Gen Z Retirement Math: Start at 22, Semi-Retire by 45-50

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Start a Budget — the first step to financial freedom

- What Is Investing? — core concepts, made simple

- The Complete Guide to FIRE — financial independence, explained

You're 22. Fresh out of college. Your first real paycheck just hit your account—maybe $3,500 after taxes if you're earning $40,000 a year.

A coworker who's 35 laughs when you mention starting retirement savings. "You've got like 40 years. Why rush? Wait until you're making real money."

Fast forward 13 years. You're 35. And something magical has happened—even though you never made a huge income, even though your salary only crept up to $55,000, you've accumulated enough that you could cut your hours in half tomorrow and still be fine.

Meanwhile, that coworker? Still working full-time. Still saying "next year I'll save more."

This isn't a fantasy. This is Gen Z's unfair advantage. And it's a math problem, not a motivation problem.

The Gen Z Advantage: Why Starting at 22 Changes Everything

Let me show you the data first, then explain why it matters so much.

Gen Z is starting retirement savings at an average age of 19-22. That's 15 years earlier than Gen X (age 34) and 20 years earlier than Baby Boomers (age 40). And here's the kicker—63% of Gen Z say they're confident they'll be financially prepared for retirement, higher than any other generation.

That confidence isn't naive. It's mathematical.

A 22-year-old with 40+ years ahead has an advantage that no amount of high income can replicate for someone starting at 35. We're talking about the raw power of time and compound interest.

Think about it this way: Traditional retirement focuses on "working as long as possible to save as much as possible." Gen Z's approach flips this entirely—it's about "starting as early as possible, then letting compound interest do the work."

The psychological shift is just as important. Instead of "I have to work until 65," it becomes "I'm building toward a point where I can choose my work." That's not a small thing. That's freedom.

