The Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

It's the last day of the month. You open your budget, scroll the damage, and there it is: four weekends of double-ordered delivery, a "free trial" that started charging two weeks ago, $200 of stuff you half-remember buying. And here's the cruel part — the money is already gone. Your monthly budget didn't fail to find the problem; it found it too late to act. That single, fixable flaw is why weekend budgeting is quietly winning in 2026.

Also called the Sunday Money Reset, it swaps the once-a-month autopsy for a tiny 15-minute weekly check-in. The #SundayReset hashtag has racked up hundreds of millions of views on TikTok — it started as a cleaning-and-self-care ritual, but a growing slice of it is now about money. The thesis is simple and, I think, correct: life happens weekly, not monthly, so a 30-day feedback loop is too slow to catch overspending before it compounds.

Why Your Monthly Budget Keeps Failing (and Weekend Budgeting Doesn't)

Start with a number that should make every budget app nervous: only about 29% of Americans reviewed their budget in the last 30 days. More than two-thirds didn't look at all. We make budgets — then never reopen them.

There's a reason for that, and it isn't laziness — it's design. A monthly budget asks you to predict an entire month of behavior in advance, then checks the result only after the month is dead. As Money Fit puts it, "thirty days is simply too long to accurately predict human behavior." One bad weekend blows the plan, and you won't know until the page turns.

