wage gap. Women earn 83.6% of what men earn. That means women have less capital to invest in the first place — making early intervention more critical, not less.

The $500K+ gap cited in research isn't an exaggeration. It's the cost of waiting. It's the cost of believing you need permission, certainty, or a perfect starting point before you begin.

Here's what the data says:

- 64% of women have never invested (vs. 47% of men)

- Average female 401(k) balance: $59,000

- Average male 401(k) balance: $89,000

- Median female retirement savings: $50,000

- Median male retirement savings: $157,000

The $89K vs. $59K gap shows up by age 45. This compounds for another 20 years. By retirement, the wealth gap is insurmountable for many women.

But here's the thing: it doesn't have to be.

Psychology Over Math: Why Women Invest 26% Less Than Men

This is the part where I need to be honest about what's actually happening.

The gap is not because women are worse at math. It's because women are carrying psychological barriers that men typically aren't.

Only 31% of women feel "very confident" about investing. Compare that to 45% of men. Both groups can do the math. One group just feels like they can't.

When researchers ask women why they don't invest, the answers are:

- 45% say "insufficient funds"

- 27% say "lack of knowledge"

- 19% say "risk aversion"

But here's what's interesting: when you control for income, the knowledge barrier doesn't fully explain the gap. College-educated women earn 23.8% less than college-educated men—but the investment gap is still there even when you account for that earnings penalty.

This is classic impostor syndrome in action. Women have the capability. They're second-guessing whether they have the right to try.

The Confidence Paradox

Here's something wild: 19% of women say that hearing about "confidence gaps" actually discourages them from investing. They feel patronized. "You're just saying I'm scared. You're not helping."

eToro's research shows that constantly messaging about women's lack of confidence backfires. It reinforces the narrative that women are the problem.

But women aren't the problem. The educational and social system that didn't expose them to investing is the problem. The media that positions investing as a male activity is the problem. The financial industry that built products and marketing around men is the problem.

The women? They're fine. They just need a framework—not a pep talk.

The Risk Reality

Here's where the psychology gets interesting.

53% of women choose moderate investment approaches. Only 39% of men do. Women are more likely to choose a balanced portfolio (60% stocks / 40% bonds).

But is that more conservative approach actually wrong? Let's check the data.

Women investors outperform men by:

- 40 basis points annually (Fidelity 10-year study of 5.2 million accounts)

- 1.8% annually on a risk-adjusted basis (Warwick Business School)

Women buy and hold. Men trade frequently, incur more fees, make emotional decisions during volatility, and underperform.

So the "risk aversion" isn't a weakness. It's the secret to outperformance.

Dispelling 3 Dangerous Myths Gen Z Women Believe (From FinTok)

Here's where I need to address the elephant in the room: FinTok.

Gen Z women are leading a genuine financial revolution. 71% of young women now invest, up from 60% just two years ago. FinTok creators deserve credit for that.

But the same platform that's teaching women to invest is also spreading pseudoscience. (For a deeper dive into what Gen Z women are getting right and wrong on FinTok, read this analysis.)

Myth #1: Manifestation Replaces Math

The #MoneyManifestation hashtag has 1.7 million posts. Creators with millions of followers are teaching people to visualize wealth on specific "lucky" dates, write financial goals on astrologically optimal days, and spend money on manifestation crystals.

Here's the hard truth: There is zero scientific evidence that manifestation builds wealth.

Visualization has real psychological benefits—it increases motivation, reduces stress, helps you plan. But the wealth doesn't come from the intention. It comes from the behavior change that follows.

Madison, 23, was inspired by a FinTok manifestation post. She spent 30 minutes daily journaling about wealth, wrote her financial goals on the "optimal" Mercury retrograde date, and bought $150 in manifestation crystals.

By the end of the year, she had saved nothing. The ritual made her feel like she was progressing while she did zero actual work.

Compare this to boring math:

Invest $200/month at 7% annual returns starting at age 23:

- Age 30: $21,748

- Age 40: $87,819

- Age 50: $263,073

- Age 65: $1,635,977

No visualization required. No lucky dates. No crystals. Just discipline, time, and compound interest.

Myth #2: Extreme Frugality Is Sustainable

The second myth is almost the opposite. It's the "no-buy challenge" movement — people going months without spending on anything non-essential.