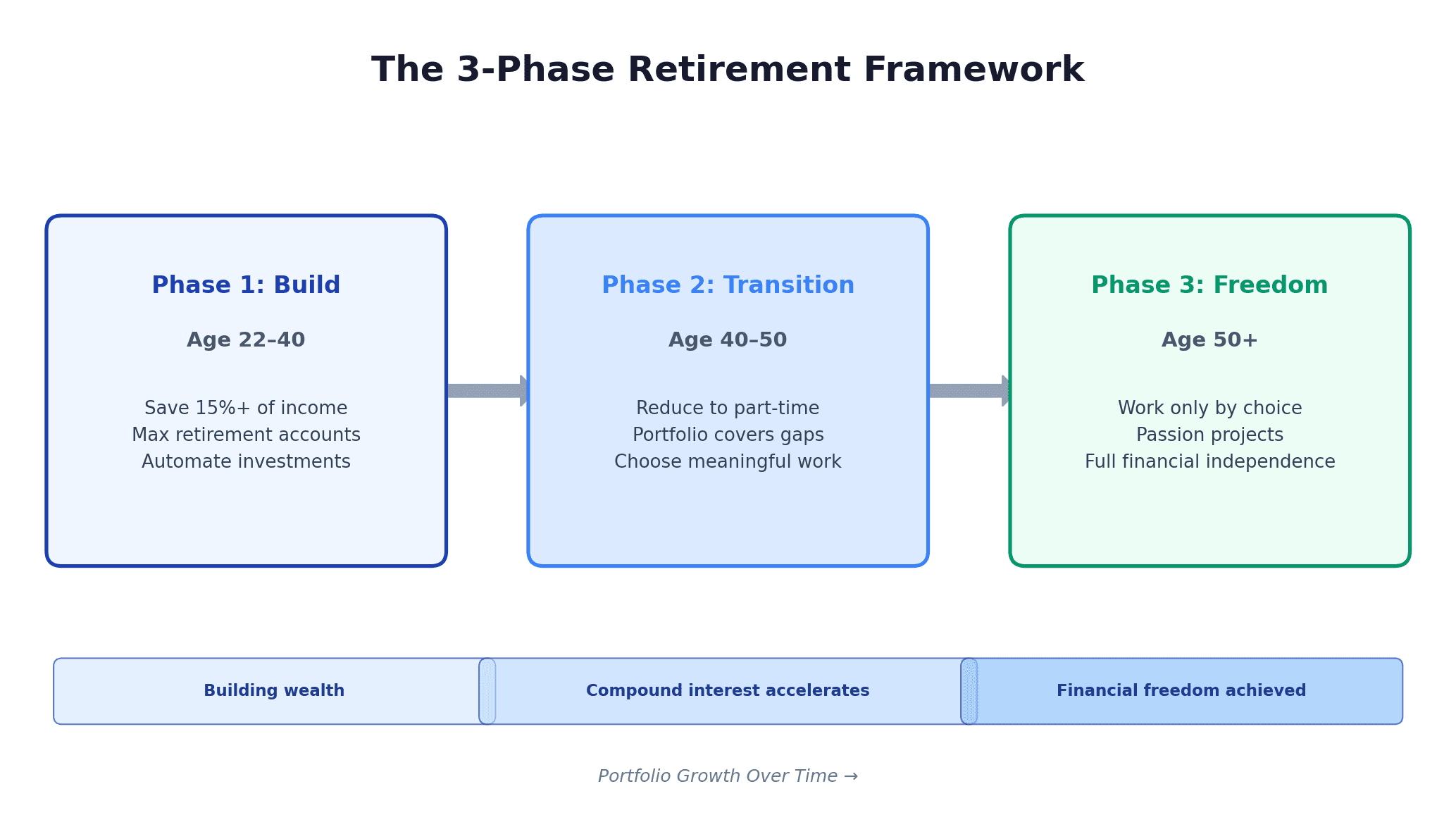

The New Retirement Playbook: Phased Freedom Over Complete Exit

Here's what I notice when I talk to Gen Z about retirement: they don't want to "stop working." They want to stop needing to work.

That's a huge distinction. And the data backs it up.

Research from the Transamerica Institute shows that 48% of Gen Z workers envision retiring by gradually reducing their hours—not by quitting everything at once. About 41% plan to reduce work hours with more leisure time. Another 39% plan to shift to less demanding work while reducing responsibilities.

Compare that to the traditional FIRE movement, which sells this idea of "quit your job, never work again." The stress of that binary choice has actually hurt early retirees. Psychologists have documented "FIRE regret"—people who hit their number and immediately felt purposeless and lost.

Gen Z is solving this problem before it starts.

Phased retirement means:

- Age 22-40: Build your financial foundation with aggressive saving

- Age 40-50: Transition to part-time work or consulting (cutting hours by 50%)

- Age 50+: Work only on things that matter to you—passion projects, part-time consulting, creative work

You're not calculating "how much do I need to live on zero income forever?" Instead, you're asking "how much do I need so that part-time work covers my expenses?"

That's a dramatically smaller number.

The Math: From $40K Salary to Financial Freedom by 45-50

Let me walk you through real numbers. This is crucial because this is where it stops being theory and becomes your actual situation.

