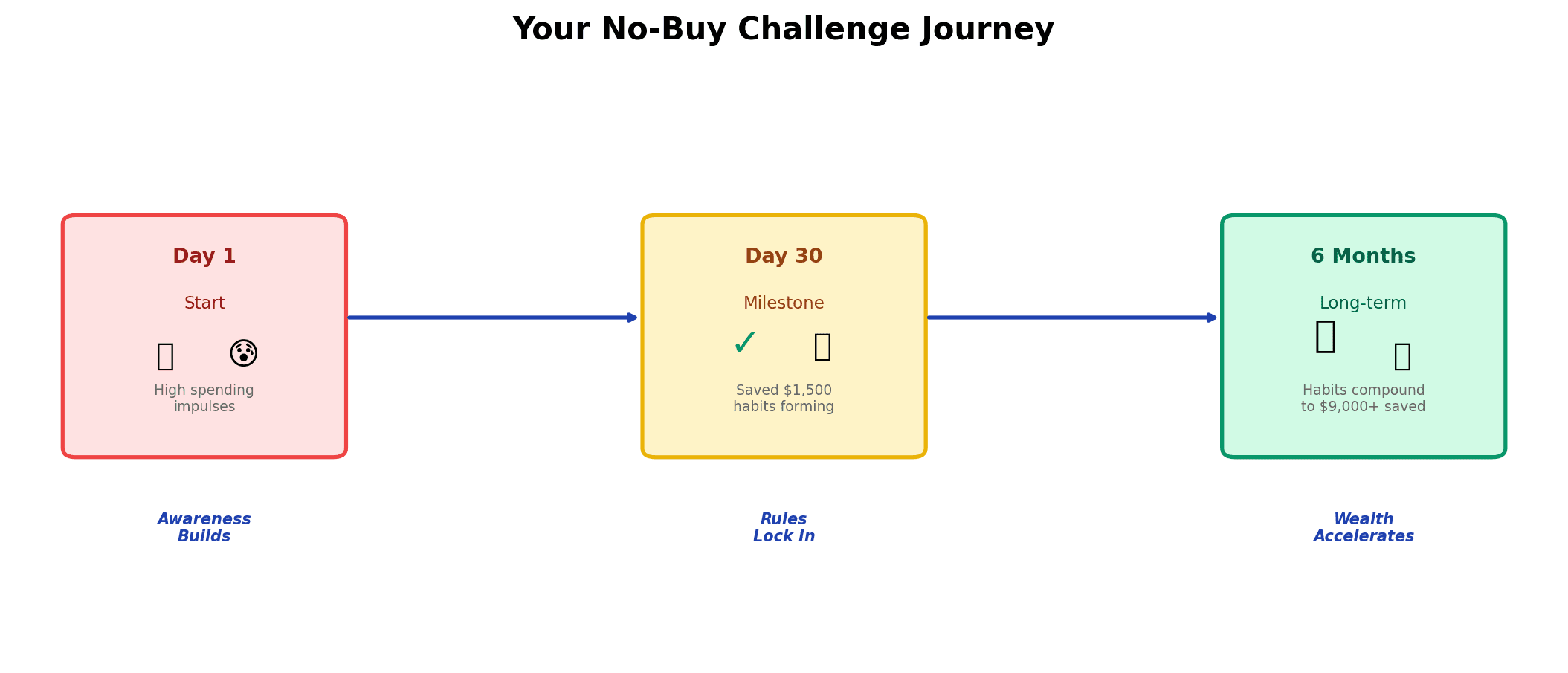

No-Buy Challenge: Rules, 4-Week Plan & What You’ll Save

Your friend texts the group chat: "I'm doing a no-buy challenge this month."

A year ago, you might've laughed. Or thought it sounded punishing. But something's shifted. According to Intuit's 2026 Financial Wellness Report, 93% of Americans plan to make changes to their money management this year. And the no-buy challenge isn't some fringe trend anymore—it's the top vehicle for financial reset in 2026.

Here's what's driving it: 54% of Americans report financial regrets from 2025. 45% admit impulse purchases have derailed their goals. People are stressed about money, tired of spinning their wheels, and ready to take control. The no-buy challenge has become the most accessible way to do that.

