Budgeting When Essentials Cost 30% More: A Triage Plan

New to budgeting under financial pressure?

If affordability is part of a bigger financial picture, start here:

- How to Start a Budget — the foundation that makes any budget possible

- How to Start a Budget — the first step out of the squeeze

- Emergency Fund Crisis 2026 — understanding why the squeeze happened

Here's what you already know: everything costs more, and your paycheck — even after the raises — doesn't feel like it kept up.

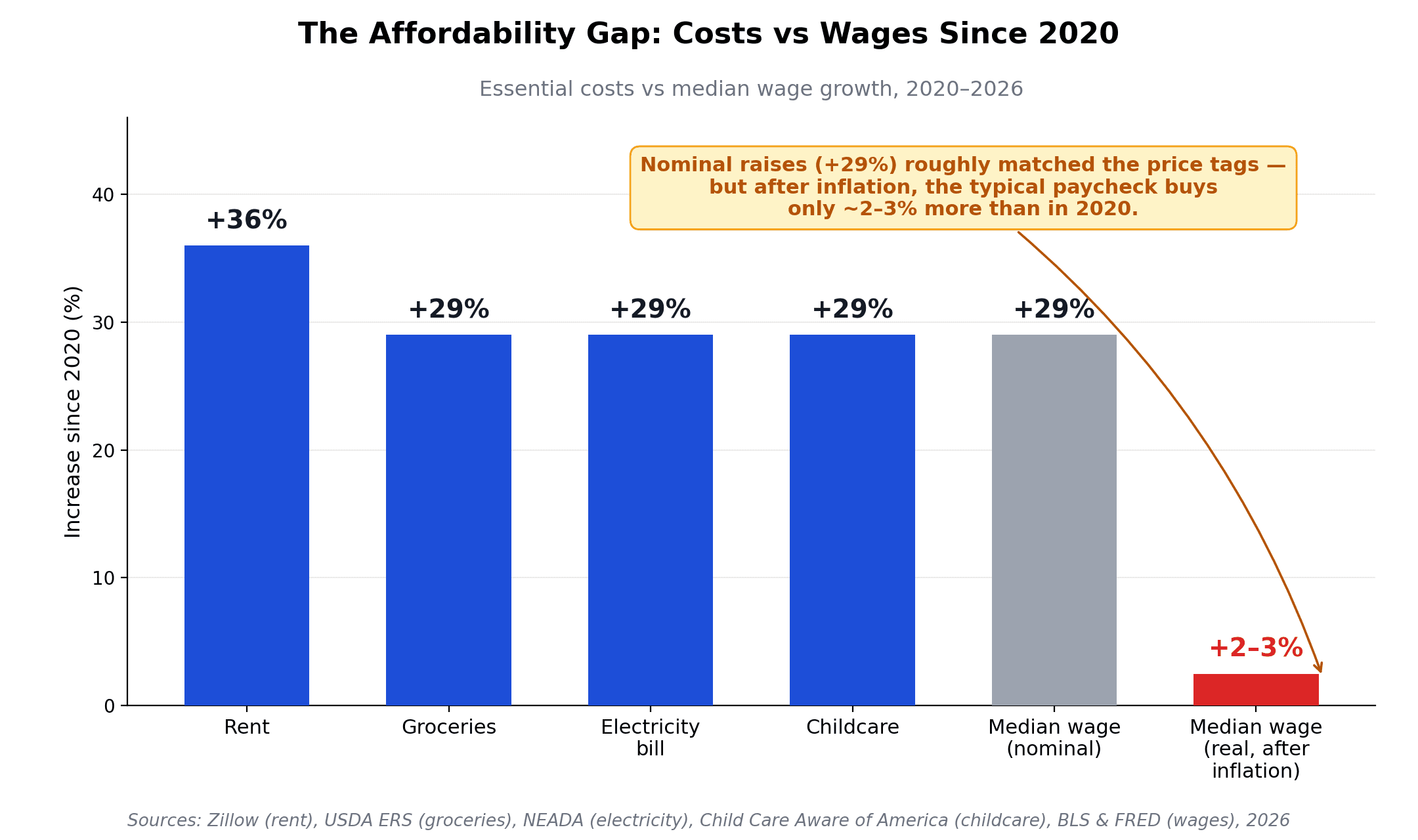

Rent +36% since 2020. Groceries +29%. The average electricity bill +29%. Childcare +29%. Median wages? Up about 29% on paper — but after inflation, the typical paycheck buys only about 2–3% more than it did in 2020. Six years of "growth" that nets out to almost nothing, while every must-pay category reset permanently higher.

