Geographic Arbitrage: Keep a Big-City Salary, Save $40K/Yr

TL;DR: Geographic salary arbitrage means keeping a big-city remote salary while living somewhere much cheaper — the data-scientist example below banks an extra $40,000 a year by moving from San Francisco to Austin. In 2026, 68% of remote workers who negotiate location-independent pay succeed, but 71% of companies now apply location-based pay adjustments, so the negotiation script matters. Done right, the FIRE community documents reaching financial independence 2-3x faster; the main landmines are return-to-office mandates and multi-state or international taxes.

New to the FIRE movement?

If geographic arbitrage is new to you, these articles will help you understand how it fits into bigger financial independence strategy:

- The FIRE Movement — the fundamentals of why geographic arbitrage accelerates your timeline

- Wealth = Time × Money × Discipline — how compound growth turns extra income into freedom

- Time Freedom Over Retirement — why arbitrage isn't about the beach; it's about buying optionality

Maya is 28, a data scientist at a fintech startup in San Francisco. Her offer letter says $155,000 base plus $35,000 bonus plus $50,000 equity vesting. She thinks she's done well.

Then her company announces permanent remote work. No office required. One catch: employees earning over $150,000 need to relocate or take a pay cut.

She does the math. Her apartment costs $3,200 a month. Her total annual expenses are roughly $72,000 — nearly 30% of gross income. If she moves to Austin, her rent drops to $1,400 a month. Annual expenses plummet to $32,000. Same job. Same salary. Same stock options.

She can suddenly save an extra $40,000 per year.

By moving.

This is geographic salary arbitrage, and in 2026 it might be the most powerful financial acceleration tactic available — especially for remote workers chasing financial independence. With 68% of remote workers successfully negotiating salary arbitrage, and companies now paying location-independent rates more openly, the opportunity is visible and achievable. But rising return-to-office mandates, aggressive location-based pay adjustments at 71% of companies, and complex tax rules have added new landmines.

This article walks through exactly how to identify arbitrage opportunities, negotiate without sacrificing salary, understand the tax implications, and decide if it's right for you.

What is Geographic Salary Arbitrage and Why 2026 is Different

Geographic salary arbitrage is a simple concept with extraordinary financial impact: earn a high-market salary from a company in an expensive city, then move to a low-cost region and keep the salary.

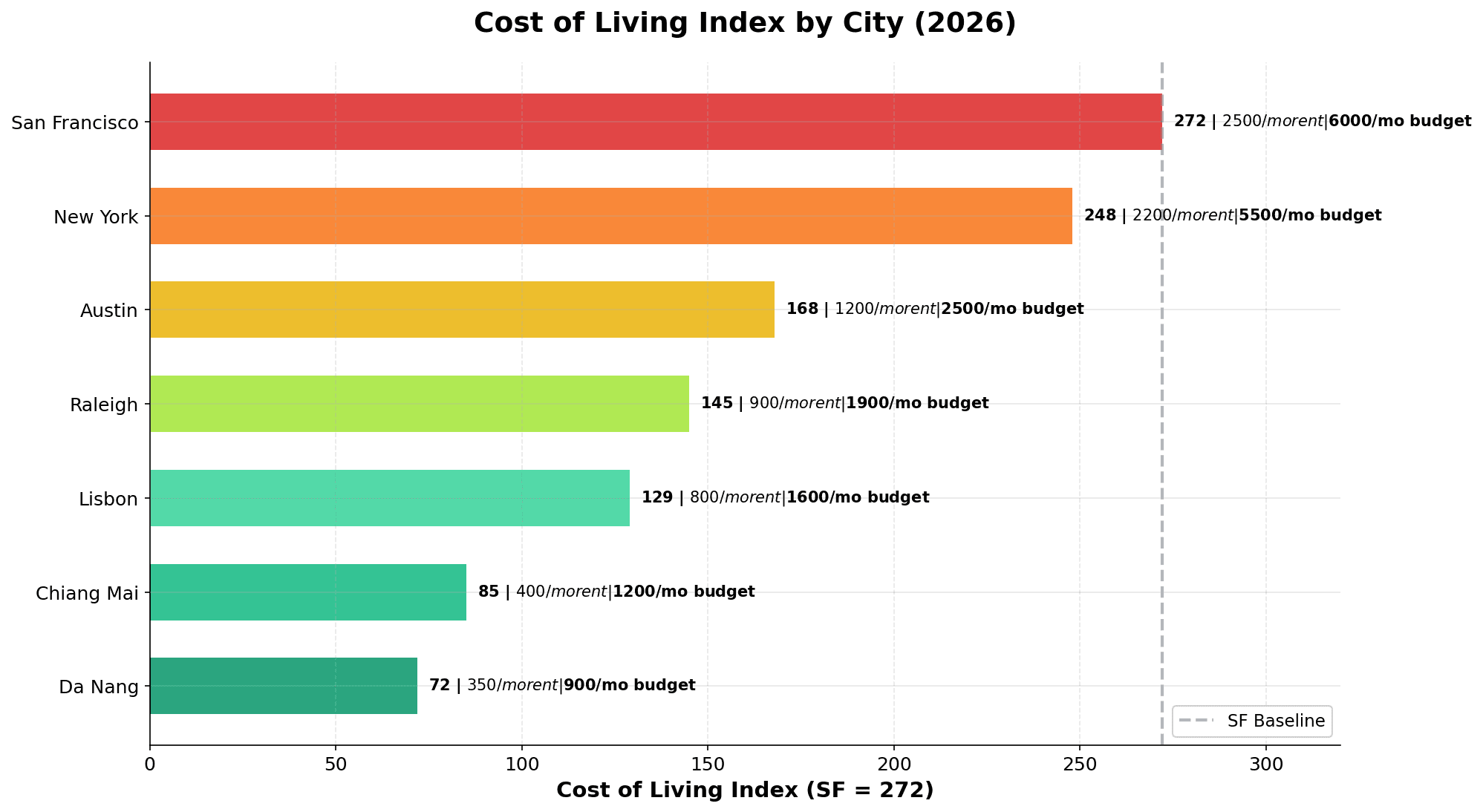

The math is straightforward. San Francisco's cost of living is 88% higher than Lisbon. New York costs 71% more than the U.S. national average. If you earn a $180,000 San Francisco salary and relocate to a low-cost U.S. city (Austin: 38% cheaper than SF) or internationally (Southeast Asia: 65-75% cheaper), your real income — what remains after paying for life — skyrockets.

This isn't new. What's different in 2026 is visibility and scale.

Remote work maturity. In 2025, 23.7% of U.S. workers teleworked on an average day. That number has stabilized at robust levels. Nearly 80% of workers in jobs that can be done remotely work hybrid or fully remote. Companies have stopped treating remote work as a pandemic temporary measure. They've built permanent remote policies, location-independent teams, and (for some) truly distributed salary models.

