Minimalism + FIRE: Cut 5-10 Years Off Your Timeline

You're not broke. You're just living like you're richer than you are.

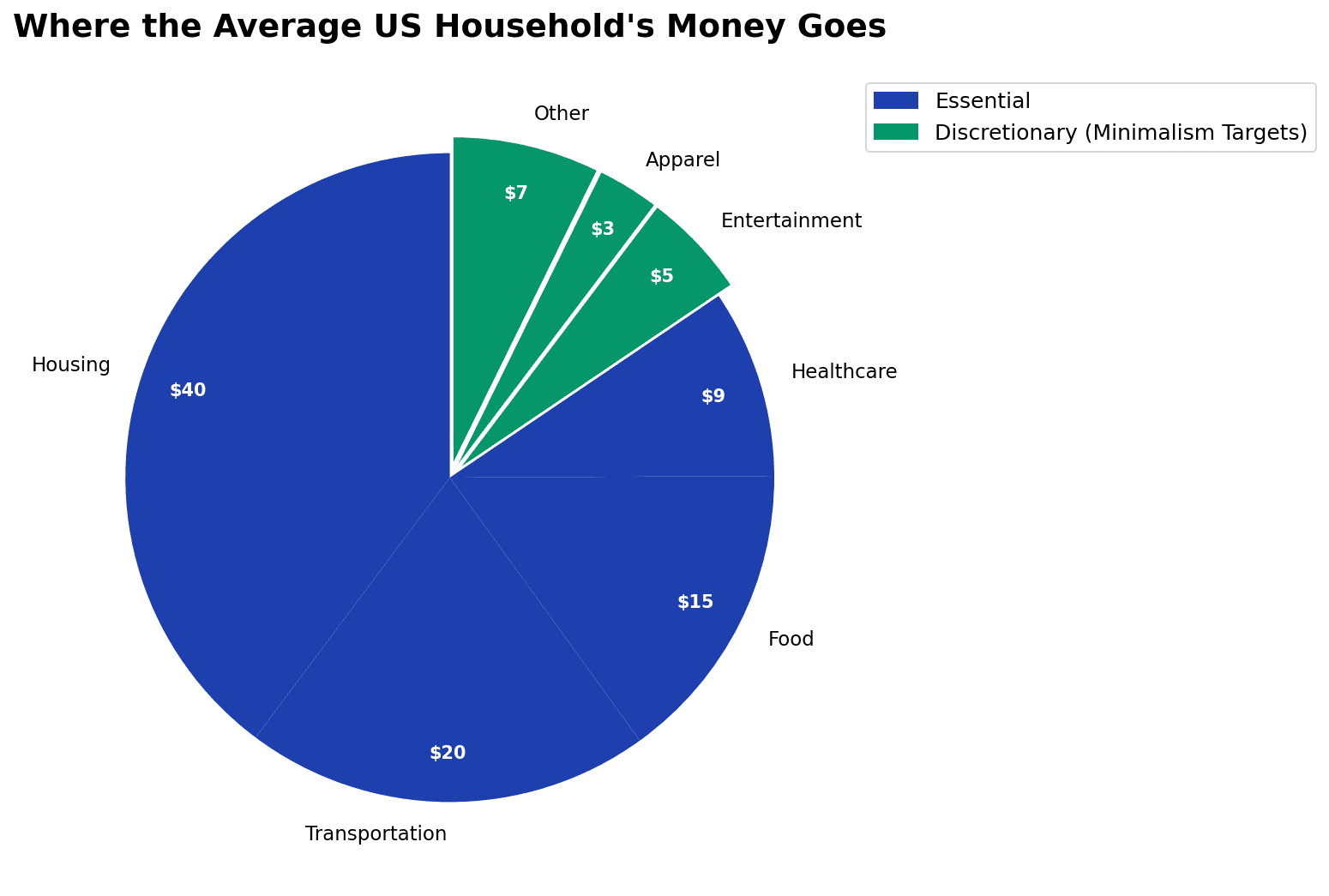

The average American household spends $78,535 a year. Not on shelter, food, or survival. On everything — including subscriptions they've forgotten about, clothes they never wear, and habits they stopped enjoying months ago.

Here's what nobody tells you: minimalism isn't about deprivation. It's about resource allocation.

And when you get it right, it's one of the fastest wealth-building strategies available. Cut your discretionary spending by just 20-30%, and you don't just save money — you compress your entire FIRE timeline by 5-10 years. That's not a side effect. That's the whole point.

