Subscription Creep Audit: Find $1,600/Year in Hidden Charges

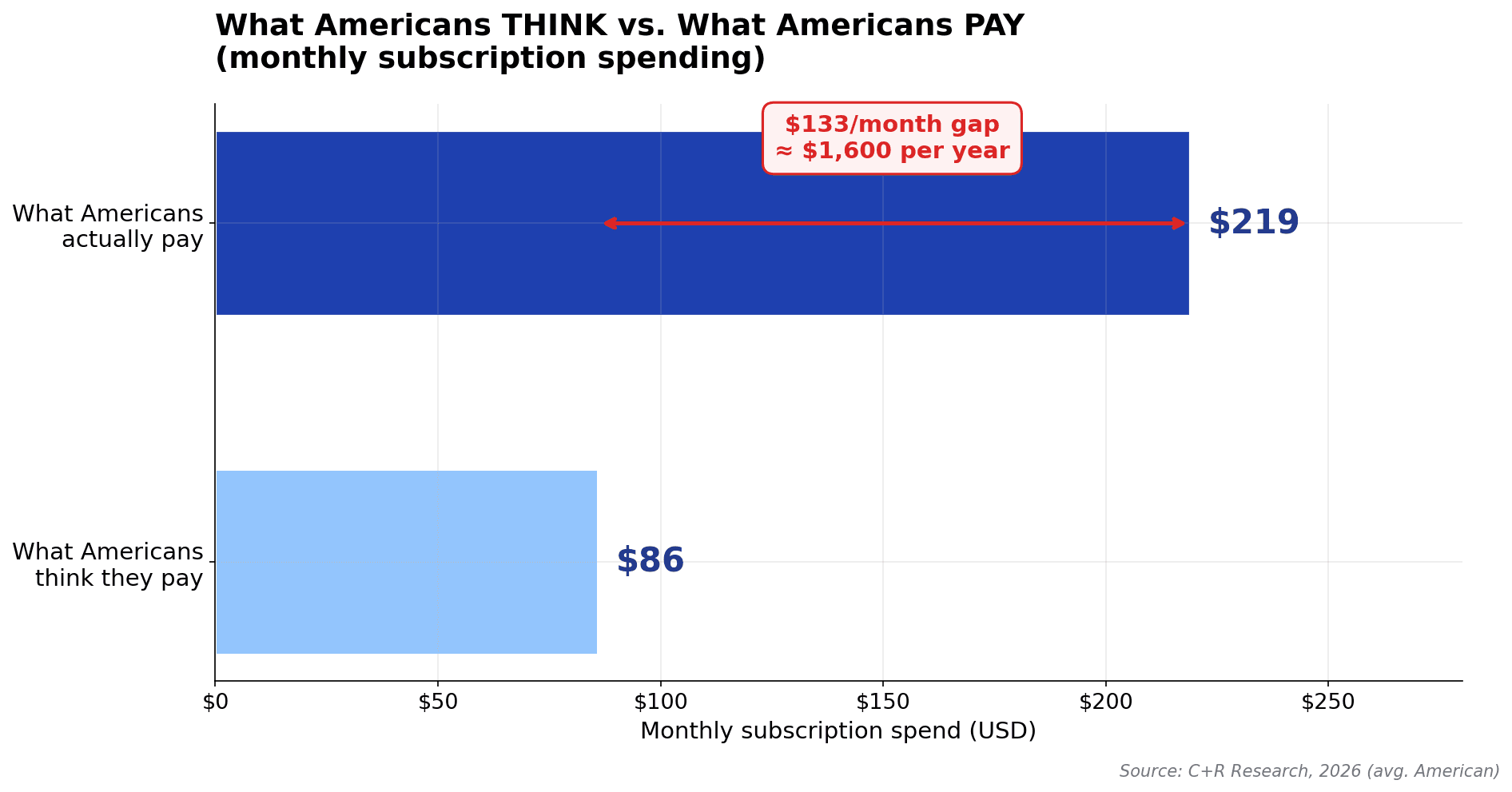

TL;DR: Americans estimate they spend $86 a month on subscriptions; itemized statements show the real average is $219 (C+R Research) — a roughly $1,600-a-year blind spot. The fix is a 30-minute audit: pull 90 days of statements, flag every recurring charge, triage into keep/pause/kill, and calendar the renewal dates. A "subscription firewall" — dedicated card, category cap, quarterly recheck — keeps it from creeping back. Invested at 7% instead, the average $219/month stack would compound to about $267,400 over 30 years.

