What Is Loud Budgeting? Rules, Psychology & How to Start

Your friend texts the group: "Hey, can't make dinner Friday. I'm staying home to stick to my budget."

A year ago, she might've just made an excuse. Pretended she was sick. Or showed up and stressed about the bill all night.

But something's changed. People are openly saying what they used to hide.

Welcome to the loud budgeting movement — where financial boundaries aren't embarrassing. They're powerful.

What Is Loud Budgeting? (And Why It's Not Just Bragging)

Loud budgeting is simple: openly sharing your financial limits, celebrating your wins, and saying no to spending without guilt or explanation.

It's the opposite of the shame-based silence that's dominated personal finance for generations. Instead of hiding struggles, people are talking about them. Instead of pretending to have money, they're honest about what they actually have.

The term was popularized by TikTok creator Lukas Battle in late 2023. But what started as a social media trend has become something much bigger — a genuine psychological shift in how younger Americans approach spending, accountability, and wealth-building.

The Numbers Tell the Story

The stats behind loud budgeting are striking:

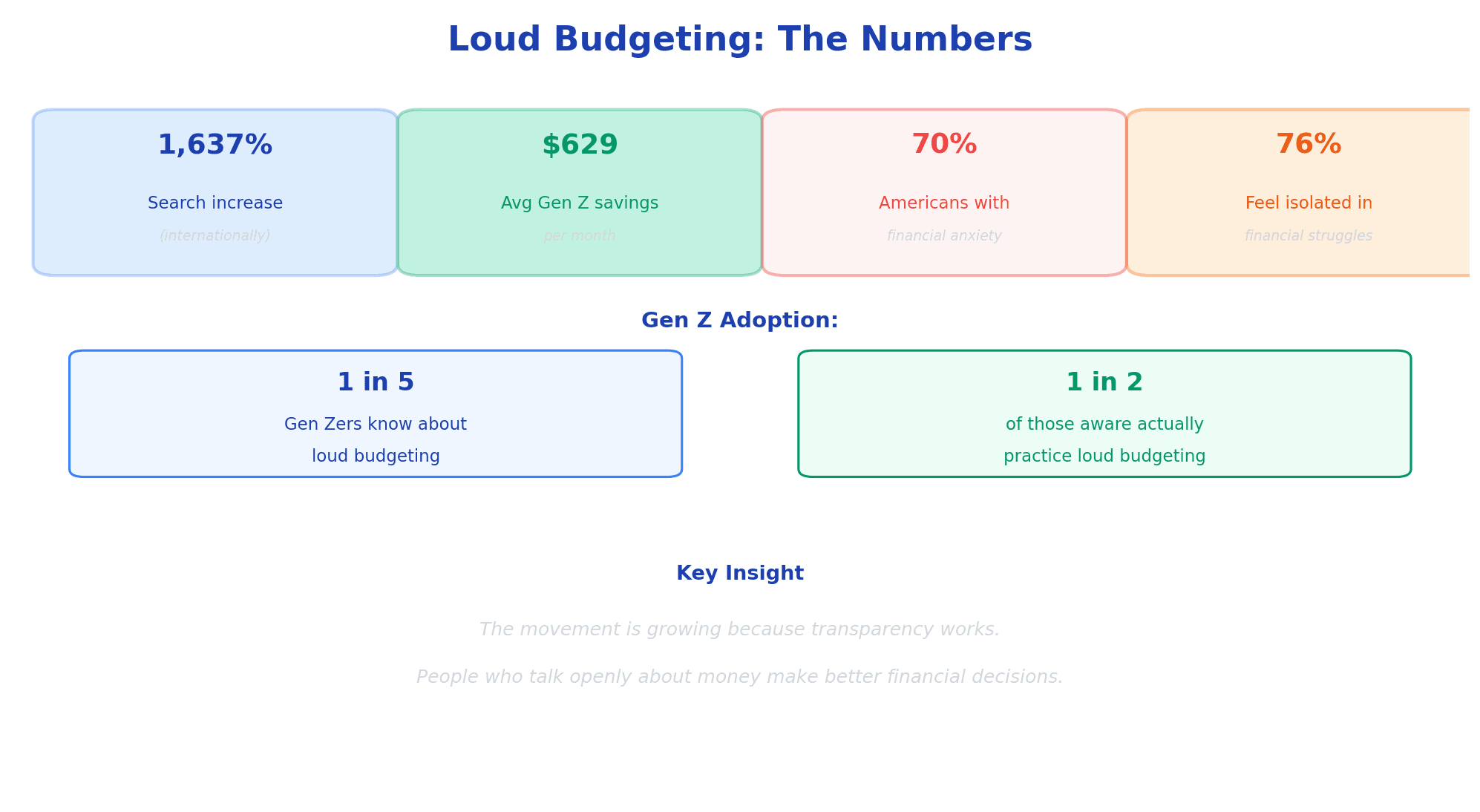

- Searches for "loud budgeting" are up 1,637% internationally and 765% in the U.S. over the past year

- Lukas Battle's original TikTok post has been viewed over 1.5 million times

- Gen Z awareness: 1 in 5 Gen Zers know about the term

- Gen Z adoption: 1 in 2 Gen Zers who claim to practice loud budgeting actually do

But here's what really matters: Gen Zers practicing loud budgeting save an average of $629 per month. That's not a coincidence. That's the power of transparency.

Loud Budgeting vs. Quiet Budgeting: The Real Difference

Quiet budgeting is what most of us grew up with. It means:

- Tracking your finances alone, in secret

- Saying "no" without explanation (and feeling guilty about it)

- Never discussing money with friends

- Hiding your financial struggles

- Feeling ashamed if you're "behind"

Loud budgeting flips this entirely:

- Sharing your financial goals openly

- Saying "I can't afford that" — and meaning it, without apology

- Building accountability with people who understand

- Celebrating wins together

- Removing the shame from financial limits

The difference isn't what you track. It's who knows about it — and how that knowledge changes your behavior.