Salary data transparency. Pay transparency laws now force companies in California, Colorado, Hawaii, Illinois, Maryland, Massachusetts, Minnesota, New Jersey, New York, Vermont, and Washington to publish salary ranges — including for remote roles that could be filled in those states. This transparency arms workers with concrete benchmarks for negotiation.

Documented wins. The FIRE community has moved from anecdotes to data. ChooseFI calls geographic arbitrage a "cheat code" in the FIRE equation — it enables reaching financial independence 2-3x faster than peers. Workers openly share their salaries, cost-of-living comparisons, and timeline compression on platforms like Levels.fyi, Blind, and Reddit. The blueprint is visible.

But here's the headwind: 71% of companies now apply location-based pay adjustments. Return-to-office mandates are rising (55% of Fortune 100 companies now require full-time office attendance, up from just 5% in 2021). Tax complexity has exploded — multi-state withholding, nexus issues, and international visa complications add real friction to the strategy.

The opportunity is real. But it's narrower and more tactical than it was in 2021.

The Math: How Geographic Arbitrage Accelerates Financial Independence

Let me show you the concrete numbers, because the impact is genuinely dramatic.

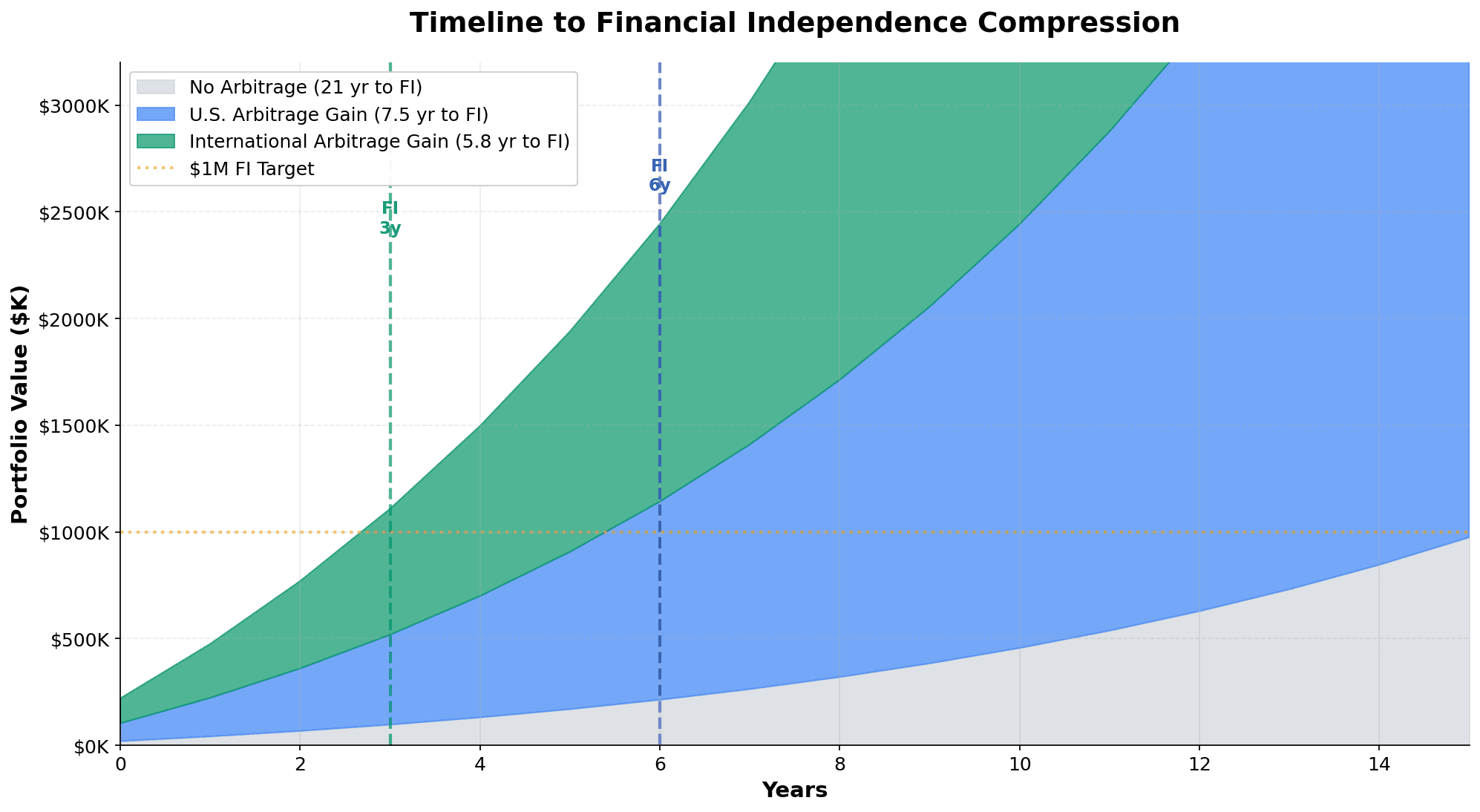

Meet Ethan. He's a senior product manager at a NYC tech company earning $180,000 base plus $60,000 bonus plus $80,000 equity = $320,000 total compensation. Life in Manhattan costs $85,000 per year. After taxes, his real savings rate is about 48% of gross — roughly $155,000/year he can invest.

At 8% annual returns, reaching a $1,000,000 portfolio takes Ethan roughly 6.5 years. That's his number for the 4% rule ($40,000 annual withdrawal to match his low-cost-of-living target).

Then he lands an offer from a remote Series-B startup (HQ: San Francisco) willing to pay $180,000 base plus $30,000 bonus, no location adjustment. He negotiates to relocate to Chiang Mai, Thailand. His annual cost of living drops to $15,000 (rent: $400/month, food, coworking, travel included).

Now Ethan saves roughly $195,000/year on a $210,000 base salary. That's a 93% savings rate.

Same income. Different cost of living. Different timeline.

| Scenario | Annual Salary | Annual Cost | Annual Savings | Years to $1M | Timeline Gain |

|---|---|---|---|---|---|

| NYC Original | $320K | $85K | $155K (48%) | 6.5 years | Baseline |

| Thailand Arbitrage | $210K | $15K | $195K (93%) | 5 years | 1.5 years faster |

That 1.5-year compression is not just math. It's real optionality. Ethan works five years internationally, hits his FI number, and either retires at 37 or pivots to work he loves without financial pressure. His peers in the $320K NYC role are still grinding 7 years in.

Now let's look at a domestic arbitrage case.