And the averages hide who's getting crushed. The lower your income, the larger the share of it that goes to must-pay categories — housing, food, utilities, childcare — and the less room you have to absorb a $380 rent increase or a $170 grocery jump. Roughly half of all workers saw less than the median raise, and a raise that arrives in 2026 doesn't refund the 2021–2023 price surge you already lived through.

This article isn't about aspirational wealth building. It's honest advice for surviving a structural crisis and building discipline that compounds even when you're starting from nearly nothing.

The Numbers That Explain the Squeeze

Let me start with the data, because data cuts through the noise.

Since 2020, essential costs have surged — and most of them outran the paycheck:

| Essential | Increase Since 2020 | Source |

|---|---|---|

| Rent (typical US asking rent) | +36% | Zillow data |

| Groceries (food-at-home CPI) | +~29% | USDA ERS |

| Average monthly electricity bill | +29% ($121 → $156) | NEADA |

| Childcare (avg. annual price, 2020–2024) | +29% | Child Care Aware of America |

| Median weekly wage (nominal) | +29% ($957 → $1,235) | BLS |

| Median weekly wage (inflation-adjusted) | +~2–3% | FRED |

That's the core math, and it's worth being precise about it: nominal wages did rise — about 29% at the median — but inflation ate nearly all of it, and the must-pay categories (rent, childcare, utilities) rose faster than the overall index. A family spending $2,500/month on essentials in 2020 now spends roughly $3,200. If their pay didn't keep pace with the median — and by definition, about half of workers' pay didn't — that gap comes straight out of survival money, not lifestyle.

Now look at who's getting hit hardest. USDA's household food security data shows the crisis is concentrated:

- Households with children: 18.4% were food insecure in 2024 — 6.7 million households

- Single-parent households and Black and Hispanic households experience food insecurity at roughly 1.5–2.5 times the national rate, per USDA's demographic breakdowns

- 7.3 million children lived in households where both children and adults were food insecure

This isn't abstract. 13.7% of American households were food-insecure in 2024 — they couldn't reliably afford enough food. That's 18.3 million households, 47.9 million people.

And here's the thing that gets me: 59% of Americans could not cover a $1,000 emergency from savings, per Bankrate's 2026 Emergency Savings Report. So the moment a transmission fails or a medical bill arrives, the budget doesn't just squeeze — it breaks.

The same report found 54% of US adults say inflation is causing them to save less for emergencies. This isn't about coffee-shop lattes or streaming habits. This is about survival.

When Budget Math Breaks: Three Families

Let me show you what this looks like in actual monthly budgets. These are composite examples, and they sit deliberately on the losing side of the wage statistics: the median wage rose 29%, but medians are made of winners and losers — job-switchers and in-demand fields captured most of the growth, while plenty of workers in retail, admin, and care roles saw their pay barely move. That's exactly where the affordability crisis bites.

