The Buy Now, Pay Later Trap: What BNPL Really Costs Gen Z

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Build Wealth From Zero — the equation that explains wealth multiplication

- Credit Card Interest Rates: The Hidden Math Trap — why credit card debt delays financial freedom

- How to Start a Budget — the foundation of money management

You pull out your phone. You see something you want. Shoes for $80. A jacket for $120. A new gaming laptop for $800.

A year ago, you might've said no.

Today, you say: "Let me just split this into payments."

Four taps. No credit check. No interest shown upfront. The money is yours now. You'll worry about the payments later.

Welcome to Buy Now, Pay Later (BNPL) — the fastest-growing payment trap of the 2020s.

For the first time, Gen Z is using BNPL more than credit cards. In a J.D. Power survey, 54% of Gen Z said they used BNPL during the 2024 holiday season, compared to 50% using credit cards. This isn't a fringe payment method anymore. This is the default.

Let me be honest with you upfront, because most articles about BNPL aren't: a single pay-in-4 plan, paid on time, genuinely costs you nothing extra. The marketing isn't lying about that.

The trap is everything around that sentence. BNPL is engineered to make you buy more than you would otherwise, to let you stack five plans before you notice, and — since 2025 — missed payments increasingly follow you onto your credit record. The costs are real; they're just not where the "hidden interest" headlines tell you to look.

This article shows you exactly where the real costs are — late fees, loan stacking, overspending, and the new credit reporting rules — and what to do if you're already caught in the trap.

The BNPL Explosion: How It Became Gen Z's Payment Method of Choice

Let me give you the context first.

For most of American history, young people built financial discipline through limitations. You didn't have a credit card. You didn't get a loan. If you couldn't pay cash, you waited.

That friction — that forced waiting — was actually good for financial health. It created discipline.

Then BNPL arrived and removed every single barrier.

Why BNPL Feels So Good

Think about the psychology of a traditional credit card:

You spend $500. Your statement arrives. You see $500 owed. There's friction. There's awareness.

Now think about BNPL:

You want $500 item. You don't see $500 owed. You see: "4 payments of $125."

Psychologically, "$125" feels completely different from "$500." Your brain doesn't process it as debt. It processes it as "affordable."

This is called the decoupling effect — when the payment is divorced from the moment of purchase, your brain treats them as separate events. You get the dopamine hit of buying the item immediately, but you don't feel the pain of paying for it. You feel the pain (the payment) weeks later, in small doses, when your emotional connection to the purchase has faded.

This is the same psychological trick that makes credit cards more addictive than cash or debit. But BNPL takes it further.

By then, you've usually made another BNPL purchase. And another.

This connects directly to what we've discussed about financial discipline and wealth building — friction creates discipline. Remove the friction, and discipline evaporates.

The Numbers That Show How Fast This Happened

- 54% of Gen Z used BNPL over the 2024 holidays — more than used credit cards (50%), the first time J.D. Power's survey showed BNPL overtaking cards for that group

- The CFPB found that more than one in five US consumers with a credit record used BNPL in 2022 — and usage has only grown since

- LendingTree's BNPL tracker shows late payments rising fast: 47% of users paid late in the past year, up from 41% a year earlier and 34% the year before

Global market? Projected to surpass $560 billion in payments in 2025, still growing at double digits.

This isn't a niche product. This is mainstream financial behavior for an entire generation.

The Real Math: Where BNPL Actually Costs You (And Where It Doesn't)

First, let's kill a bad argument you'll see all over the internet — because if I'm asking you to trust the rest of this article, I owe you the honest version.