New to taking control of your money?

If subscription creep is part of a bigger spending problem, start here:

- How to Start a Budget — the foundation that makes any audit possible

- The No-Buy Challenge 2026 — a 30-day reset that catches subscriptions in the act

- Emergency Fund 2026 — where to redirect the money you free up

You open your card statement. There's a $14.99 charge from a music app you haven't opened in eight months. A $9.99 charge from a meditation service you signed up for during a stressful week in 2024. A $24.99 charge from an AI tool you used twice. None of them feel like a big deal individually.

That's the trap.

Together, they're costing you more than your phone bill. Multiplied across ten years and the markets you're not investing in, they're costing you a small car. And they were designed to be invisible.

Welcome to subscription creep — the slow, silent leak that's now draining the average American household by $219 a month, while the average American thinks they're spending only $86. That gap, $133 per month, is real money. It's the difference between a stuck budget and one that finally works.

The good news? The tide is turning. In March 2026, the DOJ pulled $150 million out of Adobe over deceptive cancel terms. The FTC is rebooting Click-to-Cancel rulemaking. New York City stood up a junk-fee task force in January. For the first time in years, the dark patterns that built subscription creep are getting expensive to use.

This article walks you through exactly what subscription creep is, why it's so hard to see, the 30-minute audit that stops the bleeding, and the firewall system that keeps it from coming back. By the end, you'll know exactly how much you're actually paying — and how to redirect that money toward something that actually moves your life forward.

The Quiet $1,000-a-Year Money Leak (And Why You Can't See It)

Let me give you the headline number first.

A C+R Research study found Americans estimate they spend $86 a month on subscriptions. Their actual itemized spending averages $219 a month. That's a 2.5x perception gap — about $1,600 per year that people don't realize they're paying.

A separate 2026 analysis put the average household at $273 per month — over $3,200 a year.

Why is the gap so big?

Three reasons:

- The charges are individually small. Your brain registers a $99 unexpected charge. It doesn't register $14.99. Multiply by 5.6 (the average number of active subscriptions per consumer) and you've got the leak.

- The billing dates are scattered. Netflix charges on the 4th, Spotify on the 12th, that fitness app on the 28th. Your statement looks "normal" each cycle because no single charge stands out.

- The cancel paths are designed to be hard. I'll cover dark patterns in detail below. The short version: subscribing takes 1.5 clicks on average. Cancelling takes 6.7 clicks.

Here's where it stops being abstract. Rocket Money, one of the larger subscription-tracking apps, reports that on a typical user's first scan, they uncover $80–$100 a month in forgotten or unwanted subscriptions. Eighty to a hundred dollars a month, every month, gone.

That's not because the user is careless. It's because subscriptions are designed to creep.

What Is Subscription Creep, Really?

Subscription creep is the slow drift of recurring charges from "I chose this and use it" to "I forgot I had it and barely use it" — without you ever explicitly saying yes a second time.

It happens in three predictable ways:

1. Free trial conversions. You sign up for a 7-day or 30-day trial. You forget. The card gets charged. 48% of Americans have had this happen at least once. 65% of Millennials and 59% of Gen Z have done it more than once. Forty-two percent of consumers admit they were charged for a free trial they meant to cancel.

2. Silent price hikes. You signed up at $9.99/month. Now it's $14.99/month. Streaming alone has been a textbook example: Disney+ went from $6.99 at launch to $18.99 today (a 172% increase), and Netflix's premium tier just hit $26.99 in 2026. The new price slides into your statement quietly.

3. Dormant services. You used the writing app every day for a month, then once a quarter, then never. The charge keeps clearing. Your relationship with the service has changed; the billing relationship hasn't.

The point isn't that subscriptions are bad. The well-used ones are great value. The point is that subscription creep specifically targets the gap between intent and inertia, and that gap is where the money disappears.