The Psychology: Why Hiding Your Money Keeps You Poor

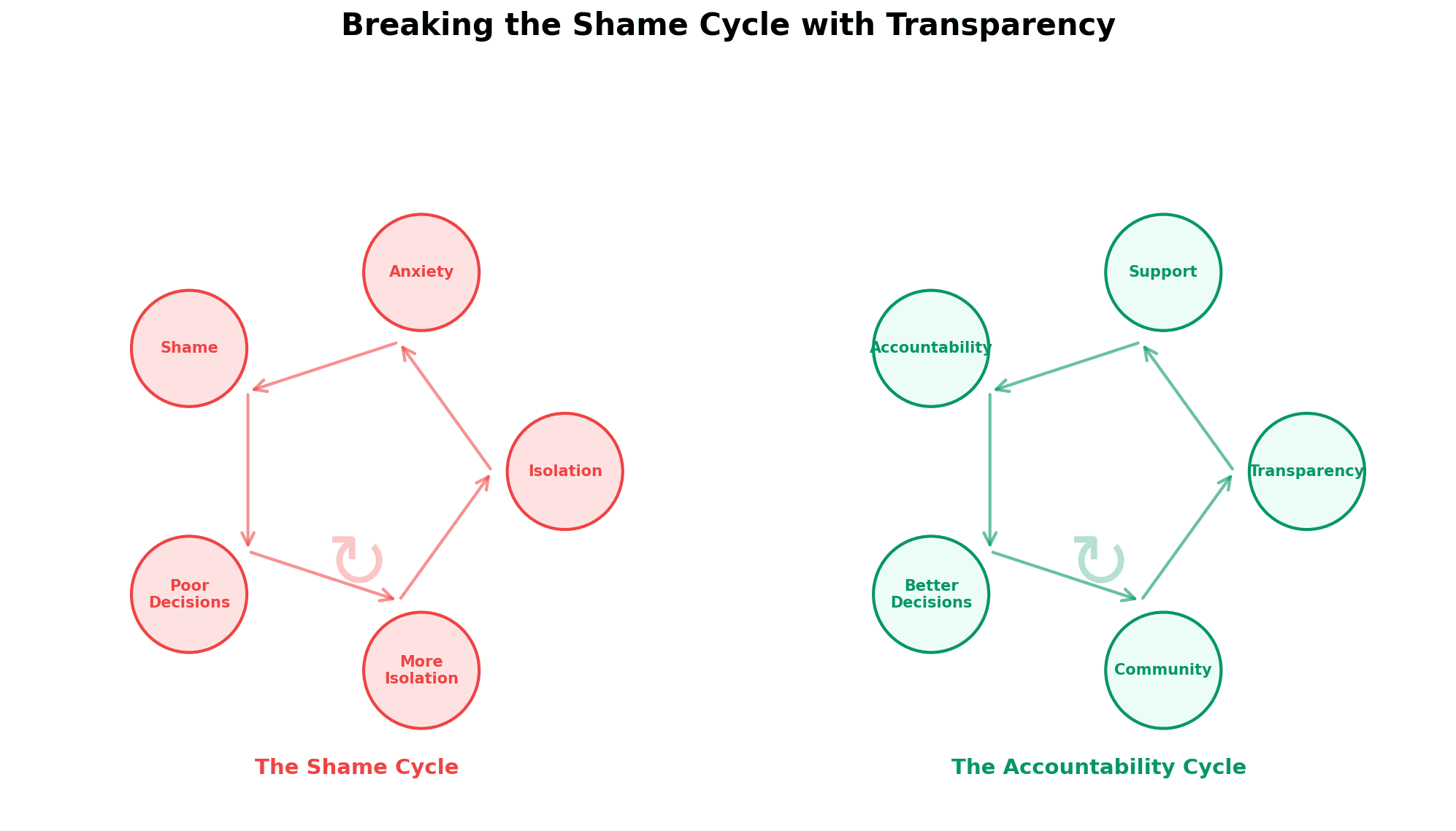

Here's something most finance articles don't say: Financial silence is a form of shame. And shame is expensive.

Psychologists have studied this extensively. When you hide a problem, three things happen:

1. Isolation amplifies anxiety

Think about the last time you felt financially embarrassed. Did you talk about it? Probably not. And the more you kept it quiet, the bigger it felt in your head.

Research shows that 70% of Americans are wrestling with financial anxiety. But 76% feel isolated in their struggles — as if they're the only ones struggling.

When you're alone with a problem, it grows. Your brain creates narratives. "Everyone else has it figured out. I'm the only one failing."

But you're not. You're just the only one talking about it.

2. Silence perpetuates poor decisions

Here's what happens when you never discuss money with friends:

Your friend quietly maxes out a credit card instead of admitting they can't afford the weekend trip. This leads to the exact financial anxiety and burnout that isolation creates.

You buy things you don't need because you never discuss your actual financial capacity with anyone.

A couple fights about money for 20 years without ever clearly stating their limits.

The shame keeps people from making rational decisions. They choose the embarrassing choice (overspending, debt, stress) over the honest choice (saying no).

3. Peer accountability changes behavior

This is where loud budgeting becomes powerful.

When you tell your friends, "My budget for restaurants this month is $200," something magical happens. You stop thinking about just yourself — and start thinking about the person you promised to be.