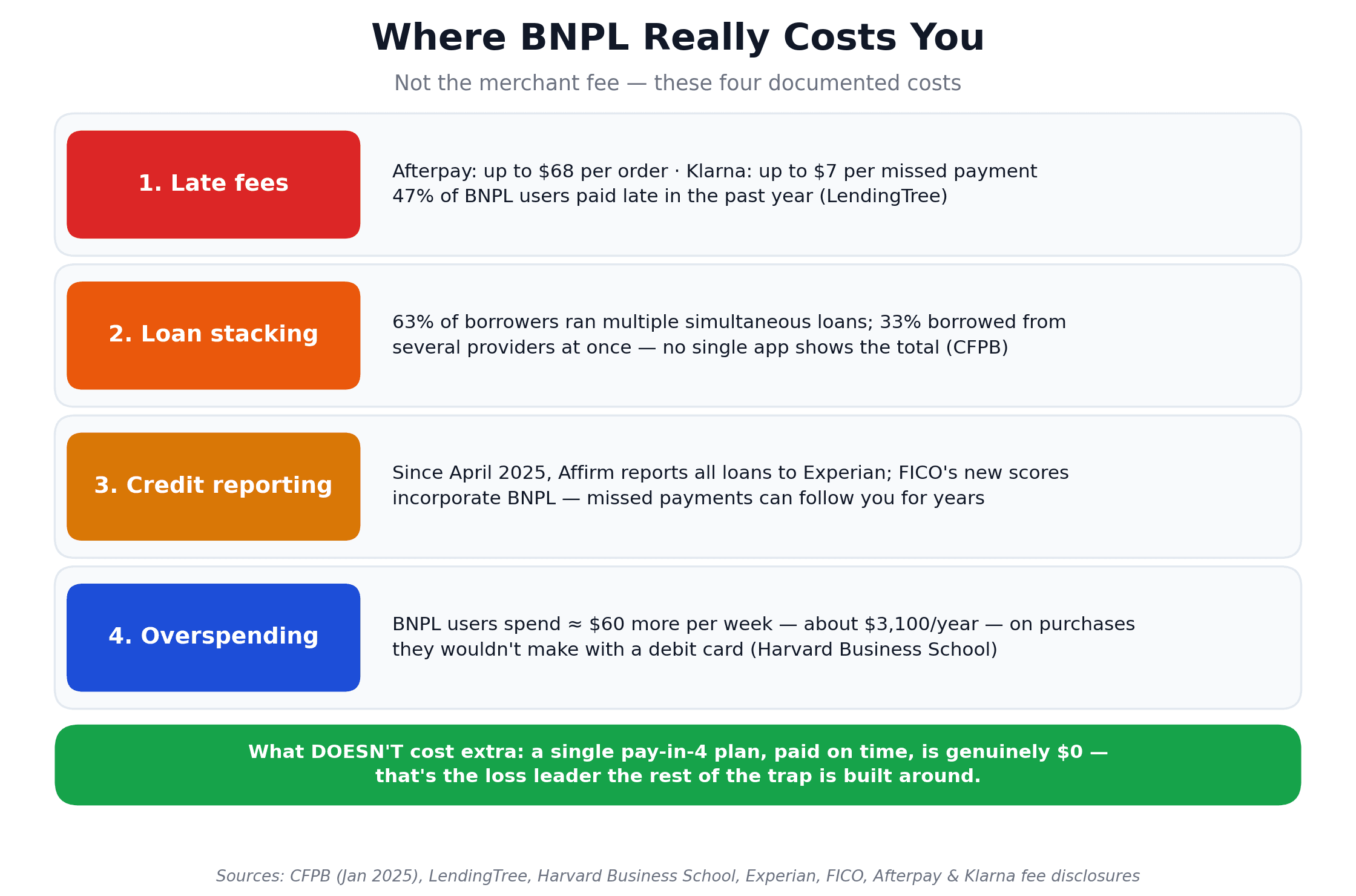

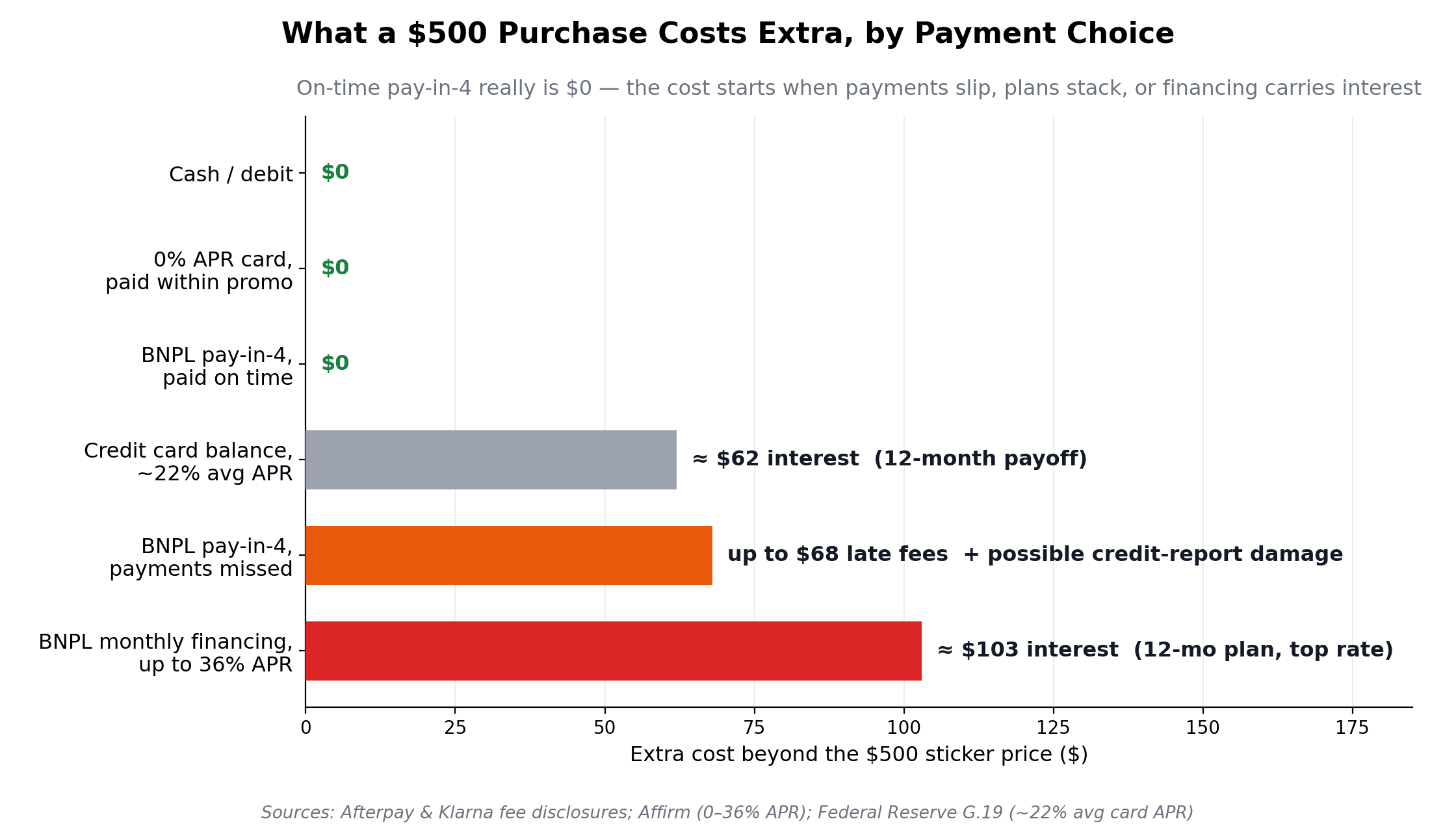

The "hidden merchant fee" argument is wrong. Yes, merchants pay BNPL providers real money — typically 2% to 8% of the purchase, more than the 1-3% they pay on credit card transactions. And yes, merchants build their payment costs into retail prices. But here's the thing: they build them into the price everyone pays — cash buyers, card buyers, BNPL buyers alike. Credit-card interchange works exactly the same way and nobody calls your Visa purchase "6% more expensive." Choosing BNPL at checkout does not make your purchase cost more than paying by card. A pay-in-4 plan paid on time costs you $0 extra.

So where does BNPL actually cost you? Four places — and they're better documented than the myth.

The Four Real Costs of BNPL

1. Late Fees

Miss a BNPL payment and here's what the platforms themselves disclose:

- Afterpay: late fees that never exceed 25% of the order total or $68 per order, whichever is lower ($10 when a payment is missed, another $7 if still unpaid after 7 days, on orders of $40+)

- Klarna: a late fee of up to $7 per missed payment, never exceeding 25% of the purchase

- Affirm: no late fees — but its longer monthly financing plans charge interest of up to 36% APR, higher than the average credit card

A $7 or $17 fee sounds small. But late fees are charged per order — and 47% of BNPL users paid late in the past year, per LendingTree. With four or five plans running, fees stack the same way the loans do.

2. Credit Reporting (the 2025 Game-Changer)

For years, BNPL lived in a credit-reporting gray zone. That ended in 2025:

- As of April 1, 2025, Affirm reports all of its pay-over-time loans — including Pay in 4 — to Experian; Klarna shares data with credit bureaus for some of its products too

- In fall 2025, FICO launched Score 10 BNPL and Score 10 T BNPL — the first scores from a major provider to incorporate BNPL data

The transition is gradual (pay-in-4 data isn't yet factored into the older scores most lenders still use), but the direction is unmistakable: your BNPL behavior is becoming part of your credit file. On-time payments may eventually help thin-file borrowers — but missed payments and a stack of overlapping loans are now visible where future lenders can see them.

3. Loan Stacking

This is the documented heart of the trap. The CFPB's January 2025 study of BNPL borrowers found that 63% originated multiple simultaneous loans at some point during the year, and 33% borrowed from multiple BNPL providers at once.