Let me show you the math.

Why Minimalism Is the Secret Wealth Hack Nobody Talks About

When people hear "minimalism," they think Marie Kondo. They picture empty rooms. They imagine deprivation.

But here's what actually happens: intentional living (which is what minimalism really is) frees up your mental bandwidth, reduces decision fatigue, and redirects massive amounts of money toward wealth-building.

The average American's problem isn't low income. It's lifestyle bloat.

Let me break down the wasted spending patterns:

Subscriptions: The average American spends $219/month on subscriptions but estimates only $86/month — a 2.5x gap. And buried in that? They're paying $32/month for services they've completely forgotten about. That's $384/year in pure waste.

Impulse purchases: 48% of Americans have charged their credit cards after forgetting to cancel free trials. 72% admit keeping subscriptions "just in case" despite never using them. That's decision fatigue talking — and it's costing them thousands.

Discretionary spending: The average U.S. household budget allocates roughly $250-$350/month to entertainment, another $150+ for apparel, and $600-$900 to dining out. These aren't survival costs. They're choices.

Here's the thing: When you audit your actual spending, you typically find 20-30% that you don't miss once it's gone. Not because you're cutting essentials. Because you're eliminating choices you stopped enjoying anyway.

And when you redirect that 20-30% into investments instead of impulse purchases?

That's when wealth acceleration begins.