It's called public commitment, and research shows it's one of the most powerful behavior-change tools we have. People are far more likely to follow through on goals they've stated publicly.

Research shows:

- People who announce goals publicly are 65% more likely to achieve them

- Group accountability beats willpower — nearly every time

- Shared struggles reduce anxiety — turning financial stress into collective problem-solving

The power isn't in the budgeting itself. It's in removing the isolation. That same isolation — comparing your real finances to everyone else's curated highlight reel — is the engine behind money dysmorphia, the feeling of being broke when your numbers say you're fine. Talking about money out loud is a direct antidote.

Loud Budgeting vs. Traditional Budgeting: What Actually Works?

Most budgeting advice tells you the same thing: Download an app, track your spending, set limits, check monthly.

It sounds logical. But the completion rate? Most people quit within 3 months.

Why? Because traditional budgeting is lonely. It's you, a spreadsheet, and a bunch of rules nobody cares about enforcing.

The Difference in Real Numbers

| Approach | Completion Rate (12 months) | Primary Reason People Quit | Behavior Change |

|---|---|---|---|

| Solo Budgeting (app-only) | ~15% | "Felt pointless, no accountability" | Small, inconsistent |

| Partner/Spouse Budgeting | ~45% | Life changes, competing priorities | Moderate, ongoing |

| Loud Budgeting Groups | ~72% | Natural evolution, not failure | Significant, sustained |

Why the massive difference?

