RAP Student Loan Plan: Formula, vs IBR & How to Switch

New to budgeting student-loan debt?

If this is your first deep dive into repayment plans, start here first:

- Student Loan Payments Resume in 2026 — the broader resumption playbook

- How to Start a Budget — where the new payment has to fit

- Hybrid Debt Payoff Method — how to attack the loan once you pick a plan

Picture Sarah, an entry-level marketer in Minneapolis making $45,000 a year.

For two years her federal student loan payment was $48 a month under SAVE. The math worked: rent was up, groceries were up, but the loan was a rounding error.

Then the email arrives. Subject: "Action required — your repayment plan is ending." She skims it twice. The pause is over. She has 90 days to pick a new plan. If she does nothing, she gets dumped into the Standard 10-year plan at about $440 a month — almost a tenth of her take-home pay, gone.

Sarah isn't alone. 7.5 million federal student loan borrowers received the same notice this spring after the Eighth Circuit Court of Appeals vacated SAVE on March 10, 2026. The replacement — the Repayment Assistance Plan (RAP) — launches July 1, 2026. So does a new Tiered Standard Plan, and so does the auto-enrollment trap that will quietly triple some borrowers' monthly bills.

This article is the do-the-math piece you were promised but probably haven't found yet. We'll walk through exactly how RAP is calculated, what its two best-kept secrets are, when it beats IBR (and when it doesn't), and the six-step playbook to switch before your 90-day clock runs out.

What Just Happened to SAVE — and What's Replacing It on July 1, 2026

Let's start with the timeline in plain English.

The Saving on a Valuable Education (SAVE) Plan launched in 2023 as the lowest-payment income-driven repayment plan ever offered to federal student-loan borrowers. It cut undergraduate payments to 5% of discretionary income, eliminated negative amortization, and put roughly 7.5 million people on payments most could actually afford.

It also got sued.

On March 10, 2026, the U.S. Court of Appeals for the Eighth Circuit officially vacated SAVE, ruling that the Department of Education had exceeded its statutory authority. The Department began issuing guidance to enrolled borrowers later that week. As of May 2026, paper notices are now arriving in mailboxes.

Three dates to remember:

- July 1, 2026 — RAP and the new Tiered Standard Plan go live. Borrowers in administrative forbearance under SAVE start being moved out.

- The day your notice arrives — your personal 90-day clock starts. Miss it and you are placed into the Standard Plan automatically.

- July 1, 2028 — the legacy PAYE and ICR plans disappear entirely. Anyone still on them transitions to RAP or IBR.

For most people the practical deadline is about October 1, 2026 — 90 days after the July 1 notices that the Department of Education has confirmed it will send.

That's the legal backdrop. The financial backdrop matters more. With credit card 90-day delinquencies at 7.05% as of May 2026 and the average federal balance at $39,633, the household budget can't absorb a doubled payment without something breaking.

