Prediction Markets: Why 69% of Polymarket Users Lose

Sarah, a 24-year-old UX designer in Brooklyn, deposited $200 into Kalshi after a viral tweet during The Masters. By Sunday she had doubled it on a McIlroy contract. Six weeks later she was down $1,600, checking the app forty times a day. She still calls it "research-y entertainment." The bank statement does not.

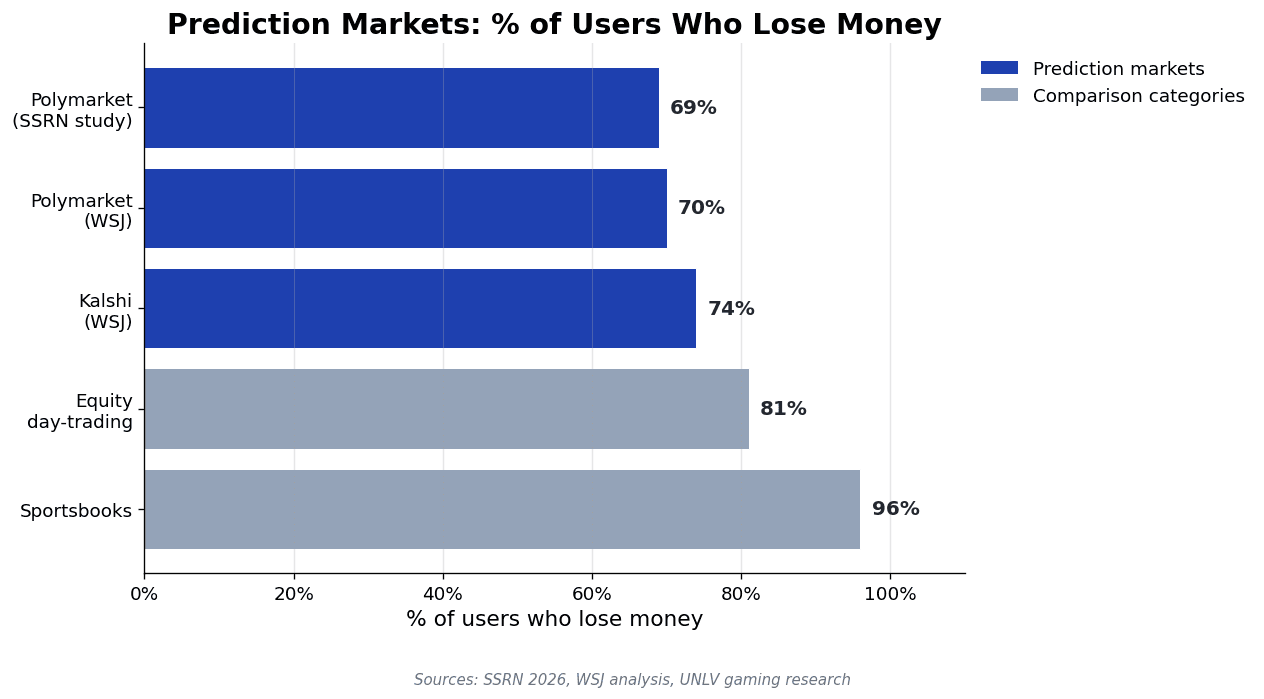

Sarah is the median. Prediction markets look like the slick, intellectual cousin of sports betting — graphs, probabilities, vocabulary borrowed from finance. The data is uglier than anyone realizes. A peer-reviewed study covering 588 million trades and $67 billion in volume found 69% of Polymarket accounts have lost money since 2022. WSJ found a similar number on Kalshi: 70-74% unprofitable, losers outnumbering winners 2.9 to 1.

This is the article I wish every Gen Z reader had open before downloading their first prediction-markets app. We will walk through the math, why the platforms extract from amateurs, how to redirect the dopamine, and a 30-day reset if you are already in the hole.

The $1 Trillion Casino No One Is Calling a Casino

Combined Polymarket and Kalshi volume went from $15.8 billion in 2024 to $63.5 billion in 2025. April 2026 monthly volume was running at $8.6 billion. Industry forecasts project the segment to cross $1 trillion by 2030.

That is not a niche. That is a parallel financial system being built in front of regulators who cannot decide what to call it.