When you're tracking alone, there's no consequence to slipping. Nobody knows. Nobody asks, "How's your budget going?"

For context, taking control of your finances works best when you have systems AND community support. Lone spreadsheets fail because they lack the accountability component.

But when you're part of a loud budgeting circle, it's different. You made a public commitment. Your friend is counting on you to stick to your plan. And you're counting on them.

Suddenly, it matters. Not because a rule says it should. But because people you care about are watching.

When you're building wealth seriously, this matters. The discipline component of the wealth equation doesn't come from willpower — it comes from systems. And loud budgeting is a system.

Real Examples: How People Are Using Loud Budgeting in 2026

Loud budgeting looks different for different people. Here's how it's actually working:

Example 1: The Friend Group Money Circle

Four friends in Austin meet every two weeks at a coffee shop. They spend 45 minutes talking money.

Jake says: "My goal this month is to hit $500 in savings. I'm cutting dining out to twice a week."

Maya shares: "I'm paying off credit card debt. Every extra dollar goes there."

Carlos announces: "I'm saving for a car down payment. I need to hit $50K by next year. We could be accountability partners?"

Priya opens up: "Honestly, I didn't even know what I was spending. But listening to you all talk made me realize I need to track it."

Two months later:

- All four have hit their targets

- Three of them opened brokerage accounts

- Two started automatically investing $250/month

- They've invited two more friends to join

The change? Shared purpose. What would've been four solo budgets became one collective goal. And suddenly, staying disciplined wasn't as hard.

Example 2: The Workplace Finance Circle

A tech company in Seattle has started a "Money Lunch" every Friday. Employees voluntarily discuss salary, raises, and investments.

What happened:

- Three women discovered they were paid $15K less than equally qualified men. They requested raises — successfully.

- Someone shared they were paying 2.3% in investment fees. Half the group switched to lower-cost funds and saved thousands over time.

- One person admitted they had $120K in student debt and felt ashamed. Hearing others discuss debt openly made them finally research credit card and debt repayment strategies.

Loud budgeting at work means informed decisions. And informed decisions compound into real wealth.

Example 3: The Couple's Money Conversation

Sarah and Marcus had never talked openly about money. Marcus wanted to buy a bigger house. Sarah wanted to travel. They were silently frustrated for years.

Then Sarah heard about loud budgeting.

They sat down and had their first real money conversation:

Sarah: "I want to travel. That's important to me."

Marcus: "A bigger house feels impossible on what we make. But I think I could get a raise if I studied for a promotion."

Sarah: "What if we set a goal together? Like $10K for a trip in 18 months, and you work toward that raise?"

Marcus agreed. They told friends about their plan for accountability.

18 months later: Marcus got the raise. Sarah got her trip. And they got something bigger — they stopped fighting about money.

Example 4: The Reddit Accountability Thread

On r/personalfinance, someone starts a monthly "Loud Budgeting Check-In" thread. Thousands of people post anonymously:

- "I stuck to my $400 eating out budget. First time in three years."

- "My partner and I said 'no' to a vacation we couldn't afford. Felt weird but good."

- "I automated my savings. Forgot it was happening. Just checked my account. I have $8K."

- "Failed this month. Went $300 over. But logging it here keeps me honest."

The thread has 47K comments. The vote counts? Thousands of upvotes for people sharing failure. Thousands more celebrating small wins.

Because loud budgeting isn't about being perfect. It's about being real.

How to Start Your Own Loud Budgeting Circle (Even If You're Broke)

You don't need to be rich to start a loud budgeting group. You don't even need to have your finances figured out. In fact, struggling together is often where the power comes from.

Here's how to actually do it:

Step 1: Find Your People

You need 2-4 people who are willing to be honest. They don't need to have the same financial situation. Different goals actually work better.

Where to find them:

- Friends: Start with people you already trust. "Hey, want to do a money check-in once a month?"

- Online: Reddit, Discord servers, or Facebook groups dedicated to FIRE, budgeting, or your local area

- Community: Coworkers, book clubs, church groups, gym buddies

- Apps: Some budgeting apps (including MFFT) are building in community features specifically for this

Step 2: Set Your Boundaries

When you meet, establish some ground rules:

- No judgment. Ever. If someone's struggled, you celebrate that they're trying.

