Quiet Burnout: The Hidden Cost to Your Savings ($5K-$15K/Yr)

TL;DR: 55% of U.S. workers experience quiet burnout — performing fine on the outside while collapsing inside — and a single year of it can cost $5K-$15K in direct costs and missed earnings growth. The bigger damage is the savings-rate collapse: dropping from a 25% to a 5% savings rate during a 2-3 year burnout destroys $76,000-$114,000 of future wealth. The 4-step recovery plan below stops the financial bleeding first, then rebuilds capacity, a visible timeline, and accountability.

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Start a Budget — the first step to financial freedom

- How to Build Wealth From Zero — the equation that explains why some people get rich and others don't

- The Complete Guide to FIRE — financial independence, explained

You're managing a demanding job. You're hitting your deadlines. Your manager praises your work. Your team relies on you.

But here's what they don't see: you're running on fumes.

The difference between this and "just being tired" is crucial. Quiet burnout is the exhausting act of appearing productive while experiencing profound emotional depletion. You're not consciously pulling back like you would with quiet quitting. You simply have no energy left.

And here's what makes this financial: burnout is destroying your savings rate.

I'm going to show you the real cost—we're talking $4,000 to $21,000 per year in lost productivity alone—and more importantly, the recovery framework that actually works.

The Quiet Burnout Crisis: More Than Just Feeling Tired

Let me be clear about what we're talking about here because there's been some confusion.

Quiet quitting is a conscious choice. You set boundaries. You decide "work is just work" and protect your personal time. It's actually healthy.

Quiet burnout is something else entirely. You're maintaining high performance while experiencing internal collapse. You hit every deadline. You respond to messages. Your productivity metrics look fine. But you're a shell of yourself.

According to research from the Maslach Burnout Inventory—the gold standard for measuring this—burnout has three core components: exhaustion, cynicism, and inefficacy. It's not just being tired. It's feeling hollowed out, disillusioned with work, and doubting your own ability to succeed.

Here's why 2026 is different: this phenomenon is spreading fast. 55% of U.S. workers now experience quiet burnout, and it's costing employers $438 billion globally in lost productivity.

