No Tax on Overtime: 2026 Rules, Caps & How to Claim It

You're working a Sunday double. Five hours of overtime, plus your usual 40.

Your buddy at the breakroom microwave looks up and says: "Don't worry, man. New tax law. You're not paying tax on any of that overtime."

You nod. You've heard the same thing on TikTok. On the radio. From your foreman.

There's just one problem.

He's wrong. The whole breakroom is wrong. And if you file your 2025 return based on that conversation, you're going to either claim three times more than you're entitled to — or miss the deduction entirely because nobody told you how it actually works.

The "No Tax on Overtime" deduction is real. It can save the right hourly worker $1,500 to $4,000+ on their 2026 tax bill. But almost everyone I've talked to has the math wrong.

Let me walk you through what's actually going on, what you actually qualify for, and exactly how to claim it without setting off an IRS audit.

What "No Tax on Overtime" Actually Is (And Isn't)

The provision comes from the One Big Beautiful Bill Act (OBBBA), signed in 2025. It created a brand-new federal income tax deduction for what the IRS calls "qualified overtime compensation" (IRS guidance).

A few things the marketing campaign did not make clear:

It's a deduction, not an exemption. Your overtime pay still hits your W-2. Then, on your tax return, you subtract a portion of it from your taxable income. The amount of tax you save depends on your marginal bracket.

Payroll taxes still apply. Social Security (6.2%) and Medicare (1.45%) come out of your overtime check just like always.

State income taxes may still apply. Most states haven't conformed to the federal deduction yet. Check your state.

It's temporary. The deduction only applies to tax years 2025 through 2028 (TurboTax explainer). After that, Congress has to renew it or it sunsets.

So "no tax on overtime" is a slogan. The real product is a federal income tax deduction — capped, phased out, and applied to part of your overtime pay. Let me show you which part.