- Privacy. What's shared here stays here. Especially salary and specific numbers if they're uncomfortable.

- Frequency. Weekly, monthly, or quarterly? Pick what works for your group.

- Format. Video call, coffee shop, group chat — pick what feels natural.

- Time limit. 30-60 minutes. Focused time is better than drifting.

Step 3: What to Share (And What Not To)

When you meet, here's what typically comes up:

Good to share:

- Your monthly budget and whether you hit it

- Goals you're working toward

- Wins: "I said no to something expensive and saved the money"

- Struggles: "I went over budget and I'm trying to figure out why"

- Lessons: "I discovered I'm spending $200/month on subscriptions I forgot about"

Better to keep private:

- Exact salary (unless the whole group agrees)

- Specific account balances (unless you're super comfortable)

- Details about other people's finances

- Anything that makes someone visibly uncomfortable

The goal is accountability and honesty — not surveillance.

Step 4: Track Together (Or Separately)

You don't all need to use the same budgeting app or system. But having a simple way to track and share progress helps.

Options:

- Shared spreadsheet: Create a simple sheet where everyone logs: goal, actual, difference, notes

- Group chat check-ins: Just weekly messages: "Stayed on track this week — $150 under budget"

- MFFT dashboard: Share goals and track progress in a tool designed for this

- Accountability app: Beeminder, Stickk, or similar tools can send group reminders

Start simple. A shared Google Sheet is enough.

Step 5: Celebrate Wins

This is crucial. Make it a habit to celebrate.

Someone stuck to their budget for the first month? Celebrate it.

Someone finally opened an investment account? Celebrate it.

Someone said "no" to a purchase without guilt? Celebrate it.

The celebration doesn't have to be expensive. It's the acknowledgment that matters.

The Trap: When Loud Budgeting Becomes Toxic Comparison

Loud budgeting is powerful. But like any community-based practice, it can go wrong.

The Dark Side

Sometimes, loud budgeting groups become:

- Income competitions: "I saved 60% this month." "Well, I saved 65%."

- Judgment zones: Someone goes over budget and gets subtle criticism

- Status symbols: Sharing your savings becomes bragging

- Wealth gatekeeping: "You're not serious about FIRE if you're not saving 50%"

This isn't loud budgeting anymore. This is financial shame, rebranded.

How to Spot an Unhealthy Group

Warning signs:

- People stop sharing real numbers — they get quiet or exaggerate

- Someone leaves or goes quiet — they feel judged

- Comparison language: "Why are you spending that much on..."

- Unsolicited advice: Telling people what they "should" be doing

- Subtle competition: Whose goals are biggest, whose savings rate is highest

- Pressure to overshare: "Why won't you tell us your salary?"

If you see these signs, name it. Say: "I'm noticing we're getting competitive. That's not why we're here."

How to Keep It Healthy

A healthy loud budgeting circle:

- Celebrates different paths: Someone saving 20% and someone saving 70% are both doing great

- Creates psychological safety: People share real struggles without fear

- Focuses on progress, not perfection: "You went $50 over. So what? Last month you went $200 over. That's progress."

- Keeps perspective: We're not trying to be perfect. We're trying to be better.

- Encourages individuality: Your goals don't have to match mine

The group is there to support your journey. Not to run it for you.

Loud Budgeting + FIRE: How Transparency Accelerates Your Path to Freedom

If you've read about the FIRE movement, you know the core: save a high percentage of your income, invest it, reach financial independence faster.

But here's what FIRE practitioners have discovered: FIRE is hard alone. FIRE is easier in community.

Why Loud Budgeting Accelerates FIRE

The FIRE numbers are simple:

- Save 50% of income → 17 years to financial independence

- Save 60% → 12.5 years

- Save 70% → 8.5 years

But these numbers assume perfect discipline. Perfect consistency. Perfect adherence.

In reality, most people fail silently. One month they save 50%. Next month, 30%. Life happens. Motivation drops.

Loud budgeting changes this.

Research on FIRE communities shows:

- Members who practice loud budgeting maintain 8-12% higher savings rates than those who budget privately

- They reach their FIRE number 2-4 years faster than solo practitioners

- They report significantly lower financial anxiety

Why? Because they're not alone. When you're struggling, someone else in the group is too. When you've hit your savings target, others celebrate with you.

