CD Ladder Strategy 2026: Lock In Yields Before Fed Cuts

New to personal finance and managing your savings?

If you're just starting out, these three articles will give you the foundation this one builds on:

- How to Start a Budget — because you can only ladder cash you've actually freed up.

- The 2026 Emergency Fund — what stays liquid, what's allowed to lock up.

- Wealth = Time × Money × Discipline — the math that explains why a small yield gap matters.

Maya opens her bank app on a Tuesday morning. Her high-yield savings account, which paid 4.20% when she opened it last summer, now shows 3.95%.

A small green banner at the bottom reads: "Your variable rate has been updated."

She refreshes. The number doesn't change.

Three months later, in May, it drops again — to 3.75%. Same banner. Same casual tone. No email. No warning. Just a quiet trim of the yield she had been treating like a fixed feature of her financial life.

Maya is not unlucky. She's just on the receiving end of the 2026 rate-cut cycle. The Federal Reserve cut its policy rate three times to end 2025 (a total of 75 basis points), bringing the federal funds range to 3.50%–3.75%, and most market forecasts call for two to three more quarter-point cuts before this year is out. Every cut passes through to high-yield savings APYs within a few weeks. The savings account that paid for half of last summer's vacation is going to pay quite a bit less for next summer's.

There's a fix for this — one that's been hiding in plain sight in your local bank's marketing materials for decades. It's called a CD ladder, and 2026 is the year it stops being a boring suggestion and starts being the smartest move most savers won't make.

This article walks through what a CD ladder is, the three designs that fit different lives, the real math against a falling-rate HYSA, and the three mistakes that turn a good strategy into a small disaster. By the end you'll know whether you should build one, which design fits you, and how to set it up in about 30 minutes.

Why Your Savings Yield Just Started Dropping — and Will Drop Again

Here's the short version of the macro picture, because the strategy only makes sense once you understand the gravity it's working against:

| Rate | End of 2024 | End of 2025 | Mid-2026 Forecast |

|---|---|---|---|

| Fed funds target | 4.25%–4.50% | 3.50%–3.75% | 2.75%–3.25% |

| Top HYSA APY | ~5.00% | ~4.50% | ~3.50%–3.75% |

| 1-year CD APY (top quartile) | ~4.85% | ~4.20% | ~3.50% |

The Fed has been cutting because inflation has cooled enough that policymakers can pull the brake off the economy. That's mostly good news. The side effect is that anything paying a variable yield on cash will pay less every quarter, like clockwork, until the cycle is over.

On $20,000, a 100-basis-point drop in HYSA yield costs roughly $200 per year in pre-tax interest. On $50,000, it's $500. That's the cost of doing nothing.

The strategy below doesn't make rates go back up. It just lets you keep most of today's rate, on most of your money, for most of 2026 and 2027.

What a CD Ladder Actually Is (Without the Bank Marketing Speak)

A certificate of deposit (CD) is a fixed-term, fixed-rate savings product. You hand the bank $X today, and the bank promises to give you back $X plus an agreed amount of interest on a specific date — six months, a year, three years, five years from now. You can't add to it. You can't easily withdraw early without paying a penalty. In exchange for that lock-up, you get a rate that doesn't move.

That's the whole point in a falling-rate environment. A 1-year CD opened today at 4.10% pays 4.10% for the full year — even if the HYSA next door drops to 3.25% by November.

A CD ladder is just a CD strategy where you split your deposit across several maturities so they expire at staggered intervals. Picture five $4,000 CDs maturing in 1, 2, 3, 4, and 5 years. Every year, one rung matures. You either reinvest it at the new 5-year rate (rolling the ladder forward) or you spend it.

Two things happen at the same time:

- Most of your money stays locked in at the original, higher rates — protecting you from falling APYs.

- A predictable slice becomes accessible every year — protecting you from being totally illiquid.

That dual protection is the entire reason the structure exists. A single 5-year CD locks 100% of your money for 60 months. A pure HYSA locks none of it but exposes 100% to the rate cuts. A ladder splits the difference on purpose.

The Three CD Ladders Everyone Should Know

There isn't one "correct" ladder. There are three classic shapes, and they suit very different financial situations. Pick the one whose liquidity matches yours, not the one with the highest headline rate.