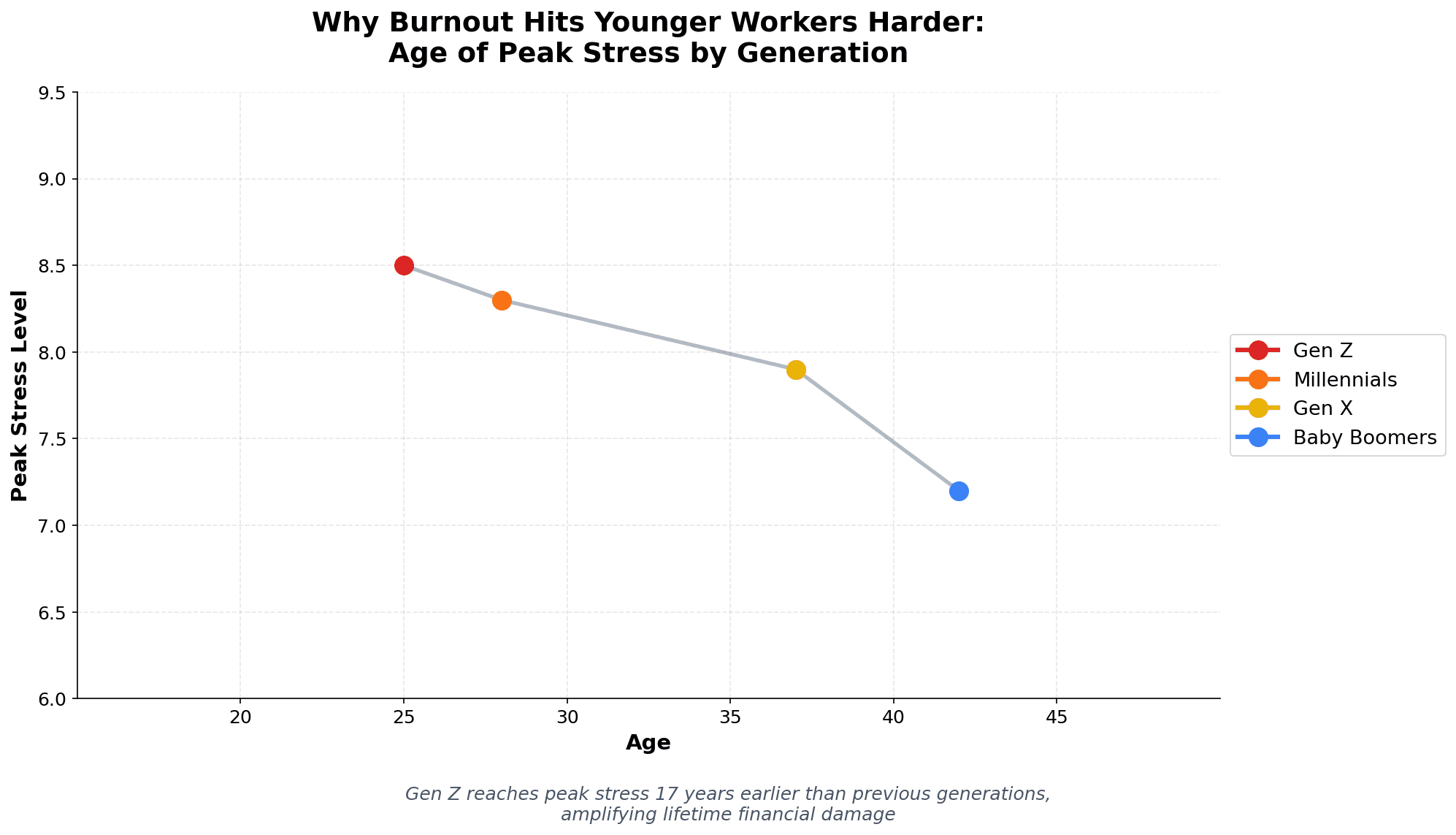

The worse part? It hits Gen Z and millennials earlier. Gen Z reaches peak stress at age 25 compared to age 42 for the general population. That's 17 years earlier—meaning the financial damage compounds over 40 years instead of 20.

What Burnout Costs You: The Real Numbers

Let me give you numbers that should make you sit down.

The American Journal of Preventive Medicine studied burnout costs at scale:

- Hourly non-manager: $3,999–$4,257 per year

- Salaried non-manager: $4,257–$5,000 per year

- Manager: $10,824 per year

- Executive: $20,683 per year

At a company with 1,000 employees, that's $5.04 million annually in direct costs.

But here's the kicker: 89% of those costs come from presenteeism, not absenteeism. You're showing up—just working at reduced capacity. Your boss doesn't see the crisis. Your metrics might even look good. But you're operating at maybe 60% of your actual potential.

That burnout employee staying late at the office? She's actually less productive than the one who leaves at 5pm and truly rests.

What does this mean for your personal finances? Healthcare costs rise 50% for workers with high stress. You take more sick days (burnout employees are 63% more likely to miss work). You miss promotions because you're not bringing full energy to the most important projects.

Let me translate that to your wallet: a single year of moderate burnout could cost you $5K-$15K in direct costs plus missed earnings growth and promotion delays.

The Savings Rate Collapse: How Burnout Derails FIRE

Here's where it gets personal.

Let me introduce Ethan, a mid-career professional earning $80,000 a year. Before his burnout, he had his finances dialed in:

Before burnout:

- Savings rate: 25% ($20,000/year)

- Trajectory: On track for FIRE by age 45

- Energy: Disciplined, motivated, making progress feel visible

Then quiet burnout hits. Ethan doesn't get fired. He doesn't quit. He just... stops feeling like himself.

During quiet burnout:

- Stress-driven spending spikes: takeout lunches (+$300/month), Amazon therapy shopping (+$200/month), weekend escapes for mental health (+$400/month)

- He skips his 401(k) contributions to "reduce financial pressure"

- New savings rate: 5% ($4,000/year)