The Math: What That $14.99 Really Costs You Over 10 Years

Here's the framing that changed how I look at small recurring charges.

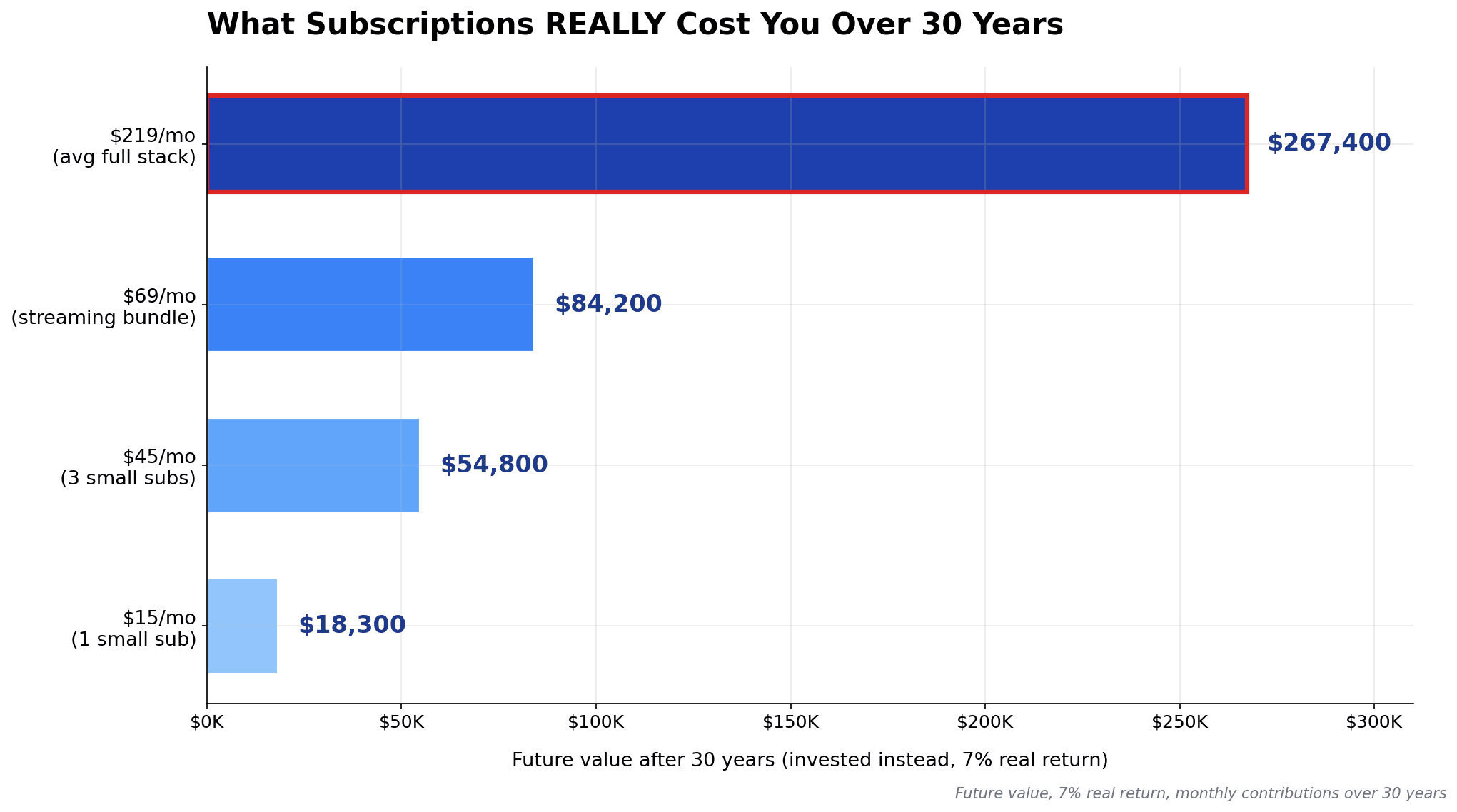

Every $14.99/month subscription you keep isn't really costing you $14.99. It's costing you whatever that money would have grown into if you'd invested it instead. At a conservative 7% real return, the math is brutal:

| Monthly subscription | 5 years | 10 years | 20 years | 30 years |

|---|---|---|---|---|

| $14.99/mo | $1,075 | $2,600 | $7,805 | $18,300 |

| $45/mo (3 small subs) | $3,225 | $7,800 | $23,400 | $54,800 |

| $69/mo (4 streaming services) | $4,945 | $11,950 | $35,900 | $84,200 |

| $219/mo (avg full stack) | $15,690 | $37,950 | $113,950 | $267,400 |

Read the bottom row again. The average American is on track to convert $267,400 into Spotify, Netflix, AI tools, and gym memberships they barely use — over a single working career.