Some people save $1,200 in three months. That sounds great. But here's what happens next: Burnout by week 8, 67% of the time. Rebound spending that wipes out gains, 72% of the time.

Chelsea tried a no-spend challenge. Three months of discipline. Saved $1,200. Then month four hit, and she psychologically crashed. She overspent on a shopping spree ($2,000), erasing gains and adding $800 in debt.

Sustainable approach: Save 20-25% of income consistently. Budget explicitly for joy spending ($50-100/month for things you enjoy).

People practicing this save $550-700/month consistently. They don't crash. They don't shame spiral. Over five years, that's $33,000-42,000 in consistent wealth-building — far more than the person who saves $1,200 once and then spends it.

Myth #3: Uncredentialed Finfluencers Are Financial Advisors

This is where I get serious about risk.

Only 20% of finfluencer investment content includes any disclosure. That means 80% of investment advice on TikTok comes with no indication of credentials, conflicts of interest, or regulatory compliance.

Meanwhile, a CFP® (Certified Financial Planner) requires:

- 6,000 hours of documented planning experience

- Passing a 10-hour comprehensive exam

- Ongoing education requirements

- Fiduciary duty (legally required to act in your best interests)

- Regulatory oversight

A "finfluencer" requires a TikTok account and followers. These are not equivalent.

Zara, 22, followed a finfluencer with 4.5 million followers who promoted "EZ Coin," calling it "the next Bitcoin." She invested her $3,000 emergency fund. Three weeks later, the coin lost 65% of value. She discovered the creator had been paid to promote it—undisclosed.

This happens at scale. The FTC estimates cryptocurrency pump-and-dump schemes orchestrated via finfluencers steal millions annually, primarily from young women.

Red flags for sketchy influencers:

- No credential disclosure

- Promises of quick wealth or "passive income"

- Heavy lifestyle flexing (designer bags, luxury cars)

- No mention of risk

- Pressure to act immediately ("limited time opportunity")

Green flags for credible voices:

- Discloses credentials (CFP®, CFA®) or clearly states they don't have them

- Lists potential conflicts of interest

- Cites sources and data

- Discusses downsides and risks

- Emphasizes that advice should be personalized

- Avoids extreme guarantees

The growth in Gen Z women's investing is real and powerful. But it needs to be paired with media literacy and a healthy skepticism of unvetted advice.

The Compounding Women's Advantage: Why Women Actually Outperform

Now here's the flip side that most articles miss.

Women investors don't underperform. They outperform.

Fidelity studied 5.2 million investor accounts over ten years (2011-2020). Their finding? Women investors beat men by 40 basis points annually. That's 0.4% every year — which compounds into enormous differences over decades.

Warwick Business School's research was even stronger: Women outperform by 1.8% annually on a risk-adjusted basis. Same risk, higher returns.

Why? Women buy and hold. Men trade.

Men engage in more frequent trading, which triggers:

- More transaction fees (draining returns)

- More capital gains taxes (draining returns)

- Emotional decisions during market volatility (locking in losses)

Women take a buy-and-hold approach to diversified index funds. They're less likely to panic during crashes. They're more likely to increase contributions during downturns.

This is the inverse of what most people assume. The media narrative is that women are too scared to invest. But the data says: women are perfectly calibrated for long-term wealth building.

