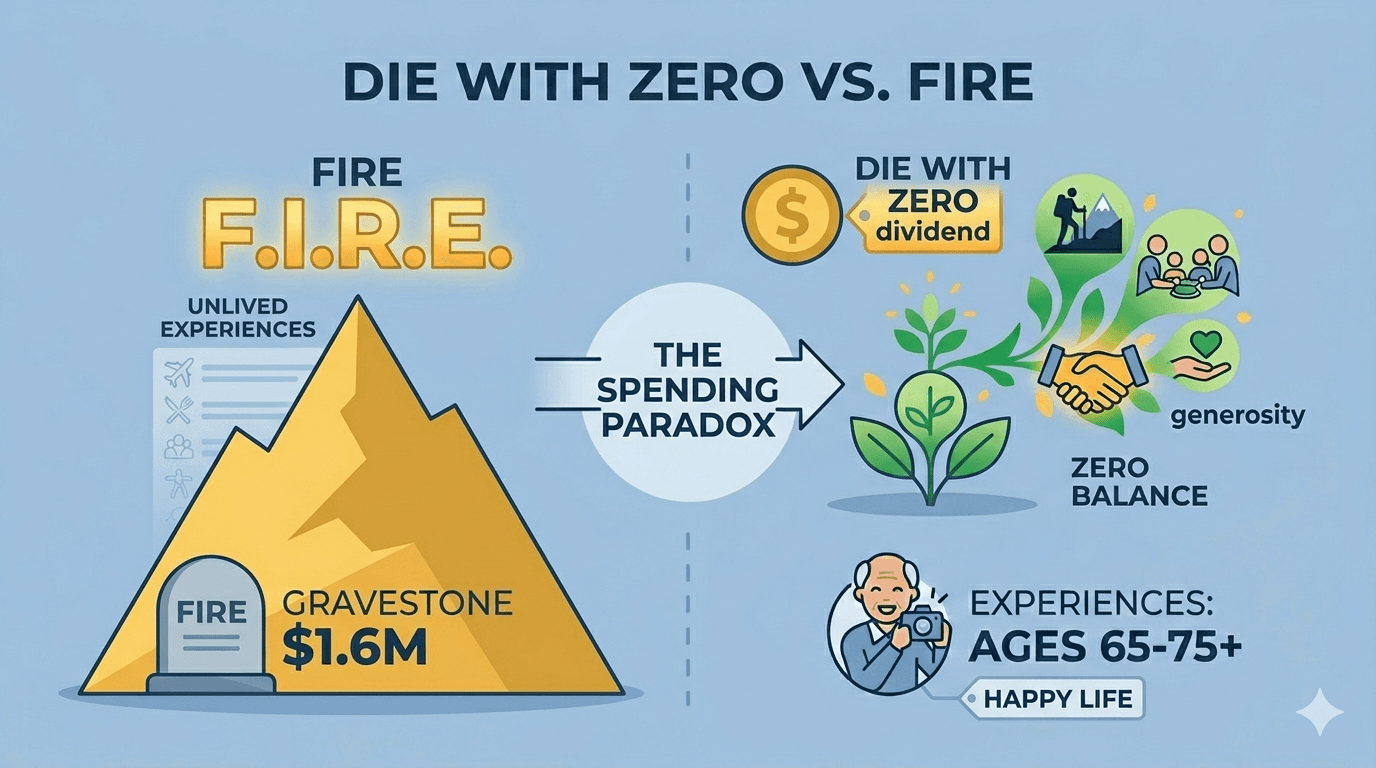

Die With Zero vs FIRE: The Retirement Spending Paradox

Picture a 65-year-old couple who did everything right.

They saved 40% of their income for thirty years. They paid off the house. They built a $1.6 million portfolio that, by every conventional measure, screams "you can finally relax."

Then, in retirement, they pull out exactly 2.1% per year — barely half of the classic safe withdrawal rate. The math is astonishing. Their portfolio keeps growing. Their hair keeps graying. The Norway trip they always talked about quietly fades into "maybe next summer." And one day someone inherits the entire balance.

This is the die with zero vs FIRE debate in one sentence: financial independence solves how much to save, but most people never solve how much to spend. And the cost of that gap, measured in unlived experiences, may be the most expensive mistake in personal finance.

Let me show you the numbers — and then a way out.

The 2.1% Problem: Where Die With Zero vs FIRE Starts to Bite

Here's a stat that should rearrange how you think about retirement.

