401(k) Hardship Withdrawals Hit Record 6%: Why Americans Are Raiding Retirement (And the Real Cost)

New to personal finance?

If you're just getting started, check these first:

- How to Start a Budget — the foundation of money management

- Emergency Fund 2026 — why 59% of Americans can't cover a $1,000 emergency

- Financial Levels Step by Step — where retirement protection fits in your strategy

Sarah is 34, with $48,000 in her Vanguard 401(k). On a Tuesday in March, her toddler runs a 104-degree fever. The ER trip ends in a $5,400 bill. She has $812 in checking, a maxed-out card, and a partner whose hours just got cut.

So she logs into her 401(k) portal. Three checkboxes, no paperwork. Two weeks later, $3,402 hits her account — the rest vanished to income tax, the 10% IRS penalty, and state withholding.

She just paid roughly $44,800 in future retirement wealth for $3,402 in present cash. A 13-to-1 exchange rate, going the wrong way.

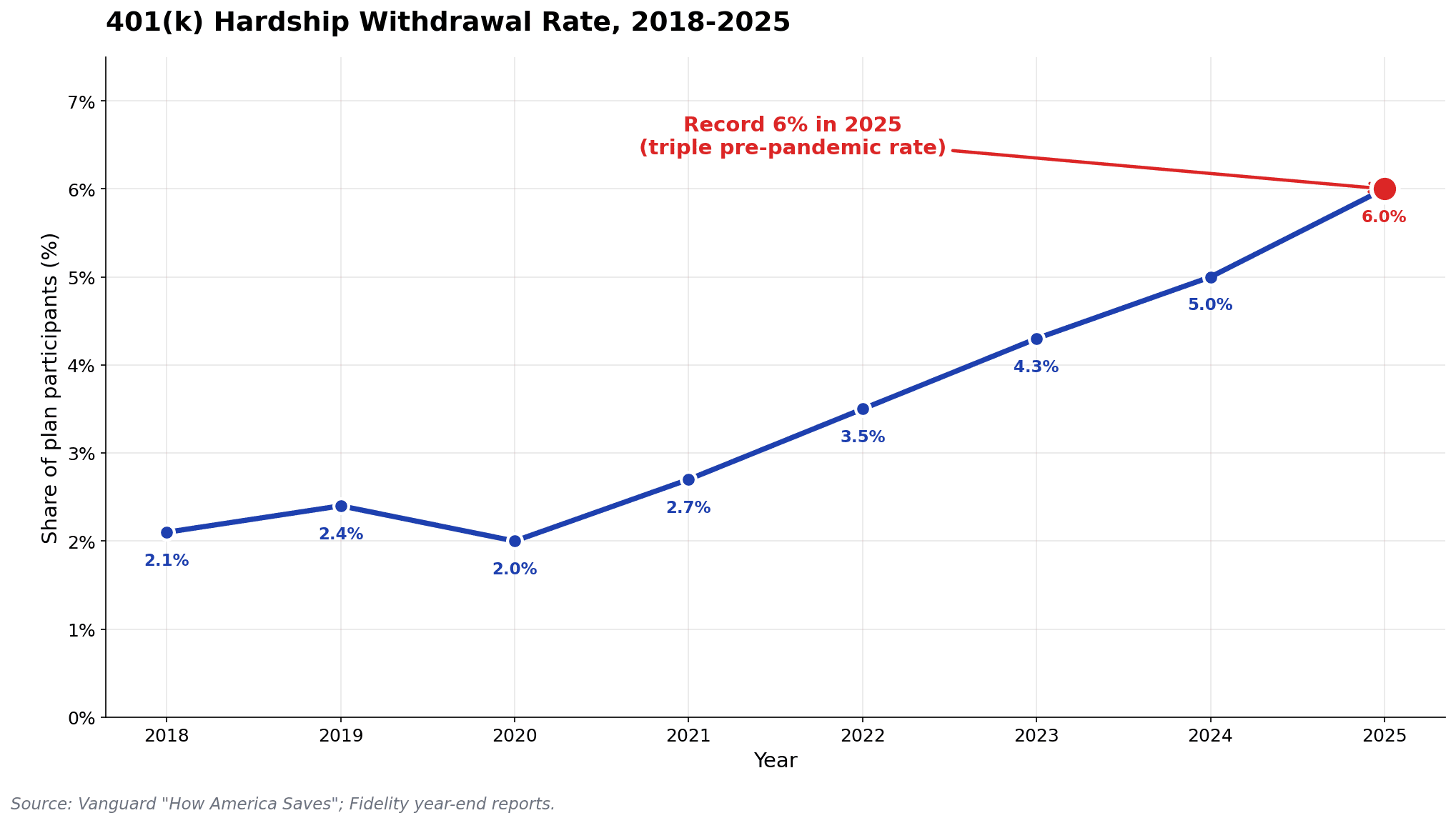

In 2025, 6% of all 401(k) participants did exactly what Sarah did — triple the pre-pandemic rate, per Vanguard's "How America Saves 2026" preview. Sixth straight annual increase. Fidelity's parallel data hit the same 6%.

This isn't reckless spending. It's millions of people running out of options — and the clearest early-warning signal in U.S. household finance right now.

In this guide: what's driving the 401(k) hardship withdrawal crisis, the long-term math nobody shows you, the four SECURE 2.0 carve-outs most workers have never heard of, seven better alternatives, and the tiered "pre-hardship buffer" framework that keeps your retirement money untouchable.

