401(k) Match Suspended? The 6-Step 2026 Recovery Plan

TL;DR: When an employer suspends a typical 3% 401(k) match, a "temporary" one-year pause costs an $80,000 earner about $18,300 in retirement wealth once compounded over 30 years — and a permanent cut erases $241,000. The recovery plan: keep contributing anyway (the tax advantages survive), redirect the phantom match into an IRA/HSA stack, negotiate the lost match back as salary, and pressure-test your FIRE date. The match was never guaranteed; the plan is what you control.

On April 30, 2026, roughly 16,000 TTEC employees opened an internal email from Chief People Officer Laura Butler.

The 401(k) employer match — up to 3% of pay if you contributed at least 6% — was suspended. Effective immediately. Through the end of the year. Re-evaluated in Q1 2027.

The funds, the memo explained, would be redirected to "AI certifications, training programs, and the implementation of AI-enabled tools."

For Sarah, a 32-year-old marketing manager at TTEC earning $85,000, that single email was a $2,550/year pay cut she never voted on. Compounded to age 65 at a 7% real return, that one suspended year alone vaporizes about $23,600 of future retirement wealth. If the pause becomes permanent, she's looking at $305,000 of retirement money that simply… isn't there anymore.

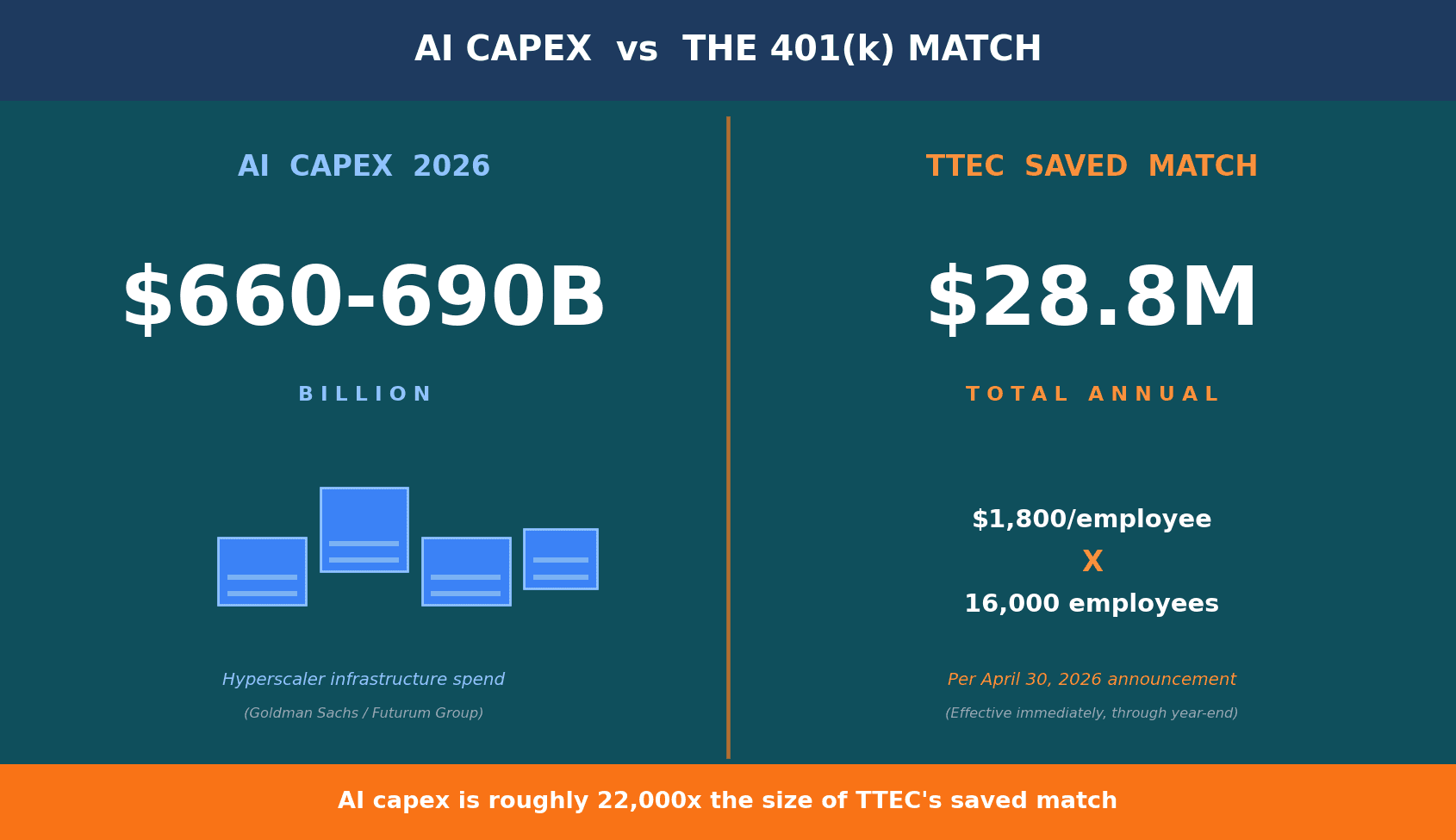

She is not alone. Sherwin-Williams suspended its 100%-of-first-6% match on October 1, 2025. Deloitte gutted parental leave, PTO, IVF reimbursement, and pension accruals for "Center" employees this January. Zoom trimmed parental leave the same quarter. And the four largest hyperscalers — Amazon, Microsoft, Google, Meta — are committing $660–690 billion of AI infrastructure capex in 2026, nearly double 2025's $400+ billion, while collectively trimming 20,000+ jobs.

The pattern is unmistakable. Margin pressure is real, AI capex is enormous, and the easiest line item to claw back is the one nobody legally has to pay you: the discretionary employer match.

If you've Googled "401k match suspended 2026" in the last few weeks because something landed in your own inbox, this guide is for you. We'll cover the actual dollar damage, why this is happening, and a six-step survival playbook to claw the lost compounding back. No doom-scrolling, no fluff — just the math and the moves.