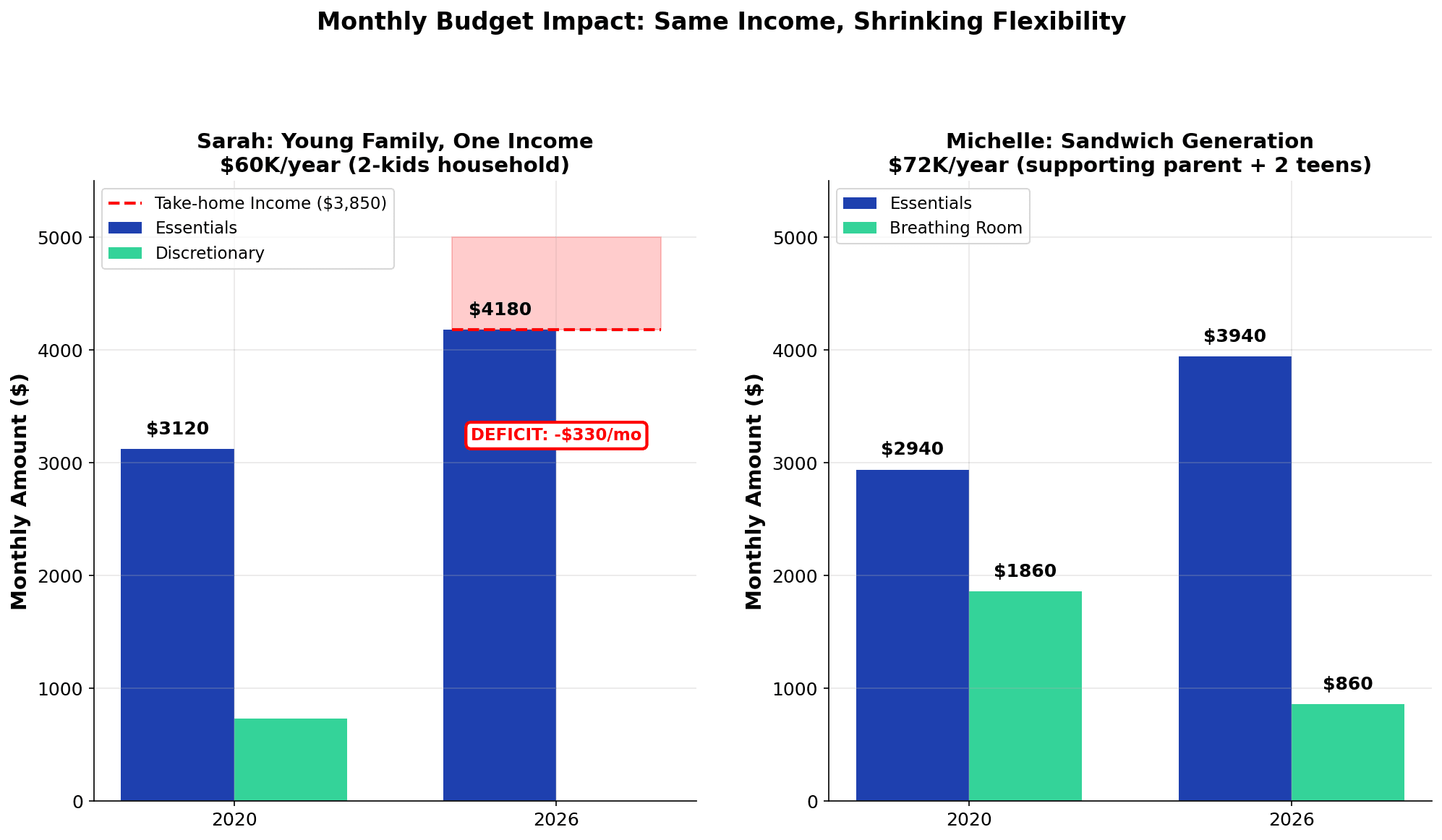

Sarah: Young Family, One Income

She earns $60,000/year (takes home $3,850/month). She's married, but her spouse stays home because childcare costs are so high that one income completely disappears into daycare. They've done the math: paying for childcare doesn't make financial sense.

| Item | 2020 | 2026 | Change |

|---|---|---|---|

| Rent (upgraded to 2BR for kids) | $1,200 | $1,580 | +$380 |

| Groceries (family of 4) | $500 | $670 | +$170 |

| Childcare (1 center, 1 preschool) | $900 | $1,240 | +$340 |

| Utilities | $120 | $170 | +$50 |

| Transportation (car, insurance, gas) | $400 | $520 | +$120 |

| Other insurance | $200 | $250 | +$50 |

| Essentials subtotal | $3,320 | $4,430 | +$1,110 |

| Take-home pay | $3,850 | $3,850 | — |

| Surplus/deficit | +$530 | -$580 | -$1,110 |

Sarah went from $530 monthly breathing room to $580 in the red. She's not overspending on lattes or streaming. She's $580 short of covering survival every month.

Michelle: Sandwich Generation

Single parent earning $72,000/year ($4,800/month after taxes). She's supporting two teenagers and helping her aging mother with medical costs.

| Item | 2020 | 2026 |

|---|---|---|

| Rent (3BR for kids + guest room for mother) | $1,300 | $1,740 |

| Groceries (family of 4 + elderly parent) | $600 | $810 |

| Mother's medications + doctor visits | $150 | $280 |

| Utilities | $140 | $200 |

| Teens' school supplies, activities | $200 | $200 |

| Car payment + insurance + gas | $450 | $580 |

| Phone, internet | $100 | $130 |

| Essentials subtotal | $2,940 | $3,940 |

| After-essentials budget | $1,860 | $860 |

Michelle went from $1,860 in breathing room to $860. She's making the same salary. The math broke anyway.