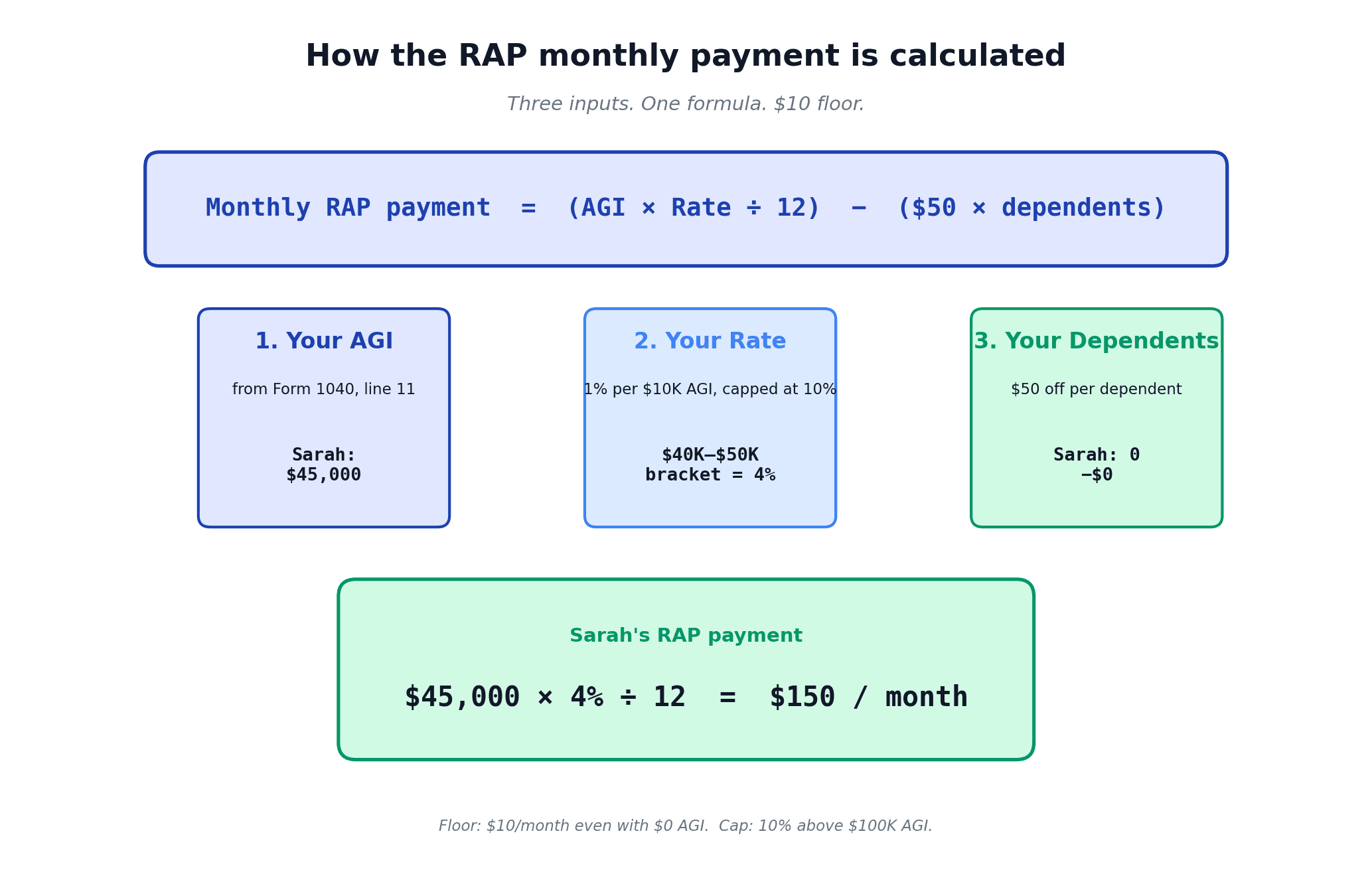

The RAP Formula in Plain English (With the Actual Numbers)

Here is the single most important formula in this article. Tape it to your laptop.

Monthly RAP payment = (AGI × Rate ÷ 12) − ($50 × dependents), with a $10 minimum.

The Rate is set by which $10,000 bracket your Adjusted Gross Income falls into:

| Your AGI | Rate |

|---|---|

| Up to $10,000 | flat $10/month |

| $10,001 – $20,000 | 1% of AGI |

| $20,001 – $30,000 | 2% |

| $30,001 – $40,000 | 3% |

| $40,001 – $50,000 | 4% |

| $50,001 – $60,000 | 5% |

| $60,001 – $70,000 | 6% |

| $70,001 – $80,000 | 7% |

| $80,001 – $90,000 | 8% |

| $90,001 – $100,000 | 9% |

| $100,001 and up | 10% (capped) |

That's it. Eleven brackets, one number per dependent, $10 floor.

Let's run Sarah. AGI $45,000, no kids, single. Bracket: 4%. So $45,000 × 4% = $1,800/year, divided by 12 = $150/month. No dependents to subtract. Done.

Now Jake — a nurse making $75,000 with two kids. Bracket: 7%. So $75,000 × 7% = $5,250/year, divided by 12 = $437.50/month. Subtract 2 × $50 = $100. $337.50/month.

Notice what's not in the formula: your loan balance, your interest rate, your school, your degree. RAP cares about your AGI and your dependents. Nothing else.

RAP's Two Best-Kept Secrets: The Interest Waiver and the $50 Principal Subsidy

Most of the coverage so far has stopped at the formula. But two RAP features quietly change the math of long-term debt payoff, and they're worth understanding before you compare plans.

Secret #1 — The unpaid interest waiver. If your RAP monthly payment is less than the interest accruing on your loans that month, the difference is waived, not capitalized. Your loan balance literally cannot grow due to negative amortization. Under the old IBR/PAYE/REPAYE plans (and under the Standard Plan), unpaid interest gets tacked on or eventually capitalized into your principal, and the balance creeps upward for years.