Each purchase feels small. But payments from different plans land in overlapping cycles, and no single app shows you the total. Within 3-4 months, it's easy to have 5-8 active plans:

- Month 1: $300 in payments due

- Month 2: $450

- Month 3: $420

- Month 4: $500

One month, you can't cover them all. One payment gets missed. Now you're managing late fees, credit damage, and the psychological stress of being in default.

4. Overspending (the Best-Documented Cost of All)

This one isn't speculation — it's measured:

- A Harvard Business School study by Di Maggio, Katz, and Williams found BNPL adoption causes "a permanent increase in total spending of around $60 per week" — roughly $3,100 a year — concentrated in retail purchases

- A Central Bank of Ireland experiment found participants spend on average 4.4% more with BNPL than with a debit card, are 22.2% more likely to buy a discretionary product, and even the expectation of future BNPL access lifts current spending by 3.1%

You're not just financing the purchases you planned to make. BNPL's frictionlessness makes you buy things you otherwise wouldn't — and that, not a hidden fee, is where most of the money leaks. One transparent approach to budgeting — the opposite of BNPL's invisibility — shows how clarity drives better choices.

BNPL vs Credit Cards: The Honest Cost Comparison

Let me show you a direct comparison — with the honest numbers, including the scenario where BNPL is genuinely free.

You want to buy a $500 item. Here's what each option can cost you over 12 months:

| Option | Sticker Price | What You Pay Extra | When It Goes Wrong |

|---|---|---|---|

| Cash / debit | $500 | $0 | — |

| 0% APR card, paid within promo | $500 | $0 | Deferred or 20%+ interest if a balance survives the promo period |

| BNPL pay-in-4, paid on time | $500 | $0 | — |

| BNPL pay-in-4, payments missed | $500 | Late fees up to $68 (Afterpay) or $7/miss (Klarna) | Possible credit-report damage under the 2025 reporting rules |

| BNPL monthly financing (e.g., Affirm) | $500 | Interest at 0-36% APR | At the top end, costlier than almost any credit card |

| Credit card, balance carried | $500 | Interest at ~22% average APR | Compounds monthly until paid |

Read that table honestly and the real pattern appears: the single, on-time pay-in-4 plan is the loss leader. It's genuinely free, and it's how the platforms earn your trust. The money is made on what happens next — the user with five overlapping plans, the missed payment that triggers fees and credit reporting, and the upsell into interest-bearing monthly financing at rates up to 36% APR.