Jake: Young Professional

Earns $85,000/year ($5,600/month after taxes) in a major city and thought he had it figured out.

| Item | 2020 | 2026 |

|---|---|---|

| Rent (1BR apartment) | $1,400 | $1,890 |

| Groceries | $250 | $335 |

| Utilities | $80 | $115 |

| Transportation (car + parking) | $350 | $455 |

| Phone, internet | $80 | $110 |

| Insurance, miscellaneous | $200 | $300 |

| Essentials subtotal | $2,360 | $3,205 |

| After-essentials | $3,240 | $2,395 |

Jake's breathing room dropped 26%. He went from feeling financially stable to wondering if he should move back home.

The pattern across all three: the essentials grew faster than the salary. Every month, the gap widens.

The Triage Framework: How to Budget Under Pressure

Here's the framework that makes budgeting under pressure survivable.

Not all spending is equal. If you cut food in half, people get sick. If you cut discretionary spending, your quality of life drops, but survival continues. These are different categories that need different strategies.

Tier 1: Survival (55-65% of low-income budget)

Housing, food, utilities, transportation to work, insurance.

Goal: Optimize, not cut. Find cheaper housing in a safe area, meal plan to prevent food waste, reduce energy consumption through audits, carpool or use public transit. These optimizations usually save 5-15%, not 50%. You're not solving the gap by optimizing Tier 1. You're just making the squeeze slightly less painful.

Tier 2: Health & Security (15-25% of budget)

Childcare, medications, car maintenance, internet (increasingly critical for work), emergency fund building, mental health support.

Goal: Prioritize ruthlessly. Cutting Tier 2 without a plan usually creates bigger problems. Childcare disruption means missed work. Skipped medications mean health crises. Deferred car maintenance means a $2,000 breakdown instead of a $200 oil change.

Strategy: Find creative alternatives. Mental health support can be a free community mental health clinic instead of therapy at $150/session. Childcare can be a daycare co-op with a trusted friend instead of a commercial center.

Tier 3: Quality of Life (Compress 50%, not eliminate)

Streaming services, restaurant meals, gym memberships, hobbies, coffee shops, subscriptions.

This is the $200-400 monthly category in a typical budget. Here's the trap of every "cancel everything" guide: remove it all and you burn out. Spend it all and the budget doesn't work.

Better strategy: Cut 50% of Tier 3, not 100%. Keep one small joy — the $15/month coffee membership, the $12/month streaming service, the $25/month hobby budget. Redirect the rest.

That frees $100-150/month without requiring you to live in total deprivation. Sustainable beats austere every time.

Tier 4: Discretionary (Eliminate temporarily)

Vacations, luxury items, premium versions of things, new clothing trends, entertainment outings. This goes to zero when you're in the squeeze. It's not forever. But when the budget doesn't work, Tier 4 is the first casualty.

Housing Affordability: Rent vs. Buy

Housing is the largest expense for most families, and 2026's housing market is still broken.

Start with the down payment. The median existing-home price was $420,600 in October 2025 (NAR). A 20% down payment on that home is $84,120 — slightly more than the entire median household income, which the Census Bureau put at $83,730 for 2024. A full year of gross income, sitting in liquid savings, before the buying process even starts. Most households don't have that.

NAR's affordability data puts the qualifying income to buy that median home at about $100,000 — well above what the median household earns. Housing affordability collapsed in 2022–2023 to its worst levels since the 1980s and has only partially recovered since.

Here's what that translates to by income bracket, per the NAR / Realtor.com Housing Affordability & Supply report:

| Income | % of Listings Affordable (2025) | % of Listings Affordable (2019) |

|---|---|---|

| $50,000 | 8.7% | ~28% |

| $75,000 | 21.2% | ~49% |

| $100,000 | 37.1% | ~63% |

This isn't a niche problem. A household earning $75,000 can afford about 1 in 5 homes on the market — down from roughly half of listings in 2019.