The $1.8 Billion 401(k) Match Suspension Nobody Voted For

Let's name what's actually happening.

A 401(k) employer match is discretionary under almost every plan document. Vested balances are yours; the future match is not. Employers can — perfectly legally — pause it, shrink it, or add a "hours worked" requirement that quietly excludes part-timers. They give 30 days' notice and it's done.

For most of the last 15 years, the match was sticky because labor markets were tight. That's changing. Tech-sector unemployment hit 5.8% in Q1 2026 — the highest since the dot-com bust — with 78,557 layoffs in the first quarter alone, 47.9% of them attributed to AI/automation. When workers have fewer outside options, employers feel less pressure to keep premium benefits.

Combine that with the AI capex sprint and you get a textbook expense reallocation. Vanguard's 2026 How America Saves preview shows the average promised match is 4.6% of pay, and 88% of plan-eligible employees receive one. That's the single largest discretionary contribution most workers get from their employer. It's also the single biggest line on the chopping block.

The good news, if you can call it that: Fidelity's mid-2026 plan-sponsor survey of ~900 sponsors found "most are not considering a reduction or suspension of the company match." TTEC and Sherwin-Williams are still outliers, not yet a majority trend.

The bad news: the historical base rate from 2008–09 says outliers can become a wave fast. 218 companies suspended their match between January 2008 and November 2009, affecting roughly 5% of all 401(k) participants. About 75% of those eventually restored the match — typically within 24–36 months — but the workers who absorbed the gap without a plan never recovered the lost compounding.

That's the asymmetry I want you to internalize. Reinstatement is uncertain. Compounding is not.

The Real Math: What a Suspended Match Actually Costs You Over 30 Years

Most articles wave at this with a single example. Let me show you the full picture.