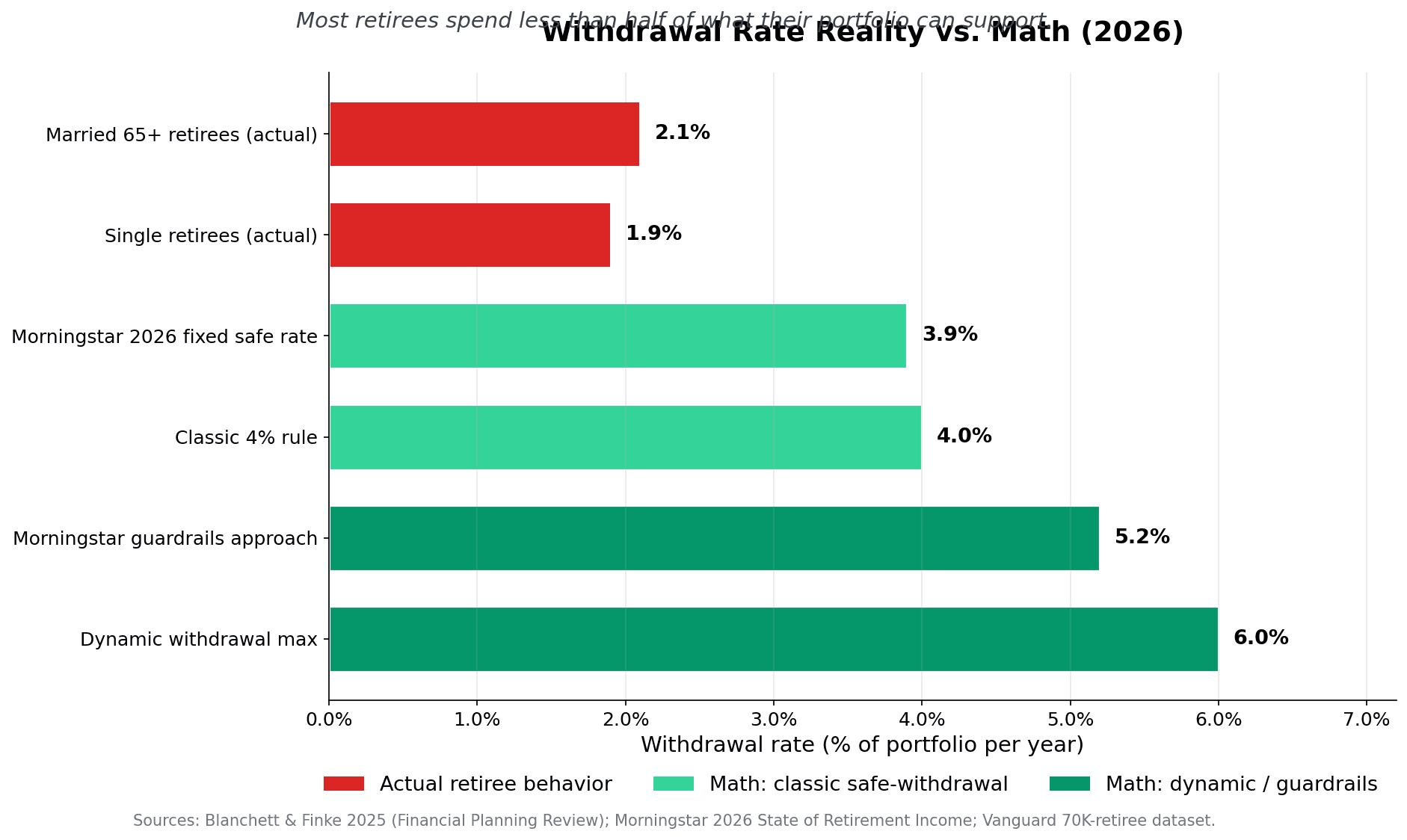

A 2025 study by retirement researchers David Blanchett and Michael Finke, published in the Financial Planning Review as "Retirees Spend Lifetime Income, Not Savings", looked at how married 65-year-old retirees with at least $100,000 in assets actually withdraw from their portfolios. The headline number: 2.1% per year. Single retirees came in even lower at 1.9%.

For context, the 4% rule — the gold standard most FIRE calculators run on — would tell that same retiree they could safely pull $64,000 a year off a $1.6M portfolio. They are pulling about $33,600. That is more than $30,000 a year of theoretically "safe" spending that they are not using.

It gets worse. Vanguard's analysis of retiree withdrawal behavior found that roughly 1 in 4 never touched their savings at all over a five-year window. Another half took only irregular, sporadic withdrawals. Only about 20% maintained anything resembling a steady spending plan.