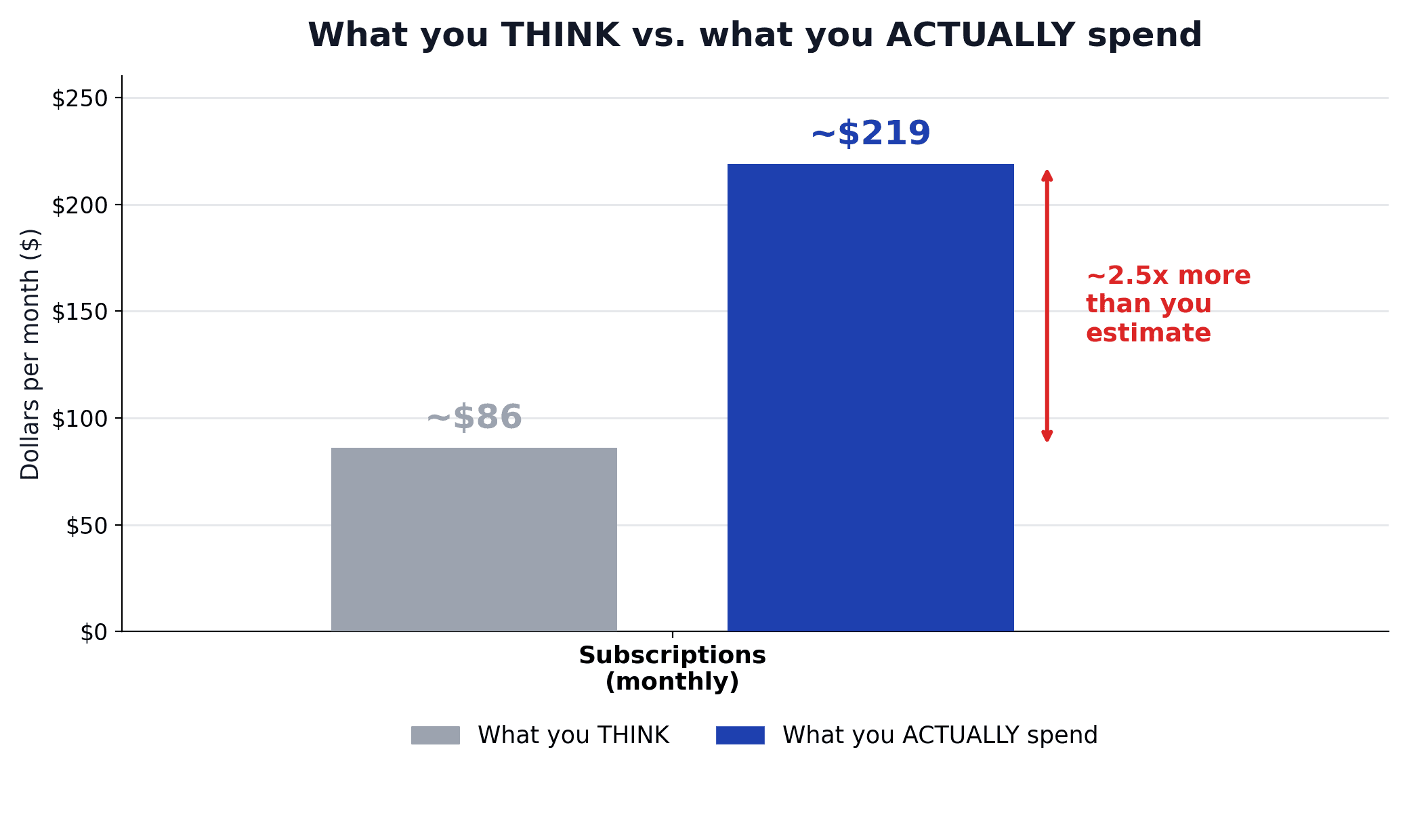

The second problem is a perception gap. The average American badly underestimates their own spending. Take subscriptions: people guess they spend about $86 a month; the real average is $219 — more than 2.5x what they think (C+R Research). A rushed review on the 31st doesn't surface that gap in time to fix it.