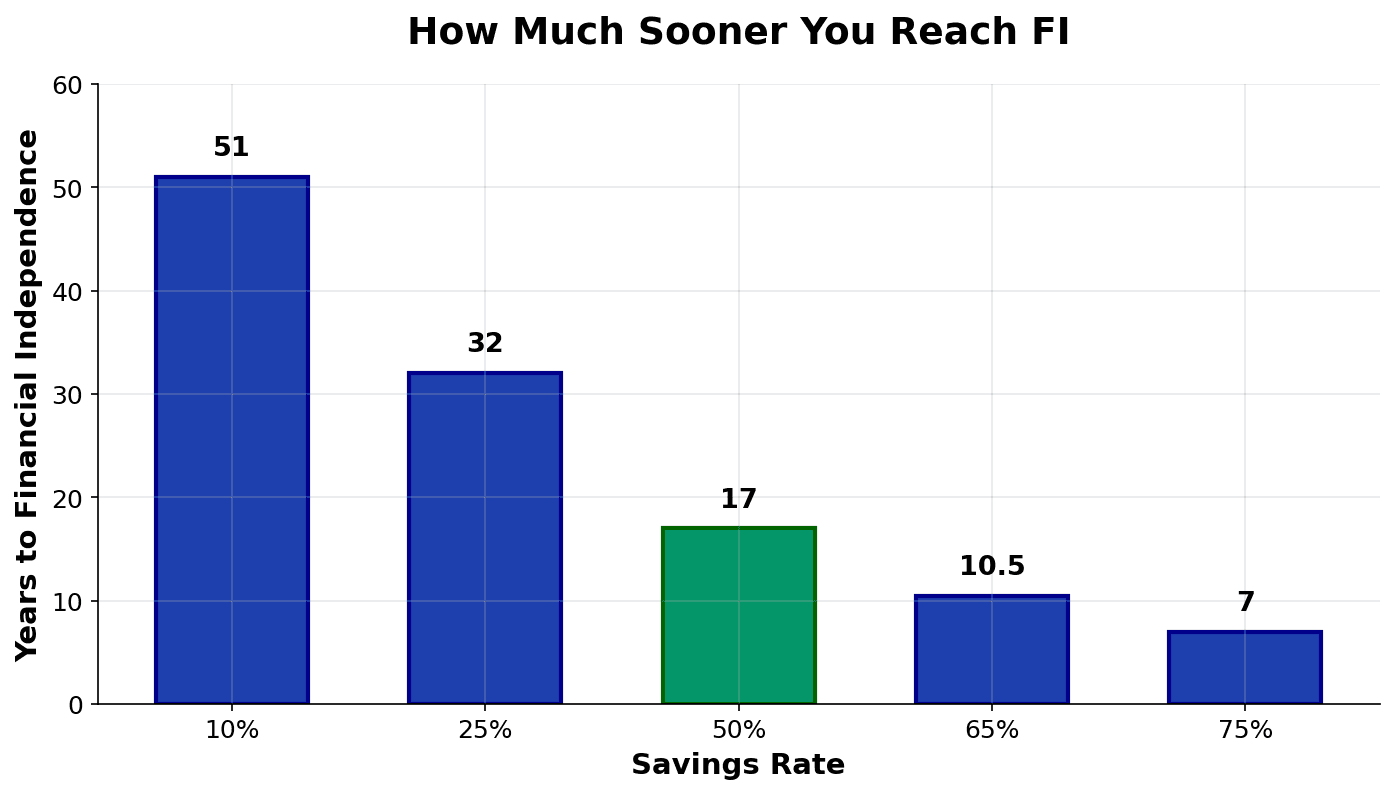

The Math: How Cutting 20% of Spending Accelerates FIRE by 5-10 Years

Let's get specific. I'm going to walk you through three real scenarios showing what happens when someone shifts from consumption to intentional living.

Sarah's Story: 20-Year Timeline Compression

Before Minimalism (Age 27):

- Gross income: $75,000

- Monthly expenses: $4,500

- Monthly savings: $400 (8.9% savings rate)

- Years to FIRE: 52 years (age 79)

Here's where her money went:

- Housing: $1,200

- Transportation: $400

- Food & dining: $600

- Subscriptions: $180 (Netflix, Spotify, gym, Adobe, Audible)

- Clothing & impulse: $400

- Other: $720

After 90-Day Minimalism Challenge:

- Same income, different choices

- Subscriptions: $45 (canceled Adobe, gym, Audible — kept Netflix + music)

- Clothing: $100 (thrift-only, quality over quantity)

- Food & dining: $450 (meal prep, eating out 1x/week instead of 4x)

- Transportation: $350 (carpooled more)

- Other: $500

- Monthly savings: $855 (19% savings rate) — $455/month recovered

What does that $455/month actually mean?