The kicker? An NBER analysis by Poterba, Venti, and Wise showed that 46% of retired Americans die with $10,000 or less in financial savings — but that's because most of them lean on Social Security and pensions. Among middle- and high-income retirees with real portfolios, the pattern flips. They die with most of their wealth intact. The Federal Reserve Bank of Richmond found that even households who claim no bequest motive end up with 14–26% larger balances than that motive would predict. Translation: they say they're not saving for the kids — but their behavior says otherwise.

If you want a sober reality check on whether your savings number is actually high enough, the net worth at age post lays out the benchmarks. But the spending side of the equation rarely shows up in those checklists. That's the gap this article fills.

The point isn't that retirees are wrong to be cautious. The point is that "I'd rather die with too much than too little" sounds reasonable until you realize how lopsided that bet actually is. Living a smaller life every year for 30 years to avoid a 5% chance of running out at 92 is not a great trade.

What Die With Zero Actually Says (And What It Doesn't)

Bill Perkins is a hedge fund manager who, in 2020, wrote a book called Die With Zero that detonated like a small bomb in the FIRE community. The thesis is deceptively simple: the goal of money is to fund a life, not to maximize the balance on a tombstone.

His argument runs roughly like this. Every dollar you save is a vote for your future self. But your future self has limits — physical, cognitive, emotional — that your present self doesn't. You can't backpack through Patagonia at 85 the way you can at 35. You can't carry your kids on your shoulders at the beach forever. There are time-locked experiences, and the price of waiting is not paid in dollars. It's paid in capacity.

So when someone over-saves and dies with $2 million in the bank, Perkins doesn't say "good for them." He says they wasted that money. Not in the trash-it sense — in the unrealized utility sense. That money could have funded thirty years of memories, family trips, sabbaticals, generosity. Instead, it became a number on a probate form.

His most quoted line: "The business of life is the acquisition of memories." That's the spirit of the framework.

But people misread Die With Zero almost immediately. So let's clear the misconceptions:

- It is not "spend recklessly." Perkins is intensely numerical. He recommends a survival-threshold formula: 0.7 × annual cost of living × years of life remaining. For a 45-year-old spending $70K/year and planning to age 100, that's a $2.695M floor that does not get touched.

- It is not "don't save." It is "stop saving past the point where additional dollars can be converted into life experience."

- It is not anti-FIRE. If anything, it's the missing decumulation chapter that the FIRE movement never quite finished writing. FIRE solved the accumulation puzzle. Die With Zero is trying to solve the spending puzzle.

The cleanest way I think about it: FIRE asks "when can I stop working?" Die With Zero asks "what is working for?" Both are valid. They're answering different questions.

The Memory Dividend: Why a $10,000 Trip at 35 Beats $94,000 at 80

This is the part that tends to convert FIRE skeptics into Die-With-Zero curious.