The tricky part? Most people fail. One in three Americans who tried a no-buy challenge in January quit within the first month. But the people who succeed don't just save money—they unlock something deeper: clarity about what they actually value, and momentum toward financial independence.

This article walks you through why the no-buy challenge works, why most people fail at it, and exactly how to succeed. We'll show you the four-week setup, real numbers from people who've done it, and how this single month can kickstart your path to financial freedom.

Why the No-Buy Challenge Is Everywhere in 2026

The stress is real. Americans are spending roughly $1,050 per month on nonessentials—discretionary spending on dining out, entertainment, clothing, and personal care. Over a year, that's $12,600 in spending that, for many people, doesn't feel intentional. It feels automatic.

According to FIRE movement research, one of the highest-leverage financial moves is reducing your baseline expenses. The no-buy challenge is the fastest way to identify where that reduction can happen.

Then 2025 ended. Financial statements arrived. People looked at their net worth and felt the gap between what they earned and what they kept.

Enter the no-buy challenge: a simple rule set that says, "For the next 30 days, I'm not buying anything nonessential." No clothing. No dining out. No subscriptions. No impulse purchases. Just essentials: food, utilities, insurance, medication, gas.

And something magical happens. When the rule is clear and the timeline is bounded, people start noticing. They see how many times per day they reach for their phone to shop. They realize how often stress or boredom triggers a purchase. They taste what financial control actually feels like.

The Intuit data shows that 49% of Americans have committed to "more mindful spending" in 2026. The no-buy challenge is the method they're using to make that real. It's not a diet—it's a reset. And unlike most financial changes, it has a finish line, which is psychologically powerful.

What Actually Is a No-Buy Challenge (And What Doesn't Count)

Before you start, let's be clear about the rules. Because confusion here is where most people stumble.

The No-Buy Challenge Rules

A no-buy challenge is simple: you define a period (usually 30 days) and a set of restrictions on what you can spend money on.

What You CAN Spend On:

- Groceries and food for cooking at home

- Utilities (electric, water, internet, phone)

- Rent or mortgage payment

- Insurance (auto, health, home)

- Medications and essential medical care

- Gas or transportation for necessity

- Replacement of essential items that break (shoes with holes, underwear, deodorant)

What You CAN'T Spend On:

- New clothing or accessories

- Dining out or food delivery

- Subscriptions (streaming, apps, memberships)

- Entertainment (movies, events, bars)

- Coffee shop purchases

- Impulse shopping of any kind

- Home decor or non-essential items

- Personal care splurges (haircuts, nail salon, massage)

| Category | Can Buy | Cannot Buy |

|---|---|---|

| Food | Groceries, essentials for cooking | Dining out, delivery, impulse snacks |

| Clothing | Essential replacements only | New clothes, shoes, accessories |

| Home | Essential repairs only | Furniture, decor, plants |

| Entertainment | Free activities, library books | Streaming new subscriptions, movies, events |

| Subscriptions | Essential services only (internet, phone) | Music, apps, entertainment services |

| Personal Care | Medications, basic hygiene | New cosmetics, salon services, luxury items |

| Transportation | Gas/maintenance for necessity | Uber/Lyft, new car, upgrades |

The key word here is "essential." This isn't about deprivation. It's about intention. You're not starving. You're not avoiding necessary care. You're just pausing the automatic spending that doesn't align with your values.