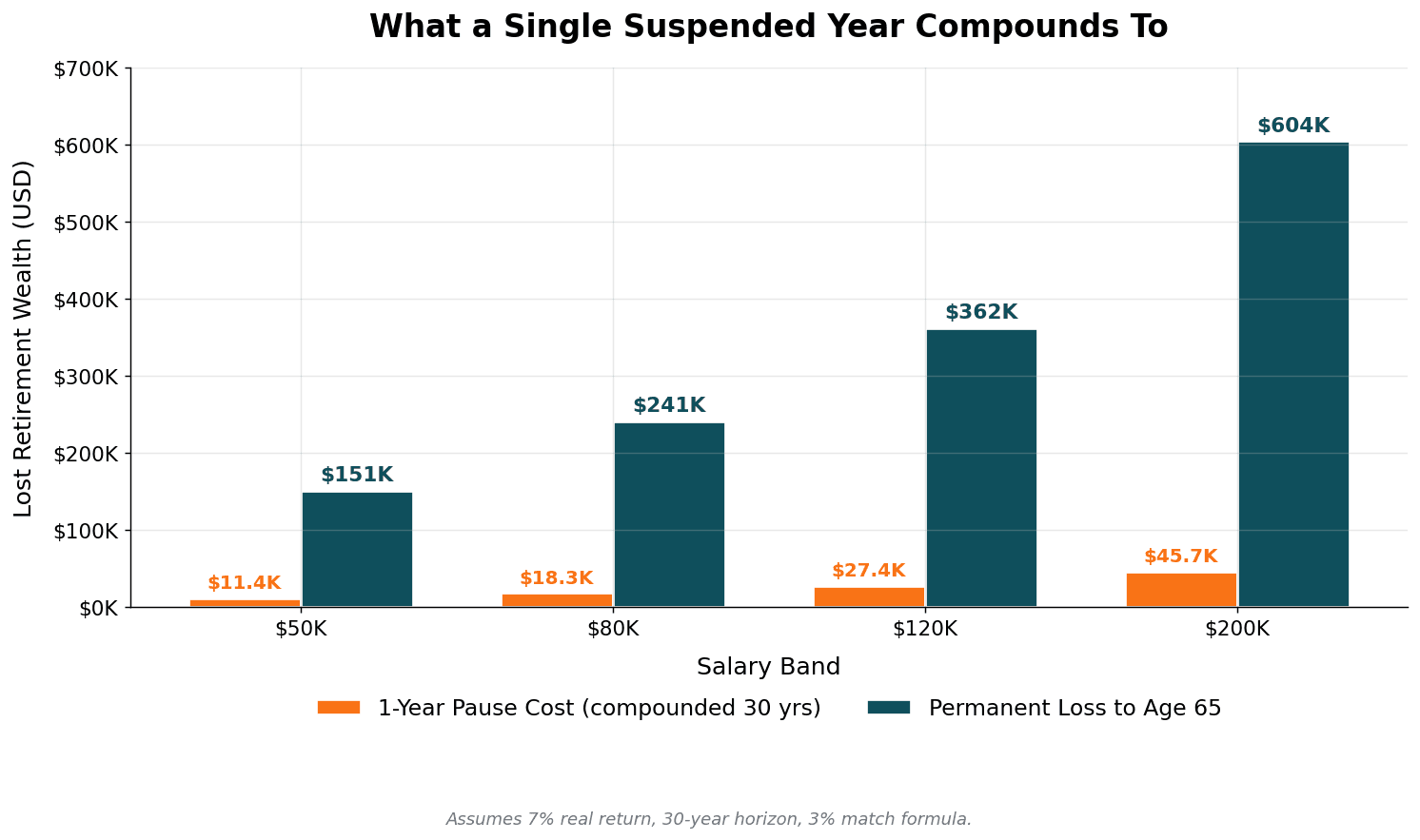

A typical match formula is 50% of the first 6% you contribute, but the all-in dollar number that matters is what your employer puts in. Here's the damage by salary band, assuming a 3% effective match (the TTEC formula), 7% real returns, and a 30-year horizon to retirement:

| Salary | Typical 3% match | One-year pause cost (compounded 30 yrs) | Permanent loss to age 65 (30 yrs) |

|---|---|---|---|

| $50,000 | $1,500 | $11,400 | $151,000 |

| $80,000 | $2,400 | $18,300 | $241,000 |

| $120,000 | $3,600 | $27,400 | $362,000 |

| $200,000 | $6,000 | $45,700 | $604,000 |

Read that again. A single year of paused match costs an $80K earner roughly the price of a new car — 30 years from now, in real, inflation-adjusted dollars. A permanent removal at $120K erases the equivalent of a paid-off house.