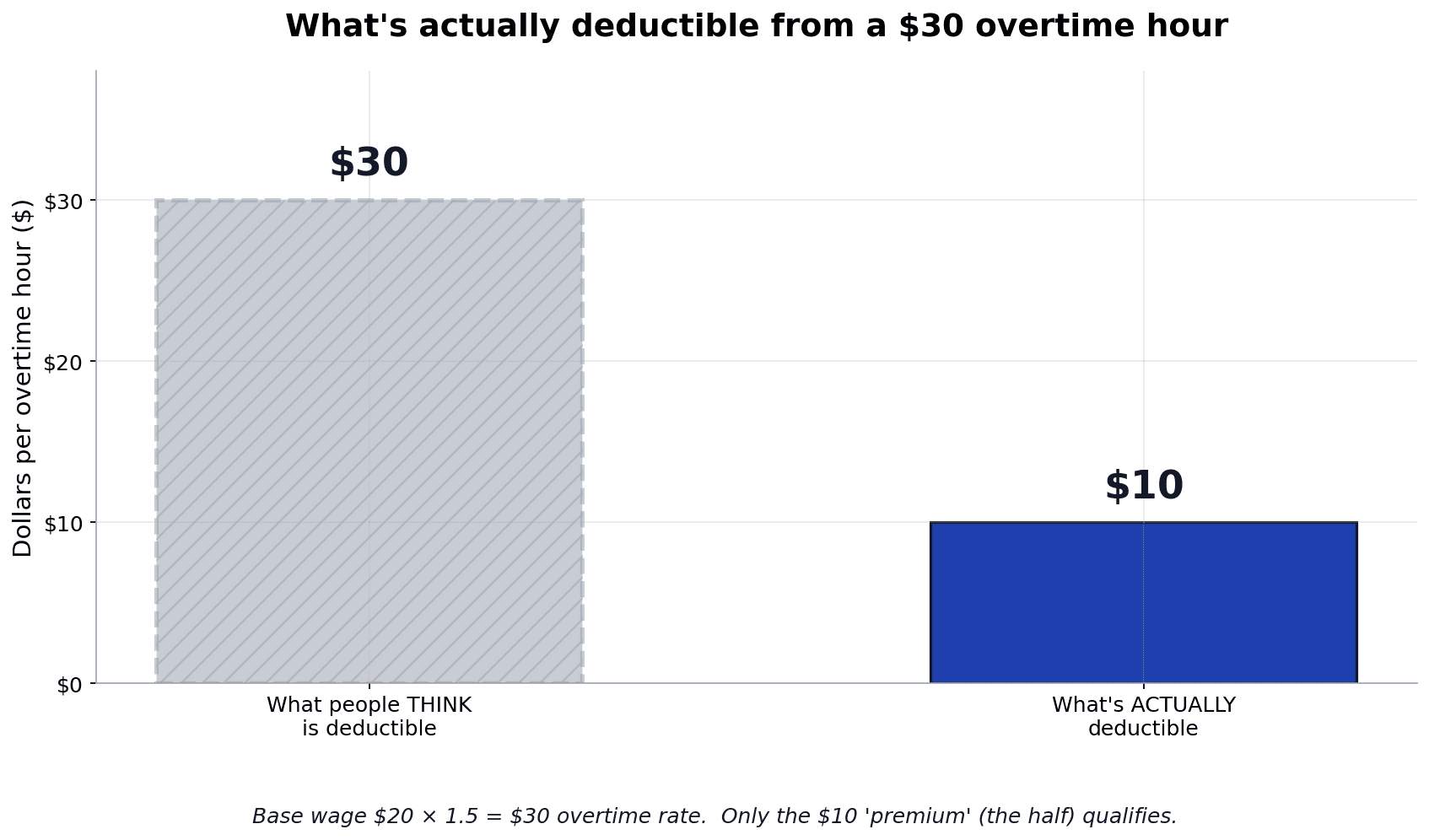

The Half Most Workers Are Missing

This is the part that trips everyone up.

When the FLSA requires "time and a half" for overtime, your overtime pay has two pieces:

- The regular rate portion (your normal hourly wage, but for hours over 40)

- The premium portion (the extra "half" on top of the regular rate)

Only the premium half is qualified overtime compensation. That's the only piece you can deduct (IRS Q&A).

Here's the cleanest way to see it:

If you normally make $20/hour and your overtime rate is $30/hour (1.5×), then for every overtime hour worked:

- $20 of that $30 is regular wages — not deductible

- $10 of that $30 is the premium — this is the qualified overtime

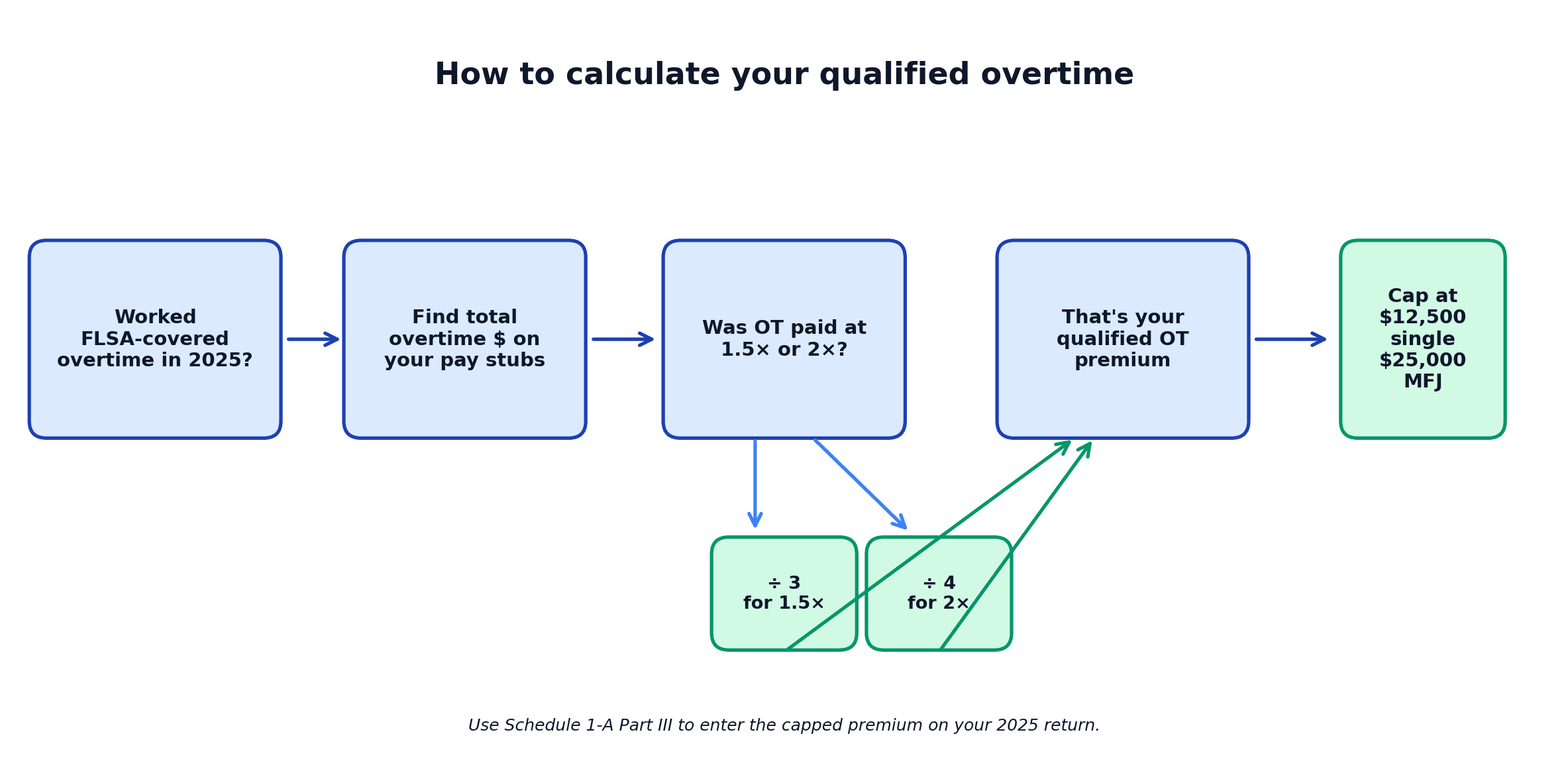

So if your pay stub shows a lump sum like $24,000 in overtime pay for the year, the qualified portion is $24,000 ÷ 3 = $8,000.

If you're paid double-time (some union contracts, holidays), divide by 4 instead. A $20,000 double-time check breaks down to $5,000 qualified overtime ($20,000 ÷ 4).

One sentence to remember: Take the total overtime line on your pay stub. Divide by 3 if you're paid 1.5× for OT, or by 4 if you're paid 2×. That number is your qualified overtime.

The CNBC tax-pros are already worried about this. Tom O'Saben at the National Association of Tax Professionals told CNBC in March 2026: "I think there could be a great deal of overstatement of that deduction." (CNBC). Filing the full overtime check instead of the premium portion could trigger an IRS notice or, worse, an audit.

The Caps and Phase-Outs

Here's where the IRS draws a line.

Maximum deduction:

- $12,500 if you file Single, Head of Household, or Qualifying Surviving Spouse

- $25,000 if you file Married Filing Jointly

Phase-out (the deduction shrinks and eventually disappears):

- Single: Phase-out begins at $150,000 MAGI

- MFJ: Phase-out begins at $300,000 MAGI

Married Filing Separately is excluded. If you and your spouse file separately, neither of you can claim the deduction at all (IRS Q&A). For most overtime-heavy households, MFJ is the right move anyway.