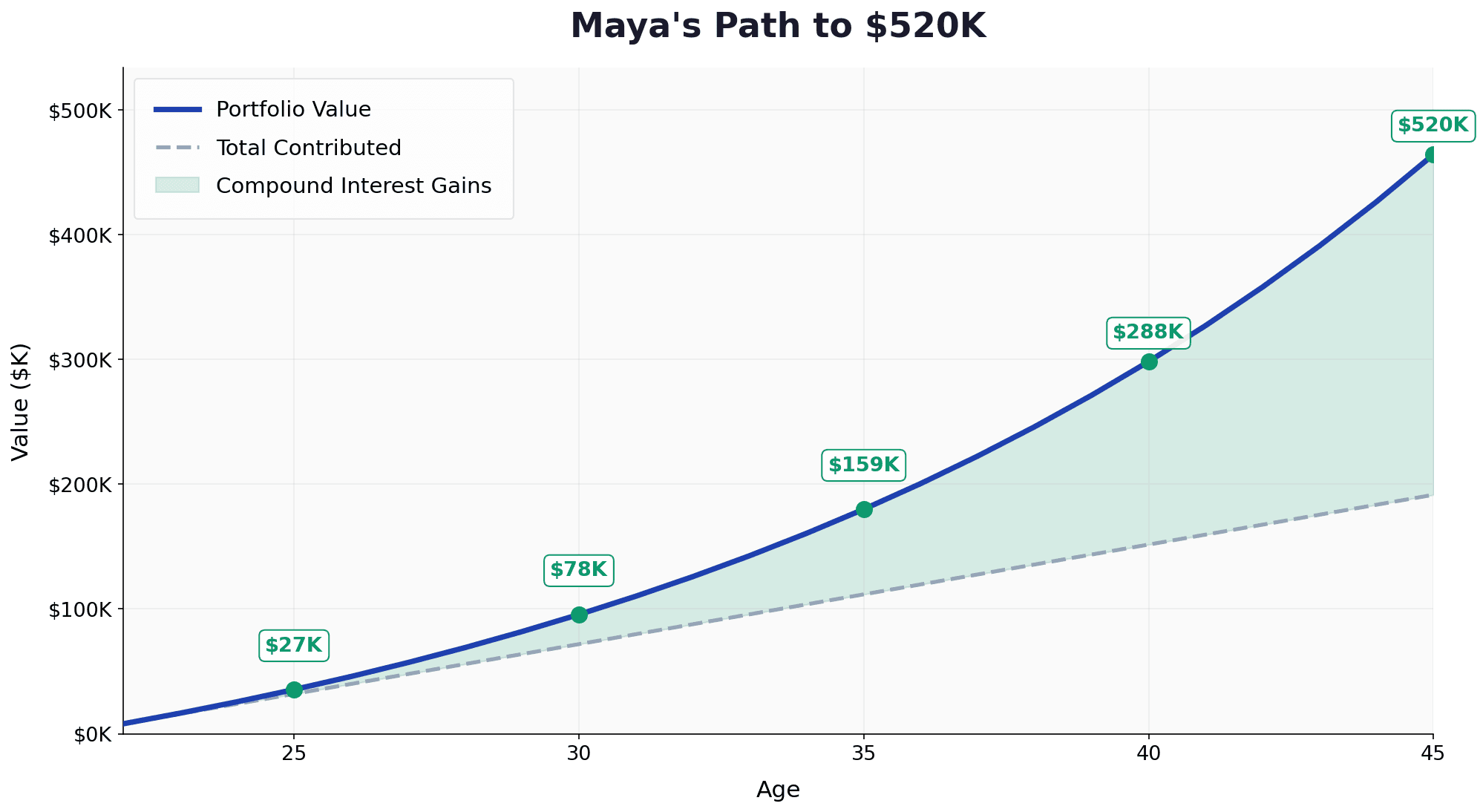

Scenario: Meet Maya

Maya graduates at 22 with a $42,000 marketing salary. She's got $8,000 in student loans at 5% interest, but she's committed to making this work.

Here's what Maya does:

- She contributes 15% of gross salary to retirement accounts = $6,300/year

- Her employer matches 4% = $1,680/year

- Total invested annually = $7,980

Over 23 years (until age 45), at a historical 7% average return, this grows to approximately $520,000.

Now here's the magic part: at age 45, using the 4% rule, Maya can withdraw $20,800 per year from this portfolio without touching principal. If she reduces to part-time work earning $25,000/year, she has a total of $45,800 annually—enough to live comfortably in most American cities.

She hit financial freedom without a six-figure income. Without luck. Without waiting for a promotion.