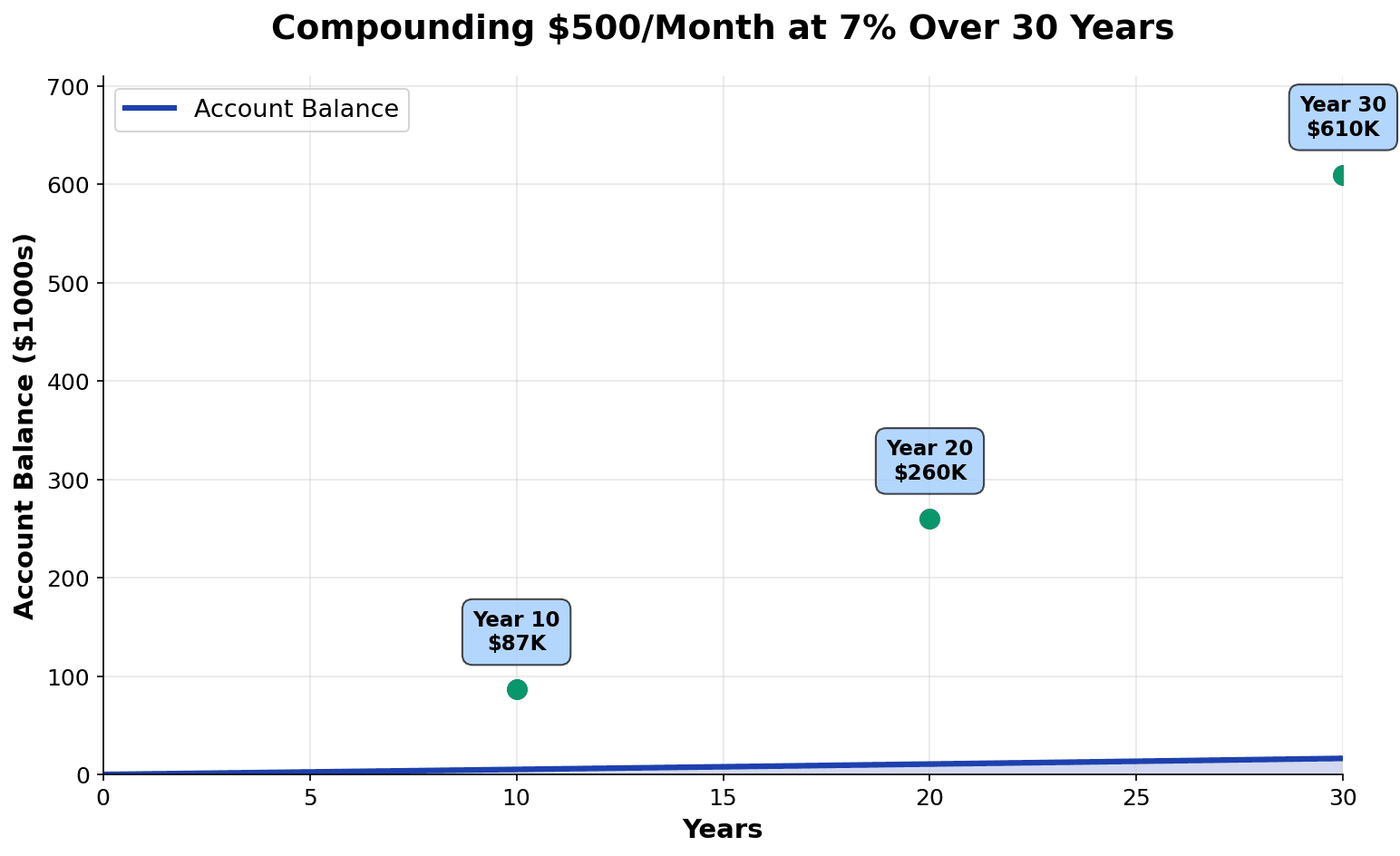

Invested at 7% annual returns over 26 years (to age 53): $585,000 additional wealth.

And Sarah's FIRE timeline? 32 years instead of 52. She reaches financial independence at age 59 — 20 years earlier.

She didn't change her income. She didn't get lucky. She just stopped bleeding money to choices she'd already stopped valuing.

Jake's Story: Aggressive Minimalism

Before Minimalism (Age 26):

- Gross income: $130,000 (software engineer)

- Monthly take-home: $8,000

- Monthly savings: $1,550 (19.4% savings rate)

- Years to FIRE: 28 years (age 54)

Breaking down his pre-minimalism budget:

- Housing: $1,800

- Transportation: $800 (car payment + insurance)

- Food & dining: $900 (lots of delivery)

- Tech subscriptions + gaming: $250

- Clothing: $300

- Entertainment: $600

- Miscellaneous: $800

After Lifestyle Audit:

- Housing: $1,800 (unchanged)

- Transportation: $400 (sold car, public transit)

- Food & dining: $500 (cooked at home, meal prep)

- Tech subscriptions: $60 (eliminated gaming, kept essentials)

- Clothing: $150 (3-4 quality basics annually)

- Entertainment: $400 (free activities + one planned trip/year)

- Miscellaneous: $400

- Monthly savings: $3,290 (41.1% savings rate) — $1,740/month recovered

The result? Jake reaches financial independence at age 40 instead of 54. A 14-year reduction.

That additional $1,740/month ($20,880/year) invested at 7% over 14 years = $503,000 additional wealth by age 40. If he keeps working until 54 with his original savings rate, he'd have $1.4M. With intentional living, he hits $1.4M by age 40 and compounds for 14 more years, reaching $3.8M+.

He didn't get a raise. He didn't change careers. He just stopped paying for convenience that was costing him a decade of his life.

Michelle's Story: The Reality Check

Not everyone can cut 50% of spending. Michelle is a 45-year-old single parent earning $55,000/year with childcare costs.

Before "Minimalism":

- Monthly take-home: $3,200

- Housing: $1,200

- Childcare: $600

- Transportation: $350

- Food & essentials: $700

- Insurance: $200

- Miscellaneous: $150

- Monthly savings: $0

Michelle isn't choosing excess. She's surviving.

After Intentional Spending:

- Transportation: $300 (minor reduction)

- Food: $600 (bulk buying, meal planning)

- Utilities: $200

- Monthly savings: $200/month — recovers $2,400/year

This matters. At 7% returns over 20 years, $200/month becomes $96,000 — real emergency security for a single parent. She won't reach early FIRE, but she stops being one emergency away from financial crisis.

The point? Minimalism works at every income level. But it works best when there's actual fat to cut.

Quality Over Quantity: The Quiet Luxury Mindset That Builds Wealth

Here's what catches most people off guard: minimalism isn't about buying nothing. It's about buying better.

The math on this is brutal once you see it.

A durable $150 dress worn 100 times costs $1.50 per wear. A $25 fast-fashion dress worn 10 times costs $2.50 per wear.