- The math: He's now saving $16,000 less per year

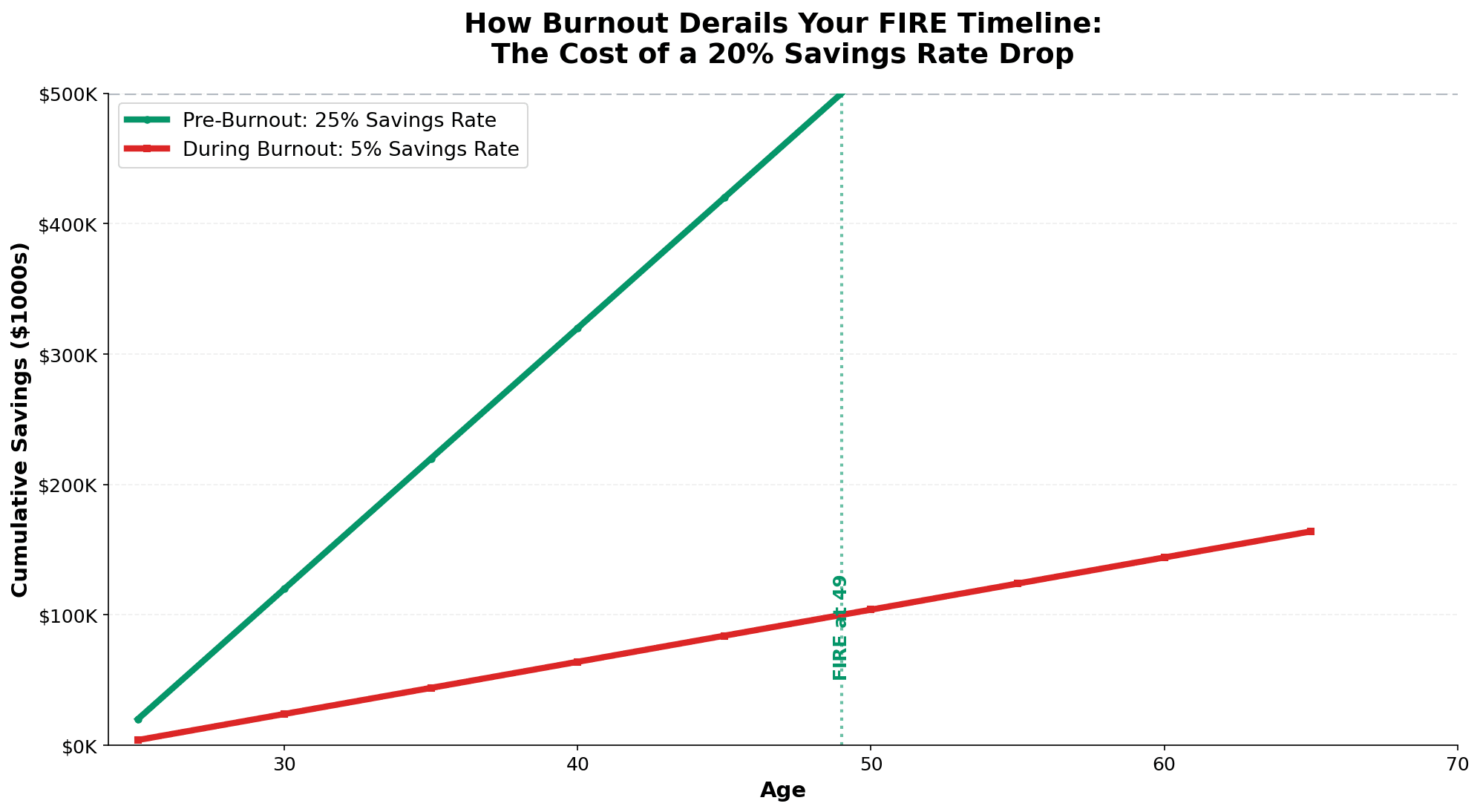

The 30-year cost: Skipping just one year of $5,000 in retirement contributions costs $38,000+ in lost retirement funds due to compound growth at 7% annual returns. One year!

But Ethan's situation usually lasts 2-3 years. That means he's losing $76,000-$114,000 in future wealth from a single burnout period.

This is why financial levels matter. Burnout pushes you backward through the levels. You move from building wealth to just surviving month-to-month.

The research shows this pattern across income levels. A $65K earner drops from 20% to 6%. A $120K earner drops from 30% to 8%. The psychological effect is identical: when you're burned out, saving discipline collapses.

Pay Inequality & the Trap: Why Quitting Isn't Simple

I hear this objection all the time: "If you're burned out, just find a new job."

If only it were that simple.

The real barrier is financial vulnerability. 24% of Americans have zero emergency savings. 47% can only cover a $1,000 emergency. When you're in that position, quitting feels impossibly risky—even if your job is destroying you.

There's also the discovery effect that makes it worse: pay inequality.

Meet Maya, a software engineer earning $110K. She discovers through job postings that peers in identical roles earn $130K-$140K externally. She's now aware she's being paid 15-20% below market rate.