Your realistic options:

Option 1: Rent + Invest — Rent for $1,500/month. Invest the difference you would have spent on a mortgage, taxes, insurance, maintenance. Over 30 years at 7% returns, that invested difference builds $500K+ in non-housing wealth. Catch: Rent rises. In high-inflation years, rent can rise 5-10% annually.

Option 2: Geographic Arbitrage — Move to a secondary market where median prices are $250-300K instead of $450K. Catch: That move might mean leaving your job, family, community.

Option 3: Multigenerational Living — Combine households. You, spouse, one or both parents in one 3BR. Rent drops from $2,800 (two separate apartments) to $2,200. Share utilities and coordinate childcare. Catch: Loss of privacy, family politics, caregiving stress. But the financial math is real.

Option 4: ADU Ownership — Buy modest home with ADU (accessory dwelling unit — a rental unit on the property). Rent the ADU for $1,200-1,500/month. Your effective housing cost drops 50-70%. Catch: Requires capital for down payment, requires being a landlord, requires dealing with local zoning.

For deeper exploration, see Housing Affordability & Multi-Generational Strategies 2026.

Food Price Inflation: Eat Cheap Without Starving

Grocery (food-at-home) prices are up roughly 29% since 2020, per USDA Economic Research Service data. A family that spent $500/month on groceries in 2020 is now spending about $645/month for the exact same items. And 18.4% of households with children experienced food insecurity in 2024.

The Tactical Approach

Meal planning: Plan meals by the week. Write down exactly what you'll eat. Shop from that list. This prevents "open the fridge and panic-buy something" spending.

Average cost per meal when you plan:

- Breakfast (oatmeal, eggs, toast, fruit): $1.50 per person

- Lunch (sandwich, salad, pasta): $2.00 per person

- Dinner (bean chili, rice bowls, pasta): $2.50-3.00 per person

- Total daily food cost: $6-6.50 per person

For a family of four, that's $24-26/day or $720-780/month.

Bulk buying: Buy rice, beans, lentils, oats in bulk. These are $0.50-0.80/pound instead of $1.50-2.00 in packaged versions.

Seasonal and frozen: Fresh strawberries in January cost 3x what they cost in June. Buy frozen. It's just as nutritious, lasts longer, and costs 60% less.

Reduce meat portion sizes: Meat is expensive. But you don't need 8oz per person. Use 4-5oz mixed into a bean-based or vegetable-based meal. A $10 chicken breast now feeds 3 people instead of 2.

Stretch proteins: A pound of ground beef becomes tacos for four people (30% meat, 70% beans). A whole chicken becomes three meals — roasted (dinner night 1), shredded for burritos or fried rice (night 2), stock made from the bones (night 3).

Make your own staples: Bread costs $4/loaf. Homemade bread costs $0.50 in ingredients. Yogurt costs $6/container; homemade costs $0.80.

Food banks: If your family qualifies for SNAP benefits or food pantries, use them. No shame. You paid into the system. This is what it's for.

The Subscription Leak: Small Charges, Big Lifetime Numbers

In a 2022 C+R Research survey, the average American estimated they spend $86 a month on subscriptions. Their actual itemized spending averaged $219 a month. That's a $133 per month gap — about $1,600 per year that people don't realize they're paying. 42% of respondents had forgotten they were still being charged for a subscription they no longer use.

| Item | Monthly | Annual | 30-Year Cost (7% returns) |

|---|---|---|---|

| Coffee runs (5x/week @ $5) | $100 | $1,200 | $128,000 |

| Streaming services (4 platforms) | $50 | $600 | $64,000 |

| Subscriptions (apps, tools, memberships) | $80 | $960 | $102,000 |

| BNPL overspending (impulse buys) | $80 | $960 | $102,000 |

| Restaurant meals (2x/week) | $60 | $720 | $77,000 |

| Total leakage | $370 | $4,440 | $473,000 |

That bottom number — $473,000 — is the cost of not looking. $370/month in small, invisible charges compounds into nearly half a million dollars over a career.

Here's what cuts without crashing:

Shift coffee from daily to weekly treat. Pick one streaming service. Finish what you're watching. Cancel. Subscribe to the next. Over 12 months, you watch the same content at 1/4 the cost. Avoid BNPL. Redirect freed money immediately to your emergency fund or investment account.