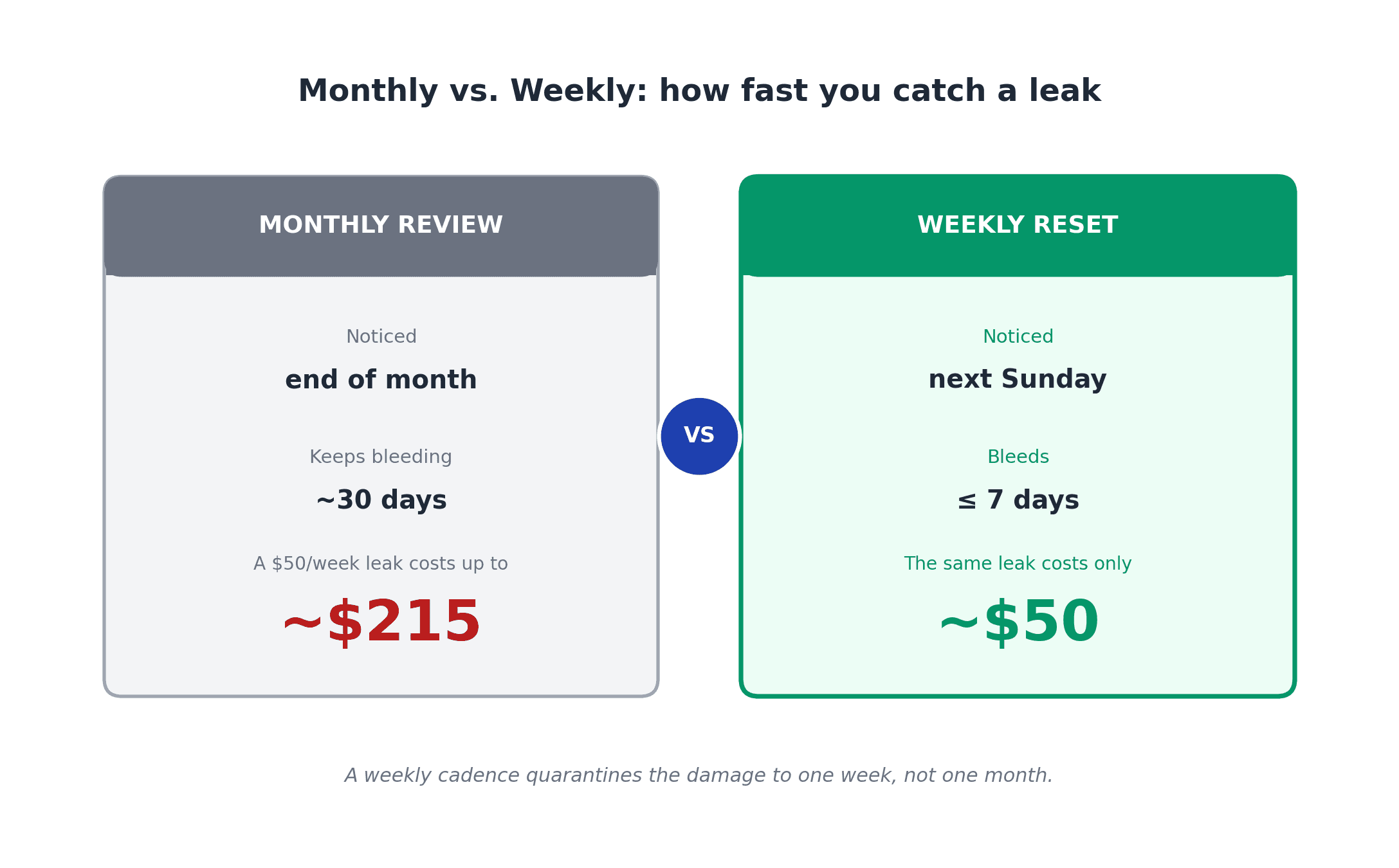

A weekly cadence doesn't make you more disciplined — it makes failure smaller. An overspend on Friday needs a few days of course-correction, not the rest of the month.

And the deepest reason budgets fail is behavioral, not mathematical. As Ramit Sethi argues, a budget runs on willpower — and willpower is a limited resource you're asked to spend "every day, forever." That's a brutal ask. Decision fatigue and all-or-nothing thinking (one slip and "I've blown it") do the rest.

If you don't yet have a budget to review on a Sunday, start one first — my 3-method budgeting walkthrough gives you the framework in an afternoon. The reset is how you keep a budget alive, not a substitute for having one.

What Is Weekend Budgeting? The 15-Minute Sunday Reset, Explained

So what is it? Weekend budgeting means setting aside a short block every weekend — most people pick Sunday — to review the week's spending, catch leaks, and set one simple number for the week ahead. That's it. No 40-line spreadsheet, no tracking every coffee. A glance, a flag, a plan.

The genius is in the timing. Sunday sits between spending cycles — right after the heavy-spend weekend, just before the new workweek. A 15-minute check-in catches overspending before a monthly review would, when the month is already over — fresh data while you can still act on it.

Here it is against its neighbors:

| Cadence | What you check | The trap it avoids |

|---|---|---|

| Daily tracking | Every transaction | Decision fatigue, anxious over-checking |

| Weekly reset | Last week's spend + next week's number | The "too slow to act" lag |

| Monthly / quarterly | Bills, net worth, the big picture | Over-reacting to weekly noise |

Weekly is the Goldilocks zone for cash flow — frequent enough to catch a leak while it's small, but not so often you're refreshing your bank app forty times a day.

There's an emotional payoff, too. About 66% of working professionals report the "Sunday Scaries" — that end-of-weekend dread — and money is one of the things that surfaces on Sunday evenings. The reset reframes that dread into something you control: one coffee, one 15-minute look, then permission to not think about money the other six days — a background hum of worry turned into a scheduled appointment you run.

It's one of several 2026 budgeting movements. Where the Sunday reset is about cadence and feedback, its sibling trend loud budgeting is about social accountability — saying "no, that's not in my budget" out loud. They pair well: loud budgeting handles the in-the-moment "no," the Sunday reset handles the weekly "where did it go?"

The Behavioral Science: Why Short Weekly Loops Beat the Perfect Monthly Plan

Here's the part most trend pieces skip: why does frequency beat precision? The answer is behavioral science, and it's well-established.

Start with the feedback loop: the longer the gap between an action and its consequence, the weaker the learning. A monthly review tells you on day 31 that you overspent on day 3 — four more weeks of the habit already baked in. A weekly review closes that loop to seven days, while the choice is fresh enough to connect cause and effect.

Then there's present bias — overvaluing the reward in front of you and undervaluing the future one, a documented driver of lower savings and higher debt. A short, frequent check-in keeps the future close enough to compete with now.