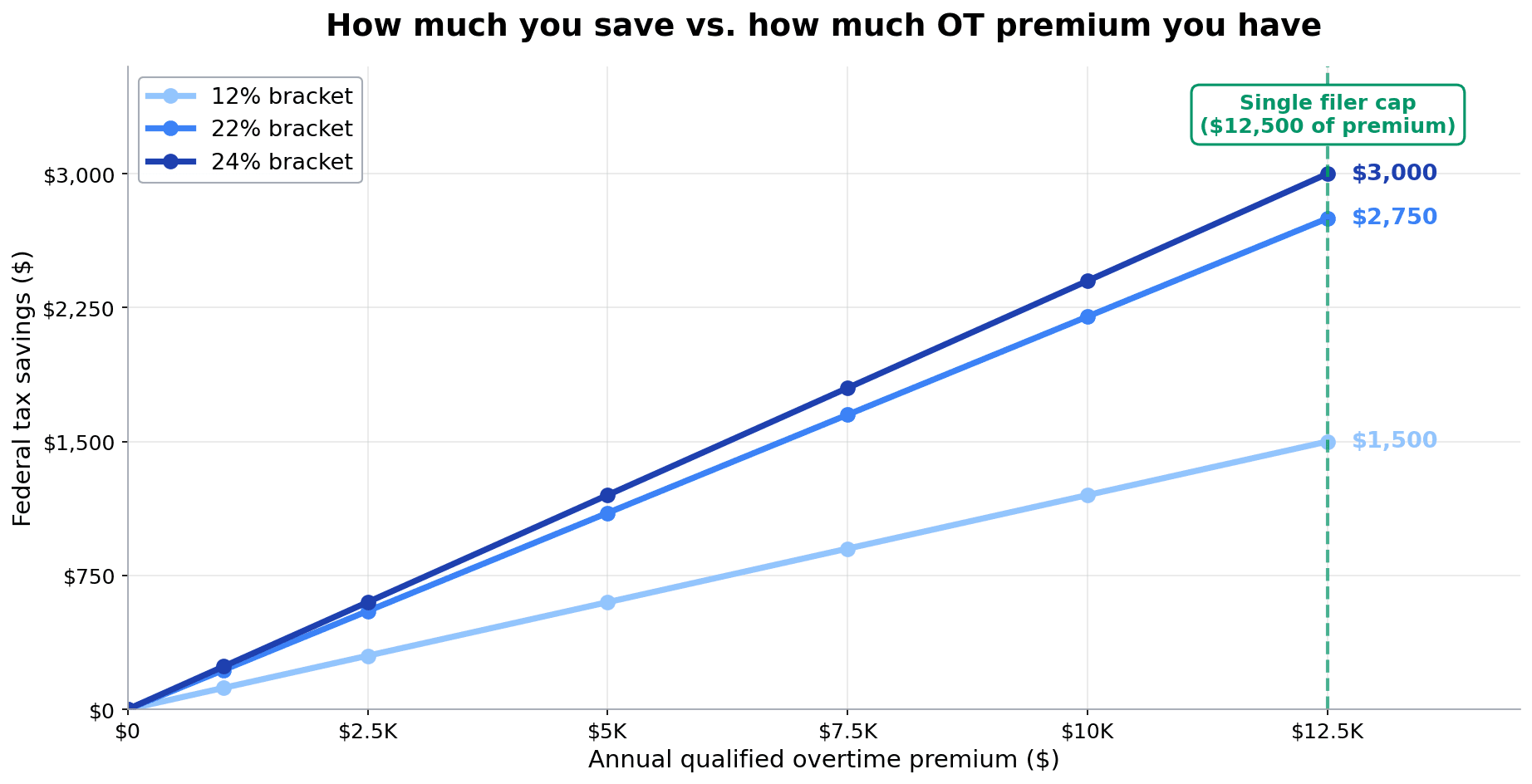

The dollar value of the deduction depends on your marginal tax bracket. Here's what it looks like at the cap:

| Marginal Bracket | Deduction at Cap (Single) | Tax Savings |

|---|---|---|

| 12% | $12,500 | $1,500 |

| 22% | $12,500 | $2,750 |

| 24% | $12,500 | $3,000 |

| 32% | $12,500 | $4,000 |

For a married filer in the 22% bracket maxing out at $25,000 deductible, that's $5,500 back.

Most hourly workers won't hit the cap — but the typical $3,000–$8,000 of qualified overtime still translates to real money.

Who Qualifies (And Who Doesn't)

The deduction is built around the Fair Labor Standards Act (FLSA) (DOL Fact Sheet 23). If FLSA doesn't require your overtime, this deduction doesn't help you.

You probably qualify if:

- You're an hourly, non-exempt worker

- You receive overtime pay required by the FLSA (over 40 hours/week)

- Your overtime is reported on a W-2, 1099-NEC, or 1099-MISC

- You have a valid Social Security Number

- You file as Single, HoH, MFJ, or Qualifying Surviving Spouse

You probably don't qualify if:

- You're a salaried exempt employee (executive, administrative, professional, outside sales, computer professional under FLSA — even if you sometimes work over 40 hours)

- You file Married Filing Separately

- Your "overtime" is a contractual bonus or shift differential not driven by FLSA section 7

- You're paid under a state-law overtime rule (like California's daily overtime) that exceeds FLSA — only the FLSA-required portion qualifies

Common edge cases:

- Tipped workers: You may qualify for both the No Tax on Tips deduction AND the No Tax on Overtime deduction. They're separate.