If you want to see this for your specific salary, current 401(k) balance, and target retirement age, plug the numbers into MFFT's net-worth and FIRE projection tool — the same dashboard I use to model these scenarios. No account aggregation, no email required, your data stays on your device.

A few worked character examples to make it tangible:

Sarah, 32, marketing manager at TTEC, $85,000 salary. Old match: $2,550/year. One-year suspension compounded to age 65 (33 years at 7%): $23,600 gone. Two years suspended: $45,000 gone. If permanent: $305,000 of retirement wealth disappears.

Jake, 28, customer-support specialist, $55,000. Old match: $1,650. One-year cost compounded over 37 years: $20,500. Permanent loss: $255,000. Jake has the longest runway and therefore the biggest absolute hit per dollar — that's just compounding doing its job.

Michelle, 45, senior consultant, $135,000. Match dollars at risk: $4,050/year. One-year cost over 20 years: $15,700. Permanent loss to age 65: $166,000. Less time to compound, but a bigger annual hit.

These numbers assume a 7% real return — the long-run S&P 500 inflation-adjusted average. Use 6% if you want to be conservative. They still hurt.

Why 401(k) Matches Are Being Suspended in 2026 (And Why It Probably Won't Reverse Quickly)

A two-minute version, because the macro context matters for your plan.

Hyperscaler AI capex more or less doubled in a single year. Goldman Sachs projects AI companies will invest more than $500 billion in 2026; Futurum Group's tracker pegs the top-five hyperscalers at $660–690 billion. Bloomberg's data-center coverage flags ~$3 trillion of associated debt-financed buildout through 2028. Bank of England warned the leverage "could heighten potential financial stability risks if valuations correct."

Morgan Stanley put it bluntly: this capex cycle "is set to exceed dot-com era telecom capex in both magnitude and length." Their projection has hyperscalers driving roughly 40% of total Russell 1000 cash capex over 2026–2028 — more than $2 trillion.

That money has to come from somewhere. Three sources, basically: debt, equity dilution, or operating margin. And every CFO with a pulse is being asked the same question by the board: what's the easiest discretionary expense to trim?

The 401(k) match is a perfect target. It's predictable, it's large in aggregate, and — critically — it's not legally guaranteed. ERISA does not require an employer to make matching contributions. A plan amendment with 30 days of notice and a quick benefits-committee meeting is all it takes.

Sam Altman flagged the obvious caveat during a recent earnings cycle: there's "AI washing where people are blaming AI for layoffs that they would otherwise do, and then there's some real displacement by AI." Some of these benefit cuts would happen anyway — the AI line is convenient cover. That doesn't change the math for the worker absorbing it, but it should change how you think about reinstatement timing. Cuts justified by genuine margin pressure don't unwind until the pressure does.

For the median worker, the practical question isn't why. It's now what.

Step 1: Don't Quit Contributing — Here's the Math on Why

The very first reaction I see in finance forums when a match disappears is some version of: "No match = no point. I'm pausing my 401(k) and putting it in a brokerage."

Don't do this.

Even without a match, the 401(k) still has three things working in its favor that a taxable brokerage doesn't:

1. Tax deduction now. A $7,000 pre-tax contribution at the 24% federal bracket saves you $1,680 in immediate taxes. That's an instant 24% return — risk-free, guaranteed, no employer required.

2. Tax-deferred compounding. Your gains aren't taxed each year. A taxable brokerage drags ~15% on long-term capital gains and ~24% on dividends. Over 30 years that drag compounds into roughly 22% less ending wealth vs. a 401(k), per the standard SmartAsset and Human Interest analyses.

3. Institutional fund expense ratios. Most 401(k) plans give you access to 0.02–0.10% institutional shares. Retail accounts pay 0.03–0.20%. Small in any single year, large over decades.