Meet Jordan, a software engineer at a Meta office in San Francisco earning $200,000 base plus $50,000 bonus plus $150,000 equity = $400,000 total comp. SF costs $72,000/year. His savings rate is about 67% of gross.

Meta applies location-based pay. If Jordan moves to Austin, his base drops to $160,000, bonus to $40,000, equity to $120,000 = $320,000 total (-20% hit).

But Austin costs $28,000/year. His savings rate is now 73% of gross on the lower salary.

| Scenario | Annual Salary | Annual Cost | Annual Savings | 10-Year Wealth | Real Income Gain |

|---|---|---|---|---|---|

| SF Original | $400K | $72K | $268K (67%) | $3.2M | Baseline |

| Austin (with 20% pay cut) | $320K | $28K | $292K (91%) | $3.5M | +$44K/year real savings |

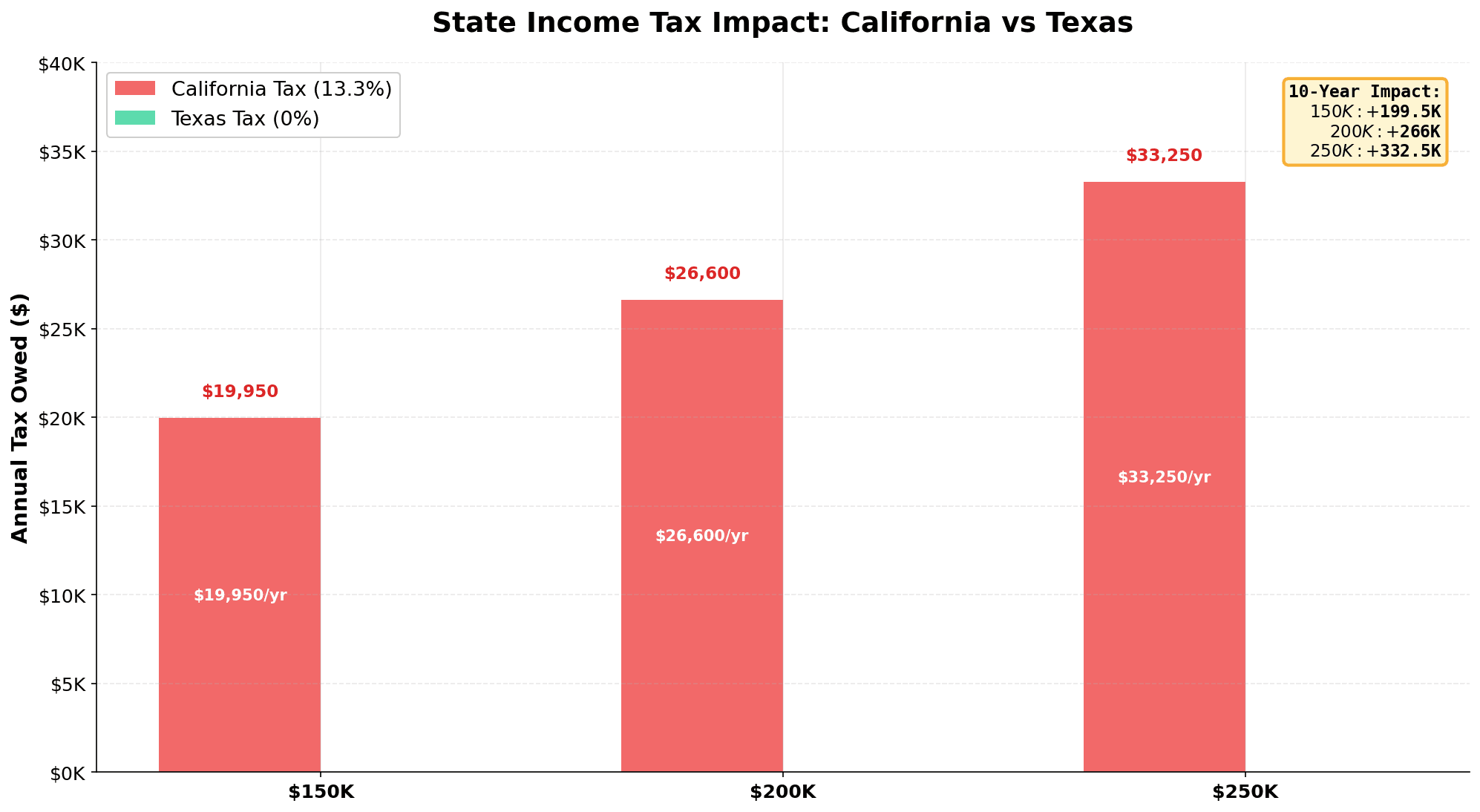

Even with Meta's aggressive location adjustment, the arbitrage still works because cost-of-living differences outpace the salary reduction. Plus, Texas has no state income tax, while California's top rate is 13.3% — that alone saves Jordan $26,600/year on his base salary.

The leverage is savings rate, not salary.

This is the insight that changes everything. In The Side Hustle Paradox, I've written about how someone earning $50,000 with a 50% savings rate reaches FI faster than someone earning $150,000 with a 20% savings rate. Geographic arbitrage takes that principle and weaponizes it: it raises both salary and savings rate simultaneously.

For FIRE seekers, this is the closest thing to a financial cheat code that exists. It compresses timelines by 4-10 years depending on your role, starting salary, and chosen destination.

Finding Your Arbitrage Opportunity: Which Roles Win

Not all professions benefit equally from geographic arbitrage. Location-dependent roles — sales (territory-based), healthcare, construction, local government — can't leverage this strategy. But knowledge work that companies value enough to pay premium rates?

The data is clear.