The Math of Discipline vs. Trading

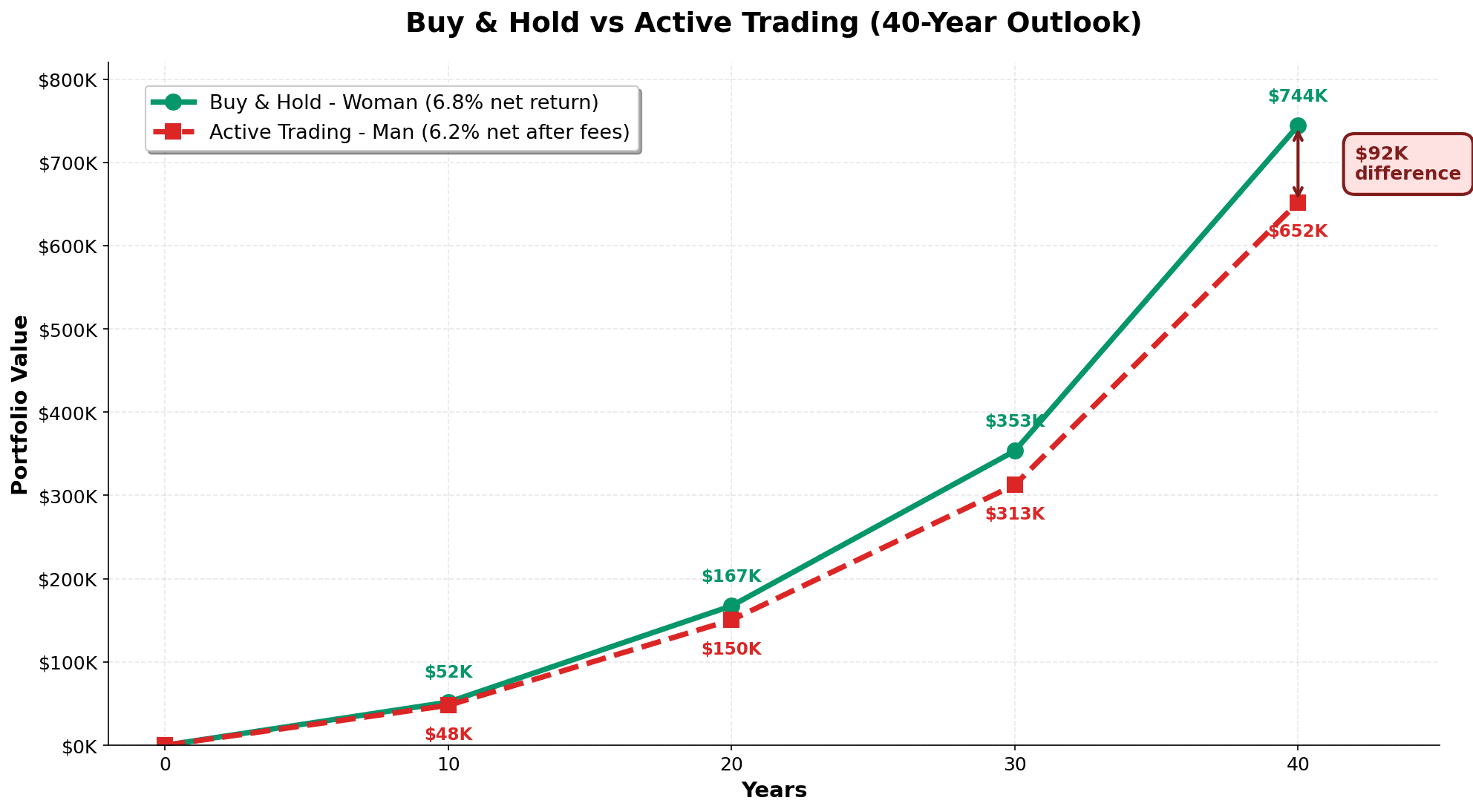

Two investors, both 25 years old. Both invest $300/month for 40 years.

Portfolio A (Buy & Hold Woman):

- Invests in 80/20 stock/bond portfolio

- Rebalances once per year

- Ignores market noise

- Average annual return (after fees): 6.8%

- Final balance at 65: $744,000

Portfolio B (Active Trader Man):

- Buys and sells frequently (6x per year average)

- Pays 1.5% in trading commissions annually

- Sells during downturns (realizes losses)

- Average annual return (after all costs): 6.2%

- Final balance at 65: $652,000

The "scared" woman who just holds ends up with $92,000 more than the "bold" trader who's constantly trying to optimize.

This is compounding at work. Small annual differences become huge lifetime differences.

Your 5-Step Investing Roadmap: From Zero Confidence to $500K Portfolio

Okay, you're convinced. You want to build $500K+. Here's the step-by-step framework.

No complexity. No stock picking. No mystery.

Step 1: Choose Your Account Type (Week 1)

This is the only decision that actually matters. Different accounts have different tax advantages.