The Quiet Crisis: 401(k) Hardship Withdrawals Just Tripled

In 2018, about 2.1% of 401(k) participants took a hardship withdrawal. By 2025, it was 6.0% — Vanguard's data, confirmed by Fidelity.

What makes it weird: balances also hit record highs in 2025. Vanguard's average climbed to $167,970 (up 13% YoY); the median rose to $44,115 (up 16%). So why are more people raiding accounts that are simultaneously growing? Because the average is a lie — skewed by mega-savers. The median worker under 35 has just $13,900. Not enough to retire on, but enough to be tempting when the rent's due.

David Stinnett of Vanguard told Axios: "It's still a small number, 6%, but it is something that is worth attention." The trajectory matters. Every percentage point is roughly 700,000 American workers permanently shrinking their retirement income.

The two forces driving it

Force #1: Real financial pressure. Cost-of-living is the top stressor for 68% of workers (Fidelity). The U.S. personal savings rate has fallen to 3.6% (FRED) — less than half the long-run average. Only 47% of Americans have sufficient liquidity to cover a $1,000 emergency, per Bankrate's December 2025 survey (2026 Emergency Savings Report).

Force #2: Policy made tapping retirement easier. The 2018 Bipartisan Budget Act killed the rule that you had to take a 401(k) loan first. SECURE 2.0 added self-certification — no more eviction notices. Three checkboxes, two weeks, money in hand.

A frictionless on-ramp to retirement raiding, opened right as balance sheets were squeezed hardest since 2008.

Who's Raiding Their Retirement (And Why)