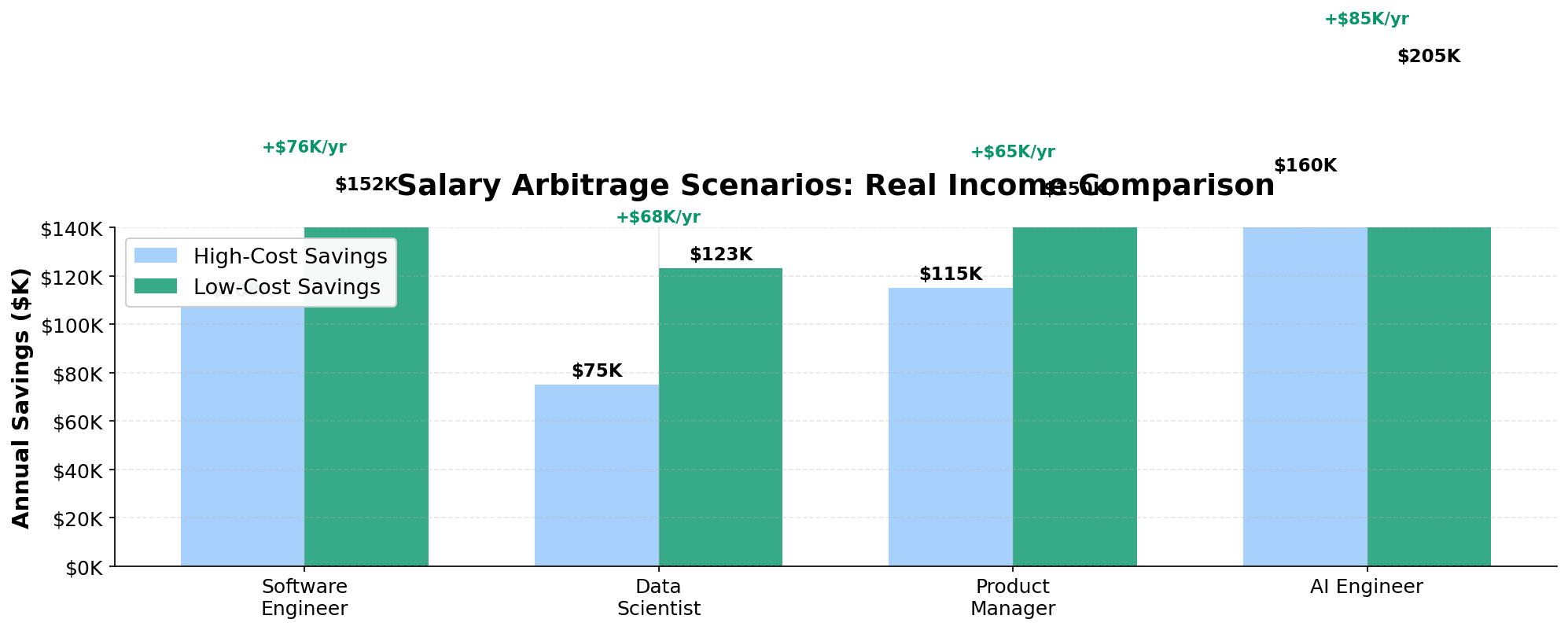

Software Engineering remains the gold standard. Remote software engineers earn 21.9% higher compensation than office-based counterparts on average. A Silicon Valley engineer earning $173,529 can move to Austin, keep $155,000+ of that (many remote-first companies don't adjust), and cut living expenses from $72,000 to $28,000. Real income gain: $67,000/year.

AI Engineers are experiencing the most dramatic arbitrage windows. The median AI engineer salary is $140,000–$185,000 base, with total compensation in the $200,000–$300,000 range at senior levels. Demand is still outpacing supply. Geographic arbitrage potential: 30-60% real income boost.

Data Science roles average $122,738 for remote positions. Mid-level to senior remote roles hit $141,000–$200,000. The role is inherently remote-friendly and companies hiring for data science are typically tech companies with remote policies in place. Arbitrage potential: 35-55% real income boost.

Product Management averages $159,405 for remote roles, with senior positions hitting $180,438–$211,699 total compensation. Product roles are increasingly remote-first; the best product managers often work distributed. Arbitrage potential: 25-45% real income boost.

Design (product/UX) is growing in remote adoption. The role is remote-friendly, and companies valuing good design pay premium rates. Arbitrage potential: 20-40% real income boost.

Finance roles — quantitative analysts, financial engineers, risk roles — often pay $150,000–$300,000+. Remote adoption is slower here, but fintech companies and trading firms increasingly offer distributed roles. Arbitrage potential: 30-50% real income boost.

What these roles share: they're knowledge-work, outcome-focused, and increasingly remote by default. Your work product is deliverables and code and analyses — not your physical presence. The companies hiring for these roles have already accepted distributed teams.

Roles that don't work for arbitrage: sales (territory-based compensation), operations (often requires office presence), HR/people roles, manufacturing/physical work, anything with local licensing requirements.

Your arbitrage potential depends on three factors: (1) your current salary tier, (2) how badly your target company competes for your skills, and (3) how much the cost-of-living difference actually is. If you're a mid-level software engineer earning $120,000 in Chicago ($77,000 COL), moving to rural Arkansas ($42,000 COL) saves you money but you won't negotiate a $180,000 SF salary as a no-name candidate. But if you're a senior engineer at a major tech company with a 5-year track record, remote-first companies will fight for you at top-of-market rates.

Start here: research your current market rate on Levels.fyi or Payscale. If remote versions of your role pay 20%+ more than office versions, you're in an arbitrage-friendly profession.

The Salary Negotiation Playbook for Location-Independent Work

Here's where most people fumble. They find a remote job, accept the offer, then mention they want to move to a low-cost area. By then, it's too late.

The right sequence is this:

Step 1: Research market rates by role, not geography. This is critical. Most people still think salary is geographically determined — a developer in SF earns more than a developer in Austin. That's true for office roles, where location limits the talent pool. But for remote roles, salary should be determined by market demand for the skill, not where you sit.

Use these tools to research:

- Levels.fyi: Real salary data submitted by employees, broken down by company, level, and total comp structure

- Payscale: Market rates with filtering for remote roles

- Blind: Anonymized employee salary posts (companies and levels clearly stated)

- LinkedIn Salary: Aggregate data for the role title

For a Senior Software Engineer role, you'll typically see $150,000–$250,000 base depending on company. That base is independent of where you do the work.

Step 2: Clarify the company's location policy before you get an offer. In your interview process, ask this directly: "I'm very interested in this role. Before we discuss specifics, can you clarify how you structure compensation for remote roles? Do you adjust salary based on where an employee lives, or do you use a standard market rate for the role?"

This gives you critical intelligence early. If they say "we pay location-independent rates," fantastic. If they say "we adjust by location," you need to know their tier system before you commit.

Step 3: Frame the negotiation around value, not geography. If they propose a location adjustment, your response should be:

"I appreciate the transparency. I want to discuss this thoughtfully. My understanding is compensation should reflect the value I deliver — my problem-solving ability, collaboration, and impact don't change based on zip code. Can we revisit this based on my track record and the market rate for this role?"

This reframes the conversation from "you're cheap because you live in a cheap place" to "you're valuable because of your skills."

Step 4: Propose creative structures if they won't budge on base. If a company insists on a location adjustment for base salary, you have options:

- Keep bonus and equity stable: Ask if the salary adjustment can apply only to base, while bonus and equity stay at full market rate. Equity especially is powerful because it grows tax-free for years.

- Performance review trigger: "I understand your policy. Would you agree to revisit my compensation in 12 months if I deliver [specific metrics]? If I exceed expectations, we return to market rate."