Most heavy BNPL users don't stay in row three. The CFPB found 63% of borrowers run multiple simultaneous loans, and late payment rates are rising every year. With multiple overlapping payment obligations, the likelihood of missing at least one payment goes way up — and that's the moment "free" stops.

The Psychological Trap: How BNPL Is Designed to Addict

This is the part where I need to be direct: BNPL isn't an accident. It's not a payment method that happened to be appealing. It's engineered to exploit psychological weaknesses.

The platforms know exactly what they're doing. The research proves it.

The Psychological Mechanisms

1. Payment Decoupling

We covered this above: the purchase and the payment are separated in time, so your brain gets the dopamine now and the pain in small doses later. With a credit card, you at least see the full amount owed on one statement. With BNPL, you see "4 payments of $125" — across four different apps if you're stacking.

2. Installment Framing

Your brain is terrible at math in the moment. If I ask you: "Do you want to spend $500?" you say no.

If I ask you: "Do you want to spend $125?" you say yes.

The fact that you have to say yes four times doesn't register as a problem. Your brain is wired to make decisions in the moment, not to add up consequences over time.

3. One-Click Checkout

There's minimal friction. No credit check. No approval process. No waiting.

With a credit card, there are barriers: spending limit, credit score, approval time.

With BNPL, the barrier is removed. One click. Money is yours.

Less friction = more purchases. This is proven behavioral economics.

4. Reaching the Financially Vulnerable

Here's the darkest part: the CFPB found that 61% of BNPL originations went to borrowers with subprime or deep-subprime credit scores (45% deep subprime, 16% subprime) — and BNPL lenders approved 78% of applications from those borrowers in 2022.

These are largely people who can't get (or can't get more) traditional credit. They're the most likely to be damaged by BNPL debt spirals — and they're the easiest customers for BNPL to acquire, because the approval bar is so low.

The Research Evidence

A Central Bank of Ireland behavioral study found:

- Participants spend on average 4.4% more when paying with BNPL than with a debit card

- They are 22.2% more likely to buy a discretionary product when BNPL inflates their perception of available funds

- The mere expectation of future BNPL access increases current spending by 3.1% — even before using it

This isn't opinion. This is measured behavioral change.

The platforms have optimized for one thing: maximum spending, minimum awareness of cost.

The Debt Spiral: How BNPL Leads to 6-Figure Debt

Let me walk you through how this actually plays out in real life.