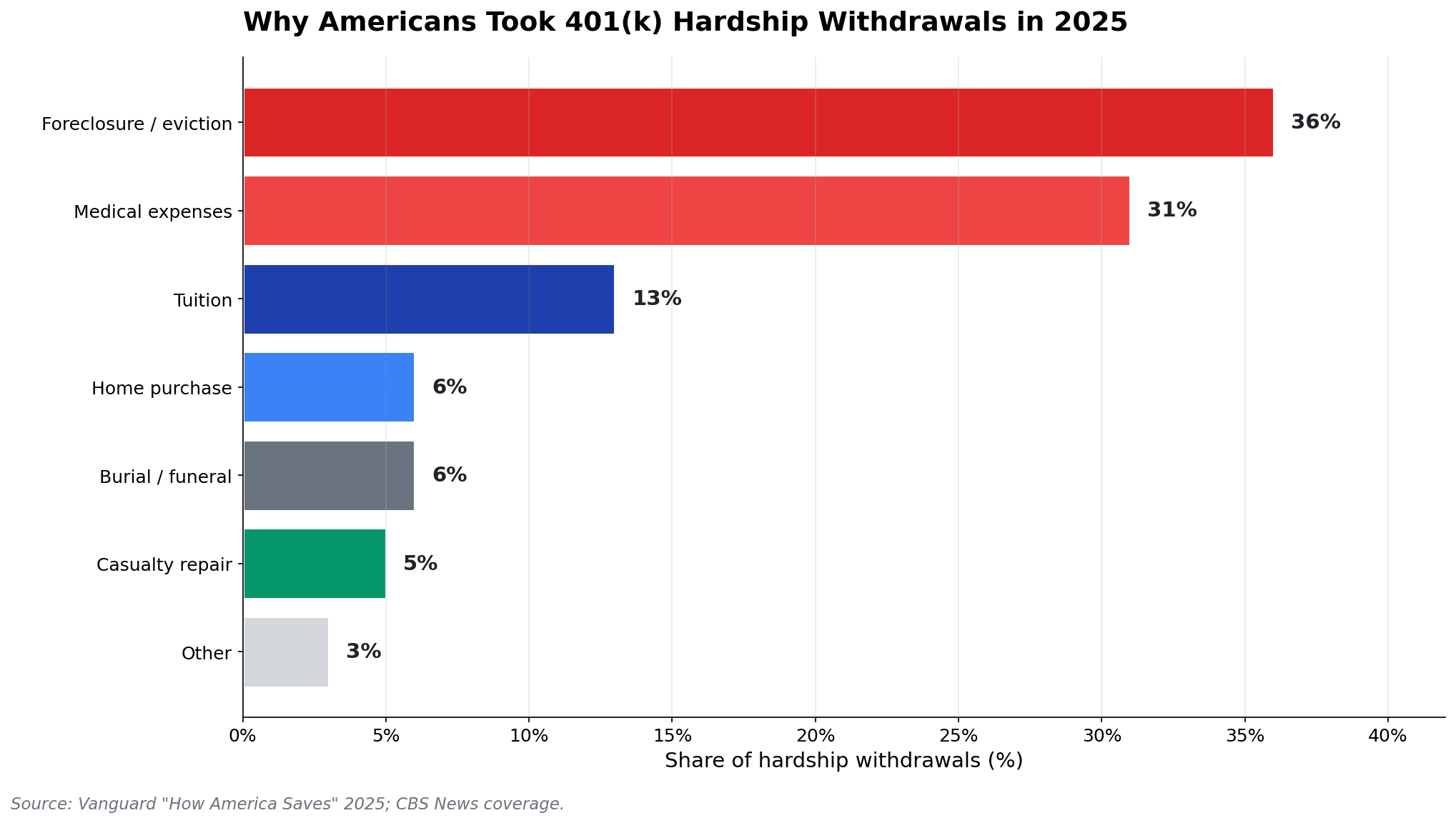

If you picture a hardship withdrawal as "person buys boat with retirement money," the data will surprise you. This is triage, not recklessness.

The 2025 breakdown per Vanguard and CBS News:

- 35–36% to prevent foreclosure or eviction

- ~31% for medical expenses

- 13% for tuition (usually a child's)

- ~6% for burial or funeral

- ~6% for first-time home purchase

- ~5% for casualty repair to a primary residence

- ~4% other

Two-thirds of withdrawals are people trying to keep a roof overhead or pay a hospital. The median was just $1,900; the average $5,400. Not Tesla money — grocery, mortgage-cure, ER-deductible money.

Workers under $100K are over-represented (higher earners have brokerage accounts and HELOCs first). Workers under 35 are most likely to pull the trigger. Black participants are nearly 2x as likely to have ever taken a hardship withdrawal (29% vs. 15%, per EBRI's Retirement Confidence Survey) — reflecting the wider wealth gap, not different choices.

The True Cost of a 401(k) Hardship Withdrawal (The Math Nobody Shows You)

Use Sarah's $5,400 withdrawal at age 35.

Step 1: The tax-and-penalty haircut

Sarah is in the 22% federal bracket; her state takes 5%; she's under 59½, so the IRS adds a 10% penalty.

| Item | Amount |

|---|---|

| Gross withdrawal | $5,400 |

| Federal income tax (22%) | -$1,188 |

| State income tax (5%) | -$270 |

| 10% early-withdrawal penalty | -$540 |

| Net cash in hand | $3,402 |

To actually net $5,400, she'd need to withdraw closer to $8,570.

Step 2: The lost-compounding cost

At a 7% real return, $5,400 invested for 30 years grows to $41,100. Sarah traded ~$44,800 in future retirement wealth for $3,402 in present cash. Real price per dollar of usable cash: $13.17.