The 2026 employee deferral limit just rose to $24,500 (up from $23,500), with an $8,000 catch-up at 50–59 and an $11,250 super catch-up at ages 60–63. There's a new wrinkle for high earners: workers with prior-year FICA wages above $150,000 must now make catch-up contributions on a Roth basis. The full landscape — and the gotchas most plans haven't communicated well — is in the 2026 retirement contribution rules and Roth catch-up trap breakdown.

The honest answer to "should I keep contributing to 401(k) without match?" is: yes, until you've maxed your better options. The match was a bonus on top of a fundamentally good vehicle. Losing the bonus doesn't make the vehicle bad.

What it does change is the priority order. Which is Step 2.

Step 2: Redirect the "Phantom Match" Into Your Own Stealth Retirement Stack

Here's the move that turns a passive loss into an active win.

Take the dollars your employer would have contributed and route them into accounts your employer can never touch. Sarah's $2,550/year is $212/month. Jake's $1,650 is $137/month. Michelle's $4,050 is $337/month. That's the phantom match — and it's now yours to direct.

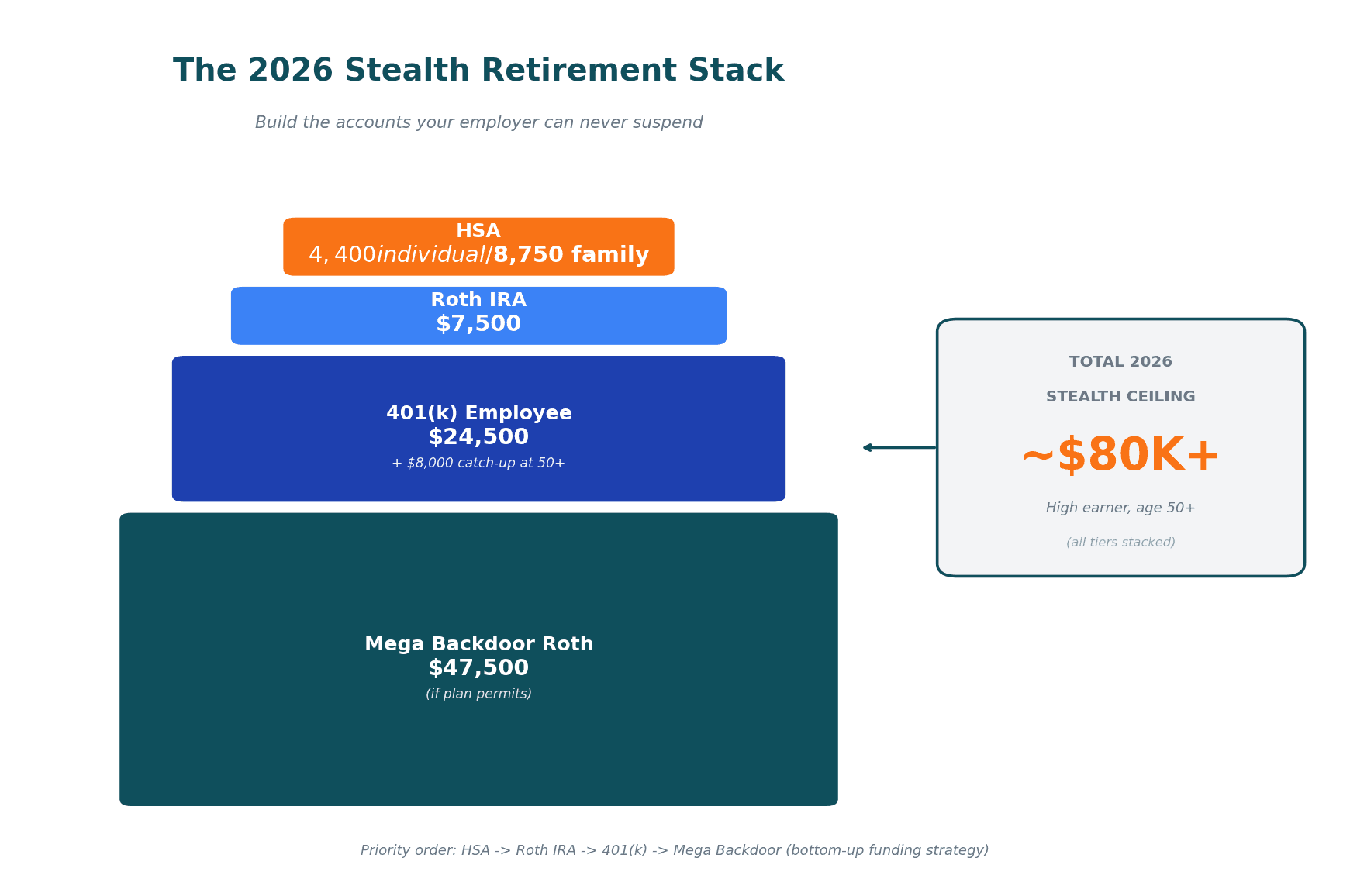

The 2026 priority order I run, in plain English:

Tier 1 — HSA, if you're HDHP-eligible. The Health Savings Account is the single most tax-efficient retirement dollar in the U.S. tax code. Triple tax advantage: pre-tax in, tax-free growth, tax-free out for qualified medical expenses. After 65 you can withdraw for any reason at ordinary income rates — effectively a second traditional IRA. 2026 limits: $4,400 individual, $8,750 family, plus a $1,000 catch-up at 55+. The minimum HDHP deductible to qualify is $1,700 self / $3,400 family. The full mechanics are in HSA: The Stealth Retirement Account That Beats Your 401(k), and honestly, if I had to pick one account to fund first when the match disappears, it's this one.

Tier 2 — Roth IRA. 2026 limit: $7,500 under 50, $8,600 at 50+. Income phase-outs: $153K–$168K single, $242K–$252K married. Above those, you're on the backdoor Roth path (no income limit on conversion) — which is genuinely simple to execute once a year.

Tier 3 — Taxable brokerage. Low-cost broad-market ETFs (VTI at 0.03%, VT at 0.06% for a global tilt). No contribution limits, full liquidity, perfect for FIRE bridge years before 59½.