The quality item is literally cheaper. This principle is what makes intentional consumption such a powerful wealth-building tool.

But most people buy 15 cheap pieces instead of 3 quality pieces. Why? Decision fatigue. Impulse. The dopamine hit of shopping. Social pressure.

Gen Z is already figured this out. 78% of consumers now prioritize sustainability in purchases. 62% of Gen Z prefer sustainable brands, even paying premium prices. Resale markets are growing 21x faster than traditional retail.

This is minimalism + values-alignment. You're not depriving yourself. You're upgrading to buying things you actually love.

The cost-per-wear principle changes everything:

Instead of 12 pieces you wear 3 times each (36 total wears, $300 spent, $8.33 per wear), buy 4 pieces you rotate and love (60+ total wears, $350 spent, $5.83 per wear).

Better stuff. Fewer purchases. Less decision fatigue. Lower cost per wear. And here's the kicker — higher resale value. A $150 quality piece sells on Vestiaire for $80. A $25 fast-fashion piece? It's worth $3.

When you factor in resale, quality pieces cost even less.

This logic extends everywhere:

- Quality kitchen tools last 15 years, cheap ones last 2

- A $1,200 espresso machine saves $5/day on coffee (pays for itself in 240 days)

- Durable furniture costs more upfront but reshuffles less frequently

The psychological benefit? Reduced decision fatigue. When you own fewer, better things, you stop shopping compulsively. Your brain isn't being hammered by 200 micro-decisions about what to wear, what to use, what to buy next.

You save money. You save mental energy. You invest the difference.

Breaking the Psychology: From Impulse Spending to Intentional Investing

Here's something behavioral economists have proven: decision fatigue is your wealth killer.

By the end of a workday, your brain has made thousands of micro-decisions. Your prefrontal cortex (the rational part) is exhausted. Your amygdala (the emotional part) takes over.

This is why you buy things at the register. Why you end-of-day online shopping happens. Why you're not thinking clearly about what you actually need.

The average American makes 35,000 conscious decisions daily. And each one depletes your mental energy. The later in the day, the worse your decisions.

Minimalism eliminates 90% of those decisions. Instead of deciding what to wear from 40 pieces, you choose from 4. Instead of deciding what to eat from 15 impulse options, you meal-prep 3 base recipes.

This is why intentional living accelerates FIRE so dramatically. You're not relying on willpower (which depletes). You're architecting your environment so the right choice is the easy choice.

The Psychology: Decision Fatigue Prevention

Research shows the 24-hour rule is devastatingly effective. Waiting a day separates emotion from rationality. The urge to buy typically fades completely.

Similarly, the 30/30 rule: anything under $30, wait 30 hours. Anything over $100, wait 30 days.

Why does this work? Because impulse buying isn't rational. It's dopamine-seeking. And dopamine fades fast. Most impulse purchases are regretted within 48 hours.

But most people don't wait 24 hours. They buy, experience regret, and rationalize the purchase to reduce cognitive dissonance.

By building in a waiting period, you break the cycle.

The Real Weekly Spending Audit

Here's how to identify where your money is actually bleeding:

Spend one week tracking literally every purchase. Cash, card, app, coffee, everything.

Then categorize:

- Guilt Purchases (you felt bad after): Impulsive buys, ordering delivery when you have food at home, duplicate subscriptions

- Obligation Purchases (social pressure): Group dinners you couldn't skip, gifts you felt obligated to buy

- Convenience Purchases (paid to avoid friction): Delivery fees, restaurant meals, premium services

- Values-Aligned Purchases (you felt good): Books, experiences with friends, quality items you'll use for years

Your answer is obvious. You're not going to eliminate values-aligned purchases. You're going to audit spending in the guilt and convenience categories and redirect that cash.

That's where your $455-$1,740/month lives.

The 90-Day Minimalism FIRE Challenge: A Step-by-Step Playbook

This is the part that differentiates intention from action.

Phase 1: Audit & Awareness (Days 1-30)

Week 1-2: Subscription Audit

List every recurring charge. Netflix, Spotify, gym, Adobe, Audible, WeWork, cloud storage, news subscriptions — everything.

For each, ask: "Did I actually use this in the last month?"

If the answer is no or "maybe," cancel today. Seriously. Not next week. Today.

Typical recovery: $80-$150/month. (The average American who audits their subscriptions recovers 40-75% of their subscription budget.)