Fortune called the moment Gen Z's "Joe Camel" — slick branding, meme-fluent marketing, low age friction, predictable losses. CNN reported that 18-21-year-olds use prediction markets specifically because state gambling laws shut them out everywhere else. The CFTC chair has called prediction markets and sportsbooks "two separate things." The American Gaming Association estimates states have lost about $1 billion in tax revenue to this loophole.

The question: if prediction markets are this big and academic-sounding, why does every independent data set say almost everyone ends up worse off?

The Brutal Numbers: 69% of Polymarket Accounts Lose Money

Let's stay with the data because the data is where the floor falls out.

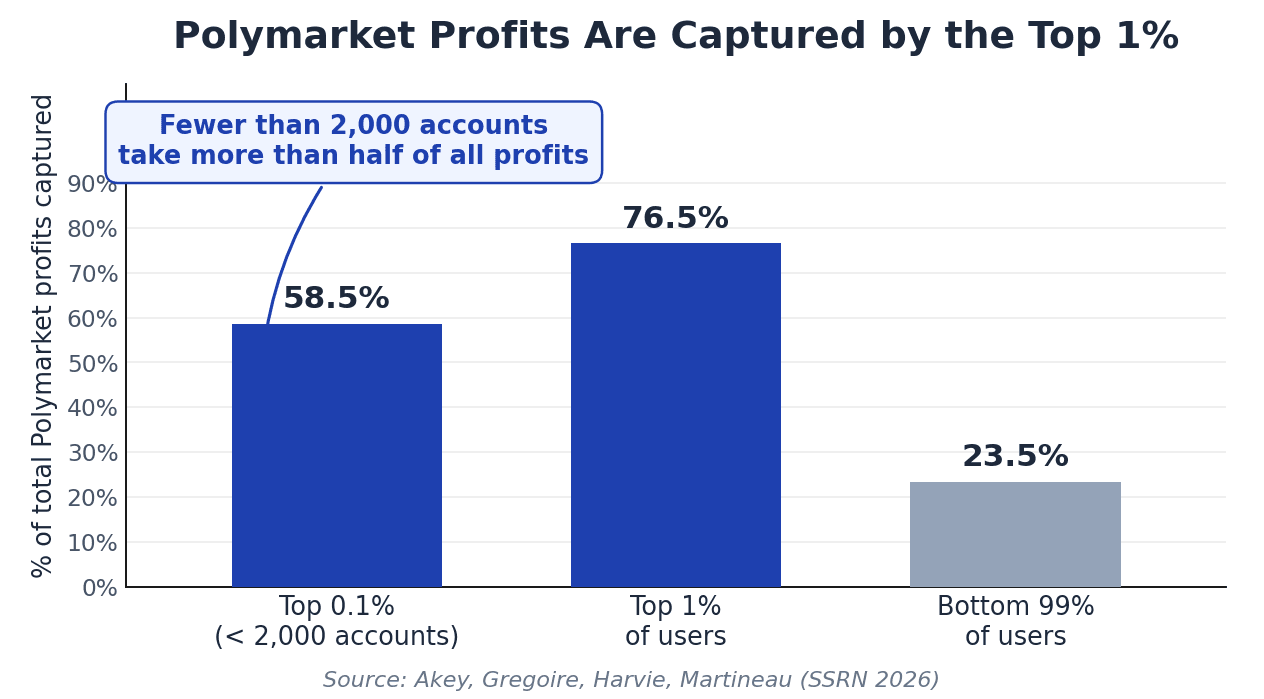

The single most rigorous study is from Akey, Grégoire, Harvie, and Martineau — a 2026 SSRN paper covering every Polymarket transaction since inception. Their headline: 69% of accounts have lost money. The top 1% of users captured 76.5% of all profits. The top 0.1% — fewer than 2,000 accounts out of roughly two million — took home 58.5% of every dollar made.

WSJ's on-chain analysis got an even sharper ratio: 0.1% of accounts captured 67% of all profits. Bloomberg reported that more than 100,000 Polymarket accounts have each lost at least $1,000 since January 2025.