- Sign-on bonus to offset: "If you're adjusting base by $20,000, could you offer a $25,000 sign-on bonus?" The sign-on hits once; the salary adjustment compounds forever. But psychologically it feels like you "got paid."

Step 5: Get the location policy in writing before you accept. This is non-negotiable. Verbal agreements shift. Email the recruiter: "Before I sign, I want to confirm in writing: If I relocate from [current city] to [new city], my total compensation remains [X], correct?"

Real scripts that work:

When they bring up location-based adjustment: "I respect your policy. Before I decide, I'd like to understand the reasoning. Is this adjustment because you believe my value to the company changes based on where I live, or is it a cost-management practice? Because I'd argue my output — the code I write, the products I ship — is the same regardless of zip code. I'm happy to discuss how we can structure this fairly."

When they say "market rates in [low-cost city] are lower": "I understand that office roles in [low-cost city] might pay less, because you're competing with the local talent pool. But this is a remote role competing for talent globally. The market rate for a remote [role title] is [X], regardless of where the person sits. That's what I'm negotiating for."

When they refuse to budge: "I understand you have a firm policy here. Before I make my decision, can you share which other companies in our space use similar tiered models? I want to benchmark whether this is competitive." (Often, you'll find they're outliers.)

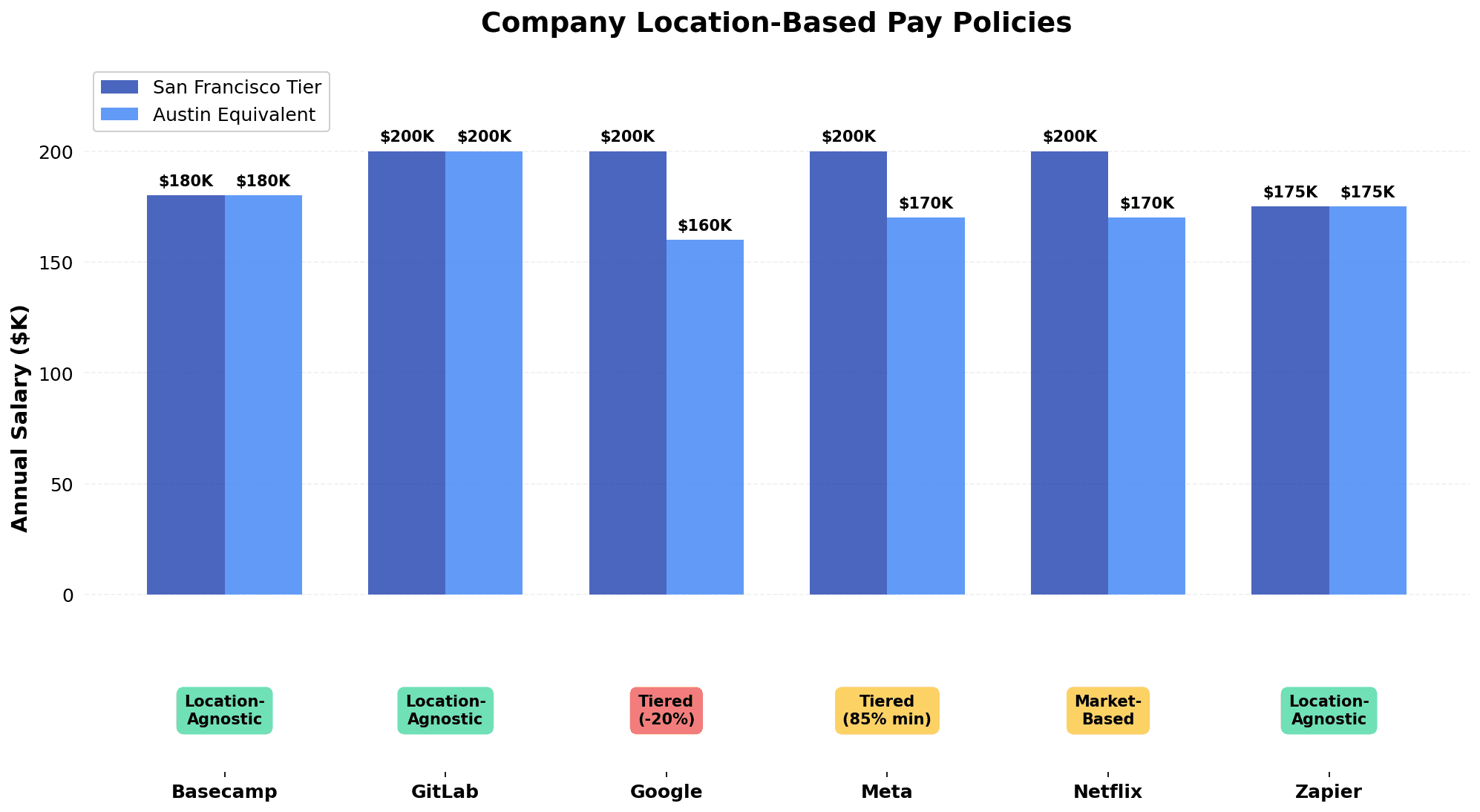

The key insight: 71% of companies use location-based adjustments. That means 29% don't. If a company won't pay market rate, find one that will. The remote-first companies — Basecamp, GitLab, Zapier, Automattic, RevenueCat — explicitly don't adjust for location. They're worth the outreach.

Navigating Employer Location-Based Pay Adjustments (The Hidden Trap)

If you negotiate successfully and keep your high-market salary, you've won. But here's the reality: 71% of companies will reduce your salary if you move to a low-cost area.

How do they do it? Tiered geography models.

Most companies use 3-5 salary tiers based on metropolitan area cost of living:

- Tier 1: San Francisco, New York, Seattle, Boston (100% of base)

- Tier 2: Austin, Denver, Chicago, Atlanta (85-90% of base)

- Tier 3: Secondary metros like Raleigh, Charlotte (75-80% of base)

- Tier 4: Non-metro or low-cost regions (70-75% of base)

- Tier 5: International (50-70% of base)

Meta's approach is less punitive than others — they never go below 85% of Bay Area minimum. Google is more aggressive, adjusting based on whether the remote location is >1 hour from an office and has lower labor costs. Microsoft applies tiered adjustment. Netflix uses individual "personal top of market" judgment, which is more opaque but potentially more negotiable.

The hidden trap: pay adjustments compound. If you're earning $200,000 and your employer cuts you to $170,000 (15% adjustment), that's $30,000/year × 30 working years = $900,000 of lifetime earnings lost. At 8% investment returns, that $900,000 would have grown to $7.2 million by retirement. A simple "15% location adjustment" is actually costing you millions in lifetime wealth.