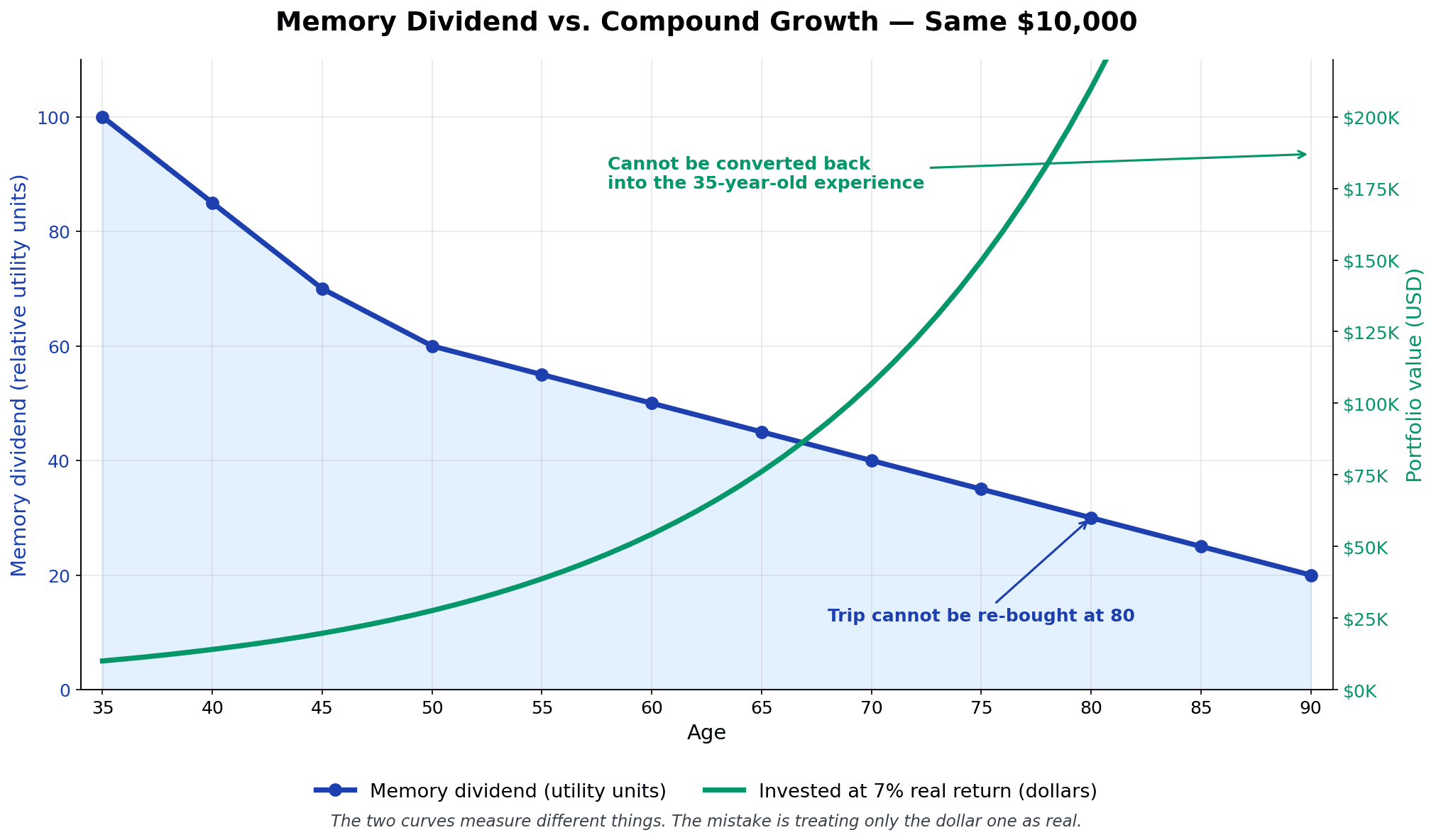

Perkins introduces a concept he calls the memory dividend. The idea: when you do something memorable — a trip, a milestone, a shared experience — the financial cost is one-time, but the emotional return compounds for years. You replay it. You laugh about it. You tell the story at dinner parties. Your kids tell it at their dinner parties.

Now run the numbers two ways.

Path A — Spend the $10,000 at 35. A two-week trip with the family. You're in your prime. The kids are 6 and 9. Your parents are mobile enough to fly out and meet you for a weekend. You take 800 photos. The trip costs $10K and "ends." But the memory keeps paying out. For the next 50 years, that experience is part of your family's story.

Path B — Invest the $10,000 at 35. At 7% real returns, that $10,000 becomes about $94,000 by age 80. On paper, that's a 9.4x return. Impressive.

But here's the asymmetry: at 80, you cannot retroactively buy back the trip you didn't take at 35. The kids are grown. Your parents may be gone. Your knees may not be cooperating with hiking trails. The experience window is closed.

Line B is denominated in dollars. Line A is denominated in life. We optimize for the one that's easy to measure and ignore the one that actually matters. That's the FIRE blind spot.

A few things to be careful about here. The memory dividend isn't infinite — its emotional weight does fade. And not every $10,000 produces a memory; spending it on a slightly nicer car generally won't. The framework only works for time-locked, intentional, peak-utility experiences. But when you find one, the math against compound growth isn't even close.

Why FIRE Hyper-Savers Get Stuck

Here's the uncomfortable truth: a lot of people who hit their FIRE number can't bring themselves to actually use it.

There's a Reddit post that gets shared every few months on r/financialindependence. A 35-year-old engineer with about $3 million invested writes that he feels "dead inside." He nailed the math. He can retire any time. And yet he keeps grinding because the idea of spending the money — actually drawing it down — feels physically wrong.

Or take Jake (a real archetype, profiled in a 24/7 Wall St. piece in April 2026). He's 52. He has a $2.4 million portfolio. It throws off about $3,500 a month in dividends. He drives a 12-year-old Honda Civic, debates a $4 latte for ten minutes, and hasn't taken a vacation since 2019. He doesn't feel rich. He feels exposed.

What's going on?

Loss aversion. Behavioral economists have shown that pulling money out of your own savings registers in the brain as a loss — heavier and more painful than the equivalent dollars from Social Security or a pension. Guaranteed income gets spent at about 80%. Personal savings get spent at about 50%. That's not preference. That's wiring.

Identity inertia. Thirty years of "I am a saver" is a hard switch to flip. The neural pathways that helped you build the portfolio are the same ones that now refuse to let you spend it.