This isn't an argument to cancel everything. It's an argument that "$14.99/month doesn't matter" is mathematically wrong. It matters a lot. It matters more than the coffee you'd skip in The Coffee That's Costing You Millions, and the math is even more compelling because subscriptions are automatic. You don't even have to make the choice each month — the leak just runs.

The point isn't to feel bad about past charges. They're sunk. The point is to recognize that every month going forward is a fresh decision about which compounding outcome you want.

The 30-Minute Subscription Audit (Step-by-Step)

Here's the audit I do every quarter. It really does take about 30 minutes the first time, and 5 minutes after that.

Step 1: Pull 90 Days of Statements (5 minutes)

You need three months because some subscriptions bill quarterly or annually. Some bill on different cycles than your card month, so the longer window catches them all.

Pull statements from:

- Every credit card you use

- Your primary checking account

- PayPal, Apple Pay, Google Pay, and any other wallet that auto-pays

If you're using a budgeting app like MFFT, your recurring transactions are already grouped — start the audit there instead of paging through PDFs.

Step 2: Flag Every Recurring Charge (10 minutes)

Highlight any charge that:

- Repeats with the same merchant name

- Has a "round" amount ($9.99, $14.99, $19.99, $4.99)

- Comes from a brand you can't immediately recognize

That last one matters. Subscription billing often appears under a parent company's name or a payment processor (PADDLE.COM, STRIPE *XYZAPP) that doesn't match the product you remember signing up for.

Step 3: Triage Into Keep / Pause / Kill (10 minutes)

For each subscription, ask one question: "If this charge wasn't on my card and I had to actively re-enroll today at the current price, would I?"

That single question is the heart of the audit. If you'd re-enroll without hesitation, it's a Keep. If you'd hesitate, it's a Pause. If you'd say no, it's a Kill.

A useful sanity check: pull up the app or service and look at the "last used" date. If it's been more than 30 days and you're paying monthly, that's a strong signal toward Pause or Kill.

Step 4: Calendar the Renewal Dates (5 minutes)

For everything you're keeping, add a calendar event 5 days before the renewal date. The reminder is about control, not cancellation. When the renewal hits, you've already had a moment to ask: still worth it?

For everything you're killing, do it now while the audit is fresh. We'll talk about the dark patterns in the next section — be ready.

For everything you're pausing: most services let you pause for 30, 60, or 90 days. This is the most underused option in personal finance. Pausing tells you whether you actually miss the service.

The 2026 Subscription Creep Crackdown: What's Actually Changing

For years, the regulatory environment let dark-pattern cancellations run unchecked. That's shifting in 2026, and it matters for your audit.

Adobe's $150 million settlement (March 13, 2026). The DOJ and FTC settled with Adobe for $150 million over hidden Early Termination Fees and intentionally hard-to-find cancel buttons. Half of that ($75M) goes to consumer relief — affected subscribers may receive one to two months of free Creative Cloud or refunds of paid termination fees. Going forward, Adobe must clearly disclose any termination fee before enrollment, send a heads-up before any 7+ day free trial converts, and provide an easy cancel path.

FTC Click-to-Cancel — vacated, but not dead. The Eighth Circuit vacated the FTC's Negative Option Rule in July 2025 on procedural grounds. But on March 11, 2026, the FTC issued an Advance Notice of Proposed Rulemaking — they're explicitly considering reviving the core requirements. Until a new rule lands, the underlying ROSCA (Restore Online Shoppers' Confidence Act) still applies, and the FTC has continued enforcement against deceptive cancel practices.