How to mitigate:

-

Target the 29% of companies without location-based adjustments. GitLab, Basecamp, Zapier, Automattic, Gumroad, and a growing list of remote-first companies have eliminated location-based pay entirely. They pay at the 90th percentile of SF market rates globally. This is your escape hatch — if your current employer is aggressive on location adjustments, these companies will poach you.

-

Use pay transparency laws. If your target company is hiring into California, Colorado, Illinois, Massachusetts, New York, or Vermont, they're required to post salary ranges. That range is your negotiation anchor. "The posted range for this role in California is $150,000–$200,000. I'm proposing $160,000, location-independent. That's within the range and reflects market rate for the role."

-

**Negotiate adjustments away from base. If they insist on an adjustment, fight to keep it away from base salary. Have them adjust bonus or defer equity vesting instead. Base salary is the compounding engine — protect it ruthlessly.

-

Document performance and revisit annually. Get your company to commit to a review trigger: "If I exceed my performance targets, we return to market rate." Then exceed your targets. After six months of exceptional delivery, make the case: "The location-based adjustment was justified when I was onboarding. I've delivered [X], [Y], [Z]. Let's revisit the rate."

-

Keep leverage. The biggest negotiating power you have is being unwilling to accept the adjustment. If your company knows you can move to a remote-first alternative at $180,000, they're more likely to negotiate. Don't bluff — actually interview at those companies and get real offers. The threat needs to be credible.

The Risks and Realities You Need to Know

Geographic arbitrage is powerful, but it's not risk-free. Here are the real headwinds:

Return-to-office mandates are rising. In early 2026, 55% of Fortune 100 companies require full-time office attendance, up from 5% in 2021. Companies that hired you remote are walking it back. Amazon, JPMorgan Chase, AT&T, Goldman Sachs, Paramount, Home Depot — all demanding five-day office weeks. If your arbitrage strategy depends on a company staying remote, you're exposed.

Counter-reality: While RTO is rising, remote work is still more common in 2026 than it was in 2023. About 82% of companies offer some remote option; 72% have permanent remote policies. But the all-remote, location-irrelevant jobs are concentrated in tech, startups, and fintech — not in traditional enterprise. You need to target remote-first industries aggressively.

Cost of living isn't static. Many arbitrage articles assume costs stay flat. They don't. Southeast Asia inflation has been 6-8% annually. Vietnam and Thailand are 20-40% more expensive than they were three years ago. If you're banking on $1,200/month living costs in Chiang Mai, budget for $1,500–$1,700 in 18-24 months. Currency depreciation amplifies this — if the Thai Baht weakens 10% against the dollar, your $1,200 budget suddenly costs $1,320.

Tax complexity is real. Moving states adds multi-state withholding, nexus issues for your employer, and potential double-taxation. Moving countries adds visa requirements, currency risk, and international tax filing. Many remote workers underestimate this. A good tax professional ($2,000–$5,000/year) is non-negotiable if you're doing international arbitrage. For multi-state U.S. arbitrage, it's highly recommended.

Social isolation is underestimated. Arbitrage often means leaving your social network. Remote work compounds isolation (no office colleagues). If you're moving internationally, visa restrictions limit community integration. The "digital nomad" lifestyle is appealing on paper but exhausting for many people long-term. Arbitrage works best if you're genuinely comfortable being solo, building communities through online channels, and not needing physical proximity to friends and family.

International Arbitrage: Taking Salary Arbitrage Global

If U.S. arbitrage doesn't excite you, international options are even more dramatic.

Portugal (D8 Digital Nomad Visa): Income requirement €3,680/month. If you work remotely for a U.S. company and spend < 183 days/year in Portugal, you're not a Portuguese tax resident — you owe no Portuguese income tax. A $150,000 U.S. salary nets roughly €138,000 after federal U.S. taxes. In Portugal, that's untaxed. Cost of living in Lisbon: roughly $2,000/month comfortable ($24,000/year). Real savings: $126,000/year. Timeline to $1M: 8 years (vs. 13 years earning the same in a U.S. high-cost city).

Spain (Beckham Law): The Spanish "Regime for Inbound Expatriates" offers a flat 24% tax on employment income up to €600,000 for six years. Income threshold: €2,849/month (~€34,188 annually). On a $150,000 salary, your U.S. federal tax is ~$17,000, Spanish tax is ~$24,000 (€150K × 24%). Total tax: $41,000. Cost of living: ~€1,600/month ($20,800/year). Real savings: $88,200/year. This is attractive for mid-to-high earners.

Southeast Asia: Thailand, Vietnam, Cambodia cost $800–$1,500/month comfortable living. Visa options: Thailand's DTV (Digital Nomad Visa) costs ~$180 and lasts 180 days (renewable). No formal income requirement. If you earn $150,000 and spend $12,000/year living costs, you're saving $138,000/year. Reality check: inflation is real, currency risk is real, and visa rules change. Budget for costs to rise 5-7% annually.

The math for international arbitrage is extraordinary — but the risk is proportional.

Multi-year arbitrage phases (5-10 years) expose you to:

- Currency depreciation (if the Thai Baht weakens, your living costs spike)

- Inflation in developing economies (food, housing cost 6-8% more annually)

- Visa policy changes (Portugal, Spain, Thailand could tighten visa rules)

- Tax law shifts (what's tax-free today might not be tomorrow)

If you're doing international arbitrage, commit to a 2-year emergency fund in stable currency (USD or EUR in a U.S. account) and plan to revisit costs annually. A 5-10 year window is aggressive; 3-5 years is conservative. You're arbitraging not just location, but also currency stability and visa policy. Treat it as a tactic within a broader strategy, not a lifetime approach.

Building Your Arbitrage Career: Long-Term Strategy

Here's the truth arbitrage articles rarely say: arbitrage is a tactic, not a lifetime strategy.

You can't arbitrage forever. Eventually, costs rise in the destination. Visa rules change. You'll crave stability, community, or proximity to family. Companies continue to mandate return-to-office. Or you hit your FI number and stop optimizing for income.

The optimal arbitrage timeline is 5-10 years. Here's how the best arbitrage players structure it:

Years 1-3: Build skills and location flexibility. You're establishing yourself in a high-paying role — software engineer, data scientist, product manager. You're building a remote-first resume. You're contributing to open source. You're documenting results. You're learning which companies truly embrace remote work. This phase establishes your market value.

Years 4-7: Maximize savings and compound aggressively. You relocate to a low-cost area. You lock in a high-market salary (or use one of the 29% of companies that don't adjust). You hit a 70-80% savings rate. You funnel extra income into index funds and let compound growth do the work. This is the most important phase for FI — high savings rate + strong returns + young enough to benefit from 20+ years of compounding.