Sarah's $39,633 balance at 6% interest accrues about $198/month in interest. Her RAP payment is $150. The other $48? Waived. Her balance does not grow.

Secret #2 — The $50 principal subsidy. If a RAP payment doesn't reduce your principal by at least $50 in a given month, the Treasury tops it up so it does. That sounds small. It's not. Over a year that's $600 of free principal reduction; over a decade it's $6,000.

Put both together for Sarah: her loan balance not only stops growing, it drops by at least $50 every month with the subsidy active, on top of any actual principal she does pay down. Even at her low income, the loan starts shrinking from day one.

This is the part the headline calculators usually skip. RAP isn't just a different payment — it's structurally designed to keep balances from spiraling.

RAP vs IBR vs the New Tiered Standard Plan: Side-by-Side Math

Here is where most people get stuck. The rules tell you what each plan does. They don't tell you which one to pick.

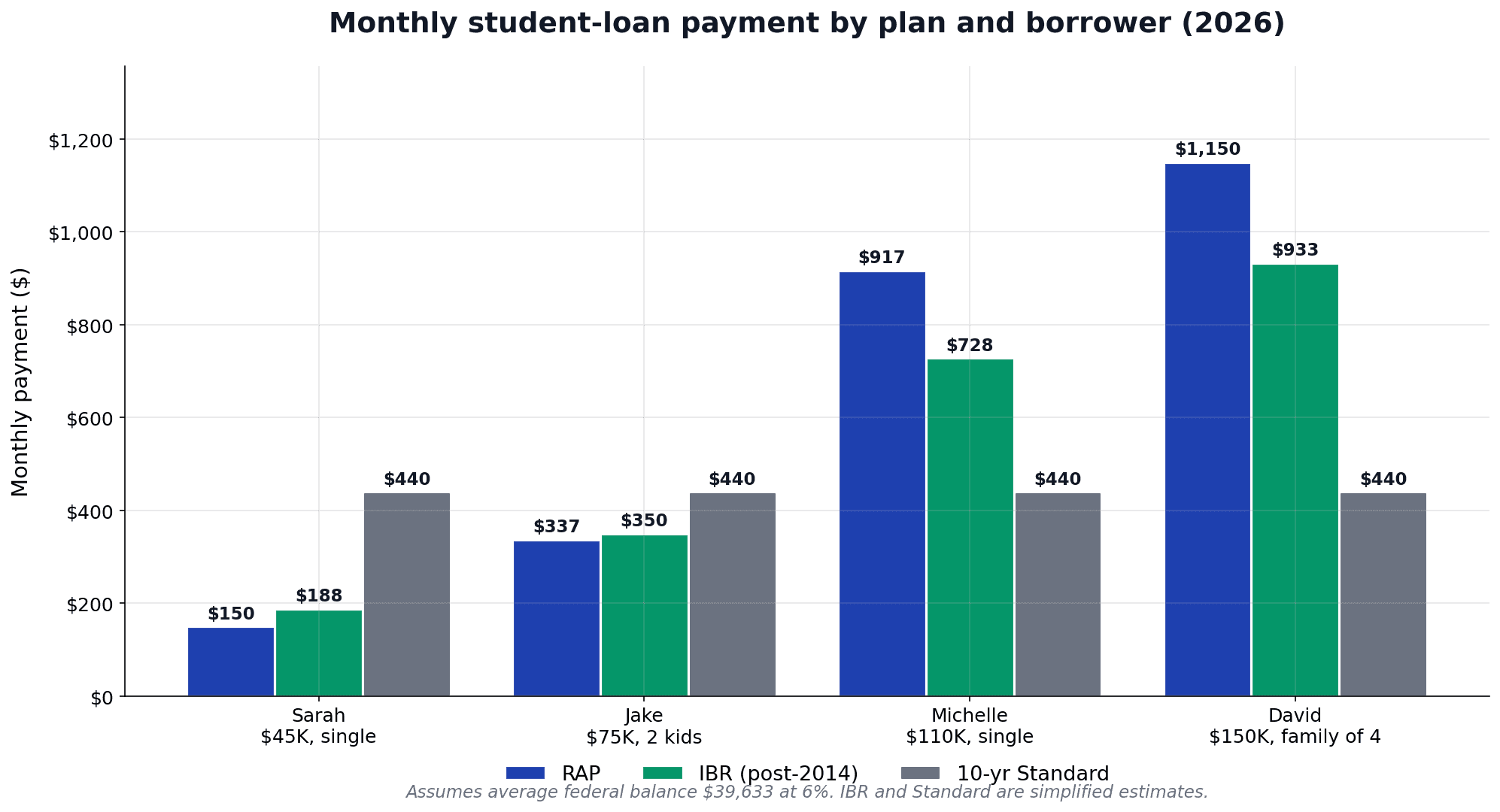

Below is the side-by-side cost for four representative borrowers, all assuming the average $39,633 federal balance at 6%, family-of-1 unless noted. IBR here is the post-2014 version: 10% of discretionary income, capped at the 10-year Standard payment, 20 years to forgiveness.