Kalshi is worse. The same WSJ investigation found about 74% of Kalshi traders are losing money. "Mention markets" — short-horizon contracts on whether a phrase will get referenced in a window — paid out only about 40% of the time at 50% implied odds. Average loss: -11% per bet. UNLV puts most Vegas slot machines at roughly -7% per spin. Kalshi's mention market is mathematically worse than a slot.

| Vehicle | % of Users Who Lose | Expected Return |

|---|---|---|

| Polymarket (SSRN, 2026) | 69% | Negative for 99% of users |

| Polymarket (WSJ analysis) | 70% | Bottom 99% net -$131M |

| Kalshi (WSJ) | 74% | -11% (mention markets) |

| Vegas slot machine (UNLV) | ~95% | -7% per spin |

| Sportsbook bettors | 96% | -5% median ROI |

| Equity day-trading | 81% | Negative median |

| S&P 500 index, 30-year hold | < 5% (any 30Y window) | +8% nominal avg |

One more uncomfortable number. Roughly 5% of wallets — mostly bots — generated 75% of all Polymarket trading volume since January 2025. The bottom 95% place 56% of their trades at extreme prices (under 10 cents or over 90 cents). The top 0.1% only place 28% of theirs there. Amateurs buy almost-certain outcomes that pay almost nothing. The pros price them.

Why Gen Z Is Drawn In: Financial Nihilism Meets Slick Marketing

If the math is this bad, why is the user base exploding? Because the math is not what gets you in. The feeling is.

Northwestern Mutual's 2026 Planning & Progress Study surveyed 4,375 Americans. 80% of Gen Z and 75% of millennials using prediction markets, sports betting, crypto, or options said the same thing: they feel financially behind and believe these are faster than traditional methods. Americans now believe they need $1.46 million to retire comfortably. Forty-six percent do not expect to be ready.

So when a 24-year-old compares a 4% real return on a Roth IRA to a viral screenshot of somebody who turned $400 into $33,000 on a 12-cent contract, the boring math loses every time. Bloomberg and the World Economic Forum called it financial nihilism: the belief that compounding is a myth and the only way out is a lottery ticket with extra steps.

I covered the parent thesis in The Anti-Influence Movement: Why Smart People Are Rejecting FinTok Hype. Prediction markets are the sharpest, most concentrated expression of it. They take a real psychological wound — being behind — and sell you the most efficient possible way to fall further behind.

The marketing knows what it is doing. Kalshi and Polymarket built growth teams that speak in memes — ironic ad copy, influencers who do not look or sound like financial professionals. The Markkula Center for Applied Ethics points out Gen Z's gambling-addiction rate runs roughly three times higher than older cohorts. A 2025 survey found 37% of Gen Z describe themselves as addicted to gambling — 14 points above the all-ages average.

For a deeper look at how FinTok content warps Gen Z money beliefs, I broke down three concrete mistakes in FinTok Money Myths: 3 Mistakes Gen Z Women Make.

The Math: Why Prediction Markets Are Worse Than Index Funds

I want to make the cost concrete. Not as a percentage. As a dollar number you can feel.