Scarcity hangover. Many FIRE pursuers come from frugal childhoods, debt traumas, or burnout-driven savings sprints. The fear muscle is enormous. The enjoyment muscle is atrophied.

Sequence-of-returns risk. A real one — Wade Pfau's research shows that about 77% of a portfolio's final outcome is determined by the first 10 years of returns. So early retirees aren't being irrational to feel cautious. They just often overshoot the caution.

This isn't a moral failing. It's a system error. The FIRE community spent two decades teaching people how to accumulate and almost no time teaching them how to deploy. If you're feeling this — and want a softer on-ramp — the time freedom over retirement framing is worth a read. It's the same money, with a saner relationship to work.

The Retirement Spending Smile (And Why It Beats the Flat 4%)

If you only take one technical idea from this post, take this one.

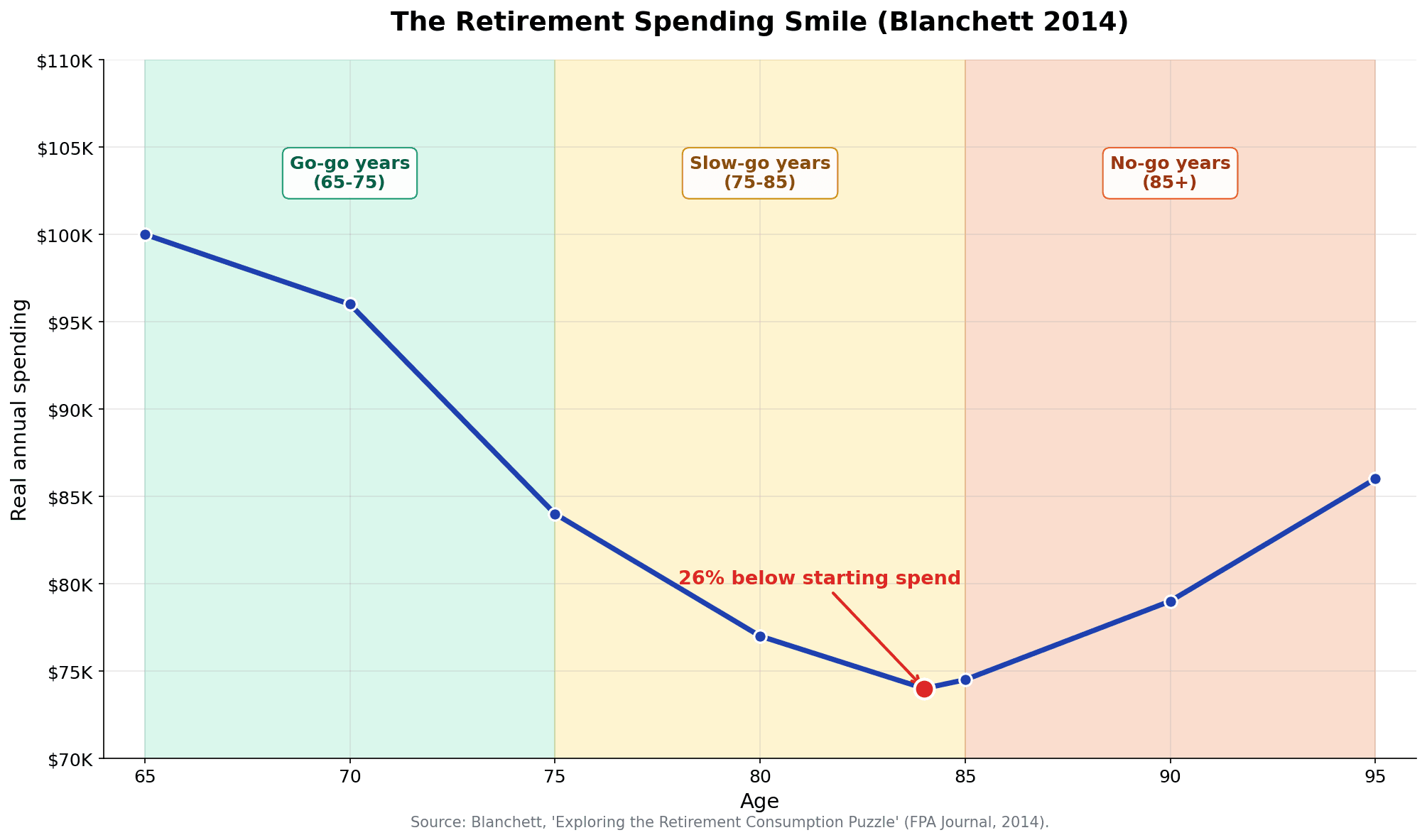

David Blanchett — the same researcher behind the 2.1% finding — published a now-famous 2014 paper titled "Exploring the Retirement Consumption Puzzle" in the Journal of Financial Planning. He looked at thousands of real retirees and found that real (inflation-adjusted) spending doesn't stay flat. It follows a U-shape, which he nicknamed the retirement spending smile.