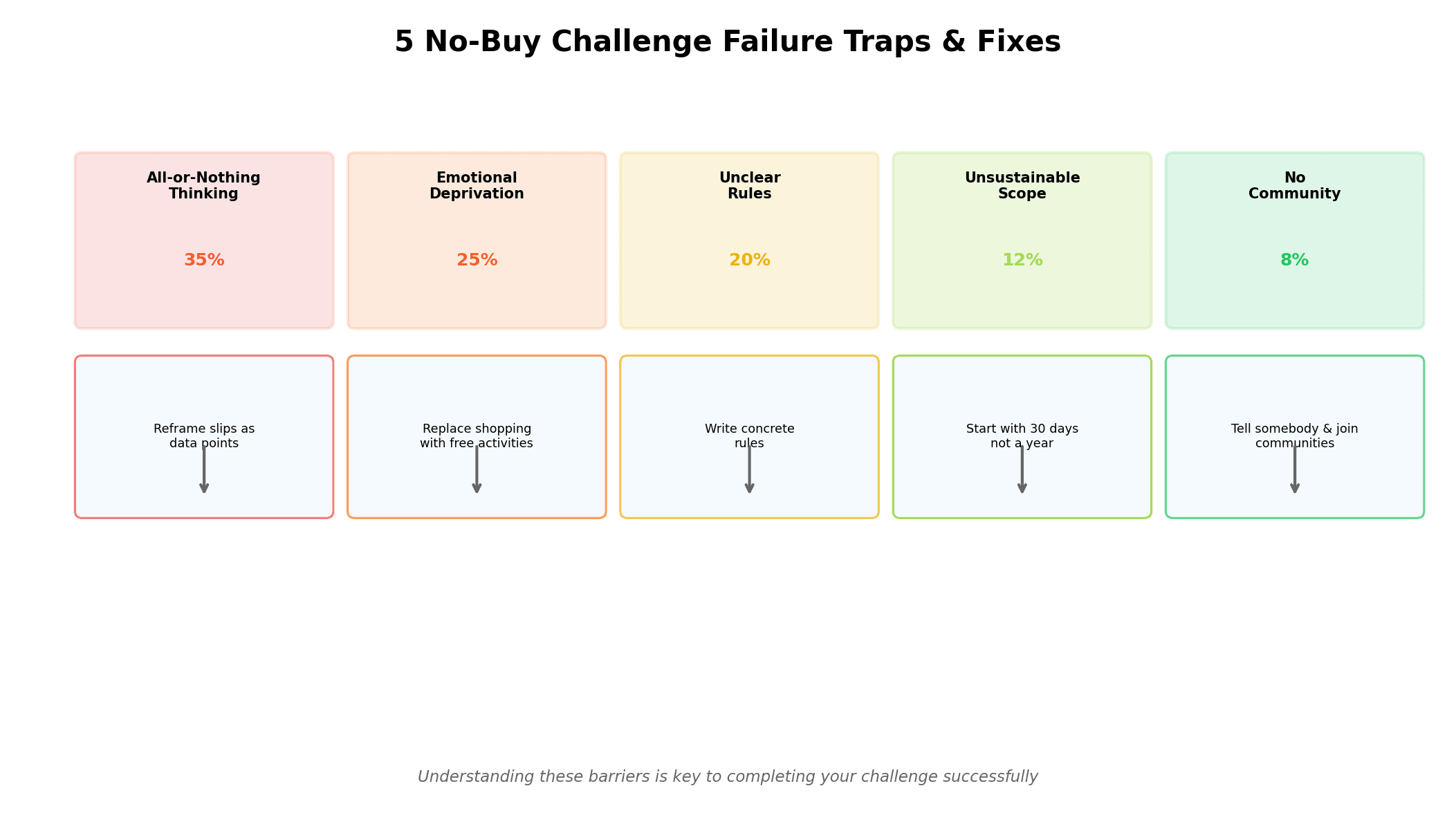

Why Most No-Buy Challenges Fail (And How to Avoid the 5 Biggest Traps)

Let's be honest: one in three people who start a no-buy challenge quit.

It's not because they lack willpower. It's because the challenge hits five specific psychological barriers, and most people don't have a plan to handle them. Once you understand the traps, avoiding them becomes simple.

Trap #1: All-or-Nothing Thinking

You go to the grocery store, walk past the bakery section, and break your rule. You buy a pastry. Immediately, your brain says, "I've failed. This challenge is over."

This is the most common failure point, affecting about 35% of people who quit. One slip-up triggers a shame spiral, which triggers a shopping spiral. "Well, I already broke the rule, might as well buy the jeans I've been eyeing."

How to Fix It: Reframe failure as a data point, not a verdict. If you spend $20 outside your rules, that's information. It tells you that Friday afternoons at the bakery are a trigger. Note it. Move on. One day off track doesn't undo your progress.

Trap #2: Emotional Deprivation (No Dopamine Hit)

Shopping is a dopamine hit. It's a reward. When you suddenly eliminate shopping, you remove that dopamine source without replacing it. Boredom hits harder. Stress feels less manageable.

About 25% of people quit because they can't handle the emotional emptiness of not shopping.

How to Fix It: Don't just restrict—replace. Replace shopping with other dopamine sources that don't cost money. Here's what works: free activities (hiking, library, game nights with friends), wish lists (put items on a list, wait 30 days, see if you still want them), visual progress tracking (seeing your savings grow is a genuine dopamine hit).