Week 3-4: Spending Audit

Track every purchase for 7 days. Use your bank app, a notebook, whatever. Just be honest.

Then identify your top 3 guilt categories. Where does the emotional spending happen?

For most people: eating out, shopping, entertainment subscriptions, impulse online orders.

Phase 1 Goals:

- Identify $200-$400/month in recoverable spending

- Establish baseline for comparison

- Implement the 30/30 and 24-hour rule

Phase 2: Replace & Redirect (Days 31-60)

Week 5-6: Quality-Over-Quantity Implementation

Pick 2-3 categories where you impulse-buy most. Clothing, tech, home goods, whatever.

New rule: Buy fewer, better items. And track cost-per-use.

Example:

- Old: 12 fast-fashion pieces, worn 2-3 times each, average $3/wear

- New: 3-4 quality basics, worn 30+ times each, average $1.50/wear

Expected savings: $100-$200/month from category consolidation, plus the mental clarity of decision reduction.

Week 7-8: Automate the Redirected Cash

Calculate your total recovered amount from Phase 1. Let's say it's $300.

On payday, automatically transfer $300 to your investment account.

Out of sight, out of mind. This is how you prevent lifestyle creep.

Phase 2 Goals:

- Replace 3-5 spending categories with intentional, quality alternatives

- Automate at least 50% of recovered spending into index funds

- Measure the psychological shift (journaling helps)

Phase 3: Sustain & Compound (Days 61-90)

Week 9-10: Values Check-In

Revisit: What spending still makes you feel guilty? What brings genuine joy?

This is Ramit Sethi's Conscious Spending philosophy in action. You're not budgeting through shame. You're spending intentionally on what matters and cutting ruthlessly on what doesn't.

Example: If you love books but hate gym memberships, cancel the gym. Buy 2-3 books/month guilt-free.

Week 11-12: Anti-Influence Habits

Unfollow influencers promoting consumption. Disable push notifications on shopping apps. Block algorithmic triggers (unsubscribe from retail emails).

Set phone "Do Not Disturb" during decision-fatigue hours (end of workday, late night).

Use the 24-hour rule strategically — don't buy anything over $50 without a full day of reflection.

Week 13: Measure & Lock In

Calculate total savings (monthly recurring + one-time recovered spending).

Project forward: If $400/month saved = $4,800/year, at 7% returns over 30 years = $660,000 additional wealth.

Set a 6-month recurring review (quarterly net-worth update). Then lock in your new baseline.

You've reduced decision fatigue, aligned spending with values, and put your future self years ahead.

Phase 3 Goals:

- Establish sustainable, values-aligned spending baseline

- Automate all recovered cash to FIRE investments

- Build anti-influence habits to prevent lifestyle creep

- Lock in timeline: "I'm on track to FI by age X instead of Y"

Connecting Minimalism to the Bigger FIRE Picture

Here's where this gets powerful: minimalism doesn't just save money. It accelerates your FIRE timeline exponentially.

Remember the FIRE math? Your FI number = 25 × your annual expenses.

If you spend $40,000/year, your FIRE number is $1,000,000.

But if you intentionally cut to $32,000/year (20% reduction via minimalism), your FIRE number drops to $800,000.

That's $200,000 less you need to accumulate.

At a 7% average return, how many years does that shorten your timeline?

Dramatically.

And that's just from the reduced FIRE number. Add in the extra $300-$500/month you're investing from redirected spending, and you're cutting years off from both sides:

- Your target is lower

- Your monthly contributions are higher

This is wealth acceleration in action.

The Common Myths That Keep People Stuck in Consumerism

Myth 1: "Minimalism means I'll feel deprived."

Real minimalism is intentional, not restrictive. You're not cutting things you love. You're eliminating things you've stopped enjoying but kept out of habit.

The difference: deprivation = cutting essentials. Intentionality = cutting waste.

Myth 2: "Minimalism is only for rich people."

Michelle's story disproves this. Minimalism works at every income level. It just looks different. For Michelle, it's not about luxury cuts. It's about survival efficiency. Even $200/month matters.

Myth 3: "I'm not minimalist enough."

Minimalism isn't binary. You don't need to own 100 items. You don't need to live in an empty room. You need to intentionally decide what stays and what goes.

Jake still enjoys coffee. Anna still buys clothes. Sarah still eats out. They're just intentional about it.

Myth 4: "Minimalism takes too long to implement."