Roughly:

- Ages 65–75 (the "go-go" years): spending is highest. Travel, hobbies, family, projects.

- Ages 75–85 (the "slow-go" years): spending drifts down — about 1% per year in real terms. Energy fades, routines settle.

- Ages 85+ (the "no-go" years): spending ticks up again, but mostly on healthcare and long-term care, not lifestyle.

The math implication is huge. A flat 4% withdrawal plan is engineered for someone whose real spending stays constant for 30 years. But almost nobody actually spends like that. Real spending bottoms out at about 26% below the starting level around age 84.

Kitces' team has run the numbers on the spending smile: a 4% constant-real withdrawal succeeds about 73% of the time historically. Switch to the spending-smile shape and you're looking at 80–91% success — for the same starting portfolio, with more spending in your high-energy years. (The failure cases cluster around one specific danger: a bad market in your first retirement years — sequence of returns risk and how to defuse it is the companion read here.)

The spending smile is also why Die With Zero isn't reckless. It says, mathematically: front-load your spending toward the years when you have both money and energy. That's not gambling on longevity. That's matching the spending shape to the actual life shape.

The Hybrid "Spend Forward, Save Back" Framework

Now we get to the practical part. Here's the five-step framework I think actually merges Die With Zero with FIRE math without breaking either one.

Step 1 — Set the Survival Floor First (Non-Negotiable)

Run Perkins' formula: 0.7 × annual essential spending × years to age 95.

Take a 45-year-old whose essentials run $60,000/year and who plans for age 95: 0.7 × $60,000 × 50 = $2.1 million. That's the floor that does not get spent forward, no matter what. Healthcare alone is a major reason: Fidelity's retiree health care cost estimate puts retirement healthcare at $172,500 for an individual and roughly $315,000–$400,000 for a couple — and that's before long-term care, where median assisted living now runs $74,400/year and a private nursing home room is $135,528/year.

Step 2 — Identify Your Time-Locked "Go-Go" Experiences

This is the homework most people skip. List 3–5 experiences that are time-locked — meaning you genuinely cannot do them at 80, no matter how much money you have. Examples: a backpacking trip with your dad while he's still mobile. Soccer summer camp with your 9-year-old. A sabbatical year before your kids start middle school. Trail running across a country.

If you can't think of any, that's a flag. The whole framework breaks down if you're saving for something you've never named.

Step 3 — Reserve 5–10% of Pre-FI Savings as "Experience Capital"

If your FIRE number is $2 million, carve out $100,000 to $200,000 that lives outside the compounding plan. This is decumulation capital, not investing capital. Most people skip this and then are surprised when "spending forward" never happens — there's no bucket to spend from.

Coast FIRE folks have a particular advantage here. Once your existing investments will compound to your number with zero new contributions, every additional savings dollar is, by definition, deferred experience capital. You can stop adding to retirement and start funding "Decade of Travel" without breaking the math.

Step 4 — Use Age-Banded Withdrawal Rates

Throw out the flat 4% rule. Try this instead, anchored to the spending smile:

| Age band | Withdrawal rate | Why |

|---|---|---|

| 60–75 (go-go) | 4.5–5.0% | Highest energy, time-locked experiences |

| 75–85 (slow-go) | 3.5–4.0% | Lifestyle spending naturally falls |

| 85+ (no-go) | 4.5–5.0% | Healthcare and care costs rise |

For early retirees bridging to 59½, you also want a tax-efficient access path. The Roth conversion ladder is the standard play — it lets you convert traditional retirement money into accessible Roth dollars without the 10% penalty, which is what makes early decumulation actually work.

Step 5 — Run an Annual "Decumulation Review"

Every January: net worth check, withdrawal rate check, then — and this is the part most people skip — schedule next year's experience spending before the year starts. Put the trip on the calendar. Wire the deposit. Buy the tickets non-refundable. If it's not on the calendar with money already moved, it won't happen.

This is where I'll plug a tool angle. Most net-worth trackers, including the budgeting and tracking features inside MFFT, are great at the accumulation side — net worth lines going up, savings rates trending right, projections out to 65. The decumulation side is rarer. Set up a "Memory Dividend" goal bucket alongside your "Healthcare Reserve" bucket and treat it as a real category, not an afterthought. Most people don't have a "Big Experiences" line in their budget. That's the line that makes Die With Zero real.