If you're a W-2 employee:

- Start with your employer 401(k) — especially if there's an employer match (free money)

- Contribute enough to capture the full match

- Open a Roth IRA separately for additional tax-free growth

If you're self-employed:

- Open a Solo 401(k) — allows up to $72,000 annual contributions (2026 limit)

- This beats a SEP-IRA because you have more control and flexibility

If you earn high income and have a high-deductible health plan:

- Max out your HSA first — triple tax advantage (deductible, grows tax-free, withdrawals tax-free for medical)

- This beats a 401(k) for tax efficiency

If none of the above fit:

- Open a Roth IRA ($7,500/year limit in 2026)

- Tax-free growth is powerful when you have decades to invest

No decision paralysis here. Pick whichever bucket applies to you. That's it.

Step 2: Open Your Account (Week 1)

Go to Fidelity, Vanguard, or Schwab. Set up an account. Takes 15 minutes online.

No minimum balance required. No special credentials needed. No advisor necessary.

Open the account. Fund it with whatever you can afford—$50, $100, $500. Doesn't matter.

Step 3: Buy One Index Fund (Week 2)

Here's where simplicity wins.

Pick ONE of these:

- VTSAX (Vanguard Total Stock Market Index) — owns every major US company

- VBTLX (Vanguard Total Bond Market Index) — owns every major US bond

- Target-date fund (Vanguard 2050, 2055, 2060) — automatically balances as you age

That's it. You don't need to research 50 stocks. You don't need to pick between growth and value. You don't need to time the market.

One index fund. Set it and forget it.

Why these?

- Expense ratio: 0.03% (among the lowest possible)

- Diversified across entire market

- No stock-picking required

- Historical average return: 7-8.5%

Step 4: Automate Your Contributions (Week 3)

This is non-negotiable.

Set up an automatic transfer from your paycheck or bank account to your investment account. Every month. Same day. Same amount.

Start with whatever feels sustainable:

- Conservative: $50/month

- Moderate: $100/month

- Aggressive: $200/month

Don't overthink this. You can increase it later. The goal is to start today, not to be perfect.

Step 5: Track Progress Using Net Worth (Monthly)

Here's the psychological part.

Every month, log your investment balance in MFFT's net worth tracker. See the number grow. Celebrate it.

This serves two purposes:

- Reinforces the habit — visual progress is motivating

- Tracks compound growth — you'll start to see the exponential curve

After six months, you'll have concrete proof that this works. After a year, you'll see real momentum. After five years, you'll be shocked at the growth.