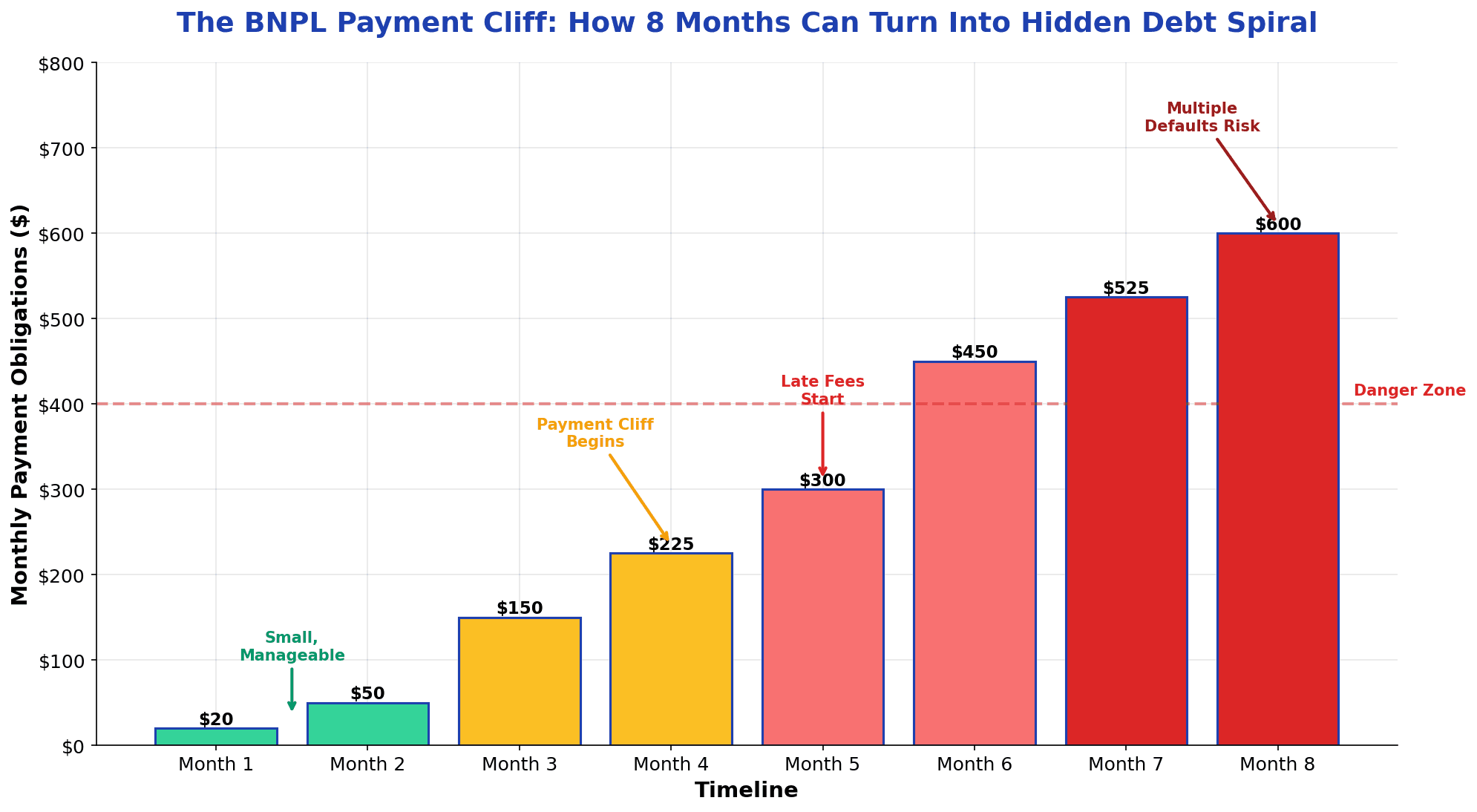

Maya's Story: From Small Purchase to Payment Cliff

Month 1: Maya, 23, sees shoes on sale ($80). She's never used BNPL before. "4 interest-free payments of $20? That's easy."

She buys them.

Month 2: The first payment hits. It doesn't hurt. She sees another item — a coffee maker for $150. "Same thing. 4 payments of $37.50."

She buys it.

Month 3: Now she has two active BNPL plans. She sees a jacket she loves ($120). Same logic. She adds it.

Total active BNPL: $350. Monthly payment obligations: $150.

Month 4: More items. Beauty products ($200). Another pair of shoes ($90).

Total BNPL debt: $640. Payment obligations: $225/month.

Month 5: Her paycheck comes. She sees $225 in BNPL payments due. She wasn't budgeting for this. She covers it, but it's tight.

She makes one payment late by 3 days. Late fee: $10. It gets reported to Experian.

Month 6: She's stressed. In a moment of emotional spending, she buys a laptop ($800) on Affirm.

Total active BNPL: $1,440. Monthly payment obligations: $450.

She also has a credit card she was paying off. Now she can't. She starts carrying a balance.

By Month 8: She has 6-7 active BNPL plans. Payment obligations hit $600 in one month. Her paycheck is $3,200. Before taxes, deductions, rent, food — 18% of her gross income is tied up in BNPL payments.

She can't cover all of them. Two payments get missed.

Now:

- Two late fees across two platforms

- Two delinquencies that can be furnished to the credit bureaus under the 2025 reporting rules

- Psychological stress: overwhelming

Her total outstanding BNPL debt: $1,800 — spread across enough apps that she never saw the number until it broke her month. And remember the Harvard finding: a meaningful slice of that $1,800 is spending she would never have done with a debit card.

The Pattern Repeats Across Gen Z

The research shows:

- 63% of BNPL borrowers ran multiple simultaneous loans at some point in a year, and 33% borrowed across multiple providers (CFPB)

- 47% of BNPL users paid late in the past year — up from 41% the year before, and 34% the year before that (LendingTree)

- The CFPB also found BNPL borrowers were far more likely to carry high balances on their other credit lines — BNPL debt stacks on top of existing card debt, it doesn't replace it

This isn't randomness. It's a system designed to extract maximum payment with minimum awareness.

BNPL's Impact on Credit Score & Financial Health

Here's what happened in 2025 that changed everything: credit reporting finally caught up with reality.

For years, BNPL operated in a gray zone. Missed BNPL payments didn't always hit credit bureaus. It felt "hidden" from your credit score.

That ended in April 2025.

How BNPL Now Touches Your Credit

Affirm reporting to Experian (April 2025):

- All of Affirm's pay-over-time loans, including Pay in 4, are now furnished to Experian

- The data appears on your Experian credit report; for now it isn't factored into the traditional scores most lenders pull, but lenders and the new BNPL-aware scores can see it

- One genuinely consumer-friendly detail: BNPL applications typically use a soft credit check, so applying doesn't ding your score the way a card application can

FICO's new scoring models (fall 2025):

- FICO launched Score 10 BNPL and Score 10 T BNPL, the first scores from a major provider to incorporate BNPL data

- As lenders adopt them, your BNPL repayment history — good and bad — directly affects your score

What a Missed Payment Actually Does

I won't give you a fake precision table here, because FICO doesn't publish one. What the bureaus do confirm:

- Payment history is the single largest factor in your FICO score (about 35% of it), so reported delinquencies hit the part of the score that matters most

- A reported late payment can stay on your credit report for up to seven years, per Experian

- The damage scales with how strong your credit was — and for Gen Z borrowers with thin files, a default can define the file

A lower score doesn't just sting emotionally. It feeds directly into the rates you're offered on car loans, apartments, and eventually a mortgage — where even a fraction of a percentage point compounds into thousands of dollars over the loan's life.

For Gen Z Specifically

This is brutal for young people because they're building credit history right now.

An 18-year-old with three BNPL accounts and one missed payment now has a credit history that starts with a default. When they apply for their first car loan or apartment at 22, lenders see: young, high credit inquiry density, payment default.

That one missed BNPL payment could cost them thousands of dollars in higher rates for the next 5-7 years.

The 4-Step Framework to Break Free (Or Use BNPL Safely)

If you're already caught in BNPL, this framework can help. If you're thinking about using BNPL, follow this to stay safe.

Step 1: Audit All Active BNPL Plans

Do this today. Don't wait.

List every BNPL service you're using (Affirm, Klarna, Afterpay, PayPal Pay in 4, etc.).