Years 8-10: Reassess and decide. After 5-7 years of aggressive arbitrage, you've likely hit or approached your FI number. Do you stay arbitrage-ing for another 3 years? Or do you pivot to location preference, lifestyle optimization, or reduced-hours work? This is the decision point.

Why this structure? Because:

- Skill builds earlier income: The best arbitrage play is a senior engineer at a top-tier remote company, not a junior. Spend your first 3 years building that seniority.

- Compound growth is strongest when there's time left: Saving $200,000/year for 3 years and investing it for 20 years beats saving $150,000/year for 20 years. Early, aggressive savings matter more than later savings.

- Arbitrage window closes: You'll get tired of low-cost living, miss your home country, want stability. 5-10 years is reasonable before you want out.

- Exit optionality matters: After 7 years of arbitrage and $1.2M saved, you can work part-time, take sabbaticals, or pursue passion projects. You've compressed your FI timeline by 10-15 years — buy yourself optionality with those years.

Skills that support arbitrage roles:

If you're not yet a software engineer or data scientist, how do you position yourself? The roles with highest arbitrage potential all require strong fundamentals:

- Software engineering: Learn a modern language (Python, Go, Rust), build projects, contribute to open source. If you're starting from zero, this takes 12-24 months of focused effort.

- Data science: Statistics, Python, SQL, machine learning. Start with online courses (Andrew Ng's ML course is foundational), build Kaggle projects, deploy models to GitHub.

- Product management: Start as a PM at a growth-stage startup (lower bar than FAANG). Focus on metrics, user research, shipping. After 2-3 years, you're competitive for remote PM roles.

- Design: Build a portfolio on Figma/Dribbble. Work on startups. Contribute to open-source design projects. Remote-first companies hire based on portfolio, not pedigree.

The key: arbitrage-friendly roles are skill-based, outcome-focused, and portfolio-demonstrable. You can prove your ability independent of where you went to school or what company you worked for.

Real Stories: How Geographic Arbitrage Shortened FIRE Timelines

Let me show you three actual (anonymized) case studies from the FIRE community.

Maya's U.S. Arbitrage: Data Scientist, SF → Austin

The setup: Maya, 28, was a data scientist at a major fintech company in San Francisco earning $155,000 base + $35,000 bonus + $50,000 equity vesting = $240,000 total comp. Her apartment cost $3,200/month. Annual expenses: $72,000 (30% of gross).

The move: After three years building her resume, the company went remote-first. Maya negotiated to stay in her role fully remote but needed to move for visa reasons. She relocated to Austin. She kept her $155,000 base (she argued value-delivery, not location). The company kept her bonus structure.

The numbers:

- Previous savings rate: 70% of $240K = $168,000/year

- New savings rate: 80% of $240K = $192,000/year

- Additional annual savings: $24,000

At 8% returns, that extra $24,000 annually for 10 years compounds to roughly $250,000 more. But the timeline compression is bigger: she moved her FI date 4 years earlier through a combination of lower costs + higher savings rate on the same income + Texas tax savings ($19,950/year on her income, since Texas has zero state tax vs. California's 13.3%).

Her FIRE timeline: From a baseline of ~11 years to FI, she compressed it to 7 years by making one move.

Ethan's International Arbitrage: Product Manager, NYC → Thailand

The setup: Ethan, 32, was a senior product manager at a NYC tech company earning $180,000 base + $60,000 bonus + $80,000 equity = $320,000 total comp. He was location-bound (in-office 3 days/week required). NYC life costs ~$85,000/year. His savings rate: 48% of gross = $155,000/year.

The opportunity: He interviewed at a fully remote Series-B startup (HQ: San Francisco) willing to pay $180,000 base + $30,000 bonus (no equity discount for location). He negotiated to relocate to Chiang Mai, Thailand. Company approved given his track record.

The numbers:

- Previous income: $320K, expenses: $85K, savings: $155K/year (48%)

- New income: $210K, expenses: $15K (rent $400/mo, food, coworking), savings: $195K/year (93%)

Despite a salary cut, his absolute savings increased by $40,000/year.

Timeline math:

- Previous: $1M FI number / $155K annual savings / 8% returns = 6.5 years to FI

- New: $1M FI number / $195K annual savings / 8% returns = 5 years to FI

- Compression: 1.5 years earlier to FI

Plus, his quality of life in Thailand was arguably better — more time for hobbies, lower stress, no commute, stronger community (digital nomad scene in Chiang Mai is robust).

Reality check: Ethan kept a 2-year emergency fund in USD and budgeted for 5% annual cost increases. After three years, his living costs had crept to $18,000/year (from $15,000), but he was still ahead of the NYC scenario.

Jordan's Domestic Arbitrage + Tax Optimization: Software Engineer, SF → Austin

The setup: Jordan, 29, was a software engineer at Meta in San Francisco earning $200,000 base + $50,000 bonus + $150,000 equity = $400,000 total comp. SF costs $72,000/year. Savings rate: 67% of gross = $268,000/year.

The challenge: Meta's location-based adjustment policy: moving to Austin would cut his base to $160,000, bonus to $40,000, equity to $120,000 = $320,000 (-20%). But Austin costs only $28,000/year.

The strategy: Instead of accepting Meta's offer as-is, Jordan interviewed at GitLab and Zapier (location-agnostic companies). He landed an offer from Zapier for $180,000 base + $20,000 bonus + $100,000 equity = $300,000 (location-independent). He countered to Meta with this offer.

Meta matched his base ($180,000) but kept the full equity package ($150,000 vesting) to retain him. Total: $380,000 — less than his SF rate, but significantly more than the location-adjusted offer.

The numbers:

- Original SF: $400K salary, $72K cost, $328K savings (82%)

- Meta's initial Austin offer: $320K salary, $28K cost, $292K savings (91%)

- Jordan's negotiated Austin offer: $380K salary, $28K cost, $352K savings (93%)

The real advantage: 10-year compounding. Saving $352,000/year at 8% returns for 10 years builds a $4.7M portfolio. His SF peer saving $328,000/year builds $4.4M. The difference is $300,000+ — entirely because Jordan negotiated creatively and didn't accept the initial location-based cut.

Tax optimization bonus: Texas has zero state income tax. Jordan saved an additional $23,400/year compared to California's 13.3% rate on his $180,000 base.

Jordan's FIRE timeline: Not materially different from SF (both roughly 7-8 years to FI), but with dramatically better quality of life (Austin vs. SF cost-of-living differences) and higher absolute net worth ($4.7M vs. $4.4M at FI).

Is Geographic Arbitrage Right for You? (Decision Framework)

Arbitrage works for some people and creates stress for others. Here's how to know if it's right for you:

Arbitrage works best if you:

- Value financial independence over immediate lifestyle. You're willing to live modestly for 5-10 years to buy optionality for the next 40 years.