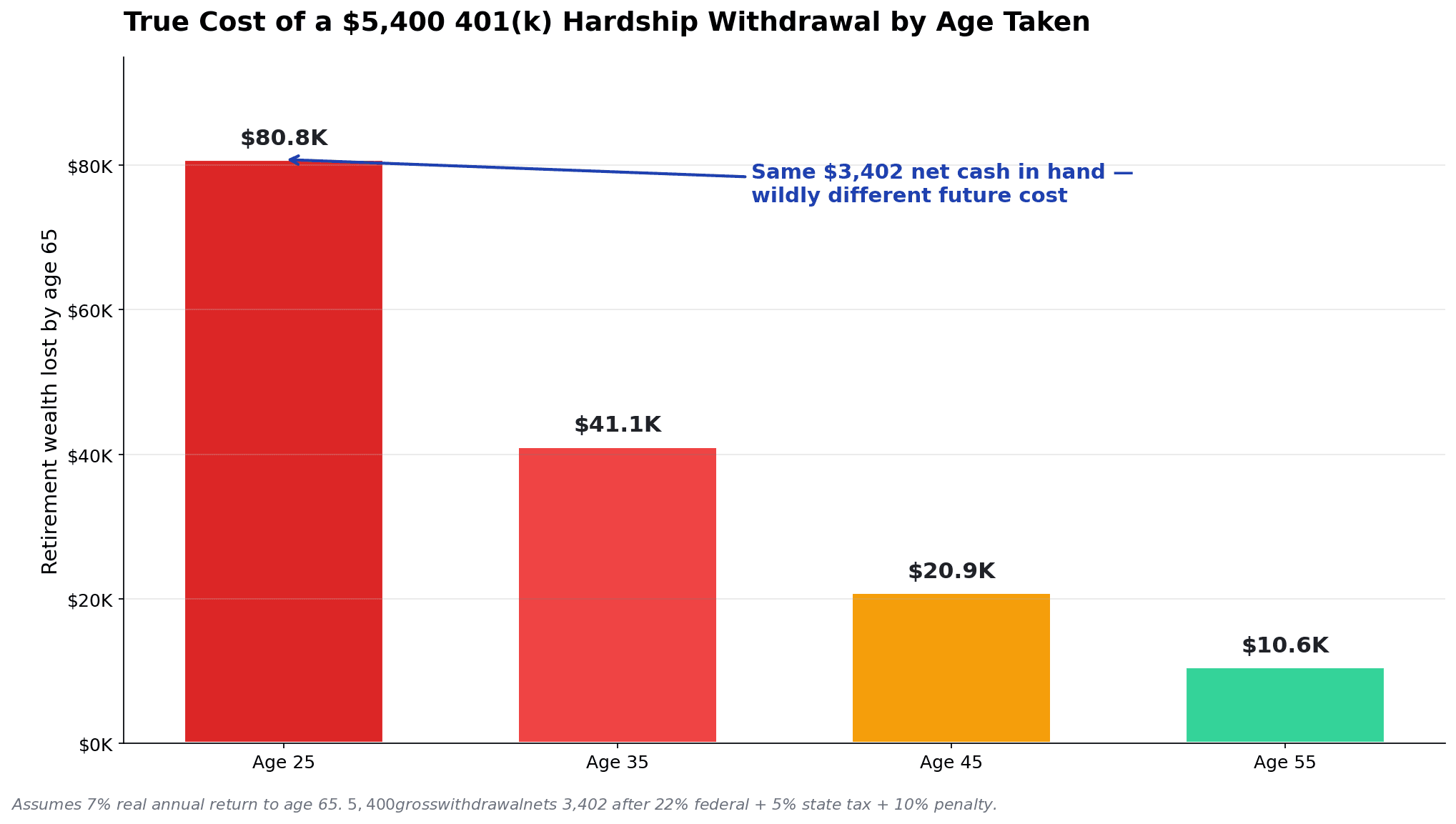

Step 3: The age multiplier

The younger you are, the worse the math gets.

| Age at withdrawal | Net cash received | Lost retirement wealth by 65 |

|---|---|---|

| 25 | $3,402 | $80,800 |

| 35 | $3,402 | $41,100 |

| 45 | $3,402 | $20,900 |

| 55 | $3,402 | $10,600 |

(7% real return to age 65.)

A 25-year-old who pulls $5,400 effectively writes a check for $80,800 against their 65-year-old self.

EBRI's research on retirement-plan "leakage" confirms it at the macro level: early withdrawals reduce the probability of replacing 80% of income in retirement by 7.0–8.8 percentage points.

The real question isn't "can I get the money?" — yes, the form is right there. It's "am I willing to pay $13 of future me for every $1 of present me?"