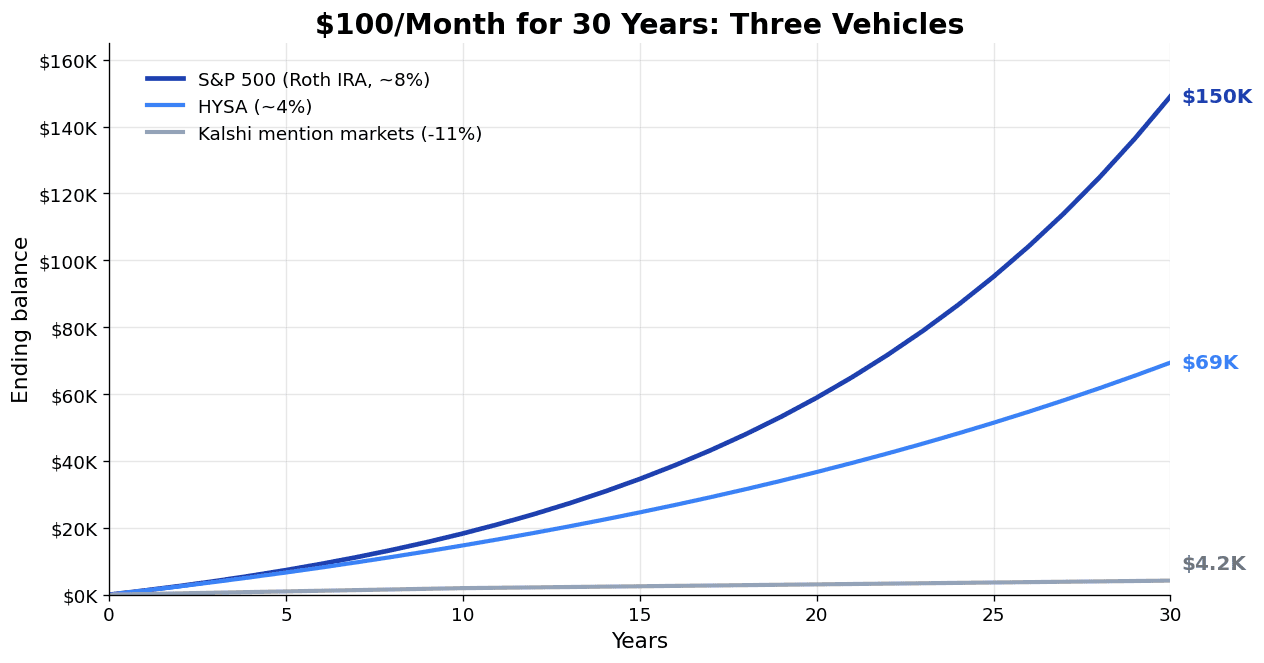

Take a 22-year-old with $100/month to put somewhere. Three choices: a Kalshi mention-market habit, a high-yield savings account, or an S&P 500 index fund in a Roth IRA. Same paycheck, three different vehicles.

| Vehicle | Expected Return | Year 10 | Year 30 |

|---|---|---|---|

| Kalshi mention markets | -11% per bet | ~$1,950 | ~$4,200 |

| HYSA at 4% | +4% | ~$14,725 | ~$69,000 |

| S&P 500 (Roth IRA) at 8% | +8% nominal | ~$18,300 | ~$150,030 |

That last column is the entire game. Same hundred bucks a month, same 30 years, ends up at $4,200 or at $150,030. Same person. Same income. The vehicle does the work — or eats the work.

Defenders will say the average user is not betting their savings rate. Fair. But the SSRN data shows only the cohort trading more than $500,000 in volume is profitable (median +2.6%). The under-$100 cohort sits at -26.8%. AI bots tested on Kalshi lost 16-30.8% over 57 days. If trained models lose, your weekend instinct on NBA storylines is not the edge.

The kicker is the liquidity-taker tax. Winners post limit orders and wait for their price. Losers take market orders and pay whatever is on offer. That spread is the house edge — and the house is not the platform. It is the 823 accounts that each netted over $100,000 by being on the other side of every retail click.

The Addiction Problem: Why Gen Z Is at 3x the Risk

This is the section where being honest matters more than being clever.

Prediction markets exploit the same neurological mechanism as slot machines. Vanderbilt dopamine research shows the brain releases its biggest dopamine response when a reward is uncertain, not when it is guaranteed. The variable-ratio reinforcement schedule casinos engineered into slots is the most addictive schedule known to behavioral neuroscience. Every "Yes" contract at 50/50 odds is a slot pull dressed in finance vocabulary.

What makes Gen Z uniquely vulnerable is wiring plus exposure. The dopamine pathways are more sensitized in users raised on social-media variable-reward feeds. The brain that grew up on TikTok is the same brain a prediction-markets app is targeting.

Warning signs, in plain English:

- You check the app more than 10 times a day.

- You have lied to a partner, parent, or friend about how much you have lost.

- You have used a credit card, BNPL, or a paycheck advance to fund a deposit.

- A loss makes you immediately want to place another bet to "win it back."

- You stopped contributing to a 401(k), Roth IRA, or HYSA but kept the prediction-markets habit going.

Two or more is not "I like markets." That is gambling. 1-800-GAMBLER exists for a reason. The same pattern that drove an extra credit-card balance in The Buy Now, Pay Later Trap is the one driving the next deposit into Polymarket. Different vehicle. Same wound.

Prediction markets are explicitly not covered by the consumer protections that exist around traditional gambling. No cross-platform self-exclusion registry. No default deposit limit. The "we are a derivative, not a casino" defense is what makes them more dangerous, not less.