- Are genuinely comfortable with location flexibility. You don't have deep roots in your current city or family obligations anchoring you to a location.

- Have strong remote-work skills. You're self-directed, communicate clearly in writing, build relationships without office proximity, and manage your own time ruthlessly.

- Can handle tax and visa complexity. Or you're willing to hire someone ($2,000–$5,000/year) to handle it.

- Prioritize savings rate over convenience. You'll cook at home, use public transport, and skip lifestyle creep for years.

- Are early enough in your career to build arbitrage-friendly skills. You're 22-35 with time to develop expertise in software engineering, data science, or product roles.

Arbitrage creates stress if you:

- Are deeply rooted in your location. Family, partner, close friends, community — these anchors matter more than financial optimization. Don't arbitrage away your life.

- Need in-person work environment for mental health. Some people thrive remote; others wither. If you're the latter, arbitrage isn't worth the psychological cost.

- Intolerant of tax complexity. If tax forms and multi-state filing stress you out, international arbitrage is genuinely difficult.

- Have family responsibilities. Partner earning local income, kids in school, aging parents nearby — these reduce location flexibility.

- Need lifestyle stability. If you value consistency, community, having an apartment with real furniture, and regular routines, the arbitrage lifestyle (frequent moves, visa uncertainty, currency risk) is draining.

Decision framework:

- Do you have access to remote-friendly roles? (Profession check: are you a software engineer, data scientist, product manager, or similar?)

- Are you willing to relocate? (Location flexibility check: no strong geographic anchors?)

- Can you negotiate without location-based adjustment? (Negotiation check: can you target remote-first companies or argue your value?)

- Is the cost-of-living difference meaningful? (Math check: is the destination >30% cheaper than your current city?)

- Can you handle 5-10 years of modest living? (Psychology check: are you genuinely comfortable with this lifestyle?)

If you answer yes to 4-5 of these, arbitrage is probably right for you.

If you answer no to 3+, focus on local income growth and investment returns instead. There's nothing wrong with earning $150,000 in an expensive city and building wealth through high savings rate and compound growth. Arbitrage accelerates the timeline, but discipline + time also works.

Integration with Your FIRE Strategy

Geographic salary arbitrage is one lever in the broader FIRE toolkit. Here's how it fits:

The FIRE Movement teaches the 25× rule: your FI number is 25× your annual spending. Arbitrage directly reduces that number. If your spending drops from $85,000 to $15,000, your FI target shifts from $2.125M to $375,000 — a 5.7× reduction. Same income, different lifestyle = dramatically faster freedom.

Wealth = Time × Money × Discipline reminds us that compound growth is the engine. Arbitrage increases the "Money" component (higher salary, higher savings rate) and gives compound growth more runway. A 5-year arbitrage phase is a decade of compounding you don't have to wait through.

The Side Hustle Paradox warns about complexity and burnout. Geographic arbitrage is a side hustle of sorts — it requires negotiation skill, tax planning, visa management. But unlike traditional side hustles, it doesn't add hours to your day. It just redirects your primary income more effectively.

Time Freedom Over Retirement captures the real goal. Arbitrage isn't about living like a miser forever. It's about compressing the accumulation phase so you can buy optionality — work part-time, take sabbaticals, live wherever you want for free — for the next 30-40 years.

If you're pursuing FIRE, arbitrage is one of your most powerful tools. Not mandatory, but worth serious consideration if the framework fits your situation.

Your Action Plan: Getting Started

If geographic arbitrage interests you, here's a concrete 90-day plan:

Month 1: Research and skill-building

- Audit your current role. Is it remote-friendly? Does it fit the arbitrage-potential list (software engineering, data science, product, design, finance)?

- Research market rates on Levels.fyi, Payscale, Blind. What does your role pay in remote versions?

- If you're not yet in an arbitrage-friendly role, commit to learning (Python, product management, UX design). Online courses exist; projects are doable.

- List 5-10 remote-friendly target destinations. Research cost of living (Numbeo, Expatistan), visa requirements, tax implications.

Month 2: Positioning

- Update your LinkedIn and GitHub. Highlight remote work experience and deliverables.

- If you're early-career, contribute to open-source projects. Build portfolio work.

- Research companies on the "location-agnostic pay" list (GitLab, Basecamp, Zapier, Automattic). Follow them. Understand their culture.

- If you're currently employed, research whether your company offers remote work. Get it in writing if they do.

Month 3: Negotiation preparation

- Identify your target salary. Use market rate research from month 1.

- Draft the negotiation email/script. Practice asking about location policy before you get an offer.

- Research tax implications for your target destination. If international, consult a tax professional ($2,000-$5,000 investment now saves 10x that in complexity).

- If you're currently employed and considering a move, decide: do you negotiate a location change with your current employer, or do you interview externally?

After month 3: Execute

- Apply to 10-15 remote roles at companies with known location-agnostic or high-percentage policies.

- Interview. Ask about location policy in every conversation.

- Negotiate. Use the scripts and frameworks above.

- Move. Once you've secured the role and clarified the location policy, execute the relocation.

- Invest immediately. Any savings from geographic arbitrage go directly into index funds. Don't lifestyle-inflate.

The window for geographic arbitrage is narrowing (RTO mandates are rising, location-based pay is spreading). If it fits your situation, acting in the next 6-12 months makes sense. The longer you wait, the fewer truly remote-first companies exist to negotiate with.

Final Thoughts: Arbitrage as a Tactic, Not a Lifetime

Geographic salary arbitrage is powerful precisely because it's temporary. You're not going to live on $15,000/year forever. You're not going to stay remote while your industry slowly mandates return-to-office. You're not going to move countries every three years.

You're doing it strategically: 5-10 years of aggressive arbitrage, high savings rate, compound growth — then pivoting to whatever comes next. Maybe that's Coast FIRE (you've hit critical mass; you stop contributing and let growth do the work). Maybe it's phased retirement (you work part-time in your hometown, location preference regains priority). Maybe it's sabbaticals and travel (you've bought the freedom to do it).

The point is: arbitrage is a cheat code in the FIRE equation, but cheating only works if it's temporary and strategic.

If you're disciplined, if the framework fits, if you can execute the negotiation: geographic salary arbitrage can compress your FIRE timeline by 5-10 years. That's not incremental. That's transformational.

The math is clear. The opportunity exists. The only question is whether you'll take it.

Next week: We're diving deep into the tax implications of multi-state and international remote work. If you're seriously considering arbitrage, bookmark the MFFT blog for the breakdown on Roth conversions, state tax nexus issues, and visa strategy. In the meantime, start mapping your target location and researching market rates — the groundwork matters.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.