| Borrower | RAP | IBR | New 10-yr Standard | Cheapest |

|---|---|---|---|---|

| Sarah — $45K, 0 deps | $150/mo | ~$188/mo | ~$440/mo | RAP |

| Jake — $75K, 2 deps | $337/mo | ~$350/mo | ~$440/mo | RAP |

| Michelle — $110K, 0 deps | $917/mo | ~$728/mo | ~$440/mo | Standard, then IBR |

| David — $150K, 2 deps (family of 4) | $1,150/mo | ~$933/mo | ~$440/mo | Standard, then IBR |

The pattern jumps out immediately. RAP wins under about $100K AGI. IBR (or even the Standard Plan) wins above $100K because RAP has no payment cap — once you cross into the 10% bracket, RAP keeps climbing while IBR is capped at what the 10-year Standard plan would charge.

If you only remember one rule from this article, make it that one.

But monthly cost isn't the whole picture. Forgiveness timelines matter too:

- RAP: 30 years to forgiveness — the longest of any current plan.

- IBR (post-2014): 20 years.

- IBR (pre-July 2014 loans): 25 years at 15% of discretionary income.

- Standard / Tiered Standard: no forgiveness, you simply finish paying.

For a non-PSLF borrower with a stable middle income, IBR's 20-year clock can mean the loan is gone a full decade earlier than under RAP — even if RAP's monthly payment is slightly cheaper. Run the math both ways before you commit.

The "Do Nothing" Trap: The Tiered Standard Plan

If you ignore the notice, you do not stay on SAVE. You do not get a grace plan. You get auto-enrolled into the Tiered Standard Plan, with the repayment term set by your total balance:

- Up to $24,999 → 10 years

- $25,000 – $49,999 → 15 years

- $50,000 – $99,999 → 20 years

- $100,000 and up → 25 years

For Sarah's $39,633 at 6% over 15 years, that's ~$334/month — more than double her RAP payment, and she gets zero progress toward forgiveness. For Jake's family with the same balance, it's still $334/month versus $337 under RAP, but Jake forfeits the $50 principal subsidy and the interest waiver. Standard never wins for someone who could qualify for RAP.

The auto-enrollment is the single biggest risk in this entire transition. Treat the 90-day notice like a tax deadline.

The Decision Tree: Which Plan Should You Pick?

Here is a clean way to think about it.

Step 1 — Are you pursuing Public Service Loan Forgiveness (PSLF)? If yes: pick the IDR plan with the lowest monthly payment. RAP and IBR both count toward the 120 PSLF qualifying payments. Standard and Tiered Standard do not. Lower payment = more forgiven at month 121.

Step 2 — If no PSLF, is your AGI under $100,000?

- Under $100K: RAP almost always wins on monthly cost, and you get the interest waiver and $50 principal subsidy on top.

- Over $100K: run RAP and IBR through the studentaid.gov simulator. IBR usually wins because of the 10-year Standard cap.

Step 3 — How fast do you want the debt gone?

- Want it gone in 10–20 years and you can afford to pay extra: pick Standard or Tiered Standard, throw extra principal at it.

- Want the smallest monthly cost so you can invest the difference: RAP if under $100K, IBR if over.

Step 4 — Are you on pre-July 2014 loans? If yes, old-IBR's 15% discretionary income / 25-year forgiveness still applies. You usually want to switch to RAP, but model both — the original 15% IBR can be a bad deal at higher incomes and a good deal at low incomes.

That four-question tree handles the vast majority of borrowers. If your situation is unusual (Parent PLUS loans, joint income with a non-borrower spouse, very small balance under $10K, or active bankruptcy), book a 30-minute call with a non-profit credit counselor or a fee-only advisor before you commit.

How to Switch — The 6-Step Playbook

Once your notice arrives, here is the exact sequence. Do not skip steps.