Your net worth is a lagging measure of your financial habits. The weekly inputs matter far more than the monthly number — which is exactly why you review them more often.

The habit research seals it. Habits form through repetition: in the famous Lally study, a once-daily action took a median of 66 days to become automatic — though it ranged from 18 to 254 depending on the person and the habit. Repetition is the lever, and a weekly ritual stacks up reps four times faster than a monthly one ever will.

My favorite evidence is from UCLA's Hershfield, Shu, and Benartzi: framing savings in smaller, more frequent units — "$5 a day" instead of "$150 a month" — more than quadrupled enrollment in a savings program. Same money, different cadence, four times the action — the whole Sunday-reset philosophy in one experiment: small and frequent beats big and rare.

Finally, James Clear's habit stacking makes it stick: "After I [current habit], I will [new habit]." Anchor the reset to something you already do every Sunday — coffee, meal prep, laundry — and it stops relying on willpower. "After my Sunday coffee, I do my money reset" survives a busy week. A standalone good intention does not.

The Exact 6-Step Sunday Reset Checklist (Copy This)

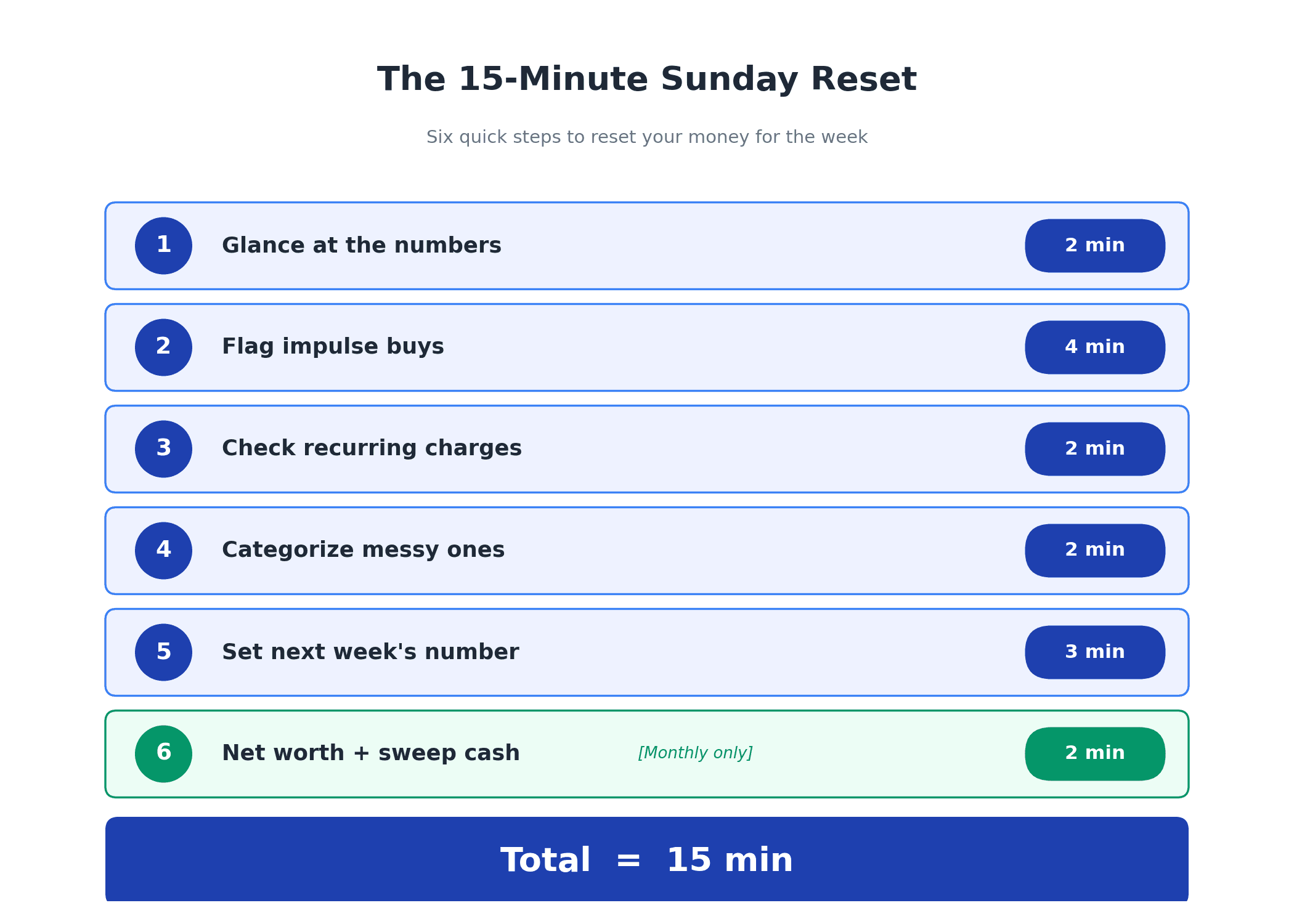

Enough theory. Here's the actual ritual, built to fit inside 15 minutes. The minute counts matter — they keep this from ballooning into a two-hour guilt session, the number-one way the habit dies.

1. Glance at the numbers (2 min). Open your bank or budget app and look at one thing: total in versus total out since last Sunday. No deep dive — just the topline. Up or down on the week?

2. Skim last week's transactions and flag impulse buys (4 min). Eyeball the list and star anything unplanned — the delivery order, the "add to cart" impulse, the duplicate. You don't have to act on them; awareness alone curbs the repeat, since impulse buys are emotion-driven and quickly regretted. (The average American makes around 10 impulse purchases a month — roughly $254 worth, about $26 a pop.)