Trap #3: Unclear Rules or Motivation

You start the challenge but never actually defined what "nonessential" means to you. Is a $15 book essential? What about coffee? Is a gym membership okay?

Without clarity, the challenge becomes confusing. Confusion leads to decision fatigue. Decision fatigue leads to quit.

How to Fix It: Before you start, write down your specific rules. Be concrete. "No shopping at Target. No food delivery. No new subscriptions." And write down your why. Are you saving for something specific? Trying to break a habit? Resetting your relationship with money? Keep that visible.

Trap #4: Unsustainable Scope (Full Year Too Long)

Some people commit to a year-long no-buy challenge. Admirable, but also predictably doomed. A year feels abstract. You can't see the finish line.

How to Fix It: Start with 30 days. Just one month. One month is concrete. You can see day 30 from day 1. After 30 days, if you want to continue, you can. But starting with a month removes the "forever" feeling that triggers quit.

Trap #5: Unsustainable Motivation (No Community)

You're tracking alone, in your spreadsheet, telling nobody. When you hit day 7 and the dopamine from the novelty wears off, you're alone. There's nobody asking, "How's your challenge going?" There's nobody celebrating your win.

About 12% of people quit because isolation weakens accountability.

How to Fix It: Tell somebody. Post in the 70,000-member no-buy Reddit community. Text a friend weekly. Share your progress on social media. The no-buy challenge works because it's trending—use that community energy.

The 4-Week No-Buy Challenge Setup (Start This Week)

Okay, you understand the psychology. Now let's get practical. Here's the exact four-week setup that works.

Week 1: Audit & Track Your Baseline

Goal: Know exactly where your money is going before you restrict anything.

Use a budget tool to understand your baseline spending. Log every discretionary expense for one week. Not to judge yourself—just to see.

You'll likely discover something shocking. Most people discover they spend $300-$400 more per month on nonessentials than they thought. You'll see the categories where the bleeding is real: daily coffee, food delivery, subscriptions you forgot about.

This week, you're not restricting yet. You're just getting honest data.

Action items:

- Pull your last month of credit/debit transactions

- Categorize every nonessential expense

- Add up the total

- Write it down

This number becomes your "before" baseline. You'll measure against it in Week 4.

Week 2: Identify Your Spending Triggers

Goal: Understand why you spend, not just what you spend.

For each category where you overspend, ask: What triggers this?

For someone who spends $200/month on food delivery, the triggers might be: "Tired after work on Wednesdays" and "Bored on Sunday afternoons." For someone who spends $150/month on clothing, it might be: "Stress at work makes me shop" and "Weekend scrolling Instagram."

Name the triggers out loud. Research shows that when you verbally acknowledge a trigger, it weakens its automaticity. You create space between the trigger and the behavior.

Action items:

- Review your Week 1 data

- Write down 3-5 spending triggers

- Identify the time, emotion, or location that precedes each one

- Plan a replacement behavior for each (call a friend, take a walk, read, etc.)

This is where habit-replacement science kicks in. You're not just restricting. You're building new neural pathways.

Week 3: Replace Habits with Free/Cheap Alternatives

Goal: You're officially in the no-buy challenge now. But this week is about replacement, not restriction.

For every spending trigger you identified, you've already got a replacement ready. Stress at work used to mean shopping? Now it means a walk. Bored on Sunday? Now it's a free activity.

Here are replacements that actually work:

- Boredom → Hiking, library, YouTube, game nights, podcast binges

- Stress → Phone call with a friend, journaling, exercise, cooking a new recipe

- FOMO (fear of missing out) → Create a wish list, wait 30 days, see if you still want it

- Social pressure ("Everyone's going shopping") → Suggest a free alternative, be loud about your budget

This is where the loud budgeting movement helps. When you tell your friends you're doing a no-buy challenge, something shifts. Social accountability becomes a tool, not a burden.

Action items:

- For each trigger, commit to one replacement behavior

- Test it for at least three days before Week 4

- Adjust if it's not working (some replacements won't stick; that's fine)

Week 4: Measure Results and Celebrate

Goal: See the actual impact of your month, quantified and real.

Pull up your Week 1 baseline. Add up your discretionary spending from the past four weeks.