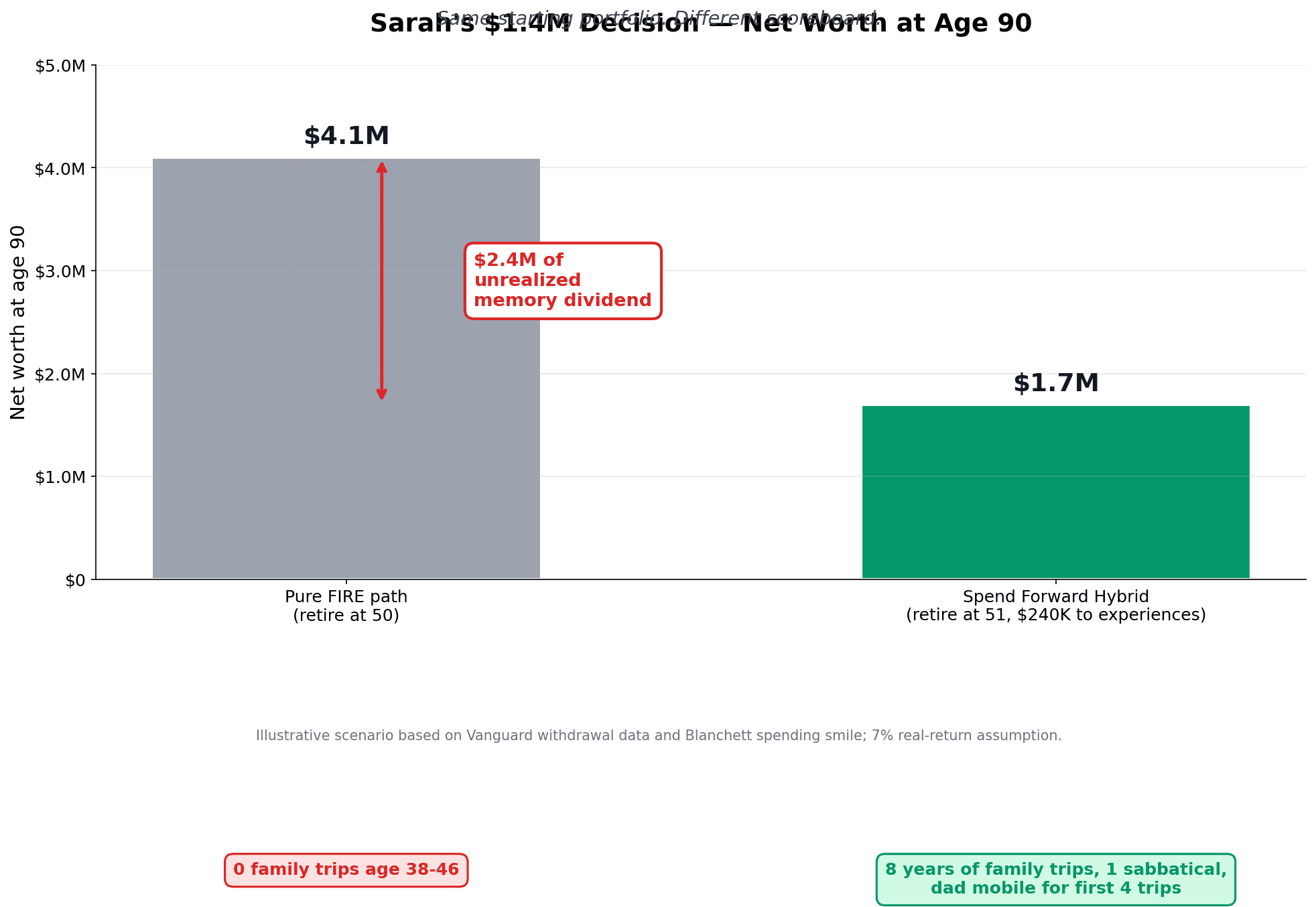

Worked Example: Sarah's $1.4M Decision

Let me make this concrete with a character.

Sarah, 38, software engineer, $1.4 million invested. Married, two kids ages 8 and 11. Her father is 71 and in good shape now but starting to slow down. She and her husband save 50% of household income.

She's running two paths through her planner.

Path A — Pure FIRE. Keep saving 50%. At 7% real returns, her invested portfolio compounds from $1.4M today to roughly $1.8M at age 50. She quits at 50, draws 4% ($72K/year), sails into traditional retirement. Net worth at age 90: about $4.1M.