When you're rested, this information might motivate you to negotiate or look elsewhere. When you're burned out? It deepens the "trapped" feeling. "I should leave, but I don't have the energy to interview. My company underpays me, but I can't afford to take the risk."

Research shows that discovering pay inequity while burned out intensifies burnout severity because it combines exhaustion with a sense of powerlessness. You're stuck and you know it.

34% of workers have actually accepted lower-paying jobs to protect their mental health—a real option, but one that most burned-out people don't feel they have.

The Stress Spending Trap: How Burnout Kills Your Budget

Let me explain the psychology here because this is crucial to understanding your own behavior.

When your cognitive capacity is depleted by burnout, your brain craves dopamine.

Stress spending is real. It's not weakness or greed. It's your nervous system trying to regulate itself through the easiest available method: shopping.

Burnout → Cognitive depletion → Impulse purchases → Temporary dopamine hit → Temporary relief → Next day: repeat.

Meanwhile, your morning coffee that you used to feel guilty about? Now it's a small comfort in an unbearable day. Your Friday takeout? Justified because you're too exhausted to cook. Your Amazon cart? It's emotional regulation, not consumerism.

The average person under stress increases discretionary spending by $300-600/month. Over a year, that's $3,600-$7,200 in additional expenses on top of the reduced income from missing career growth.

Compound this over a career: someone earning $80K who experiences 3 years of burnout-induced spending and saving losses is looking at $200K-$300K in lifetime wealth reduction.

And here's the part that creates a vicious cycle: financial stress amplifies burnout. 75% of workers say financial stress impacts their job motivation. When you're spending more and saving less due to burnout, you create financial anxiety that makes the burnout worse.

It's a feedback loop. Financial stress → burnout → stress spending → more financial stress → deeper burnout.