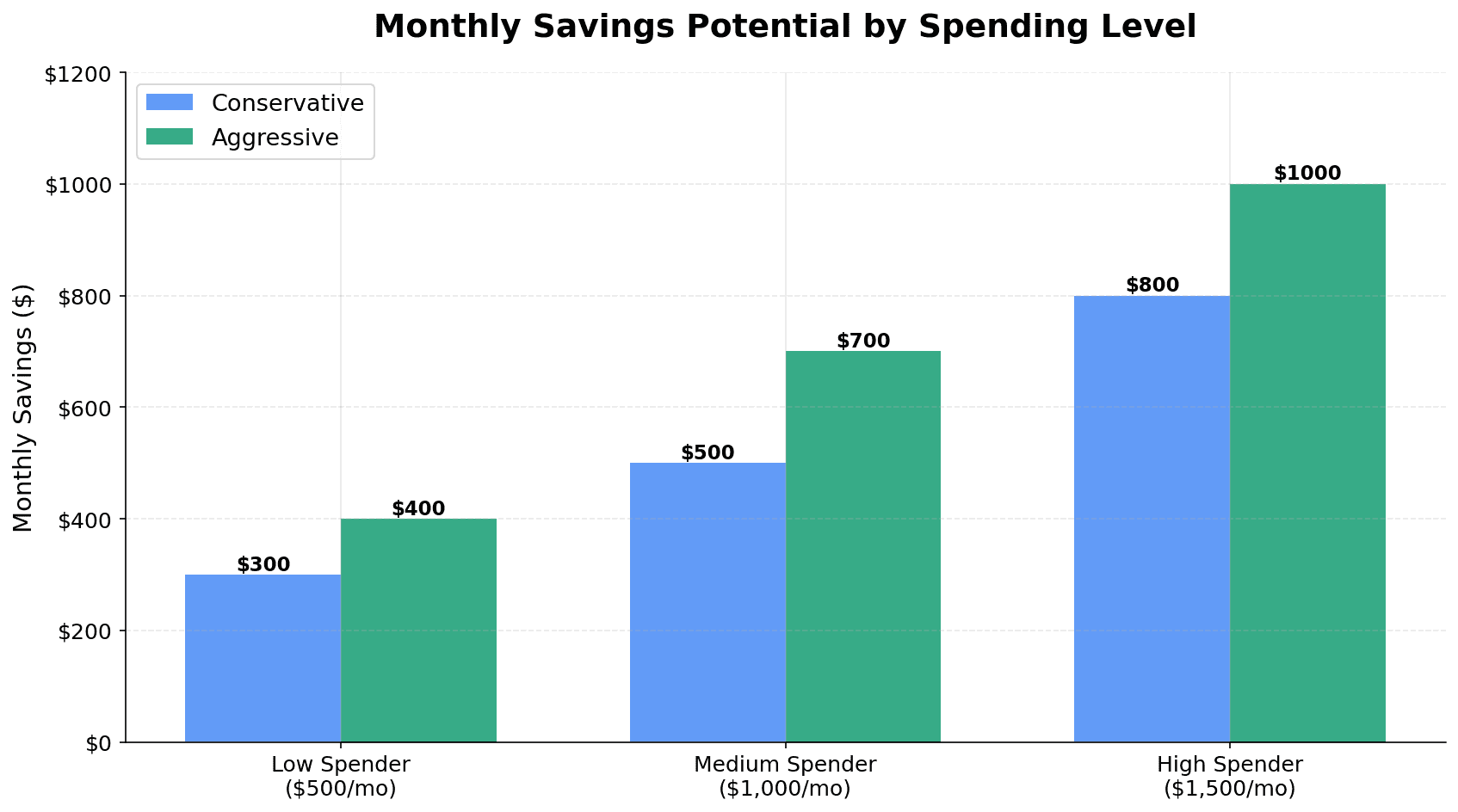

The typical result? $300-$750 saved in a single month. That's $3,600-$9,000 per year if you run four quarterly challenges.

But here's what matters more than the number: How do you feel? Did you miss shopping? Or did you discover you didn't actually need any of the things you usually buy? Did the challenge feel punishing? Or did it feel like clarity?

This is the data that tells you whether to continue, modify, or take a break.