State-level laws. California (SB 313, AB 2863), Colorado, and Tennessee maintain easy-out subscription cancellation laws. Several pre-date the FTC's effort and remain in force.

NYC junk-fee task force. Executive Order 9 (January 5, 2026) established a citywide task force directing the Department of Consumer and Worker Protection to crack down on hidden fees and subscription traps.

What this means for you, practically: if you hit a wall trying to cancel — required calls, mandatory verification, fees you weren't told about — you may have grounds for a complaint with your state AG or the FTC. The Adobe settlement is the proof of concept that companies are now writing real checks for this behavior.

Dark Patterns to Watch For (And How to Beat Them)

In a 2024 sweep across 27 countries, the International Consumer Protection and Enforcement Network audited 642 subscription platforms. 75.7% used at least one dark pattern. 66.8% used two or more.

Knowing the patterns is half the battle. Here are the ones you'll meet most often, and how to handle each:

The roach motel. Easy to enter, hard to leave. The cancel button is buried five clicks deep under "Account → Settings → Membership → Manage Plan → Cancel".

Counter-move: Search the company's help docs for "cancel subscription" and follow the breadcrumb directly. Bookmark the cancel URL.

Confirmshaming. "Are you sure? You'll lose all your saved playlists / progress / data!"

Counter-move: That's the point. The data you'll lose is data they're using to keep you paying. Cancel anyway.

Forced re-engagement. Phone calls, postal mail, "schedule a chat with a retention specialist" — anything that adds friction to canceling but not to subscribing.

Counter-move: Document what they're asking for. Many states (and the FTC under ROSCA) require parity between sign-up and cancel friction. If they require a 20-minute call to cancel a service you signed up for in 1.5 clicks, that's likely illegal.

Retention discount loops. "Stay 3 more months at 50% off!" — which often quietly resets your contract to a fresh 12-month term.

Counter-move: Read the offer. If it resets the contract or comes with new terms, decline. If you genuinely want a discount, ask for it without committing to additional time.

Account-required cancellation. You forgot the password to the billing portal. They make you reset it. The reset link goes to the email you no longer use.

Counter-move: Most banks let you block specific merchants or reject future charges from a specific recurring vendor. This is your "I give up trying to cancel" nuclear option.

Hidden Early Termination Fees. You didn't know there was an annual contract. Now you owe 50% of the remaining 8 months.

Counter-move: Always read the cancellation terms BEFORE you subscribe. Adobe just paid $150 million for hiding these.

The throughline: when you can't cancel through the company's interface, your card issuer is your backup. Most major issuers will help you stop unauthorized recurring charges, especially for known dark-pattern offenders.

Pause vs. Kill: A Decision Framework

Not every subscription should die. The trap of every "cancel everything" guide is that it ignores how subscriptions actually work in life — some serve you well, some serve you sometimes, some serve you not at all.

Here's the framework I use:

Keep if all three are true:

- I've used it in the last 14 days

- It serves a goal I actively have right now (not "someday")

- If forced to re-subscribe at the current price today, I would

Pause if any of these are true:

- I haven't used it in 30+ days but I'm not sure I'm done with it

- The service offers a pause feature (most streaming, fitness, and AI tools do)

- The pause length is 30 days or longer

Kill if any of these are true:

- I haven't used it in 90+ days

- I've been "meaning to use it" for more than a month

- I forgot it existed before this audit

- The service no longer matches my goals (e.g., a fitness app I signed up for during a 2024 New Year's reset)

A useful rule of thumb: if you have to convince yourself to keep it, kill it.

Building a Subscription Firewall (So It Stops Creeping Back)

The reason most audits fail isn't the audit. It's the rebound.

People purge $200/month in subscriptions, feel great, then sign up for three new things over the next four months because the underlying habits didn't change. The firewall is the system that prevents the creep from rebuilding.

1. Use a Dedicated Subscription Card

The most effective tactical move: use one card for ALL recurring charges, and only that purpose. A virtual card from your bank (most major issuers — Capital One, Citi, Chase, and most credit unions — offer them) makes this easy. Some banks even let you set per-merchant spending caps.

The win: you can scan one statement and see every subscription. New ones can't sneak in across multiple cards.