Let me show you the timeline:

| Maya's Age | Annual Savings | Portfolio Value | Notes |

|---|---|---|---|

| 22 | $7,980 | $0 | Start |

| 25 | $7,980 | $27,000 | 3 years in |

| 30 | $7,980 | $78,000 | Still looks small |

| 35 | $7,980 | $159,000 | Compound interest accelerates |

| 40 | $7,980 | $288,000 | Getting real now |

| 45 | $7,980 | $520,000 | Freedom achieved |

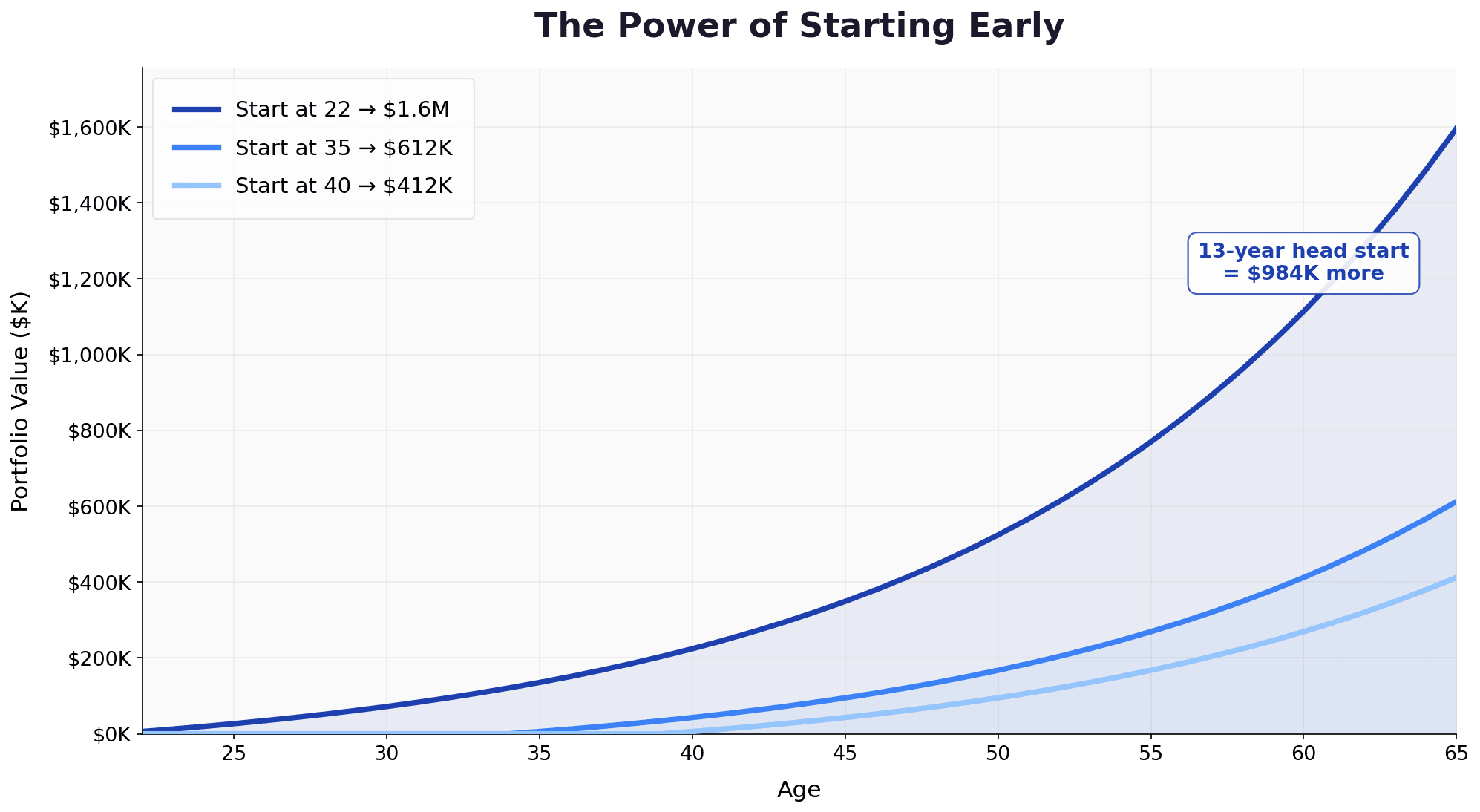

The Compound Interest Secret: Small Choices, Huge Outcomes

Here's a comparison that will blow your mind. This is why starting early is so powerful.