For each one, write down:

- Total balance currently owed

- Monthly payment amount

- Due date of next payment

- Any late fees already paid, and the APR if it's a monthly financing plan

Add them all up. See the number.

Most people don't realize they have $1,500+ active until they audit. The shock is necessary.

Red flag threshold: If your total active BNPL debt exceeds 5% of your monthly income, you have too much. If it exceeds 10%, you're in serious trouble.

Step 2: Calculate the True Cost of Each Plan

For every active plan, calculate: Original price + late fees paid + interest (on monthly financing plans) + the honest answer to "would I have bought this at all with a debit card?"

That last item is the big one. The research says BNPL users spend about $60 more per week than they otherwise would. Go through your audit list and mark every purchase you wouldn't have made paying cash. That's the real cost of BNPL in your life — not a fee, but purchases that wouldn't otherwise exist.

Step 3: Set Up Payment Reminders and Auto-Pay

This is crucial.

Missed BNPL payments are now reported to credit bureaus. One missed payment can cost you thousands in future borrowing costs.

Options:

- Set a phone reminder 3 days before each due date

- Set up auto-pay directly from your checking account (if the platform allows)

- Use MFFT's tracking dashboard to monitor all BNPL obligations in one place

If you use MFFT, set alerts when your total BNPL debt exceeds 5% of monthly income.

Step 4: Implement the "Pause and Wait" Rule

Before making any new BNPL purchase:

- Wait 48 hours. Don't buy it today. Wait two days.

- Ask yourself: Would I buy this with cash? Is this a need or a want?

- If the answer is "want," and I'm only buying it because BNPL makes it feel affordable," don't buy it.

This 48-hour rule breaks the psychological decoupling. It reconnects the purchase with the payment.

After 30 days of following this rule, most people cut their BNPL spending in half.

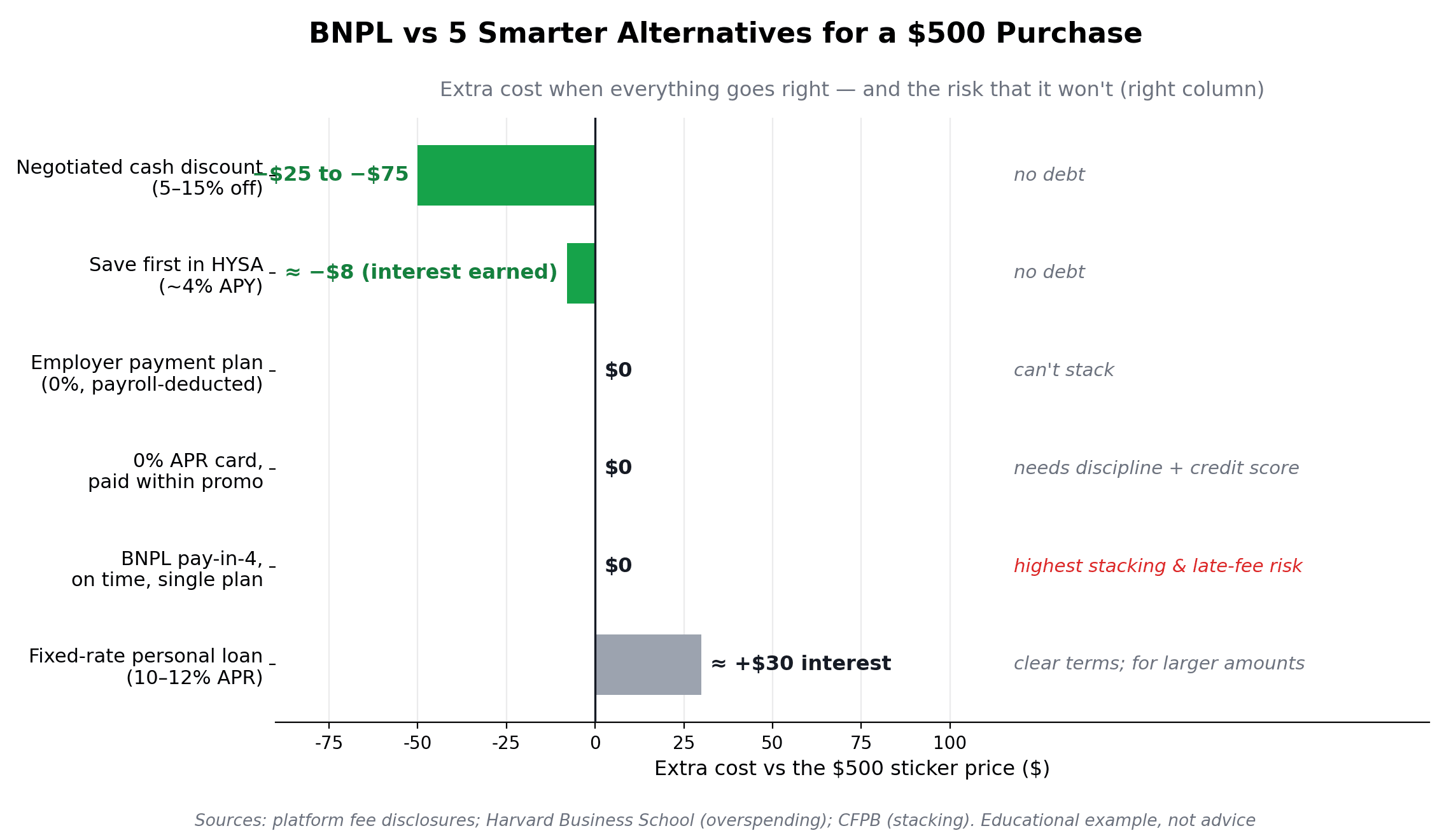

Smarter Alternatives to BNPL

If you need to finance a purchase, here are five alternatives — and an honest assessment of when each one actually beats BNPL:

1. Zero APR Credit Card (12-21 months)

Cards like Citi Diamond Preferred or Wells Fargo Reflect offer 0% APR for 12-21 months on purchases.