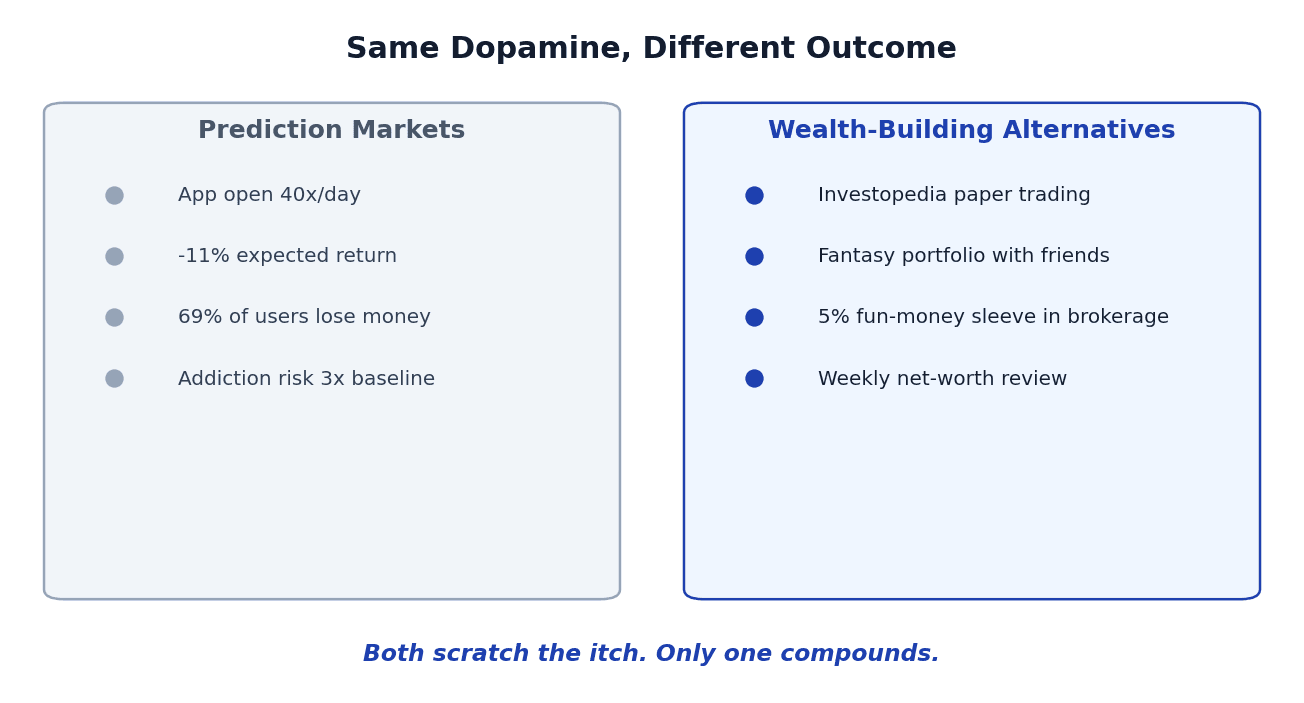

The Redirect: Same Dopamine Hit, Build Real Wealth Instead

The all-or-nothing approach does not work. "Just stop" is the worst financial advice ever given. Brains do not stop wanting things. They redirect.

Paper-trading apps. Investopedia Stock Simulator, Webull paper trading, and thinkorswim's paperMoney are free. Same "place a bet, watch it move, feel the hit" experience with virtual money. Most people who paper-trade for 90 days find their real win rate sits at 40-45% — exactly the SSRN math. Better to learn on play money.

A fantasy-portfolio league with friends. Six people, five stocks each at the start of the year, smallest portfolio buys dinner. Bragging rights is the neurological hit you were chasing anyway.

The hard-capped 5% fun-money sleeve. Put 95% of investable assets into boring index funds and a savings buffer. Take 5%, no more, into a brokerage where you can pick individual stocks or options. The rule: the 95% never funds the 5%. When the sleeve goes to zero, it stays zero until next year.

Replace the daily check with a weekly review. A daily Polymarket check is a dopamine vending machine. A weekly net-worth review is the same activity — looking at numbers — but the numbers represent your actual future. Most people who switch report the MFFT dashboard provides the same psychological payoff within a month.

The point is not to be a monk. Keep the part of you that likes the action without letting it eat the part of you that wants to retire.

The 30-Day Prediction Markets Reset Plan If You Are Already In Deep

If you recognized yourself, here is the playbook. Every reader I have run this with says step one is the hardest.