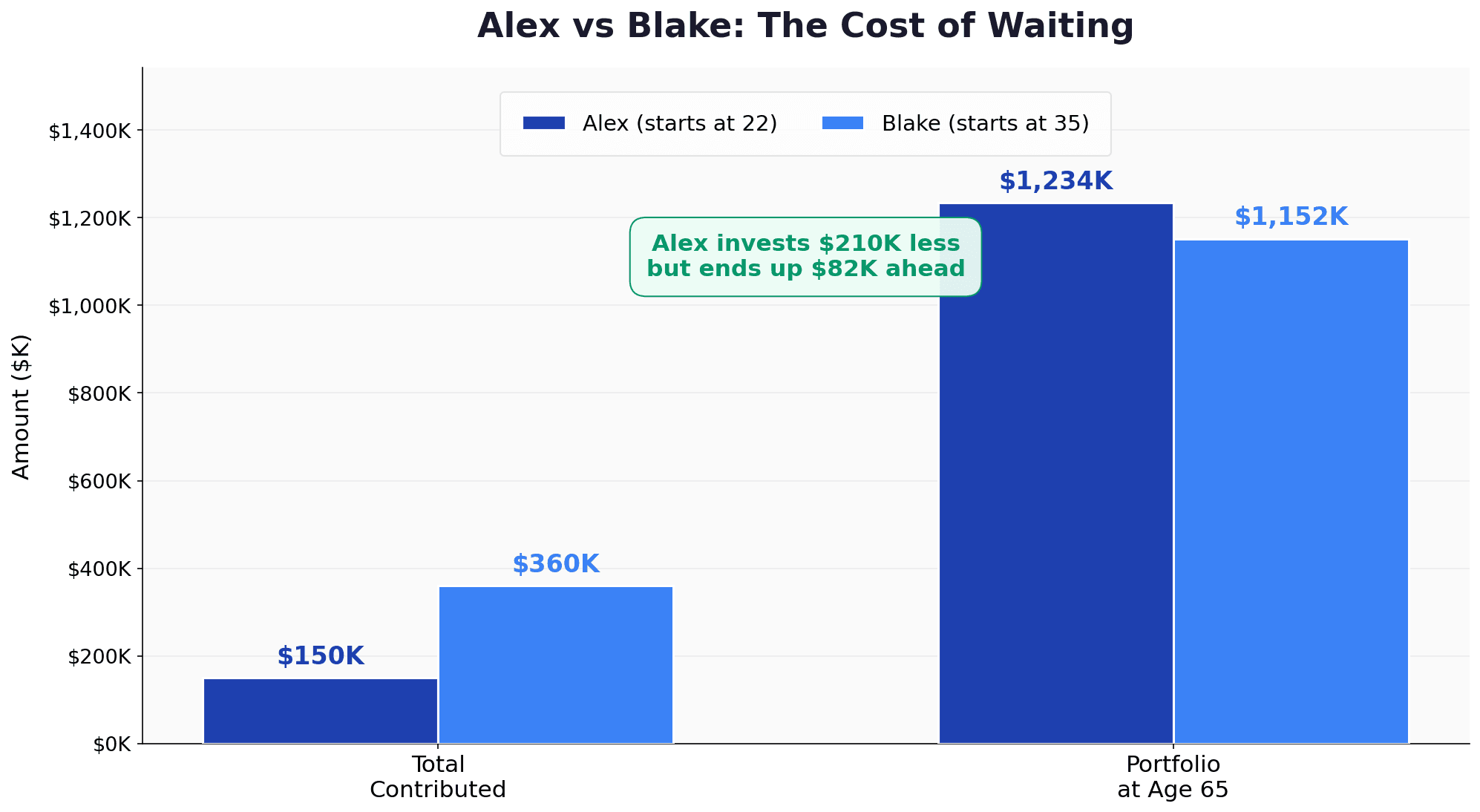

Scenario A: Alex, starting at 22

- Saves $6,000/year for 25 years (age 22-47)

- Then stops completely—doesn't invest another dollar

- Total contributions: $150,000

- Value at age 65: $1,234,000

Scenario B: Blake, starting at 35

- Waits 13 years, then starts saving

- Saves $12,000/year for 30 years (age 35-65)

- Doubles the annual amount, invests twice as long

- Total contributions: $360,000

- Value at age 65: $1,152,000

Read that carefully. Alex invested half the money for a shorter time period and ended up with $82,000 more.

Why? Because Alex's early money had 40 years to work instead of 30 years.

This is the entire concept of Coast FIRE—that moment when you've invested enough that compound interest finishes the job without you adding another dollar.

For Alex, that moment came around age 47. From that point on, the money just grew. For Blake, it never comes—he has to keep saving until 65.

The cost of waiting 13 years? Over $360,000 in additional contributions just to fall slightly behind.

Beyond 401(k)s: The Multi-Stream Approach Gen Z Is Using

Most people think retirement investing is just "contribute to your 401(k) and that's it." Gen Z is getting smarter than that.

The real strategy involves layering different accounts, each with different tax advantages:

1. Employer 401(k) with Match (free money)

- Contribute enough to capture the full match (usually 3-6%)

- This is mandatory. You're literally leaving money on the table otherwise

2. Roth IRA (tax-free growth forever)

- $7,000/year limit (2026)

- Your contributions grow tax-free

- Withdrawals in retirement are tax-free

- Perfect for early career when you're in a low tax bracket

3. HSA (Health Savings Account) (triple tax advantage)

- $4,150/year limit (2026)

- Contributions are tax-deductible

- Growth is tax-free