The 90-day framework is 13 weeks. Week 1 is subscription cancellation. That alone recovers $80-$150/month. You're not reinventing your life. You're eliminating waste.

From Stuff to Sustainability: How Minimalism Aligns Values With Wealth

Here's something powerful: minimalism has become a values statement, not just a financial strategy.

78% of consumers now prioritize sustainability in purchasing decisions. 62% of Gen Z prefer sustainable brands, even paying premium prices. 91% of Gen Z will pay more for sustainable products.

This isn't nostalgia. It's the future of consumption.

And here's the beautiful part: sustainable consumption (fewer, better things) is identical to minimalist consumption. Buy quality. Buy less. Buy intentionally. Buy for durability.

The result? You reduce environmental guilt while reducing spending simultaneously.

This is the quiet luxury movement. It's not about showing off. It's about intentional choices that reflect your values.

When you stop buying for status and start buying for longevity, your spending naturally aligns with minimalism. And your wealth accelerates.

Your Minimalism Wealth Roadmap: Next Steps After 90 Days

After 90 days, you've built new habits. You've redirected thousands. You've locked in a new baseline.

Now what?

Step 1: Measure Your FIRE Progress

Take your baseline FIRE number from before minimalism. Calculate it again with your new expenses.

How many years did you just remove from your timeline? For Sarah, it was 20 years. For Jake, 14.

That's not theoretical. That's your actual life.

Step 2: Automate the Whole System

On payday, the recovered money automatically moves to investments. You never see it. Lifestyle creep can't touch it.

Step 3: Quarterly Reviews

Every 3 months, update your net worth. Watch the compound growth from minimalism decisions.

Seeing that growth reinforces the behavior. You're not budgeting for the sake of rules. You're building wealth in real-time.

Step 4: Protect Against Lifestyle Creep

Minimalism works until it doesn't — until a raise comes in and you spend 100% of it instead of redirecting half.

Protect against this: when income increases, automatically increase investments by 50% of the raise. Let lifestyle expand with the other 50%.

This is how wealth accelerates while life still improves.

The Real Power of Intentional Living

Minimalism as a wealth strategy isn't about suffering. It's about clarity.

You stop asking, "Should I buy this?" and start asking, "Does this align with who I want to be?"

When you flip that question, everything changes.

The $180/month subscription you forgot about? That's not about cutting subscriptions. That's about reclaiming attention and redirecting capital.

The impulse clothing purchases? Not deprivation. Resource allocation.

The dining out that became a habit? Intentionality, not restriction.

This is how to build wealth from zero — through discipline, yes, but discipline that's built on clarity, not willpower.

And when you get it right?

You don't just save money. You save time. You reduce decision fatigue. You align spending with values. And you compress your FIRE timeline by 5-10 years.

That's not just wealth acceleration. That's freedom acceleration.

Start Your 90 Days Today

You have two choices:

Choice 1: Keep living like you have more than you do. Spend 40 years working for money you'll forget about. Hope the system works out.

Choice 2: Spend 13 weeks auditing, replacing, and sustaining. Recover $300-$500/month. Compress your FIRE timeline by half a decade. Buy your freedom sooner.

The 90-day framework is ready. Week 1 is a subscription audit — takes 30 minutes and recovers $80-$150/month.

That's how you start.

And if you want to track your progress — your recovered spending, your redirected investments, your FIRE timeline compression — tools exist to make it visible. MFFT's Subscription Tracker, Budget Tracker, and Investment Tracker turn minimalism from an intention into a measurable system.

You don't need a philosophy. You need a framework. You have it.

Now choose: keep spending on things you've forgotten about, or redirect that money toward the freedom you actually want.

The math is simple. The timeline is compressed. The only barrier is starting.

So start.

Ready to see your minimalism impact on your FIRE timeline? Track your spending, automate your investments, and measure your wealth acceleration with MFFT. Start your 90-day challenge this week.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.

Master Your Money

Master Your MoneyAI Scams Stole $21 Billion: How to Protect Yourself in 2026

AI scams hit a record $20.9B and could reach $40B by 2027. Scammers clone a loved one's voice from 3 seconds of audio. Here's the calm, free, afternoon-long defense playbook to protect your money in 2026.

Master Your Money

Master Your MoneyPrediction Markets: Why 69% of Polymarket Users Lose

69% of Polymarket users lose money and the top 1% take 76.5% of profits. The math, why Gen Z is targeted, and a 30-day reset plan.