Step 1 — Find your AGI and dependent count. Pull your 2025 federal tax return (line 11). Note your dependent count from line 6. That's all the personal data RAP needs.

Step 2 — Log in to studentaid.gov. If you've never set up an FSA ID, do it now — the wait time can be 30 minutes when the site is busy. Confirm your servicer name (the company that sends your bills).

Step 3 — Run the Loan Simulator with RAP, IBR, and Standard. The studentaid.gov simulator was updated in May 2026 to include RAP. Plug in your AGI, family size, and current balance. Look at monthly payment AND total paid over the life of the loan.

Step 4 — Pick your plan, file the IDR application. One form (the same IDR application you'd file for any income-driven plan) is sufficient. You can request both RAP and IBR be evaluated and the lowest-cost option chosen automatically.

Step 5 — Verify your payment-count carryover. Any qualifying payments you've already made under SAVE, REPAYE, PAYE, or old IBR carry over toward both the new IDR forgiveness clock and PSLF. Confirm the count on the IDR confirmation page after your switch is processed.

Step 6 — Set up autopay for a 0.25% rate cut and a 30-day calendar reminder. Autopay is the cheapest way to ensure a payment never lands late. Set a separate calendar reminder 30 days before each year's IDR recertification deadline.

The whole process takes about 45 minutes once your FSA login is set up. Procrastination here is expensive.

What This Means for Your FIRE, Emergency Fund, and Budget

The right repayment plan is a starting point, not the finish line. The plan choice changes how much cash flow you free up — and that cash flow is the lever for everything else.

For a FIRE-focused budget, RAP's $50 principal subsidy and interest waiver function as a quiet, automatic accelerator. Combine RAP with a 1% raise each year that you funnel entirely to extra principal, and a $39,633 balance disappears in under a decade for most middle-income borrowers — without inflating monthly payments. That cash gap is what you redirect into a Roth IRA or your taxable brokerage.

If your bigger problem is monthly cash flow rather than long-term payoff, RAP is still the safer landing. Pair it with the framework in How to Start a Budget, and the new payment slots in as a fixed expense alongside rent and utilities.

If you are also juggling credit-card or auto debt, the Hybrid Debt Payoff Method shows how to sequence which loan to attack first. Under RAP, the student loan is essentially "paused with progress" — its balance shrinks automatically — which lets you direct extra dollars to higher-interest debt.

And before you put a single extra dollar toward principal, build the buffer that the Emergency Fund Crisis 2026 lays out. A missed RAP payment still triggers servicer fees and a credit-report ding even if your "real" payment is $0.

Finally, if you are aiming for FIRE Movement-style early retirement, the IDR choice quietly changes your timeline by years. The 20-year IBR clock is a full decade shorter than RAP's 30. For non-PSLF borrowers willing to pay slightly more per month, IBR can mean a debt-free FIRE date a decade earlier — at the cost of a tighter monthly budget today. There's no universal right answer; there is a right answer for your numbers.

Bottom Line: Who Wins Under RAP, Who Loses, and What to Do This Week

Boil 2,500 words down to the four lines you need:

- Under $100K AGI, no PSLF: RAP almost always wins on monthly cost and includes the only no-balance-growth guarantee in federal student loans.

- Over $100K AGI, no PSLF: IBR usually wins because of the 10-year Standard cap, and the 20-year forgiveness clock arrives a decade sooner.

- PSLF on the table: pick whichever IDR plan has the lower payment. RAP for sub-$100K, IBR for higher earners.

- Do nothing: auto-enrolled into Tiered Standard, payment roughly doubles, zero forgiveness clock.

Three things to do this week, even if your notice hasn't arrived yet:

- Log in to studentaid.gov and confirm your FSA ID still works.

- Pull your 2025 AGI and dependent count from your tax return.

- Run the Loan Simulator for RAP, IBR, and Standard so you know your number before the 90-day clock starts.

Ready to Fit the New Payment Into a Real Plan?

The RAP payment is just one line in your monthly budget. The bigger question is whether the rest of the plan — savings rate, debt order, investing — still makes sense once your loan starts back up.

Use MFFT's budget and net-worth tracker to model the new payment against your full picture. You'll see how the cash flow shifts, when your savings rate dips, and how long it takes for the RAP balance to actually start shrinking under the waiver and subsidy.

Pick your plan. File the form. Build the budget. Then keep moving.

Your future self will thank you for treating the 90-day notice as the deadline it actually is.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.