1. The Short Ladder — 3 / 6 / 9 / 12 Months

Split your deposit into four equal chunks across CDs maturing in 3, 6, 9, and 12 months. When the 3-month CD matures, reinvest it into a new 12-month CD. Three months later, repeat. After a year of doing this, every quarter you'll have a 12-month CD maturing.

- Liquidity: very high — you get a maturity every 90 days.

- Average locked yield: typically the lowest of the three, because short CDs pay less.

- Best for: savers who think they might need the cash within a year (a planned down payment, a wedding, tuition).

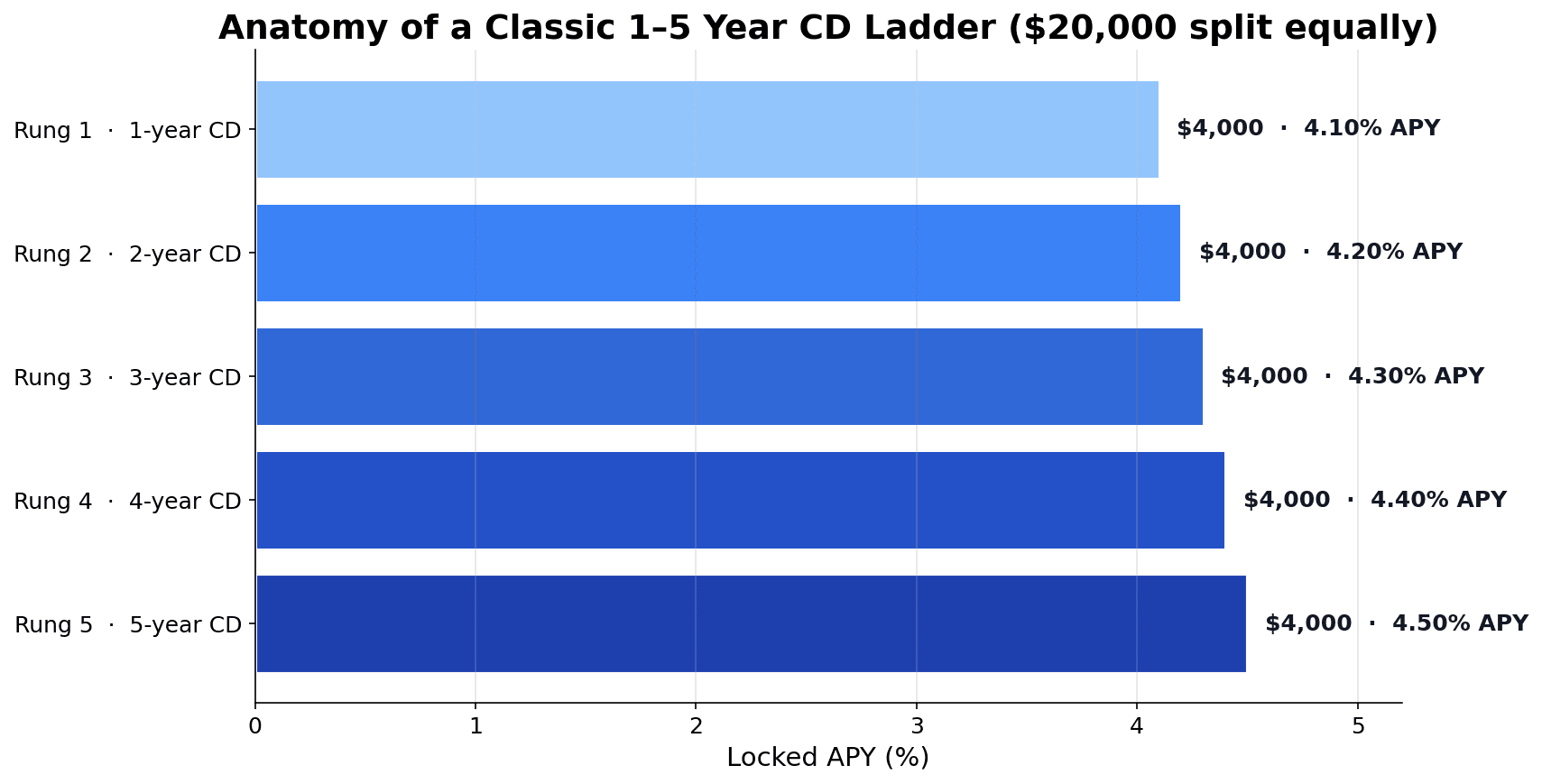

2. The Classic Ladder — 1 / 2 / 3 / 4 / 5 Years

Split into five equal chunks across CDs maturing in 1, 2, 3, 4, and 5 years. Each year, the maturing rung gets reinvested into a new 5-year CD. After five years of rolling, every rung is a 5-year CD — but a different one matures every year.