The 4 SECURE 2.0 Carve-Outs Most People Don't Know Exist

Four legal penalty-free distributions Congress quietly added through SECURE 2.0 (a 2022 law overhauling retirement rules):

- $1,000 emergency personal expense withdrawal. Once per calendar year, self-certified, no penalty. Income tax still applies — unless you repay within 3 years, in which case the tax also disappears.

- $2,600/year long-term care insurance withdrawal. Brand new for 2026. Penalty-free. Most plans haven't adopted it yet.

- Domestic abuse victim withdrawal. Self-certify; pull the lesser of $10,000 or 50% of account, penalty-free, repayable within 3 years.

- Federally-declared disaster withdrawal. Up to $22,000 penalty-free, three years to repay.

Ask your plan administrator which ones your plan has adopted.

7 Better Alternatives Before You Touch the 401(k)

Best to worst — even the worst here beats the withdrawal.

1. Roth IRA contribution withdrawal. Every dollar you've ever contributed to a Roth IRA can be withdrawn at any age, any reason, with zero tax and zero penalty. Only earnings are restricted.

2. HSA reimbursement for past medical expenses. If you've paid medical bills out-of-pocket since opening your HSA — even years ago — you can reimburse yourself tax-free, no time limit. Just need the receipts. For more on this, see my deep dive on the HSA stealth retirement account — the most tax-advantaged vehicle in the U.S. code.

3. 401(k) loan. Often confused with a hardship withdrawal, completely different. Borrow up to 50% of vested balance or $50,000. Pay yourself back at ~8-9% APR. No tax, no penalty. Main risk: if you leave your job, the loan is due by the next tax-filing deadline. A worker who needs $25K to cure mortgage arrears would pay ~$1,800 in interest via a loan — vs. ~$116,200 in lost compounding via the withdrawal.

4. HELOC. May 2026 national average rate: 7.26%. Setup takes 2-6 weeks, so open it before the crisis and don't use it.

5. 0% APR balance transfer card. Cards like Citi Diamond Preferred offer 0% APR for 21 months (3-5% transfer fee). The trap: when the promo ends, the rate snaps to ~22% — I dig into this in credit card interest rates hitting 20%+. Important: do NOT transfer hospital medical debt to a card — you lose CFPB medical-debt protections.

6. Employer Assistance Fund (EAF) grant. Ask HR. These are grants, not loans — typically $500-$5,000, no repayment. Massively underutilized.

7. Negotiated payment plan. Most hospitals will accept $50-$100/month at 0% interest indefinitely; many wipe 30-100% of the bill via charity care if you're under 400% of the federal poverty line.

The seven alternatives side by side

| Alternative | Cost | Speed | Tax/penalty |

|---|---|---|---|

| Roth IRA contributions | $0 | 1-3 days | None |

| HSA past-medical reimbursement | $0 | Instant | None |

| 401(k) loan | ~8-9% APR | 1-2 weeks | None unless default |

| HELOC | ~7.3% APR | 2-6 weeks | None |

| 0% APR balance transfer | 3-5% fee, 0% APR 21 mo | 1-2 weeks | None |

| Employer EAF grant | $0 | Days-weeks | Sometimes taxable |

| Negotiated payment plan | 0% to low APR | Same day | None |

| Hardship withdrawal | 32-42% effective | 1-2 weeks | Income tax + 10% penalty |

Almost nobody exhausts this list — the 401(k) portal is just the easiest button to click.

The "Pre-Hardship Buffer" Framework

Everything above is reactive. This is preventive — the four-tier safety system you build before the emergency, in this order, so the 401(k) is the last thing you'd ever touch.

Tier 1: $1,000 cash, accessible same-week. Just $1,000 sitting in checking. Handles 80% of "true emergencies" — car battery, ER copay, vet bill. The reason 6% are raiding their 401(k) is, overwhelmingly, that Tier 1 doesn't exist. Forty-five percent of Vanguard participants have less than $2,000 in emergency savings. If you're stuck at zero, the 2026 emergency fund crisis walks you through how to build it from a $20-per-paycheck start.

Tier 2: One month of essentials in a HYSA. Rent, utilities, groceries, insurance, minimum debt payments. Typically $3,000-$5,000 at 4.0-4.5% APY. Your job-loss runway for the first 30 days.