- Withdrawals for medical expenses are tax-free

- After age 65, you can withdraw for anything (just pay income tax like a traditional IRA)

- Most people don't realize they can use this as an extra retirement account

4. Taxable Brokerage Account (for flexibility)

- No contribution limits

- Can withdraw anytime without penalties

- Long-term capital gains taxed at preferential rates (potentially 0% if your income is low)

Here's how this looks in practice for someone earning $48,000:

| Account | Annual Contribution | Tax Advantage |

|---|---|---|

| 401(k) to match | $1,920 (4%) | Tax-deferred |

| Roth IRA | $7,000 | Tax-free growth & withdrawals |

| HSA (if eligible) | $4,150 | Triple tax advantage |

| Taxable brokerage | $5,000 | Low capital gains rate |

| Total | $18,070 | Diversified across 4 accounts |

That $18,070 is roughly 38% of gross income—aggressive, yes, but possible. And most importantly, it's spread across different accounts, giving you flexibility that a single 401(k) never could.

The Psychological Edge: Why "Retiring Into Something" Beats "Retiring From Something"

Here's something researchers noticed about early FIRE adopters in their 40s and 50s: many of them struggled with purpose and identity after quitting.

Some describe a kind of emptiness. They'd spent decades working toward a number, hit it, quit—and suddenly had no structure, no community, no meaning.

It's called "one more year syndrome." People who should retire don't, because retirement itself feels empty.

Gen Z's phased approach solves this entirely.

By not making retirement about "quitting everything," you're instead asking "what would I want to do if I didn't need the money?" That's a completely different question. And it means when you hit your number, you're not starting from zero. You've already thought about what comes next.