- Multiple jobs: Each W-2 can have its own qualified overtime — sum them up to one Schedule 1-A entry.

- Mid-year exempt-to-non-exempt switch: Only the non-exempt period counts.

- Independent contractors with 1099 OT: Yes, these can qualify if the payer reports qualified OT. Most won't.

If you're not sure whether you're FLSA non-exempt, look at your offer letter or ask HR directly. "Are my hours over 40 paid at 1.5× under the FLSA?" is the clean question.

How to Actually Claim It on Your Taxes

For the 2025 tax year (filed in 2026), the IRS released a new form — Schedule 1-A — on March 2, 2026 (IRS announcement). It handles all four OBBBA worker deductions: tips, overtime, car loan interest, and the senior bonus.

The two-step process:

Step 1. Fill out Part I of Schedule 1-A. You report your MAGI here so the form can apply the phase-out.

Step 2. Fill out Part III of Schedule 1-A — the qualified overtime section. Enter your qualified overtime premium (the "divide by 3" number from earlier), apply the cap and phase-out, and the form calculates your deduction.

The deduction then flows to your Form 1040. You can claim this deduction whether you take the standard deduction or itemize — that's a big deal. It's an "above the line" style deduction that reduces your AGI directly.

Watch out: Treasury and the IRS waived the 2025 W-2 reporting requirement in November 2025. Translation: most workers' W-2s for tax year 2025 will not have a separate qualified-overtime line. You have to compute it yourself from your final 2025 pay stub or YTD payroll statement (IRS guidance).

For tax year 2026 forward, employers must report qualified overtime separately:

- W-2 Box 12, code TT

- 1099-MISC Box 14

- 1099-NEC Box 1d

So 2025 is the most error-prone filing year. After that, your W-2 will hand you the number.

Documents to keep on file (audit-proofing):

- Your last 2025 pay stub showing YTD overtime

- Your overtime hours log (a simple spreadsheet is fine)