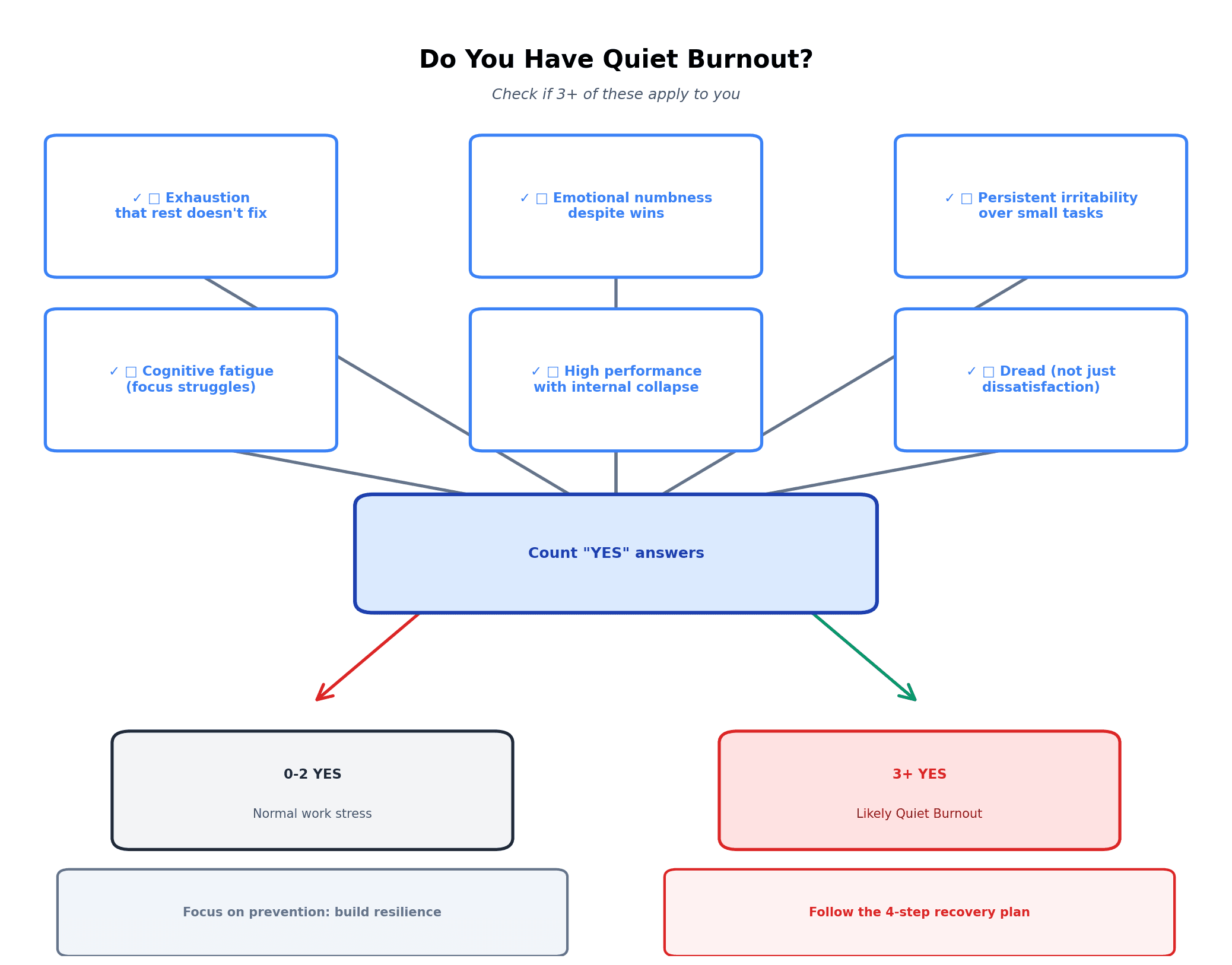

Diagnosis: Do You Actually Have Quiet Burnout?

Before we talk about recovery, let's make sure we're identifying the right thing.

You might have quiet burnout if:

- Exhaustion that doesn't improve with rest. You take the weekend off and Tuesday you're already exhausted again. Sleep doesn't help.

- Emotional numbness. You hit deadlines but feel hollow. Accomplishments that used to feel good now feel like "just what I'm supposed to do."

- Persistent irritability. Small tasks feel overwhelming. A simple email request triggers disproportionate frustration.

- Cognitive fatigue. You reread emails. You lose focus. You struggle to think clearly. Your brain feels like it's running through mud.

- High performance with internal collapse. Others praise your work while you're falling apart inside. This gap is key—the appearance of fine while being deeply not fine.

- Dread, not dissatisfaction. You're not consciously pulling back. You simply have no energy left.

If 3+ of these apply, you're likely experiencing quiet burnout, not normal work stress. That's important because the recovery path is different.