Maybe it's consulting in your field at half hours. Maybe it's finally starting that side project you've been putting off. Maybe it's mentoring, teaching, creating, or something nobody's thought of yet.

The data on this is clear: people are happiest when they have challenge, purpose, and autonomy. Traditional retirement removes all three. Phased retirement maintains them.

Plus, here's the practical benefit: if part of your phased retirement income comes from work you enjoy, you're far less likely to make emotional financial decisions or deplete your portfolio too quickly.

You've essentially created a time freedom situation where your portfolio is a safety net, not your entire lifeline.

Common Traps Gen Z Should Avoid

This system works beautifully—if you avoid a few predictable pitfalls.

Trap #1: Lifestyle Inflation

You get a 10% raise. Your salary goes from $45,000 to $49,500.

What happens? Your spending usually creeps up by... about 10%. New apartment, nicer car, better restaurants. Suddenly you're saving the same dollar amount as before, just on a higher income.

Solution: Every time you get a raise, commit to putting 50% of the increase toward retirement accounts. If you get $4,500 extra, save $2,250 and enjoy the other $2,250. Your lifestyle improves, but your progress compounds.

Trap #2: Analysis Paralysis

"I want to invest, but I need to find the perfect fund first."

Meanwhile, months pass and you've invested... nothing.

Solution: There is no perfect fund. A simple portfolio of broad index funds (total market or target-date funds) beats 90% of active investors after fees. Start with "good enough" today instead of waiting for "perfect" next year.

Trap #3: Lean FIRE Without a Safety Net

The formula often taught is "save 50% of income, spend the other 50%, and you can retire in 17 years." Sounds great. But 50% spending doesn't account for:

- Healthcare (the big one—$10K-$20K/year before Medicare at 65)

- Unexpected major expenses

- A serious market crash in year one of retirement

Solution: The phased approach actually handles this. You're not retiring on 100% portfolio withdrawals. Part-time work covers most basics, and the portfolio is your cushion. That's why 45-50 is more realistic than 35.

Trap #4: Not Tracking Progress

You know you're "saving something," but you don't know if you're on track. You don't update your math. You never calculate your personal "freedom number."

This is huge because what gets measured gets managed. People who track their net worth quarterly hit their goals. People who don't usually give up around year 5 because they lose sight of progress.

Solution: Use a tool like My Financial Freedom Tracker to monitor your net worth monthly. See the portfolio grow. Make it visual. That momentum matters psychologically.

Your 2026 Action Plan: The Gen Z 22-50 Retirement Framework

Alright. You understand the math. You understand why phased retirement works. Now—what do you actually do?

Here's the concrete framework:

Month 1: Set Up Your Accounts

Week 1: Open a Roth IRA with Vanguard, Fidelity, or another no-fee broker. Choose a target-date fund (like "Vanguard Target Retirement 2065 Fund"). This requires one click. Seriously.

Week 2: Enroll in your employer's 401(k) plan. Contribute enough to capture the full employer match (ask HR what that percentage is). Set it to auto-increase by 1% every year.

Week 3: If you have a high-deductible health plan, open and max out your HSA ($4,150 for 2026). Invest the money rather than keeping it in cash—it's a long-term account.

Week 4: Calculate your personal "freedom number" using the 4% rule: (monthly expenses you'd be happy with) × 12 × 25.

Ongoing: Automate Everything

Set up automatic transfers on payday:

- 4-6% to your employer 401(k) (auto-increased by 1% annually)

- $583/month to your Roth IRA (= $7,000/year)

- $346/month to your HSA (= $4,150/year)

- Whatever you can spare to a taxable brokerage account

The key word: automatic. You don't need discipline if you never see the money.

Quarterly: Check Your Progress

Spend 15 minutes every three months:

- Log into your brokerage accounts

- Add up your total net worth

- Compare it to last quarter

- Notice the compound interest working

That $50,000 you invested in year one? It's now generating returns. Those returns generate their own returns. The curve gets steeper every year.