Honestly? On pure price, an on-time pay-in-4 plan and a 0% card both cost $0 extra. The card wins on structure: one statement instead of four apps, a longer runway for bigger purchases, on-time payments that build your traditional credit score today (not just the new BNPL scores), and consumer protections like chargeback rights that BNPL plans often lack.

The catch: you need the credit score to qualify — and the discipline to clear the balance before the promo ends, or the ~22% average card APR kicks in.

2. High-Yield Savings Account (Save First, Buy Later)

This is the boring but right answer.

Open a high-yield savings account earning ~4% APY. Automatically transfer $100/month into a "laptop fund" or "vacation fund."

Cost comparison: $500 purchase in 6 months

- BNPL: $500 if everything goes perfectly — plus late-fee and stacking risk, plus the documented overspending pull

- Savings account: $500 minus the interest you earned on the way — and zero new debt obligations

Winner: Saving first. Not because BNPL charges hidden interest — it's because the delay forces you to ask: "Do I really want this?" By the time you can afford it, you might not. That question is worth more than any fee math.

3. Personal Loan (Fixed Rate, Clear Terms)

For larger purchases, compare a personal loan at 10-12% APR against BNPL monthly financing — which runs as high as 36% APR at Affirm. A pay-in-4 plan is cheaper than both, but pay-in-4 typically caps out around $1,000-2,000; for a $5,000 purchase you're being offered the interest-bearing product, and that's where a fixed-rate personal loan often wins on price and always wins on clarity: one payment, one rate, one end date, no stacking.

Winner: Personal loan if you must borrow a large amount; savings account if you can wait.

4. Employer Payment Plans

Some employers offer payment plans for large purchases (electronics, furniture, medical procedures).

These are often 0% interest, payroll-deducted, and impossible to stack. If your employer offers this, use it.

5. Negotiate a Discount for Cash Payment

Go to the retailer. Say: "What discount do you offer for paying in full today?"

Smaller retailers especially will sometimes give you 5-15% off, because BNPL and card transactions cost them real fees that cash doesn't. This is the one place merchant fees do become your opportunity: a discount for paying outright makes the item genuinely cheaper than any financing option.

If you want to start with foundational budgeting principles, learn the basics here.

Is BNPL Ever Okay? When (And When Not) to Use It

I'm not going to tell you to never use BNPL. That's not realistic for a generation that's grown up with it.

But I will tell you when it's acceptable and when it's a trap.

When BNPL Makes Sense

1. Planned emergency with full repayment ability

Your car breaks down. You need a $800 repair. You have $800 in savings, but you want to preserve cash flow for the next two weeks until your paycheck.

In this case: BNPL for the repair is fine. You're using it as a cash flow tool, not debt. You'll pay it off immediately.

2. You have 100% cash available to cover all active BNPL plans

If you have $5,000 in BNPL purchases active AND $5,000 in savings specifically for those payments, you're using BNPL correctly.

Most people don't. Most people use BNPL because they don't have the cash.

3. A single plan with autopay, for a purchase you'd make anyway

One pay-in-4 plan, on a planned purchase, with autopay on and the cash already in your account, is genuinely free financing. The rules that keep it that way: one plan at a time, never stacked, never for impulse buys.

When to Absolutely Avoid BNPL

1. Impulse purchases

"I want this right now" + BNPL = debt trap. Full stop.

2. Multiple simultaneous BNPL plans

If you already have 2+ active BNPL plans, don't add more. The payment cliff is coming.

3. You have credit card debt above 15% APR

Paying off 22% credit card debt should be priority #1. Using BNPL for new purchases while carrying credit card debt is wealth destruction.

4. You've missed a BNPL payment before

If you've already demonstrated you can't reliably make BNPL payments, stop using it.

5. You don't know what you owe across all platforms

If you can't track your total BNPL debt, you've lost control. Stop using it immediately.

How to Track BNPL and Prevent Debt Chaos

The single biggest problem with BNPL is visibility. You can have $1,500 in active plans and not realize it because the payments are scattered across platforms and payment dates.

Here's how to solve it:

Option 1: MFFT Budgeting Dashboard

MFFT's transaction tracking automatically categorizes all BNPL purchases. You can:

- See all active BNPL plans in one dashboard

- Set alerts when total BNPL exceeds your threshold

- Track payment due dates to prevent missed payments

- Monitor credit impact as it changes

This is the easiest solution because it's automated.

Option 2: Simple Spreadsheet

Create a Google Sheet with columns:

- Platform (Affirm, Klarna, Afterpay, etc.)

- Purchase amount

- Payment due date

- Remaining balance

- Notes

Update it every Sunday for 5 minutes.

Option 3: Dedicated Checking Account

Open a second checking account for BNPL payments only. When you make a BNPL purchase, transfer that month's payment amount to this account immediately.

This forces you to "pay now, use later" and prevents the payment cliff surprise.