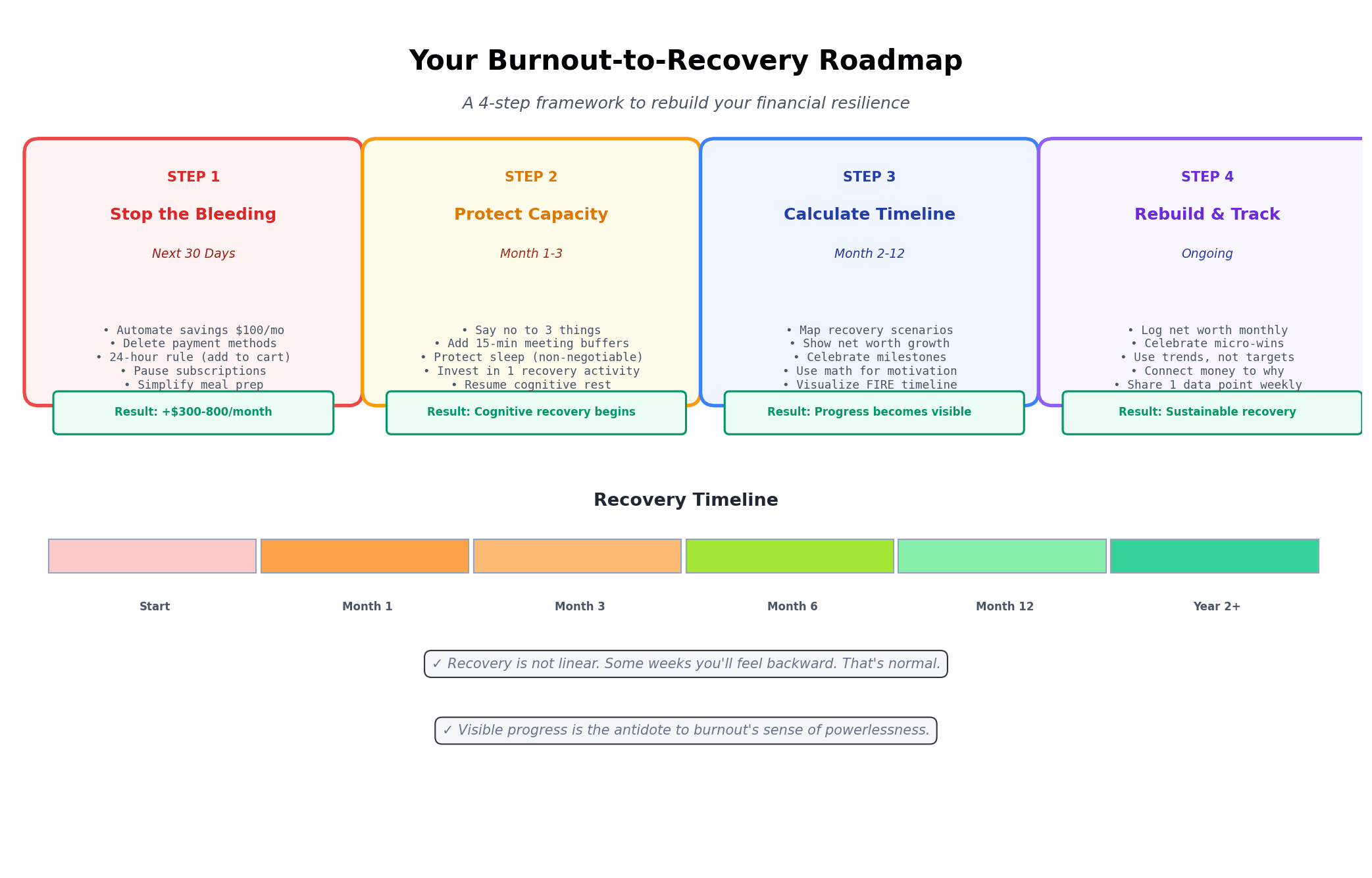

Your Burnout-to-Recovery Action Plan

Alright. If you recognize yourself in this, here's what actually works.

Step 1: Stop the Financial Bleeding (Next 30 Days)

Don't try to fix your savings rate yet. First, stop the hemorrhaging.

These aren't about willpower. They're about removing decision-making burden:

- Automate minimum savings before you see the money. Even $100/month. Set it and forget it.

- Delete saved payment methods from shopping apps. Create friction for impulse purchases.

- Implement a 24-hour rule: Add items to your cart, walk away, revisit tomorrow when cognitive energy is higher.

- Pause subscription reviews. Don't cancel anything yet. Just freeze new subscriptions for 3 months.

- Simplify meals: One weekly meal prep instead of daily takeout. Saves $400-600/month without decision fatigue.

- Track one spending category in a tool like MFFT. Often the visibility alone—"Oh wow, I spent $800 on food delivery this month?"—creates behavior change without shame.

These changes typically recover $300-800/month without requiring discipline. Just systems.

Step 2: Protect Your Remaining Capacity (The 80/20 of Recovery)

You can't optimize your way out of burnout with more systems. You need fewer decisions and more rest.

- Say no to 3 things. Work projects, social commitments, goals—free up 10 hours/week for actual recovery.

- Build 15-minute buffers between meetings. Your cognitive capacity needs recovery time.

- Protect sleep above all else. One extra hour of sleep > one extra hour of work. Sleep deficit amplifies burnout exponentially.

- Invest in one restorative thing. Therapy, coaching, a hobby you actually enjoy. Not a luxury. Essential maintenance.

Step 3: Calculate Your Recovery Timeline (Make It Visual)

Burnout destroys your sense of progress. Math rebuilds it.

Use this simple table and make it real with your own numbers:

| Scenario | Year 1 Savings | Year 5 Savings | Year 10 Savings | Age 65 Net Worth |

|---|---|---|---|---|

| Status quo (5% savings rate on $80K) | $4,000 | $20,000 | $40,000 | $500K |

| Recovery to 15% (realistic by year 3) | $12,000 | $60,000 | $120,000 | $1.2M |

| Back to 25% (your old rate) | $20,000 | $100,000 | $200,000 | $1.8M |

Frame it this way: "Getting back to 15% savings (not even my old 25%) unlocks $700K more by retirement."

Make it visible. Put it in a spreadsheet. Update it monthly. Progress is the antidote to burnout's sense of powerlessness.

Step 4: Rebuild Using MFFT Tools (Accountability Without Judgment)

This is where visibility matters most.

- Log net worth monthly (not weekly—monthly removes noise).