- Liquidity: moderate — one rung per year.

- Average locked yield: typically the highest of the three, because the 4- and 5-year rungs lock in long-term rates.

- Best for: medium-term savers, semi-retirees, anyone treating cash as a permanent allocation rather than a holding pen.

3. The Barbell Ladder — Short + Long, Skip the Middle

Put roughly 40% into a 12-month CD and 60% into a 5-year CD. No middle rungs. The short side gives you fast access; the long side captures the highest available yield.

- Liquidity: fair — most of your money is locked, but the short side is large enough to absorb most surprises.

- Average locked yield: between the short and classic ladders, depending on the curve.

- Best for: savers who want a structural barbell — emergency-adjacent cash plus a long-dated yield anchor — without the bookkeeping of five rungs.

The Math: How Much More You'll Earn vs. Leaving It in HYSA

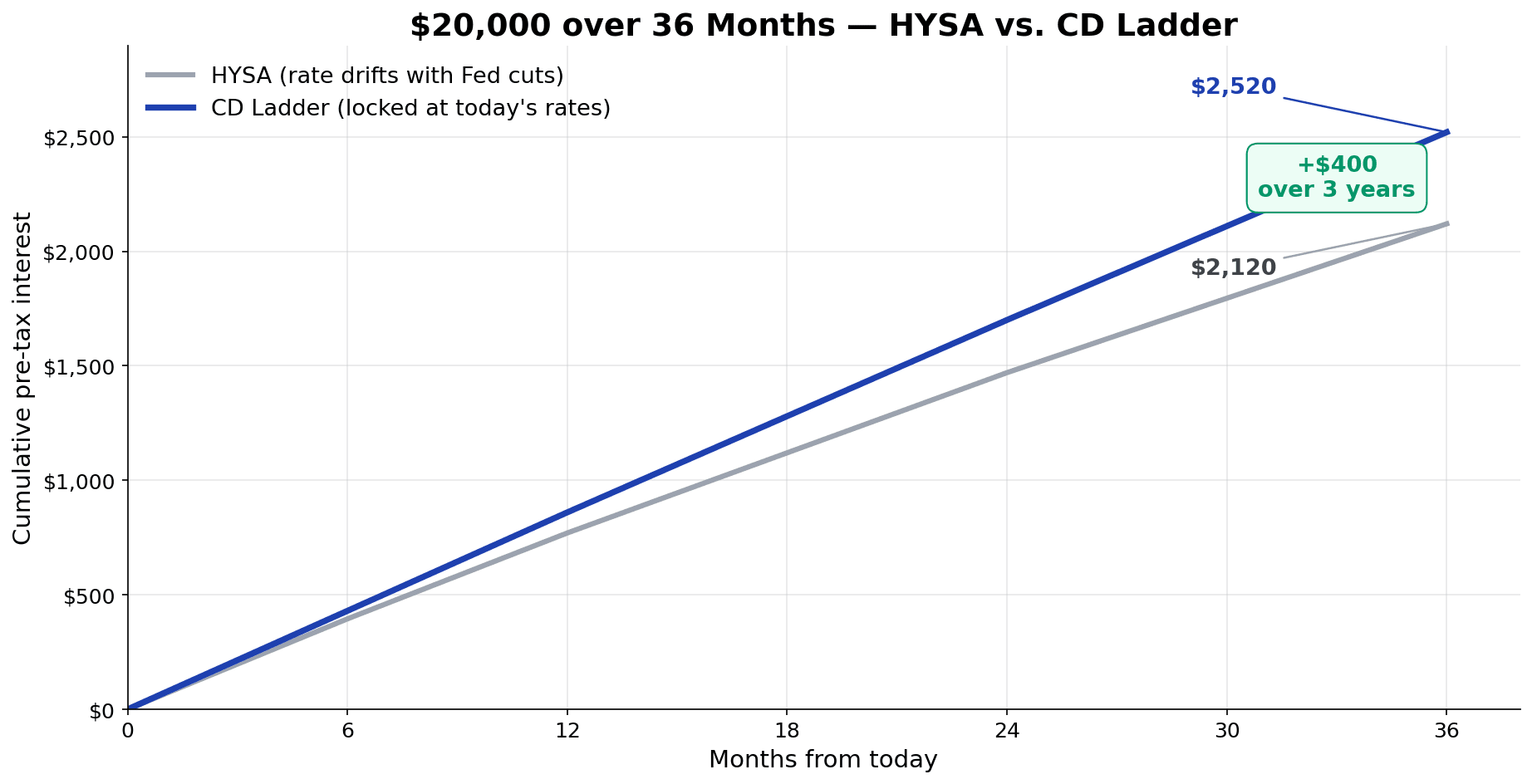

Let's run a concrete example using Maya's $20,000.

We'll compare two paths over 36 months, assuming the Fed cuts two more times in 2026 (50 bps total) and one more in 2027 (25 bps), and that her HYSA rate tracks those cuts with a small lag.

Path A — Leave it in HYSA:

- Months 1–6: 3.95% → ~$394 interest

- Months 7–12: 3.75% → ~$375 interest

- Months 13–24: 3.50% (full year) → ~$700 interest

- Months 25–36: 3.25% (full year) → ~$650 interest

- Total: ~$2,119 in pre-tax interest over 36 months.

Path B — Classic 1–5 year ladder, opened today:

- $4,000 each at 1-yr (4.10%), 2-yr (4.20%), 3-yr (4.30%), 4-yr (4.40%), 5-yr (4.50%) — these are realistic top-quartile online-bank rates as of May 2026.

- Weighted average locked APY ≈ 4.30%.

- Pre-tax interest over 36 months (assuming Year 1 and Year 2 rungs roll into new 5-year CDs at the falling prevailing rates): approximately $2,580.

The ladder produces roughly $400 more pre-tax interest over three years on a $20,000 balance — about 19% more yield than the do-nothing path. That's not a fortune. It is, however, several months of an MFFT subscription, a long weekend trip, or a respectable contribution to an IRA — for 30 minutes of setup.