3. Check recurring charges for creep (2 min). Scan for any subscription or auto-renewal that hit this week and cancel the zombies on the spot. This is where the ~$204 a year ($17 a month) in unused subscriptions goes to die — nearly 60% of subscribers have at least one they haven't touched in the past month. Run a full subscription creep audit once and the weekly scan becomes a 30-second glance after that.

4. Categorize the messy ones (2 min). Drop any "uncategorized" transactions into the right bucket so next week's glance starts clean. Broad buckets only — "food," not "Tuesday lunch with Dave." You want a quick map, not a forensic ledger.

5. Set ONE number for the coming week (3 min). Decide your discretionary or "fun money" ceiling for the next seven days — one number is far stickier than a twelve-line spreadsheet. Glance at which bills land this week so nothing ambushes you.

6. (Monthly, not weekly) Update net worth and move cash (2 min). On the first Sunday of the month only, log your net worth and sweep any leak-savings toward your top priority — emergency fund first, then debt or investing.

Notice that net worth is monthly, not weekly — deliberate, and we'll come back to why. The rule to remember: spending is a weekly check; net worth is a monthly one.

The Math: What Catching Small Leaks Weekly Does to Your Savings Rate

Now for the part that turned me from a casual fan into a true believer. Meet Michelle.

Michelle isn't a big spender. On her first few resets she found the same boring leak most of us have: a little delivery, an impulse buy, one forgotten subscription — about $50 a week that wasn't buying her any real happiness. A monthly review had let it slide for years because she only looked at the total. The weekly glance caught it in week one.