Tier 4 — Mega backdoor Roth, if your plan permits. Up to $47,500/year of after-tax 401(k) contributions converted to Roth. Most plans don't offer it; the ones that do (typically big tech, big finance) hand high earners a six-figure tax-advantaged headroom most people don't know exists.

For our characters, the redirect math is clean:

- Sarah moves $212/month → maxes her Roth IRA ($625/month limit) by year-end and replaces ~83% of her lost match dollars with tax-free growth.

- Jake splits $137/month between an HSA contribution and his Roth IRA — fully replaces the match dollar-for-dollar with better tax treatment than the 401(k) ever offered.

- Michelle redirects $337/month into HSA ($367/mo for individual max) plus a backdoor Roth ($625/mo) plus taxable brokerage. Her after-tax dollars buy back the equivalent within the first $11,900/year of redirect.

The priority order does the work. You just have to set up the auto-transfers.

Step 3: Negotiate the Match Back — As Salary

Here's the move 55% of workers never make.

A suspended 3% match is, in plain English, a 3% pay cut. Most workers absorb it silently because the message landed in a benefits portal instead of a one-on-one with their manager. That framing is wrong, and you should fix it.

The data on negotiation is striking. 73% of employers say they will negotiate, but 55% of workers never ask. Of those who do ask, roughly 66% get what they request, and 85% of counter-offers yield at least a partial gain. Those numbers come from CareerBuilder and Procurement Tactics' aggregated 2025 data. The full playbook — when to ask, who to ask, how to anchor — is in the Salary Negotiation 2026: Data-Driven Playbook.

The key reframe for this specific situation: don't ask for the match back. Ask for the value back, in base salary or a one-time retention bonus.

Here's a copy-paste email opener I've shared with friends in this exact spot:

Subject: Quick chat about total compensation

Hi [Manager],

I wanted to set up a 30-minute conversation about total compensation in light of the recent 401(k) match suspension. The pause represents an effective $X,XXX reduction in my annual total comp this year.

I'm fully bought into the team and the work — and I'd like to discuss restoring that value through one of two paths: (1) a base-salary adjustment of $X,XXX, or (2) a one-time retention bonus equivalent to the suspended match value. Both are dollar-neutral to the company's stated budget reallocation.