Energy, Utilities, Childcare: The Inelastic Squeeze

Some expenses don't compress. An electricity bill that's up 29% doesn't compress to 0% by turning off lights. Childcare that's up 29% doesn't compress by having kids skip school. These are inelastic.

Electricity and Utilities

The average US monthly electricity bill rose from about $121 in 2021 to $156 in 2025 — up nearly 29% — and the EIA expects prices to keep climbing. The result: about 21.5 million households — roughly 1 in 6 — are behind on their energy bills, per the National Energy Assistance Directors Association.

Micro-tactics that actually work:

- Energy audit: Many utilities offer free audits. Identify where energy is leaking. A one-time $500 improvement saves $30-50/month forever.

- Time-shift usage: Run dishwasher, laundry at off-peak hours (usually 9pm-6am). Many utilities offer time-of-use rates that can save 20-30%.

- Water heating: Lower the thermostat to 120°F. Take shorter showers. Save $20-30/month.

- Appliance replacement: Old fridge uses 2x electricity of new one. Upgrading costs $800-1,200 but saves $15-20/month. That's 5-6 year payback.

Reality check: These tactics save 5-15%, not 50%. They matter, but don't solve the problem.

Childcare

The national average price of childcare hit $13,128 per year in 2024 — up 29% since 2020, outpacing overall inflation, per Child Care Aware of America. It's now the second-largest expense for many families with young children.

Full-time center-based care commonly runs $1,300-1,800/month for infants and $900-1,300/month for preschool in higher-cost states (prices vary enormously by state). With two kids, you're at $2,000-2,500/month.

Non-traditional alternatives:

- Daycare co-ops: 3-4 families share a care provider. Cost drops 40%.

- Nanny share: Two families share one nanny. $1,000-1,400/month per family.

- Family support: If grandparents nearby, cost drops to free-low cost.

- Shift work: One partner works nights/weekends. Eliminates childcare but is exhausting.

Building Wealth From Almost Nothing

Here's the game-changer: financial discipline in constraint actually builds stronger wealth habits than discipline when money is loose.

The wealth equation: Wealth = (Income − Expenses) + (Returns × Invested Money) + Time

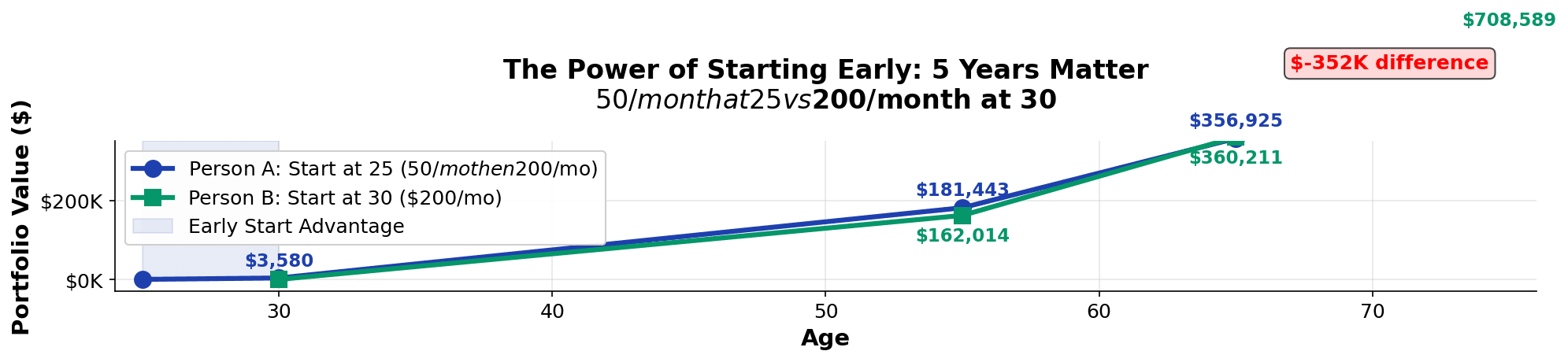

When squeezed, income is limited and expenses are nearly fixed. You can't control those much. But you control time. Time is the lever.

Person A starts at 25 with $0. Saves $50/month for 5 years (saves $3,000), then $200/month for 25 years. At 7% returns: $297,000 by 65.

Person B waits until 30 to start. Saves $200/month for 35 years. At 7% returns: $263,000 by 65.