The Math Applied to Your Life

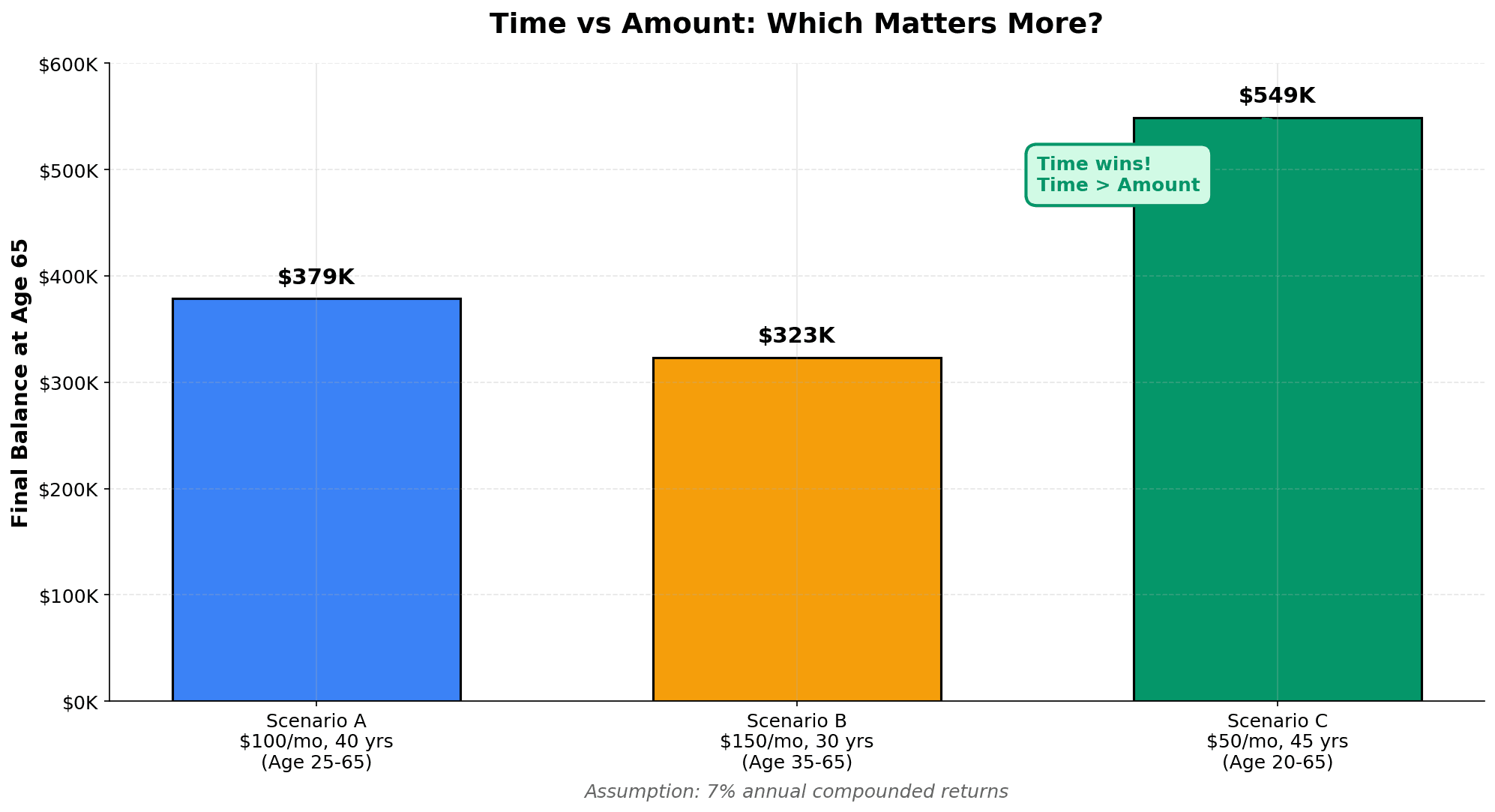

Scenario 1: $100/month for 40 years at 7% annual returns

- Starting age: 25

- Monthly investment: $100

- Total invested: $48,000

- Final balance at 65: $378,600

Scenario 2: $150/month for 30 years at 7% annual returns

- Starting age: 35

- Monthly investment: $150

- Total invested: $54,000

- Final balance at 65: $323,300

Scenario 3: $50/month for 45 years at 7% annual returns

- Starting age: 20

- Monthly investment: $50

- Total invested: $27,000

- Final balance at 65: $548,700

Notice: Starting five years earlier, even with half the monthly investment, beats starting late with more money. Time is the most powerful variable.

Choosing Your First Investment Vehicle: HSA vs 401(k) vs Brokerage Account

You've opened an account. Now the question: which account type is actually best for your situation?

There's no single answer. It depends on your employment status and timeline.

The Decision Tree

Do you have an employer 401(k) match?

- YES → Contribute enough to get the full match first. That's immediate 50-100% return on your money.

- NO → Skip to next question.

Are you self-employed or own a business?

- YES → Solo 401(k) (up to $72K/year) or SEP-IRA (up to $72K/year). Solo 401(k) gives you more flexibility.

- NO → Skip to next question.

Do you have a high-deductible health insurance plan?

- YES → Max out your HSA (stealth retirement account). Triple tax advantage: deductible contributions, tax-free growth, tax-free withdrawals for medical expenses. This beats a 401(k) for efficiency.

- NO → Skip to next question.

Do you want flexibility and tax-free withdrawals later?

- YES → Roth IRA. $7,500/year limit, but tax-free growth forever. Perfect for younger women with lower current income.

- NO → Traditional IRA or taxable brokerage account.

Account Comparison Table

| Account | 2026 Limit | Tax Advantage | Best For | Withdrawal Rules |

|---|---|---|---|---|

| Roth IRA | $7,500 | Tax-free growth & withdrawals | Young women, variable income | Tax-free after 59.5, no RMD |

| Traditional IRA | $7,500 | Tax deduction now | High earners | Taxed at withdrawal, RMD at 73 |

| 401(k) | $24,500 + $8K catch-up (50+) | Employer match + pre-tax | W-2 employees | Taxed at withdrawal, RMD at 73 |

| Solo 401(k) | $72,000 total | Large contributions possible | Self-employed | Taxed at withdrawal, RMD at 73 |

| HSA | $4,400 individual / $8,750 family | Triple tax advantage | HDHP users | Tax-free for medical, taxed otherwise |

For most women reading this: Start with a Roth IRA if you're self-employed or don't have a 401(k). Max out your employer 401(k) match if you have one. Consider the HSA if you qualify.