Day 1-3: Tally the damage. Open every prediction-markets account. Get to the lifetime profit-and-loss screen. Polymarket: Profile → Activity → Total P&L. Kalshi: Profile → Statistics. Write the number down. The reader I worked with last month thought he was "about even." He was down $7,400. Until you see it on paper, you will rationalize.

Day 4-7: Self-exclude. Both platforms have account-closure flows; they are buried but they exist. Kalshi: Settings → Account → Close account. Polymarket: Settings → Security → Close account / withdraw funds. Withdraw the balance to a checking account, not a card. The card path makes re-deposit too easy.

Day 8-14: Redirect automatically. Whatever you were spending on prediction markets per month, set up an auto-transfer for the same amount to a Roth IRA or high-yield savings account. Use the auto-transfer feature, not your willpower. If you do not have an emergency fund yet, start there — I made the case in Emergency Fund 2026: Why 59% of Americans Cannot Cover a $1,000 Emergency.

Day 15-21: Replace the daily check. Delete the apps. Move icons off your home screen if you cannot delete. Replace 30-40 daily checks with one weekly 15-minute review of net worth, savings rate, and one dollar amount you are tracking.

Day 22-30: Find the community substitute. A big part of the prediction-markets pull is the Discord, the X group chat, the screenshots in your friend feed. Replace it. Bogleheads forums, the r/FIRE subreddit, a local FI meetup, even a two-person accountability text with one friend who also wants to fix this. Isolation is what makes relapse easy.

End of 30 days, be honest about whether the urge has reduced. If not, the next step is not another budgeting tool. It is professional help.

If You Are Already Investing The Boring Way

A note for the reader who is not in trouble — who already auto-invests in VOO every month and feels like a dork because their friends post 10-bagger Polymarket screenshots.

You are correct. You are not the dork. They are the survivorship-bias sample.

Every viral prediction-markets screenshot is, by definition, drawn from the 1% of accounts that profited. The 1.4 million silent losers do not post. The 100,000+ accounts down more than $1,000 do not screenshot the red number.

The math is on your side. Over any rolling 30-year window in S&P 500 history, the probability of a loss is essentially zero. Over any single day, it is roughly 47%. The prediction-markets app is selling you the worst version of that probability — short-horizon, high-friction, negative expected value — while telling you it is the smart-money version. The data says the opposite.

If you want the foundational read on why boring works, Investing Made Simple is where I would start a friend who asked. Thesis unchanged from 2015 to 2026: time in the market, low fees, broad diversification, automated contributions. Everything else is decoration.

Bottom Line: The House Always Wins — And the House Is the Top 1%

Pull the whole article into one screen.

| What the data says | What the marketing says |

|---|---|

| 69-74% of users lose money | "Smart money trades here" |

| Top 1% capture 76.5% of profits | "You could be next" |

| Mention markets: -11% expected | "Better than the news" |

| 5% of wallets = 75% of volume (bots) | "Wisdom of the crowd" |

| 80% of Gen Z users feel "behind" | "Catch up fast" |

| AI bots lose 16-30% over 57 days | "Edge over the market" |

| Gen Z gambling addiction: 3x baseline | "Just entertainment" |

The honest summary: prediction markets are a wealth-transfer machine from amateurs to a few thousand professional liquidity providers. Every dollar you put in at a market order is roughly an 11-cent gift to whoever posted the limit order on the other side.

You can love information aggregation as a concept without confusing it with a personal investment strategy. Prediction markets are useful for forecasting things polls miss. That is the use case: read the prices, do not trade them.

If you take one action today, make it this: redirect whatever monthly amount was going to a prediction-markets account toward a Roth IRA or your emergency fund, and automate the transfer before you can change your mind.

The first paycheck that goes to an index fund instead of a Polymarket deposit is the moment you stopped being the liquidity and started being the compound. The 22-year-old who makes that swap, on $100/month, ends up with roughly $150,000 at age 52 instead of $4,200. Just arithmetic.

If you want a privacy-first home for the boring math, the MFFT net-worth tracker is built for exactly this redirect. No signup gate, no upsell. Track the real number going up. That is the dopamine hit that actually pays.

Email me at dennis.vymer@myfinancialfreedomtracker.com if you tried the 30-day reset or are mid-decision on deleting the apps. I read every reply.

The house always wins. Stop being the house's customer.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.