Person A ends with $34,000 more, even though they saved $3,000 less total. The difference: the five-year head start.

Here's the math in action:

Sarah starts at 25, makes $35,000/year, takes home $2,600/month.

| Expense | Amount |

|---|---|

| Rent | $1,000 |

| Food | $300 |

| Transportation | $400 |

| Utilities + phone + internet | $150 |

| Insurance | $300 |

| Subscriptions + miscellaneous | $150 |

| Total | $2,300 |

| Available to invest | $300 |

$300/month at 7% annual returns for 40 years = $1.1 million.

That's not a typo. That's compounding. Time is the variable you control when you have no money.

The system: (1) Set a hard cap on discretionary spending (not zero, but $100-150/month). (2) Automate savings on payday before you see it. (3) Direct any windfalls: 50% emergency fund, 50% investments. (4) Ignore the noise.

Tools & Systems: MFFT, YNAB, Rocket Money

The right tool prevents financial fog. It's the difference between "I don't know where my money is going" and "I see exactly where my money is going and why."

MFFT: Categories, category limits, net worth tracking. Free until August 2026. Best for seeing your full financial picture simply and visually.

YNAB: Rule-based budgeting. Every dollar gets a job before you spend it. $15.99/month. Best for step-by-step guidance.

Rocket Money: Finds forgotten subscriptions and highlights waste. Free tier available, premium $12.99/month. Best if subscriptions are your main leak.

Spreadsheet: Full control, manual entry, free. Slowest but most customizable. Best if you're technical.

Which to choose? New to budgeting and overwhelmed? Start with MFFT or YNAB. Your main leak is subscriptions? Rocket Money first. Technical and want full control? Spreadsheet.

The Reframe: Discipline in Crisis Becomes Discipline for Life

Here's what I want you to understand: the budget you build during a squeeze is the strongest foundation for wealth-building you can construct.

It's easy to be disciplined when money is loose. Save 10% and still live comfortably. But when you're tight — when you're saving $50/month on a $35,000 salary — that's the real discipline. That's the habit that doesn't break when life gets complicated.

The families that survive recessions aren't the ones with the highest incomes. They're the ones with the strongest spending discipline. And they built that discipline when it mattered most.

You're not in this position because you failed. You're in this position because the cost of living exploded and your paycheck didn't keep up with the parts of it you can't skip. That's structural. But your response — the budget, the automation, the discipline, the reinvestment of freed-up dollars — that's yours.

Over time that response compounds. The person saving $50/month at 25, increasing to $200/month at 30, then $500/month at 35, and $1,000/month by 45 — that person isn't just accumulating money. They're accumulating wealth. By 65, they're not working because they have to. They're working because they choose to.

That's where this leads.

You're Not Alone, and the Math Works

Right now: 59% of Americans can't cover a $1,000 emergency from savings. 13.7% of households are food-insecure. 1 in 6 households is behind on its energy bills.

That's not personal failure. That's a structural crisis.

But structural crises have structural solutions. And one of them is available to you right now: the discipline to build a budget that acknowledges reality, protect the things that matter most, cut without crashing, and invest the freed-up dollars into a future that's genuinely different from today.

The math works. It always does. It just takes time, consistency, and the willingness to feel uncomfortable for a season so you don't feel broken forever.

You can do this.

Stay Updated

Get notified about new articles and MFFT build-in-public updates.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Real Return-to-Office Cost: I Put My Commute in a Spreadsheet

Our VP announced 'exciting news about how we work together,' which is corporate for a three-day return-to-office push. So I did the tool-builder thing and put my commute in a spreadsheet. The yearly number stung. The 30-year compounded one made me close the laptop. Here's the honest math.

Master Your Money

Master Your MoneyStablecoin Savings Accounts: Is 8% Yield Worth the Risk in 2026?

My savings rate slid to 2.4% and an app dangled 7.2%. I almost bit. Here's where a stablecoin savings account's yield in 2026 really comes from, what the ads hide, and the math that stopped me.

Master Your Money

Master Your MoneyRent vs Buy in 2026: I Ran the Numbers, Kept Renting, and Invested the Difference

My uncle swears renting is throwing money away. So I built the rent vs buy 2026 model: renting wins in all 50 metros, but only if you invest the difference.

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.