Building Your Personal Investing Circle: Community Over Isolation

Here's something the research is clear on: women cite "isolation" and "lack of accountability partners" as major barriers to investing.

You don't have to do this alone.

Women are organizing locally and online. There are Reddit communities (r/investing, r/personalfinance with active women-only threads). There are groups like Invest for Better, Women With Capital, and local Women Investors Clubs.

Why does community matter?

Accountability changes behavior. People who announce goals publicly are 65% more likely to achieve them. When you're part of a group, you're not just trying to build wealth for yourself — you're committing to people who are watching.

Women's wealth is accelerating. Women now hold 34% of U.S. investable assets ($18 trillion). By 2030, that projection grows to 38% ($34 trillion). The investing conversation among women is no longer niche. It's mainstream.

What you could do:

- Join a local Women Investors Circle (meetup.com, reddit, Facebook groups)

- Start an informal accountability group (3-4 women, monthly coffee, share progress)

- Find an online community and participate (Reddit threads, Discord, monthly check-ins)

- Work with a female financial advisor if you want professional guidance

The point: you don't have to figure this out in isolation. Thousands of women are doing exactly what you want to do.

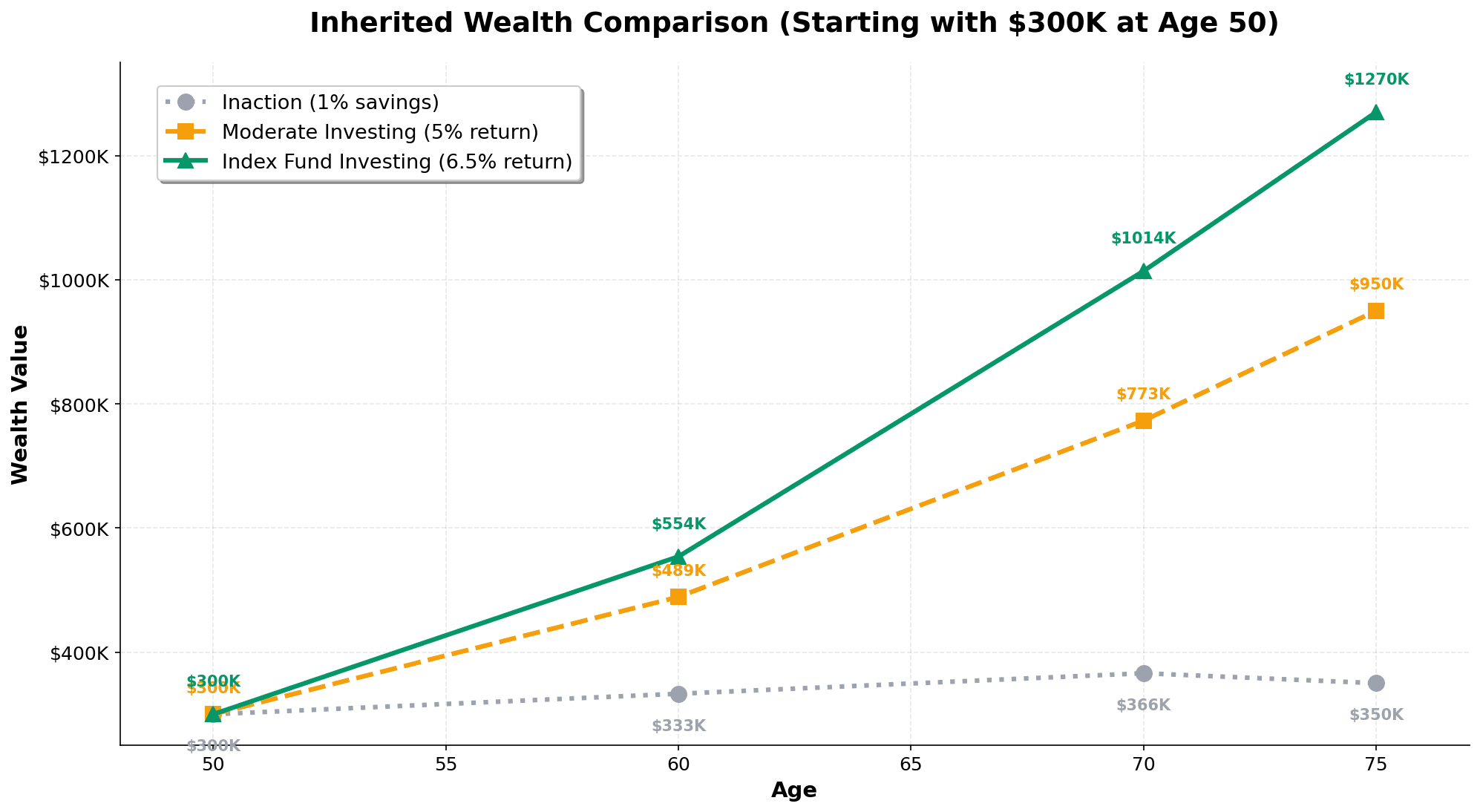

The Inheritance Advantage: Women's Wealth Transfer Opportunity in 2026

Here's a stat that's often missed: $124 trillion will transfer to the next generation through 2048. Women will inherit 70% of it.

That's $87 trillion flowing to women. Not men. Women.

But here's the problem: 84% of women feel overwhelmed or confused managing inherited wealth.

Michelle, 48, inherited $300,000 from her parents. She felt guilty about the money—like she didn't "deserve" it. She let it sit in a savings account earning 1% for three years while she figured out what to do.

Three years at 1% = $9,000 in interest. Meanwhile, if she'd invested it: three years at 7% = $62,500 in compound growth. She left $53,500 on the table through inaction.

The fix: Have a plan before you inherit.

Read our complete inheritance guide for step-by-step decisions. But the quick version:

- Don't invest immediately — sit with the windfall for 30 days

- Allocate: 20-25% emergency fund (high-yield savings), 75-80% invested