Annually: Recalculate and Adjust

Each year, answer these questions:

- Did my income increase? Redirect 50% of the raise to retirement accounts.

- Did my expenses change? Recalculate my freedom number.

- Am I still on track? (Compare your portfolio to your projected timeline.)

- Should I increase my contribution rate? (Can I push from 15% to 17%?)

This is especially important if you get windfalls—bonuses, tax refunds, inheritance. Every additional dollar matters at this stage.

The Inheritance Wildcard: 70% of Gen Z Expect Family Assets

I need to address this because it's real and it changes things.

68% of millennials and Gen Z have received or expect to receive an inheritance averaging $320,000. Some expect far more. And statistically, inheritances often come in your 30s-40s—right when you're building momentum toward your freedom number.

Here's my view: don't count on it, but plan for it.

If it doesn't come: You're fine. You hit your number through disciplined saving and compound interest. You built it yourself.

If it does come at 35: Incredible. Now you have choices. Pay off the mortgage? Max out your retirement accounts for years? Move toward part-time work sooner than planned? You have optionality.

If it comes at 50: Even better. Your portfolio is already substantial. The inheritance becomes acceleration toward a very comfortable phased retirement.

The key: don't anchor your retirement plan to an expectation. The inheritance is a bonus, not the foundation.

Is This Real or Just for High-Income Tech Workers?

I need to smash this myth because it's the biggest reason Gen Z doesn't start.

"This only works if you earn $150K+," people say. Wrong.

Let me show you three scenarios at different income levels:

Scenario A: $40K Salary

- Annual savings: 15% = $6,000

- Employer match: 4% = $1,600

- Total: $7,600/year

- At 7% return over 25 years: $500,000

- At 3.5% withdrawal rate: $17,500/year passive income

- Plus $25,000 part-time work = $42,500 total at 45

Scenario B: $60K Salary

- Annual savings: 15% = $9,000

- Employer match: 4% = $2,400

- Total: $11,400/year

- At 7% return over 25 years: $750,000

- At 3.5% withdrawal: $26,250/year passive income

- Plus $30,000 part-time work = $56,250 total at 45

Scenario C: $100K Salary

- Annual savings: 15% = $15,000

- Employer match: 4% = $4,000

- Total: $19,000/year

- At 7% return over 25 years: $1,250,000

- At 3.5% withdrawal: $43,750/year passive income

- Plus $40,000 consulting work = $83,750 total at 45

Do you see the pattern? The system scales. It's not that high-income earners have a different math—they just reach their number faster.

But a $40K salary with discipline gets you to phased retirement by 45. That's not "someday eventually." That's within 23 years from today.

Conclusion: Your Unfair Advantage

You're Gen Z. You have something no previous generation had at your age: time, data, and tools.

Your parents and grandparents didn't have low-cost index funds. They didn't have Roth IRAs. They didn't have apps that show compound interest in real-time.

You do.

You also have knowledge—not just financial knowledge, but the lived understanding that traditional careers might not exist in the same form when you're 50. That job security is an illusion. That independence matters more than a title.

The math is simple:

- Start at 22

- Save 15% of your income

- Let it compound for 25 years

- At 45-50, you can choose your work instead of depending on it

You don't need a high income. You don't need luck. You don't need to understand advanced investing strategies.

You just need consistency, time, and patience.

And you already have those.

So here's my challenge: This week, open a Roth IRA. Just do it. Ten minutes. Choose a target-date fund. Contribute $583. Set it to automatic monthly transfers.

That's it.

In 25 years, you'll thank me. Not because you got rich, but because you got free.

P.S. If you want to track your progress toward financial freedom and see your net worth grow in real-time, My Financial Freedom Tracker has tools built exactly for this. You can set your personal freedom number, monitor your portfolio, and see exactly how close you are to the retirement you want.

Questions? Email me at dennis.vymer@myfinancialfreedomtracker.com.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.