- Your offer letter or HR confirmation that you're FLSA non-exempt

- Your filing status confirmation if MFJ

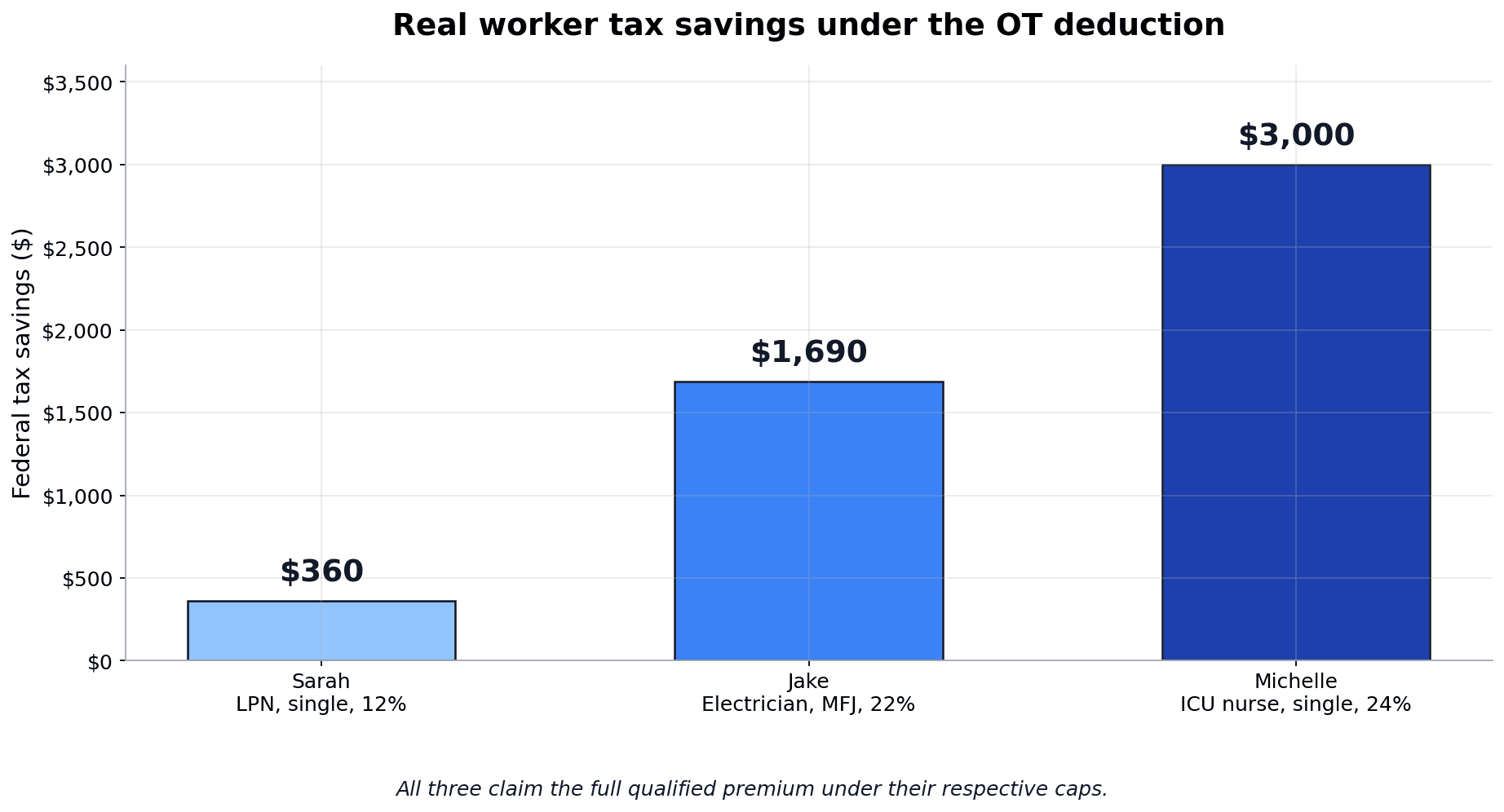

Real Worker Examples: What This Actually Saves

Numbers in the abstract are easy to ignore. Let me show you three real-world scenarios.

Sarah, LPN at a regional hospital

Sarah is single, no kids, makes $24/hour as a licensed practical nurse. She picks up about 5 hours of overtime each week for 50 working weeks a year.

- Hourly base: $24

- OT premium per hour: $24 × 0.5 = $12

- Annual qualified OT premium: $12 × 5 × 50 = $3,000

- Sarah's marginal federal bracket (single, ~$70K AGI): 12%

- Tax savings: $3,000 × 12% = $360

That's not life-changing. But it's $360 she didn't have last year — and Sarah uses it to top up her emergency fund. (More on what to do with the windfall in a minute.)

Jake, union electrician

Jake is married filing jointly, base $32/hour, runs 10 hours of OT every week for 48 weeks (he takes a couple weeks off).

- OT premium per hour: $32 × 0.5 = $16

- Annual qualified OT premium: $16 × 10 × 48 = $7,680

- Marginal bracket (joint, ~$130K combined): 22%

- Tax savings: $7,680 × 22% = $1,690

Jake's family puts that into their HSA and high-yield savings.

Michelle, ICU nurse hitting the cap

Michelle is single, base $42/hour, working 15-20 hours of OT every week during a hospital staffing crunch.

- Annual qualified OT premium: ~$14,000

- Capped at $12,500 (single)

- Marginal bracket (single, ~$110K): 24%

- Tax savings: $12,500 × 24% = $3,000

Michelle has $3,000 of "found money." But she also has ICU burnout. We'll come back to that.

The Top 5 Mistakes I See People Making

Tax pros are flagging these errors all over the place. Don't be the audit risk.

1. Deducting the full overtime check. This is by far the most common mistake. The deduction is the premium half — not the whole overtime line. Divide by 3 (or 4 for double-time).

2. Filing Married Filing Separately. MFS disqualifies both spouses from this deduction. If one of you has overtime, file jointly.

3. Ignoring the phase-out. Above $150K single / $300K MFJ MAGI, the deduction shrinks. Fill out Schedule 1-A Part I correctly.

4. Trying to deduct exempt-salaried "overtime." If you're an exempt employee paid extra for overtime hours as a discretionary bonus, that's not FLSA section 7 overtime. It doesn't qualify.