- Invest in the same index funds we discussed above — VTSAX for stocks, VBTLX for bonds

- Rebalance annually

- Let it compound for decades

The math: $300,000 inherited at age 50, invested at 6% annual return, becomes $967,000 by age 75. Inheritance without a plan is wealth slipping through your fingers.

Closing the Gap: Your Wealth-Building Timeline

The gap between women and men investors isn't genetic. It's not about math ability or intelligence. It's about access, encouragement, and breaking through psychological barriers.

Here's what I want you to understand: you have an advantage if you start now.

Women investors outperform. Women hold their positions through volatility. Women are building wealth faster per dollar of risk taken.

The compound math is relentless. $100/month starting today at age 25 becomes $378,600 by 65. That's $500,000+ if you increase contributions with raises and side hustle income.

But $100/month starting at age 35? It becomes $185,000 by 65. You lose $193,600 by waiting ten years.

Time is your rarest resource. Compound interest is your biggest wealth-building tool.

The steps are simple:

- Pick an account type (Roth IRA, 401k, HSA)

- Open it this week

- Buy one index fund

- Automate $50-150/month

- Track your net worth monthly

- Ignore the noise and let it compound for 30+ years

You don't need to feel confident. You don't need to understand every detail. You just need to start.

The women who reach financial independence in 2035, 2045, 2055 won't be the ones who had the most money. They'll be the ones who started earliest and stayed disciplined longest.

That could be you.

Start tracking your net worth with MFFT today. Log your first investment. See the growth compound. And in five years, you'll look back and be shocked at what compound interest built.

The $500K gap? You're going to close it. And then you're going to build wealth that compounds for the rest of your life.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.

Master Your Money

Master Your MoneyAI Scams Stole $21 Billion: How to Protect Yourself in 2026

AI scams hit a record $20.9B and could reach $40B by 2027. Scammers clone a loved one's voice from 3 seconds of audio. Here's the calm, free, afternoon-long defense playbook to protect your money in 2026.

Master Your Money

Master Your MoneyPrediction Markets: Why 69% of Polymarket Users Lose

69% of Polymarket users lose money and the top 1% take 76.5% of profits. The math, why Gen Z is targeted, and a 30-day reset plan.