Scale the same logic to a $100,000 cash bucket (a common pre-retiree situation) and the difference grows to $1,800–$2,100 in extra interest over three years. At that size, the question isn't whether to ladder. It's why you haven't yet.

Real Trade-Offs: Liquidity, Penalties, and Tax

This is the section bank marketing pages skip. Read it before you wire any money.

1. Early-withdrawal penalties are real and hurt. Most major banks charge a penalty equal to a portion of the interest if you break a CD early. Capital One, for example, charges three months of interest for CDs with terms of 12 months or less, and six months of interest for terms longer than 12 months. If you pull a 5-year CD in month 4, the penalty can exceed what you've earned — you walk away with less than you deposited.

2. Inflation can outpace your locked rate. A 4.30% locked APY feels great when inflation is 2.5%. It feels worse when inflation jumps back to 4%. Real (inflation-adjusted) yield is what matters. If your view is that inflation will spike higher than the Fed expects, a CD ladder is the wrong place for most of your cash.

3. Interest is taxed at ordinary income rates. Federal tax applies every year on interest accrued, even on multi-year CDs (the bank issues a 1099-INT annually). In a high-tax state, T-Bills can be a better swap — they're exempt from state and local tax. CDs are still simpler for most people. Just know the trade.

4. FDIC coverage is per-bank, per-ownership-category, capped at $250,000. If you're laddering a large cash bucket and you cross $250,000 at one bank, the excess isn't FDIC-insured. The fix is to split across two or more banks, or use different ownership categories (single, joint, retirement) at the same bank.

5. Auto-roll is a small trap. When a CD matures, most banks roll it into a new CD of the same term — often at a non-promotional rate that's noticeably worse than the rate they offered to attract you the first time. Set a calendar reminder one week before every maturity. Compare rates the day it matures. Re-shop or move banks if you have to.