Path B — Spend Forward Hybrid. Carve out $30,000/year for 8 years into a "memory dividend bucket" — Norway with the kids while her dad is mobile, Patagonia in summer, six weeks in Italy with extended family. Total redirected: $240,000. Her FI date slips one year — she retires at 51 instead of 50, with about $1.5M. Net worth at age 90: about $1.7M.

The Path-A version has $2.4M more on a probate form at 90.

The Path-B version actually took the trips while her dad was alive, while her kids were young enough that "summer in Italy" still meant something, while her own knees still worked. The hybrid plan loses about a year of "early retirement" and gains an entire decade of irreplaceable family memory.

The hybrid wins on life utility by a wide margin. It "loses" on the dollar tally if you measure success at a funeral. Pick which scoreboard you're playing on.

When Die With Zero vs FIRE Comparisons Break Down

I want to be honest here, because the framework gets oversold.

Die With Zero stops working — and starts being dangerous — in a few specific situations:

- You don't have a Social Security or pension floor. Without guaranteed lifetime income, longevity risk is genuinely scary. If you live to 95 and the portfolio runs dry at 90, there's no safety net. The framework assumes that essentials are covered by something other than the depleting portfolio.

- You have dependents whose well-being depends on your assets. Special-needs children, aging parents you support, a non-working spouse meaningfully younger than you. In these cases, the portfolio is partly theirs, not yours. Don't spend forward someone else's safety.

- You face above-average late-life medical exposure. Family history of dementia, expensive chronic conditions, or no LTC insurance turns the late-life cost stack from "manageable" into "ruinous." Long-term care risk in particular is asymmetric — most people won't need it, but the ones who do can spend $135,000+ per year for years.

- Your problem is having too little, not too much. Critics rightly point out that Bill Perkins is a hedge fund manager. If your savings are below the longevity floor, the right move is to keep saving, not to spend forward against money you don't have.

The cleanest test: write down your essential annual spend, multiply by 0.7, multiply by years to 95. That's your floor. Above it, you can spend forward responsibly. At or below it, keep accumulating.

The Bottom Line: Wealth Without Time Is Just Numbers

Here's the philosophical core of the whole die with zero vs FIRE debate, as I see it.

FIRE answered the most important first-half-of-life question: can I stop trading my time for money? For a generation that watched their parents work 40 years and arrive at retirement exhausted, that's a real and worthy answer. I'm not anti-FIRE. I write about it constantly. I still believe a high savings rate compounded for a decade is the most powerful financial lever most people have access to.

But FIRE alone never answered the second-half-of-life question: what is the money for?

Die With Zero forces that question. It says — bluntly — that a portfolio is a tool, not a trophy. That memory is the only currency that pays dividends after you stop earning. That capacity (to hike, to travel, to be present, to take the trip) is itself a wasting asset. That dying with millions of unspent dollars isn't prudent — it's a category error, like winning Monopoly by hoarding the most cash and never trading for properties.

The synthesis: financial independence without a spending plan is just wealth-hoarding with extra steps.

So here's a homework assignment, the same one I gave myself last year. Pull out a sheet of paper. Write down three experiences you would deeply regret not doing in the next five years. Be specific. Names, places, who's coming with you. Then look up roughly what each one costs and add them up.

Whatever number you get — that is your starting decumulation budget. That is the dollar figure that begins to convert your savings into the only return that actually compounds: a life you wouldn't trade.

The FIRE math will keep doing its thing in the background. The years won't.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Start Here

Start HereEmpower vs Monarch Money (2026): Fees, Features, Verdict

Empower is free but sells 0.89%/yr advice once you link $100K. Monarch costs $99.99/yr and budgets better. June 2026 verified pricing, honest verdict.

Start Here

Start HereNet Worth Trackers That Don't Link to Your Bank (2026)

Track net worth without handing over bank logins: spreadsheets, GnuCash, Wealthfolio, Worthy, Kubera, and my manual-first tracker — honestly compared.

Start Here

Start HereYNAB Alternatives That Are Actually Free (2026 Guide)

YNAB costs $109/year in 2026. EveryDollar, Goodbudget, Actual Budget, spreadsheets, and my own tracker — what's actually free, with every catch listed.

Start Here

Start HereSocial Security 2033: FIRE-Proof Your Plan for a 23% Cut

The May 2026 CBO update moved insolvency to 2032 — a 23-28% benefit cut by 2033. How FIRE investors recalibrate nest egg, claiming age, and withdrawals.

Start Here

Start HereBarista FIRE vs Coast FIRE: Two Paths to Time Freedom

Barista FIRE vs Coast FIRE: both can cut your FI target 40-60% below 25x expenses. The math, trade-offs, and why 1 in 5 retirees go back to work anyway.