Action items:

- Calculate your total nonessential spending for the month

- Compare it to your Week 1 baseline (the difference is your savings)

- Celebrate the win (take yourself to dinner, gift yourself something nonmaterial)

- Write down what you learned

- Decide: Will you do another 30-day challenge? Or shift to permanent mindful spending?

Real Money: What Three People Actually Saved in 30 Days

Numbers are abstract. Let's get concrete.

Sarah: The $800 Success (High Spender)

Sarah, 34, was spending roughly $1,600/month on nonessentials. Her no-buy was broad: nothing except groceries and utilities.

Week 1 audit: coffee ($120), food delivery ($280), streaming subscriptions ($45), clothing ($320), random shopping ($440).

By Week 3, the habits stuck. She:

- Switched to home coffee ($8/month instead of $120)

- Cooked at home instead of delivery (cost $80 for groceries vs. $280 usual)

- Paused her subscriptions (saved $45)

- Wore what she owned (saved $320)

- Stopped random shopping (saved $440)

30-day total: $800 saved. She ran two more quarterly challenges. One year: $3,200 in new savings.

She told me later: "The wild part was realizing I didn't actually want most of the things I was buying. I was buying to fill time."

Marcus & Julie: The $2,400 Win (Couple, Aggressive)

Both worked full-time. Both were stressed. Both were spending unconsciously.

They did the no-buy together. Combined baseline: $2,100/month nonessential. They set a goal: $1,500/month or less.

By Week 2, they realized food delivery was a $400/month stress response. They committed to cooking Sunday-Thursday together (it became couple time, not a chore). Food delivery reduced to $50/month (one splurge per week).

Other wins: Paused $90 in subscriptions they weren't watching. Stopped "stress shopping." Audited their closets and realized neither had worn 40% of their clothes in a year.

30-day total: $1,200 saved. Annualized (just from the food delivery change alone): $4,200.

Marcus said: "We thought we'd resent the restrictions. Instead, it was weirdly bonding. We were working toward something together."

David: The Mixed Results (Beginner, Mid-Month Slip)

David had never tracked his spending. He committed to a 30-day no-buy challenge on a whim.

Days 1-14: He was disciplined. Saved about $400. But he hit a rough patch at work. As research on the coffee that's costing you wealth shows, stress often triggers small, compounding purchases.

Days 15-21: He broke the rules. Bought a jacket, got takeout, downloaded a new app. Felt shame. Almost quit.

But instead of quitting, he recalibrated. Days 22-30: No more shopping, but he lowered his emotional stakes. He accepted that he'd spent $200 outside the challenge and moved on.

30-day total: $320 saved. Not as impressive, but the real win was different: he discovered that willpower was less important than self-compassion. He finished the month, learned his triggers, and committed to a second month with better boundaries.

David's lesson: "The challenge isn't about perfection. It's about awareness. I'm already planning the next one."

How a No-Buy Challenge Kickstarts Your FIRE Timeline

This is where it gets really interesting. Because a no-buy challenge isn't just about saving money this month. It's about compounding.

Let's say you save $1,500 over your first 30-day no-buy challenge. Maybe you run three more quarterly challenges over the year. Total saved: $6,000.

Now invest that $6,000 at a 7% annual return (a reasonable long-term market average):

| Year | Annual Savings | Account Value | Compound Growth |

|---|---|---|---|

| 1 | $6,000 | $6,420 | $420 |

| 5 | $30,000 | $37,310 | $7,310 |

| 10 | $60,000 | $104,518 | $44,518 |

| 20 | $120,000 | $463,768 | $343,768 |

| 30 | $180,000 | $1,355,234 | $1,175,234 |

Wait—let that sink in. You save $180,000 directly through four quarterly challenges over 30 years. But compound growth gives you $1.18 million in additional returns.

Here's where this intersects with FIRE: if you run a no-buy challenge for just one year and save $6,000-$8,000, then stop actively doing the challenge but keep some of the habits you built, you've created a permanent baseline shift in your spending. You keep maybe 3-4 new habits (cooking at home instead of delivery, no mindless shopping, pausing unused subscriptions).

That 3-4 habit shift saves you $200-$400/month forever. Over 30 years at 7% returns: $850,000-$1.7 million in additional wealth.

One month of discipline. Thirty years of compounding. That's the FIRE math that makes the no-buy challenge so powerful.