5. Not keeping documentation. With 2025 returns, the W-2 may not break OT out. The IRS hasn't said how aggressively it will scrutinize Schedule 1-A claims, but a one-page log of your weekly OT is cheap insurance.

If you've already filed and claimed too much, you can file an amended return (Form 1040-X) to correct it. Amending is far better than waiting for a CP2000 notice.

Should You Chase Overtime for the Tax Break?

Here's the honest answer most articles won't give you.

No. The tax break is a bonus on top of overtime you were going to work anyway. It's not a reason to volunteer for more shifts.

Why? Look at Sarah and Michelle.

Sarah saves $360 on her tax bill by working 250 hours of OT a year. She also gives up 250 hours of her life. That's $1.44 per hour of life saved.

Michelle saves $3,000 — better — but she's running 15-20 hours of OT every week. She is one staffing emergency away from burnout. And quiet burnout has its own brutal cost — your career trajectory, your health, and ultimately your earnings all suffer when you push past sustainable hours.

The math on chasing overtime almost never works out. Time-and-a-half pay (the base overtime, not the tax break) is already a great deal hour-for-hour. The tax deduction is gravy. But if you're trading sleep, family, and health for a 12% tax savings, you're trading a dollar bill for ninety cents.

A better option for many workers is a controlled, scalable side income — read The Side Hustle Paradox for the trade-offs. Side hustle income is also taxed and can be unpredictable, but you control the hours.

The framing that works: "I work the OT my employer needs. The tax deduction is found money. I deploy it intentionally."