Could we find time on your calendar this week or next?

Thanks, [You]

A few things this email does on purpose:

- Names the dollar amount. Vague "I'd like more comp" loses; specific numbers anchor.

- Acknowledges the company's reasoning. You're not fighting the AI capex story. You're asking for an individual exception within it.

- Offers two paths. Easier for your manager to approve when there's a menu.

- Ties to retention. Even cost-conscious CFOs hate replacement costs (typically 50–200% of salary).

If your manager pushes back, the fallback ask is a larger annual bonus target or a stock grant adjustment. Don't walk away with nothing. The data says two-thirds of askers get something.

Worth saying clearly: the labor market in mid-2026 is not the labor market of 2021. With tech unemployment at 5.8% and hiring soft, "I'll just go elsewhere" is a weaker bluff than it was three years ago. Negotiate hard, but negotiate from a position of staying.

Step 4: Pressure-Test Your FIRE Timeline (And Adjust)

If you're on a Coast FIRE or Lean FIRE path, a 2-year match suspension can shift your FI date back 6–14 months, depending on your age. That's not catastrophic. But it's not zero.

For readers new to the term: Coast FIRE is the point at which your existing portfolio, left untouched and compounding at a reasonable rate, will grow to your full FI number by your target retirement age — so all you need to cover from that day forward is your living expenses. The full math and how to calculate your own coast point is in What Is Coast FIRE: Definition, Math, and Examples.

When the match disappears, two variables in your FIRE projection move:

- Annual contribution drops by the match amount.

- Your "savings rate" — measured as a % of total compensation — silently falls because total comp dropped first.

Here's what that looks like for our three readers:

Dave, 42, Coast FIRE plan, $115K salary, 2-year pause. Lost match: $3,450 × 2 = $6,900 nominal. Compounded to age 65 (23 years at 7%): roughly $32,000 of portfolio value. If his Coast target was age 60, the pause pushes that back about 7 months — unless he replaces it. A $300/month side income to a brokerage erases the gap entirely.

Sarah, 32, original FI target age 50. Lost match $2,550 over one year, compounded over 18 years: about $8,600. Her FI date moves back roughly 3 months before any countermeasures. With Step 2's redirect into a Roth IRA, the date moves back by less than a month.

Michelle, 45, catch-up phase. Lost match $4,050/year. Two-year pause compounded over 20 years: about $31,000. FI date back by 8–11 months. The fix: max her HSA + backdoor Roth in 2026 and 2027 — net-positive vs. the pre-pause plan because the redirect dollars get better tax treatment.

To run this for yourself, open MFFT's FIRE projection tool, model two scenarios — Scheduled Match and Suspended Match — and look at the spread. The dollar gap is your replacement target. The time gap is your motivation.

The takeaway: the cost is real, the recovery is mechanical, and the dashboard is the difference between guessing and knowing.

Step 5: Build the "Anti-Fragile Income" Layer

Defense is good. Defense plus a second offense is better.

The cleanest insurance policy against a benefit cut is a second income stream specifically equal to the lost match. The math is friendlier than people realize:

- $200/month invested at a 7% real return → $245,000 in 30 years. Roughly replaces a typical lost match for a $50K–$80K earner.

- $300/month → $367,000 in 30 years. Covers the loss for a $100K–$120K earner.

- $500/month → $612,000 in 30 years. Wipes out the entire compounded loss for most six-figure earners.

The IndexBox 2026 survey found 72% of Americans now rely on secondary income in some form — freelancing, contract work, Etsy, Uber, content, consulting. The Penny Hoarder's data has the median side hustler bringing in ~$200/month and the average closer to $810–$1,242/month. You don't need to build a small business; you need to find $200–$500/month of recurring income and route it directly to a brokerage.

The full strategic framing — why 72% of workers are now structurally dependent on secondary income, and how to pick a side hustle that scales without burning you out — is in The Side Hustle Paradox: Why 72% of Workers Now Need Secondary Income.