How to Set Up Your Ladder in About 30 Minutes

Here is the practical workflow that gets you from "I should do this" to "It is done."

-

Confirm the cash is truly surplus. Run your monthly numbers in your budgeting tool of choice and identify cash you genuinely don't need access to inside a year. If you're not sure, you don't have surplus — you have an emergency fund. Stop here and read the 2026 emergency fund guide.

-

Decide which ladder shape. If the money might be needed within 12 months, use the short ladder. If it's a permanent cash allocation, use the classic or barbell. Write the choice down.

-

Compare APYs across at least three online banks. Bankrate, NerdWallet, and the bank's own page are the standard starting point. Online banks routinely beat brick-and-mortar by 50–150 basis points on the same term.

-

Open the CDs in one session. Most online banks let you open multiple CDs with the same logged-in flow. Fund them from your linked checking account. Save the confirmation emails.

-

Set calendar reminders. One reminder one week before each maturity date. Future-you will thank current-you.

-

Track each rung in your net-worth view. Whether you use MFFT, a spreadsheet, or another tool, each CD should be its own account line. "Out of sight" is how locked money gets forgotten about, missed maturities happen, and auto-roll dings you.

Three Mistakes That Turn a Ladder into a Mousetrap

These are the failure modes I see most often. They're not exotic. They are common, expensive, and entirely avoidable.

Mistake 1: Laddering the emergency fund. A 3–6 month emergency fund needs to be on-demand. If your hot water heater dies on a Tuesday, you can't wait until the 9-month rung matures in September. Emergency money lives in a HYSA or money market account. Surplus money goes in the ladder. Mix them up and you'll either pay a penalty or rack up credit card debt — both of which cost more than the yield you locked in.

Mistake 2: Treating a CD ladder like Coast FIRE. A ladder is a cash strategy. It is not an investment strategy. The long-run real return on CDs is roughly inflation, plus a small premium. It will not get you to financial independence. If your time horizon is 10+ years and the money is genuinely long-term, broad-market index funds inside tax-advantaged accounts are doing the heavy lifting. See Coast FIRE for the math on why duration, not yield, dominates long-horizon outcomes.

Mistake 3: Forgetting taxes and chasing teaser rates. A "5.00% APY" headline often applies to balances under $5,000 or only to the first three months. Read the fine print. After the teaser drops, you might be earning 2.10% — worse than a boring 3.75% HYSA you didn't have to shop for. The marginal effort of finding a genuinely good CD is small. The marginal effort of switching banks again in six months is bigger than people admit.

The Bottom Line: Should You Build a Ladder Right Now?

Here is the decision matrix in one place:

| Your situation | Recommended action |

|---|---|

| No emergency fund yet | Build it in a HYSA. Do not ladder. |

| Emergency fund covered, surplus cash you might need within 12 months | Short ladder (3/6/9/12 month) |

| Emergency fund covered, surplus cash with no specific need date | Classic 1–5 year ladder |

| Emergency fund covered, large balance, want minimal bookkeeping | Barbell (12 month + 5 year) |

| Surplus cash, but 10+ year horizon and you can take volatility | Skip CDs — invest in broad-market index funds |

| Live in a high-tax state (CA, NY, NJ, etc.) | Compare Treasury bills as a CD substitute |

For most readers who have an emergency fund and at least a few thousand dollars of surplus cash sitting in a high-yield savings account, 2026 is the right year to build a ladder — for the simple reason that the rate environment is moving against you and a ladder partially freezes it.

The discipline of doing this is the same discipline that builds every other piece of long-term wealth: deciding now, against the small inertia of "I'll deal with it later," to make the small move that compounds. That's the whole time × money × discipline equation, applied to the boring 4% slice of your balance sheet.

It is not glamorous. It will not go viral on FinTok. It just quietly works — and right now, for the first time in two years, the gap between doing this and not doing this is wide enough to be worth the half hour.

If you've been tracking your net worth in MFFT and watching your savings line creep down rate cut by rate cut, you already have the data telling you what to do. Half an hour. Five clicks per CD. A calendar reminder per rung. That's it.

The Fed is cutting. Your savings rate is following. You don't have to.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.