Tier 3: Three months of full expenses. All of life, including discretionary. $15,000-$30,000 for most middle-income households. HYSA plus a short CD ladder.

Tier 4: Untapped credit capacity. Before the 401(k) gets touched, you should also have unused borrowing capacity standing by: an open, unused HELOC; confirmed 401(k) loan eligibility; a 0% APR card with zero balance kept open. You don't want to use these — but knowing they exist means the 401(k) is firewall #5, not #1.

Vanguard's own research on hardship withdrawals found that participants with at least $2,000 in dedicated emergency savings are 70% less likely to take a hardship withdrawal. The buffer literally protects the retirement account from the participant's worst moments. The framework's whole point is sequencing — each tier protects the next.

If You Already Took a 401(k) Hardship Withdrawal: The Recovery Playbook

Step 1: Check your repayment window. SECURE 2.0 lets you repay the $1,000 emergency, disaster, and domestic abuse withdrawals within three years to reverse the tax hit. A standard hardship withdrawal for medical or foreclosure is unfortunately permanent.

Step 2: Recalculate your FIRE timeline honestly. Log the withdrawal. Re-run the projection. If you were on track for FIRE at 52 and pulled $25K at 42, your new number is more like 53.5.

Step 3: Automate the replacement contribution. A $5,400 withdrawal at 7% is roughly $150/month for 36 months on top of your normal contribution.

Step 4: Use the catch-up window if you're 50+. Workers 50+ can add $7,500/year extra to a 401(k) in 2026 (high-earners $145K+ must do it on a Roth basis). The math is forgiving in your 50s in a way it isn't in your 30s.

Step 5: If the withdrawal covered debt, build a real payoff plan. My hybrid debt payoff method combines the snowball's psychological wins with the avalanche's math.

Step 6: Plan your post-recovery FIRE strategy. If FIRE was the goal, the Roth conversion ladder becomes critical — the long-term strategy for accessing retirement money before 59½ without penalties.

When a hardship withdrawal IS the right call

Five situations where I'd actually tell someone to take one:

- You're 55+ and the time horizon is short.

- The alternative is Chapter 7 bankruptcy.

- End-of-life medical care where the alternative is no treatment.

- You qualify for a 72(t) exception that waives the 10% penalty (medical >7.5% AGI, total disability, federally-declared disaster, qualified birth/adoption).

- Imminent foreclosure AND every alternative above has been exhausted.

If none of those fits, you're probably making a mistake.

How MFFT Spots the Hardship Risk Before It Happens

The 6% who took a hardship withdrawal in 2025 didn't wake up surprised. The squeeze built for months: shrinking cushion, growing minimum payments, declining savings rate. All of it visible in cash-flow data — if anyone was looking.

MFFT's combined budgeting + net worth + FIRE projection view surfaces three early-warning signals:

- Discretionary cushion shrinking 3+ months in a row → buffer is being eaten.

- Credit card minimum payments rising while balances grow → debt momentum is building.

- Emergency fund vs. monthly essentials ratio below 1 → less than 30 days of runway.

The point isn't the app — it's visibility. Most people figure out the squeeze the same week the withdrawal request gets approved.

The Bottom Line

The 6% is not the disease. It's the diagnostic.

The personal finance question isn't "how do I never need a 401(k) hardship withdrawal." Life will throw a $5,400 ER bill or a $25,000 foreclosure threat at most of us eventually. The right question is: "Have I built a buffer system so the 401(k) is the LAST place I turn, not the first?"

That's the move. It's not exciting and it won't go viral on TikTok, but it's the difference between a FIRE plan that compounds quietly to freedom and one that gets gutted by a single emergency.

Your action plan this week

- Check whether your plan adopted the SECURE 2.0 $1,000 emergency withdrawal.

- Confirm your 401(k) loan eligibility. Knowing it's there changes the math.

- Open the HYSA. Tier 2 doesn't build itself.

- Audit your unreimbursed HSA receipts. You may already have a Tier 1 cushion you forgot existed.

- Re-rank your safety net using the four-tier framework.

A hardship withdrawal isn't a strategy — it's the absence of one. Build the system instead. Track it in MFFT's budgeting and net worth dashboard. The 6% didn't fail at willpower — they failed at visibility. Don't make the same mistake.

Questions about building your pre-hardship buffer or recovering from a withdrawal? Email me at dennis.vymer@myfinancialfreedomtracker.com. I read every one.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.