- Celebrate micro-wins. First month of positive cash flow? Recognize it.

- Use trends, not targets. Instead of "save $20K this year," track "move from 5% → 8% → 12% savings rate over 12 months."

- Connect money to your why. Link net worth tracking to time freedom, not just a number.

- Share one data point weekly. Tell one person "I recovered $200 in spending this month." External accountability shifts mindset.

Visible progress is powerful. It counters the helplessness that burnout creates.

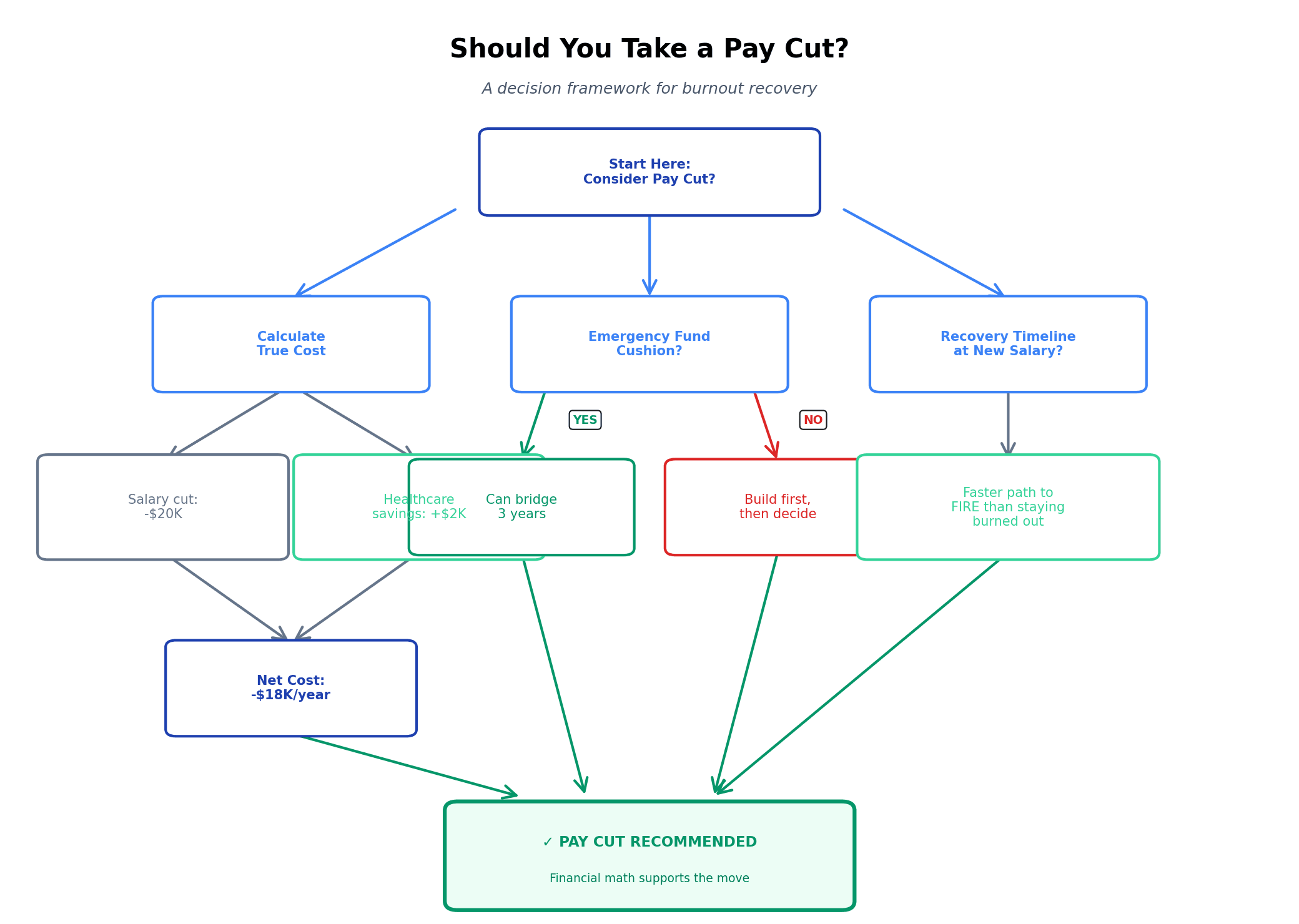

The Career Decision Framework: Should You Take a Pay Cut?