Two adjacent moves worth flagging:

Geographic arbitrage. If you're remote, relocating from HCOL to MCOL while keeping your salary can save $20K–$40K/year. That single move dwarfs most lost matches.

Negotiated bonus structures. Variable comp tied to a metric you control (sales, project delivery, performance) is harder for HR to claw back than a discretionary match. Restructure where you can.

The principle: build at least one income stream the company you work for cannot vote to cut.

Step 6: Watch the Watchlist — How to Spot the Next Round of 401(k) Match Cuts Before They Hit You

If TTEC and Sherwin-Williams have taught us anything, it's that the announcement is always the second signal. The first signals are usually visible in earnings calls and HR newsletters weeks earlier.

Here are the five red flags I track — none of them subtle once you know to look:

- Stock buyback announcement paired with cost-cutting language. Buybacks return capital to shareholders; "right-sizing" returns it from labor. When both appear in the same press release, benefit cuts usually follow within two quarters.

- "Talent architecture," "restructuring," "right-sizing," or "modernization" language in HR comms. These are the polite verbs that precede line-item cuts. Deloitte's "Center talent model" announcement was a textbook example.

- Sudden announcement of a "comprehensive benefits review" or "modernization initiative." Reviews don't conclude with more benefits.

- Heavy AI capex disclosure in the 10-Q paired with margin-pressure commentary. When the CFO says "investing aggressively in AI infrastructure" and "evaluating cost discipline" in the same paragraph, the bridge between those two ideas is your benefits budget.

- CEO or CFO turnover combined with "operational discipline" messaging. New finance chiefs always look for quick wins. Discretionary benefits are the quickest.

If you see two or more of these in your own employer's reporting, here's the 30/60/90-day playbook I recommend:

Days 0–30: Top up your emergency fund to 4–6 months. Pull your latest plan documents and identify which benefits are contractual vs. discretionary. Front-load your Roth IRA contribution.

Days 30–60: Open or refresh accounts at the next-best tier (HSA if eligible, taxable brokerage, second Roth). Set up automatic transfers equal to your current match in case it disappears.

Days 60–90: Refresh your résumé and LinkedIn. Have one informal coffee outside the company. The goal isn't to leave — it's to know your market value before you need to negotiate from it.

The watchlist is not paranoia. It's the same forward-looking discipline that good investors apply to portfolio risk — applied to your largest single source of capital, which is your job.

The Bottom Line: The Match Was Never Yours, But the Plan Always Is

The workers who absorbed the TTEC announcement in an afternoon weren't lucky. They had a plan. They had a written FIRE number, a known savings rate, a stealth retirement stack already running, and a side income that didn't need HR's permission to exist.

The workers scrambling are the ones who outsourced retirement to "whatever HR offers." That's not a moral judgment — most American workers were trained to do exactly that for forty years. It's just no longer enough.

The 401k match suspended 2026 trend is, on net, a forcing function for a healthier behavior: take direct ownership of your retirement plan, route dollars through accounts that don't depend on a future CFO's mood, and build at least one income stream you control. None of these moves requires permission from your employer.

If TTEC reverses the suspension in Q1 2027, your phantom-match dollars stay in your Roth IRA earning tax-free returns for life. If they don't, you've already replaced the lost compounding. The asymmetry is on your side.

Three things to do this weekend:

- Calculate your number. Multiply your salary by your match percentage. That's the annual dollar figure now at risk. Multiply by 7.6 for the 30-year compounded cost of a single suspended year.

- Open the next account in your stack. HSA if eligible, Roth IRA otherwise. Move the phantom-match dollars into auto-transfer.

- Model both scenarios in MFFT. Run match-on and match-off projections side by side. The spread is your insurance premium.

Free money disappearing from your benefits package is genuinely annoying. But the math is solvable, the playbook is short, and the worst version of this story is the one where you do nothing because the news made you tired.

You've got the moves. Run them.

If you want one place to model both scenarios, track your phantom-match redirect, and watch your FIRE date move in real time as you replace the lost compounding, that's exactly what My Financial Freedom Tracker is built for. Privacy-first, no email required. Run the numbers, decide your next 90-day move, then go enjoy your Sunday.

The match was never yours. But the plan always is.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.