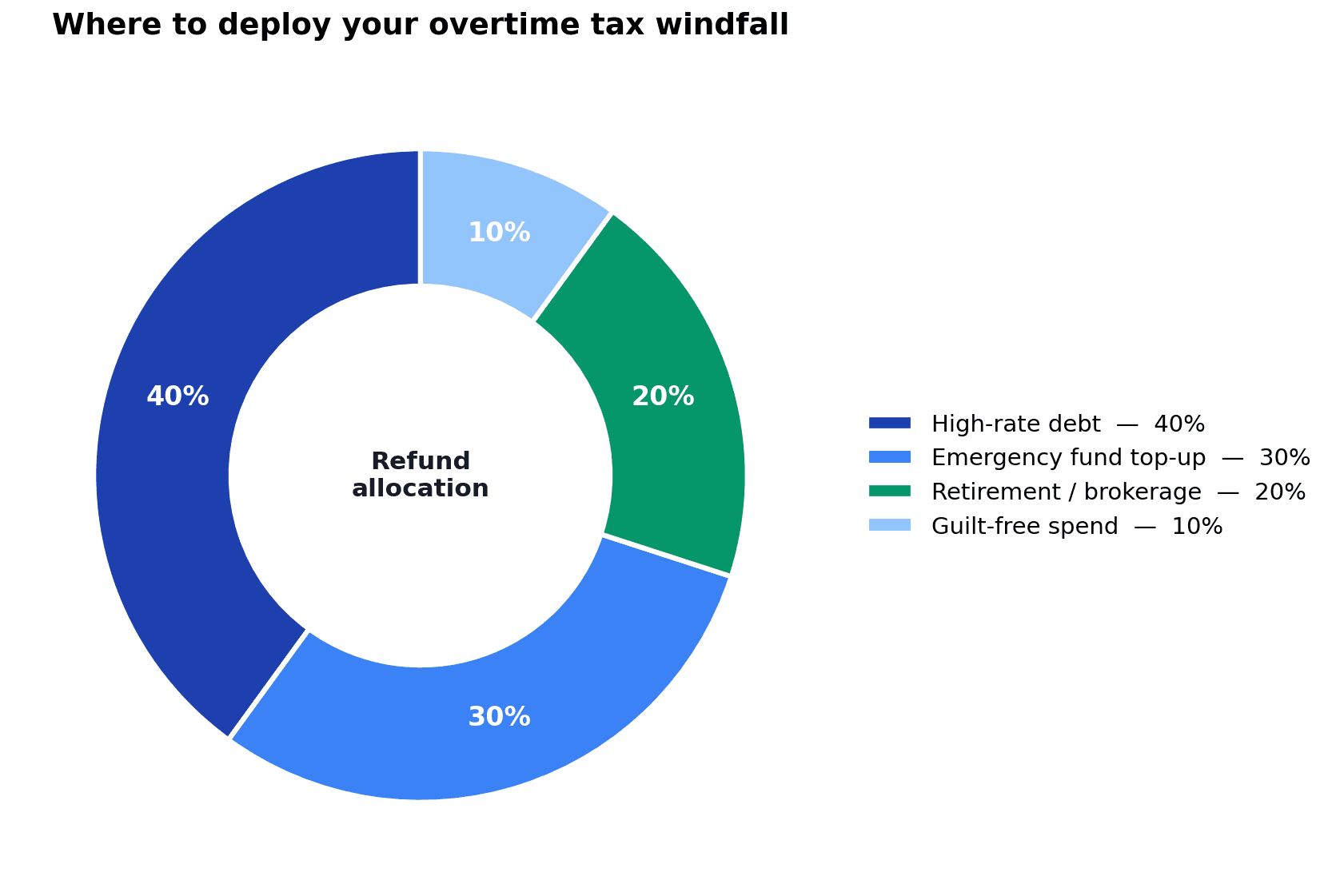

Where to Put the Windfall

If you're getting an extra $1,000–$4,000 back this year because of the OT deduction, here's the priority order I'd use.

1. Backstop your emergency fund first. If you don't have 3-6 months of expenses set aside, this is where the money goes. Period. The emergency fund crisis of 2026 is real — 59% of Americans can't cover a $1,000 emergency. Don't be in that group.

2. Crush high-rate debt second. With credit card APRs sitting above 20% in 2026 (the math is brutal), every dollar you throw at credit card debt earns a guaranteed 20%+ return. There is no investment that beats it.

3. Stack other 2026 tax wins third. The OT deduction isn't the only OBBBA win. The 2026 retirement contribution rules also changed — read my breakdown of the new contribution limits and the Roth catch-up trap before you set your 401(k) deferrals.

4. Invest the rest. After the emergency fund is full and the high-rate debt is gone, the OT windfall goes to retirement contributions or a taxable brokerage. Boring beats clever.

5. Don't lifestyle-inflate. The fastest way to lose this money is to roll it into a bigger car payment or a new subscription stack. Track the windfall as a separate line item.

A simple way to handle this: when the refund hits your account, immediately split it. 60% to debt or savings, 30% to investment, 10% guilt-free fun. Automate it the day the deposit lands.

Putting It All Together: Your 2026 Action Plan

Here's the simple checklist:

- Pull your final 2025 pay stub and find total YTD overtime pay.

- Divide by 3 (1.5× OT) or divide by 4 (double-time). That's your qualified overtime premium.

- Cap it at $12,500 single / $25,000 MFJ.

- File jointly if you're married. (No MFS.)

- Use Schedule 1-A when you file your 2025 return — Part I for MAGI, Part III for the OT deduction.

- Keep your pay stub and a hours log in a folder for at least 3 years.

- Decide where the windfall goes before the refund hits your account. Don't let it land in checking and disappear.

- For 2026 onward, your W-2 Box 12 code TT will list qualified OT directly — much easier.

The "No Tax on Overtime" provision is one of the few tax wins in the OBBBA aimed squarely at hourly, working-class Americans. Don't leave the money on the table — and don't claim three times what you're owed and end up with an IRS letter.

Track the qualified premium. Run the math. Deploy the savings on purpose. And get back to your life.

One last thing — if your overtime is part of a bigger budgeting picture (variable income, side gigs, irregular shifts), tracking the post-tax windfall in a budgeting tool helps. The whole reason MFFT's net worth + budgeting tracker exists is to catch exactly this kind of one-time inflow before it gets absorbed into normal spending. Make the deduction count.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.

Master Your Money

Master Your MoneyAI Scams Stole $21 Billion: How to Protect Yourself in 2026

AI scams hit a record $20.9B and could reach $40B by 2027. Scammers clone a loved one's voice from 3 seconds of audio. Here's the calm, free, afternoon-long defense playbook to protect your money in 2026.

Master Your Money

Master Your MoneyPrediction Markets: Why 69% of Polymarket Users Lose

69% of Polymarket users lose money and the top 1% take 76.5% of profits. The math, why Gen Z is targeted, and a 30-day reset plan.