Let me address the hardest question: what if the job itself is the problem?

Some burned-out people consider a pay cut for mental health. Alex is considering leaving finance at $120K for a tech role at $100K.

Here's how to evaluate it:

-

Calculate true cost:

- Salary reduction: -$20K

- But stress-related healthcare costs drop from $2,500 to $500 = +$2,000 savings

- Net true cost: $18,000/year

-

Run a 3-year scenario:

- Can your emergency fund bridge the gap for 3 years?

- At lower burnout, savings rate recovers from 8% to 18% at new salary = $10,000 additional annual savings

- Break-even: The pay cut is absorbed within 2-3 years by improved financial discipline

-

Calculate opportunity cost:

- What's the recovery timeline for reaching FIRE at new salary vs. staying burned out longer?

- A 3-year lower-stress role might let you achieve in 12 more years what 15 years of burnout would prevent

Sometimes a pay cut IS the fastest path to financial independence if burnout is destroying your decision-making capacity.

Why Time Freedom Matters More Than Retirement

Here's a reframe that might help: financial independence isn't the goal. Time freedom is.

The research on FIRE regret shows that people who hit their number often feel purposeless. They optimized for "never work again" when what they actually wanted was "work on things that matter."

The antidote to burnout isn't more money. It's the ability to choose. The ability to say "this job isn't serving me" and actually have options.

Every percentage point of savings rate increase = 1% more negotiating power. Every $10K in net worth = 1% more agency.

Financial independence IS burnout insurance. When you own your time, burnout loses its grip because you have exit options.

This reframe changes how you think about recovery. You're not just "rebuilding your savings rate." You're building time sovereignty.

Build Financial Resilience BEFORE Burnout Hits

This is the ultimate prevention strategy.

Emergency fund: 6-12 months if you have unstable income or are high-earning (you have more to lose). 3-6 months for stable salary.

Flexible budget slack: Reserve 10% of income for discretionary spending. This gives you "permission" to stress-spend within limits, so burnout doesn't completely derail you.

Career optionality: Build skills, network, side projects that make you not dependent on your current job. This gives you power.

Boundary capacity: Only commit to 80% of what you could do. Reserve 20% for overflow and recovery.

Measurement: Track your net worth monthly. Each 1% increase = 1% more power to say "no."

The people who recover fastest from burnout are those who built resilience before it hit. They had the financial cushion to make choices. They had career options. They had boundaries.

You can build that now.

Why AI Workload Creep Is Making This Worse in 2026

One thing that's unique about 2026 burnout: AI is making people work harder, not easier.

This sounds backwards. AI productivity tools should reduce workload. But research from the Harvard Business Review shows something unexpected: workers using AI spend 27-346% more time on daily tasks. Focus hours dropped an additional 2% despite "productivity gains."

What's happening? Workload expectations expand. When AI makes your tasks faster, your manager adds more tasks. You voluntarily extend hours because tasks feel "easier." You take on broader projects.

The result: cognitive overload, burnout, poorer decision-making, and declining work quality.

It's the dark side of productivity tools. They enable more work, not less.

This is important for your financial plan because it means burnout is getting harder to avoid through willpower alone. You need structural solutions: firm boundaries, ruthless prioritization, and possibly role changes.

Conclusion: Recovery Is Measurable

Quiet burnout hits suddenly but recovery is slow. That's not weakness. That's the nature of chronic stress depletion.

But here's what matters: recovery is measurable.

You can track your savings rate month to month. You can see your net worth rebuild. You can count the months until your stress markers improve. You can calculate your actual timeline to freedom.

The people who recover successfully are those who:

- Stopped pretending they were fine and diagnosed the actual problem

- Focused on systems instead of willpower (automate savings, remove temptation)

- Made progress visible through tools and monthly tracking

- Redefined the goal from "work forever" to "own my time"

- Took action on career/role changes when needed, using math to evaluate the tradeoff

Burnout won't disappear tomorrow. But your financial recovery can start this week.

Open a tracking tool. Set your minimum savings amount. Tell someone what you're doing. Make the first month visible.

That's how recovery starts.

Have questions about tracking your recovery? My Financial Freedom Tracker is built exactly for this—to show your net worth progress in real-time and help you see the light at the end of the tunnel when burnout makes everything feel hopeless.

Email me at dennis.vymer@myfinancialfreedomtracker.com if you want to talk about your specific situation.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.