Using MFFT to Track Your No-Buy Challenge Progress

Here's the practical part: tracking matters. A lot.

When you can see your progress, your brain releases dopamine. That dopamine is what keeps you going when motivation drops.

Using MFFT's budget tracking tools during your no-buy challenge does three things:

1. Real-time progress visibility Instead of guessing how much you've saved, you see it. "Day 15: I've saved $340 so far." That number grows visibly. Your brain notices. Motivation increases.

2. Trigger identification MFFT's expense categorization shows patterns. You log your spending, and suddenly you see: "Okay, $180 of my overspending is coffee, $240 is subscriptions, $320 is food delivery." This granularity is what let Sarah, Marcus, and David adjust their strategies.

3. The net worth milestone When you complete your 30 days and your savings hit the account, your net worth visibly increases in MFFT. You're not just saving money—you're building wealth. That milestone moment is psychologically powerful.

Track your no-buy challenge in MFFT's budget mode during the month. Then watch your net worth jump when you deposit the savings. That's the feedback loop that builds momentum.

After the Challenge: Making It Stick

Here's the uncomfortable truth: most people complete a 30-day no-buy challenge and then rebound. They spend more to "make up" for the deprivation. Psychologists call this the deprivation rebound effect.

It's real. It's predictable. And it's 100% avoidable with the right transition strategy. One more perception trap worth knowing: if the savings pile up and you still feel broke, that's not a money problem — that's money dysmorphia, and it has its own fix.

The Rebound Risk

When Day 31 hits, your brain expects relief. "The challenge is over, I can shop now." If you don't plan for this moment, you'll spend $500+ in Week 5, erasing your gains.

The Solution: Plan Your Re-Entry Budget

Instead of going cold-turkey from restriction to freedom, plan a modest spending budget for Week 5.

Say you saved $600 in your challenge. Allocate $150 of it to a "re-entry budget" in Week 5. That $150 is permission to buy something you genuinely want—but intentionally, not automatically.

The other $450 stays invested.

This small permission prevents the rebound. Your brain gets relief without sabotaging your savings.

The Habit Sticking Strategy

Research shows that 3-4 habits from your challenge will naturally stick. Food delivery reduced, coffee from home instead of the shop, fewer subscriptions.

To lock these in:

- Don't call them restrictions anymore. Call them "my new normal"

- Automate the good ones. Home coffee: set up a subscription to great beans. Cooking: weekly meal planning every Sunday

- Replace the dopamine source permanently. If you replaced shopping with free activities (hiking, library), schedule them recurring in your calendar

The magic is that these replacements cost nothing and feel good. You're not sacrificing. You're gaining.

Conclusion: The No-Buy Challenge as Your Financial Reset Button

Here's what we've covered:

Per Intuit's research, 93% of Americans plan changes to how they manage money this year — and 49% specifically commit to more mindful spending. The no-buy challenge is the most effective first step because it's time-bounded, clear, and proven to work.

Most people fail because they hit five predictable psychological barriers. But once you understand the barriers, avoiding them is simple: reframe slips as data points, replace shopping with dopamine alternatives, clarify your rules, start with 30 days, and build community.

A 30-day no-buy challenge saves $300-$800 depending on your baseline. Run four per year: $1,200-$3,600 in annual savings. Invest those savings at 7% returns over 30 years: $850,000 to $5.4 million in additional wealth.

And here's the thing most people miss: it's not really about the money saved in 30 days. It's about the habits and clarity you build. The person who completes a no-buy challenge makes different choices forever. They understand their triggers. They know what they actually value. They've tasted financial control.

When your challenge is complete, take control of your finances by turning the insights you've gained into permanent budgeting habits. Track your challenge in MFFT, celebrate your milestones, and when Day 30 hits, remember that the real victory isn't the savings. It's the shift in how you see money.

The no-buy challenge isn't a month of restriction. It's a month of reset that ripples across the rest of your life.

Ready to start? Join the 70,000-member Reddit no-buy community, tell a friend, and commit to 30 days. Your future self—the one looking at a portfolio that's compounded for 20+ years—will thank you.

📩 Have questions about your specific no-buy plan? Email me at dennis.vymer@myfinancialfreedomtracker.com. And if you want to track your savings and see how your 30-day reset compounds into wealth, use My Financial Freedom Tracker to visualize your progress.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.