A related move worth knowing about, especially if you're trying to keep card debt under control: pair the dedicated subscription card with the strategy in Credit Card Interest Rates Hit 20%+. The subscription card should be a card you pay off in full every month — never a slow-roll.

2. Set a Subscription Category Limit

In your budgeting tool, give "Subscriptions" a hard monthly cap. The cap forces an active choice when a new subscription pushes you over. MFFT users can set this as a category limit and see in real time when a new recurring charge crosses the line.

3. Quarterly Recheck

Calendar event every 90 days, 30 minutes blocked. Repeat the audit — but with the audit done once, future passes take 5 minutes because most charges are already labeled.

4. The "Before You Subscribe" Checklist

Before any new recurring charge clears, you ask:

- Where will this charge appear? (Card name, billing descriptor)

- When does the free trial end? (Calendar reminder set NOW)

- How do I cancel? (Find the cancel link before you sign up)

- Are there termination fees? (Read the contract)

- What does this replace? (If it's not replacing anything, it's adding to your stack)

That last question kills more bad subscriptions than any other.

5. Redirect, Don't Just Save

The most effective psychological move: as soon as you cancel a subscription, set up an automatic transfer of that exact amount into your emergency fund or investment account. Otherwise the money disappears into general spending and you don't feel the win. Treat your emergency fund as the natural destination — that's $80–100/month flowing toward security instead of streaming.

FAQ: The Edge Cases

"What about bundles?" Bundles save money only if you'd have bought every component separately. The Disney+/Hulu/ESPN bundle at $20/month with ads is a deal if you actively watch all three. If you only watch Hulu, the bundle is more expensive than the standalone. Audit each bundle component as if it were standalone.

"What about family/student plans?" Same logic. The Spotify Family plan is great if 4+ people in your household actually use it, terrible if it's really 2 people sharing a $19.99/month plan instead of two $11.99 individual plans.

"What about AI tool subscriptions in 2026?" This is the new frontier of subscription creep. Many people now have ChatGPT Plus + Claude Pro + Cursor + Perplexity + Notion AI + a writing tool — easily $100/month. If your work depends on one or two of them daily, fine. But the "I'll keep this in case I need it" stack is exactly the inertial spending the audit is designed to catch.

"What about subscriptions for businesses or freelancers?" Subscriptions are a legitimate operating expense and often tax-deductible — but the audit logic still applies. The question shifts from "do I use it personally" to "what's the ROI per tool, and could a free or cheaper alternative cover 90% of the use case?"

"My friend says they 'cancel and re-sign-up' to get the discount price every year." It works for some services and not others. It's a legitimate strategy, but only if you actually leave for the lockout period — re-signing up immediately often disqualifies you from the new-customer pricing. Treat it as a "high effort, low reward" move; the firewall above scales better.

"How is this different from just budgeting?" A budget tells you how much you spent. A subscription audit tells you which specific recurring decisions are still serving you. The two work together — and both feel less restrictive when you've talked about them out loud, the way Loud Budgeting makes spending choices socially normal.

Conclusion: Stop Renting Your Future to Things You Don't Use

Subscription creep is small charges, but it isn't a small problem. The average American household is leaking $219 a month — over $2,600 a year — to recurring charges they've half-forgotten about. Compounded over a working career, that's a quarter of a million dollars rented out to streaming services and apps that often don't even survive the year.

The audit takes 30 minutes. The firewall takes 30 minutes a quarter to maintain. The tradeoff isn't even close.

You don't need to cancel everything. You don't need to live a stripped-down life. You just need to do what subscription companies bet against you ever doing: look at what you're actually paying for, and decide which of it still serves you.

So here's your assignment for this week: pull 90 days of statements, run the audit, and pick one service to cancel today. Just one. That's the first crack in the dam.

Tell me what you cancelled. I want to know how much you got back.

📩 Have questions or want to share your audit results? Email me at dennis.vymer@myfinancialfreedomtracker.com.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyRent vs Buy in 2026: I Ran the Numbers, Kept Renting, and Invested the Difference

My uncle swears renting is throwing money away. So I built the rent vs buy 2026 model: renting wins in all 50 metros, but only if you invest the difference.

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.