Whichever method you choose, the goal is the same: visibility and control.

The FIRE Impact: How BNPL Is Delaying Financial Independence

Let me connect this to something larger: your long-term freedom.

If you're interested in reaching financial independence (FIRE), BNPL is your biggest obstacle — not housing costs, not student loans, but BNPL.

Here's why:

The Math of Wasted Wealth

Let's build a conservative scenario from the sourced numbers, not invented fees:

- Overspending caused by BNPL: the Harvard Business School study measured roughly $60/week in additional spending — call it $3,100/year. Let's assume you're more disciplined than average and count only half: $1,550/year

- Late fees: with 47% of users paying late each year and fees per missed order, a realistic $50-100/year for a regular user

- Interest, if you slide into monthly financing plans (up to 36% APR) or carry card debt to cover BNPL payment months: easily $200+/year

Conservative total: roughly $1,800-2,900/year flowing out instead of into investments.

Take the midpoint — about $2,350/year — and invest it instead at a 7% average annual return: that's roughly $32,500 after 10 years, and nearly $100,000 after 20.

So a typical BNPL habit plausibly costs tens of thousands of dollars in lost compound wealth over a decade — almost all of it from purchases you wouldn't otherwise have made.

How This Delays FIRE

FIRE is fundamentally about one equation: Savings Rate = Path to Freedom.

- 50% savings rate = 17 years to FI

- 60% savings rate = 12.5 years to FI

- 70% savings rate = 8.5 years to FI

But BNPL reduces your effective savings rate through:

- Direct costs (the $1,800-2,900/year scenario above)

- Psychological burden (reducing motivation)

- Credit damage (increasing future borrowing costs)

A drag of that size on a typical savings rate can extend your FIRE timeline by 2-4 years.

For someone planning to reach FIRE at 40, BNPL pushes it to 42-44.

For someone planning to reach FIRE at 45, BNPL pushes it to 47-49.

This is why the FIRE movement emphasizes eliminating consumer debt first — it's the biggest brake on your path to financial independence.

Real Example: Emma's FIRE Timeline

Without BNPL:

- Income: $75,000/year

- Savings rate: 45% = $33,750/year invested

- Target FI number: $1.5M

- Years to FI: 18 years (by age 40)

With Average BNPL Usage (hypothetical):

- Income: $75,000/year

- Direct BNPL drag: -$2,500/year

- Effective available for investing: $31,250/year

- Plus psychological burden erodes discipline toward a 40% savings rate: $30,000/year

- Years to FI: 22 years (by age 44)

BNPL just cost Emma 4 years of freedom.

That 4-year delay compounds. At 7% annual spending (lifestyle inflation), that's roughly $100K+ in additional costs during those 4 years of working.

This is exactly why understanding the wealth equation — income × discipline × time — is so important. BNPL poisons all three variables.

Conclusion: Your Choice, Starting Now

BNPL isn't evil. But it is designed to exploit how your brain works.

It takes the friction out of buying on credit. It splits the cost into pieces too small to feel. It reaches the most financially vulnerable borrowers — 61% of originations go to subprime credit scores. It compounds across multiple platforms until the payment cliff arrives and you realize you're drowning.

And for a generation already struggling with housing costs, student debt, and inflation, BNPL is one more invisible drain on wealth they desperately need.

Here's what you need to know:

1. A single on-time pay-in-4 plan really is free — that's the loss leader. The costs live in what surrounds it: late fees, stacked plans, and financing plans at up to 36% APR.

2. BNPL is engineered to make you spend more. The measured effect is about $60 a week in extra spending — purchases you wouldn't make with a debit card.

3. BNPL now reaches your credit file. Since April 2025, Affirm reports all loans to Experian, and FICO's new scores incorporate BNPL data. Missed payments can follow you for years.

4. The overspend-and-fees drag plausibly delays FIRE by 2-4 years. A couple thousand dollars a year not invested compounds into tens of thousands over a decade.

5. You have alternatives. Save-first with a high-yield account, a 0% APR card used with discipline, a fixed-rate personal loan for big purchases — or one un-stacked BNPL plan with autopay, used deliberately.

If you're using BNPL right now, I'm not asking you to cut it out cold turkey. Follow the 4-step framework:

- Audit what you owe

- Calculate the true cost

- Set up payment reminders

- Implement the 48-hour pause rule

In 30 days, you'll have dramatically reduced your BNPL usage. In 90 days, you might eliminate it entirely.

The goal isn't perfection. The goal is awareness. Once you understand the true cost, your behavior changes naturally. Start by taking control of your finances — that's the foundation.

You don't need to be rich to use money wisely. You just need to be honest about what things actually cost.

BNPL is built to keep that total out of view. The platforms benefit when you don't add it up.

But now you know. You know the loan-stacking pattern. You know the late fee risk. You know the credit impact. You know the FIRE delay.

The question is: are you going to let frictionless payment technology cost you years of freedom?

Or are you going to take back control?

The answer you give to yourself today determines the freedom you have (or don't have) in 10 years.

Make it count.

📩 Have questions about your BNPL situation? Email me at dennis.vymer@myfinancialfreedomtracker.com.

For better control of your BNPL spending, use MFFT's budgeting dashboard to track all your purchases in one place. Visibility is the first step to freedom. Or, if you're struggling with multiple types of debt, learn how to escape the credit card interest trap — the strategies are similar.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.