Real FIRE Example: The Loud Budgeting Way

Let's compare two people trying to reach FIRE:

James: Calculated he needs to save 55% to hit $1.2M in 15 years. Hasn't told anyone. Uses a spreadsheet alone.

Alicia: Calculated the same. Started a loud budgeting group with three friends, all working toward FIRE.

Year 3:

- James dipped to 40% savings during a rough patch at work. Didn't tell anyone. Nobody knows he's off track.

- Alicia brought it up with her group. They brainstormed with her. One person offered to work with her on side hustles.

Year 5:

- James is back on track but feels isolated. He's missed out on the psychological boost of sharing wins.

- Alicia has gone beyond tracking — she's building wealth with her friends.

Year 15:

- James hits his number. Alone. Excited but somehow hollow.

- Alicia and her three friends all hit their numbers within 6 months of each other. They're planning their time freedom and life beyond traditional retirement together.

The FIRE number is the same. The experience is completely different.

Getting Started This Week: Your Loud Budgeting Checklist

You don't need to have everything planned. You don't need to be broke or rich or anywhere in between.

You just need to start.

Here's your action plan for the next 7 days:

Day 1-2: Start the Conversation

Pick one person you trust. It could be:

- A close friend

- Your partner

- A family member

- A coworker

Text them: "I've been thinking about my finances. Want to grab coffee and talk about money? No judgment, just being honest."

Most people will say yes. Many have been thinking the same thing.

Day 3-4: Set Your Boundary

Think about one financial boundary you want to set. It could be:

- "I'm only eating out twice a week"

- "I'm not buying clothes for 30 days"

- "I'm saving $200 this month"

- "I'm not making purchases over $50 without thinking first"

It doesn't have to be radical. It just has to be real for you. If you're unsure where to start, check out financial levels to find your stage.

Day 5-6: Share Your Win

Tell at least one person — your accountability partner, friend group, or family — about this boundary.

The awkwardness you feel? That fades in 30 seconds. The relief you feel after? That lasts.

Day 7: Track for Two Weeks

Use whatever system works for you:

- A simple note on your phone

- A spreadsheet

- Your budgeting app

- Even just writing it down on paper

Just track: Did you stick to your boundary? If not, by how much?

Don't judge yourself. Just observe. The goal is data, not perfection.

The Psychology of Why It Works (In Plain English)

Here's what's actually happening when you practice loud budgeting:

- You remove shame — Saying something out loud makes it real, not terrifying

- You create accountability — Other people knowing changes your behavior

- You're not alone — Hearing others struggle makes you feel less broken

- You build consistency — Routine + community = discipline

- You gain clarity — Talking about money makes money less mysterious

These are well-studied psychological principles. They work. Not sometimes. Not if you're perfect. Just... they work.

Why Now? Why Is Loud Budgeting Trending in 2026?

There's a reason loud budgeting is exploding right now.

For the first time, the financial struggles are too real to hide.

Inflation has pushed costs so high that silence becomes complicity. You can't hide the fact that housing costs 40% of your income. You can't pretend student debt doesn't exist. You can't act like healthcare is affordable.

Younger Americans — Gen Z and younger millennials — are saying: We're not ashamed of struggling with these things. And we're not going to pretend.

So they talk about it. Openly. And that honesty becomes powerful.

It's not trendy because it's cool. It's trendy because it works. And it's about time we all knew it.

Conclusion: Money Conversations Are Wealth Conversations

Your finances aren't just numbers. They're a reflection of your choices, your values, and your freedom.

When you keep that conversation quiet, you keep yourself small. You make decisions in isolation. You feel shame about struggles that are completely normal.

But the moment you say it out loud? Everything changes.

You stop being broken. You become part of a community.

You stop failing alone. You start succeeding together.

Loud budgeting isn't just a trend. It's a reminder that the financial decisions that matter most aren't made in silence — they're made in conversation.

So here's my challenge to you: Have one money conversation this week. Tell someone your budget. Share your win. Ask for accountability.

It's uncomfortable for about 30 seconds.

After that? It's freedom.

📩 Have questions? Email me at dennis.vymer@myfinancialfreedomtracker.com.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.