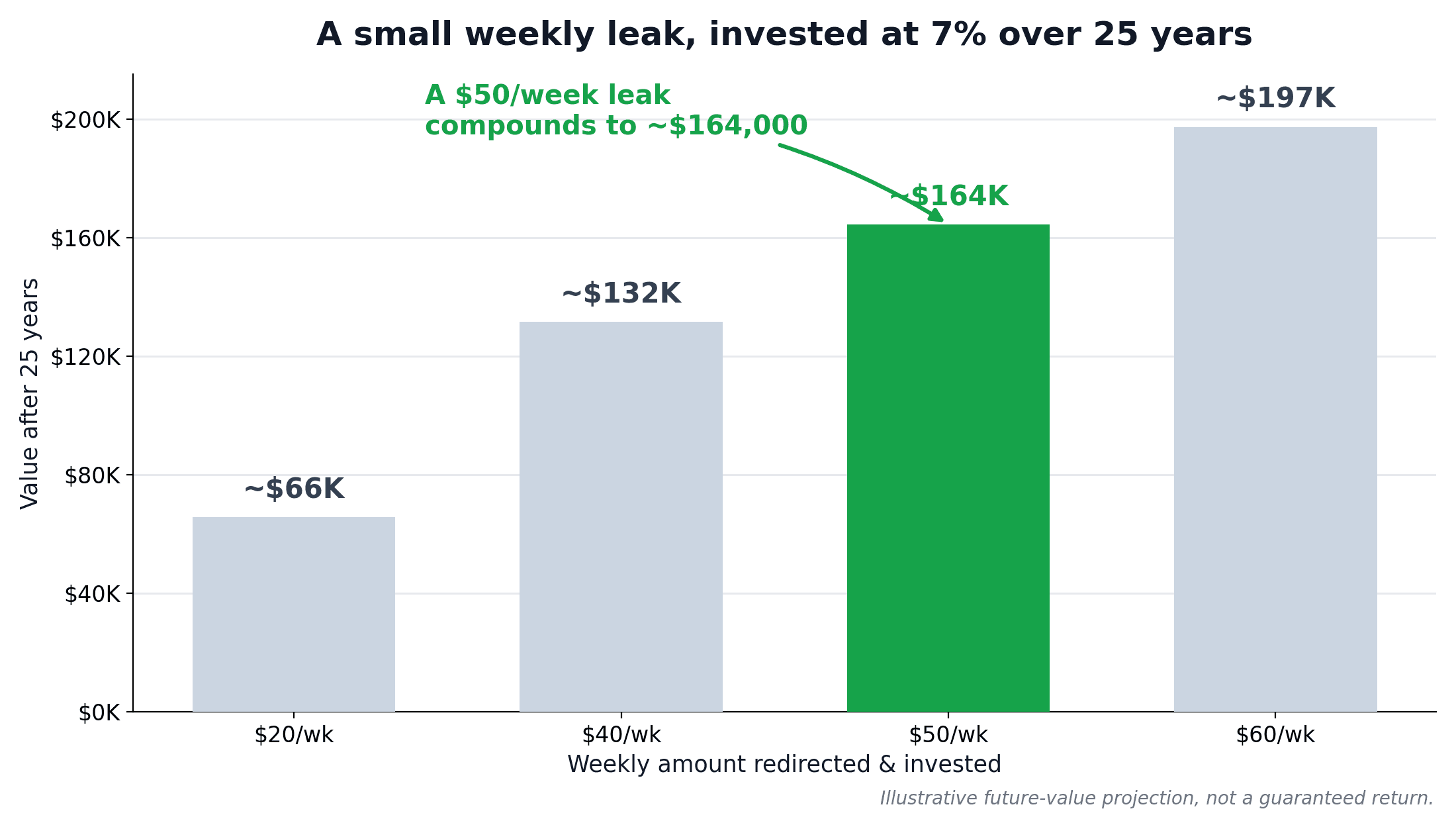

Stopping that $50-a-week leak frees up about $2,600 a year. Redirected into investments at a 7% return, here's what it becomes — illustrative math, not a guaranteed return:

| Weekly leak plugged | Per year | Invested 10 yrs (7%) | Invested 25 yrs (7%) |

|---|---|---|---|

| $20/wk | $1,040 | ~$14,400 | ~$66,000 |

| $40/wk | $2,080 | ~$28,700 | ~$132,000 |

| $50/wk | $2,600 | ~$35,900 | ~$164,000 |

| $60/wk | $3,120 | ~$43,100 | ~$197,000 |

Michelle's quiet $50-a-week leak is a $164,000 decision over 25 years. She didn't earn a raise or "try harder" — she looked weekly and caught what a monthly review let bleed.

And where that cash goes matters. The biggest lever on reaching financial independence isn't your income or your investment picks — it's your savings rate:

| Savings rate | Approx. working years to financial independence |

|---|---|

| 10% | ~51 years |

| 25% | ~32 years |

| 40% | ~22 years |

| 50% | ~17 years |

Plugging weekly leaks nudges your savings rate up without earning a cent more. And before that money goes anywhere clever, send it somewhere safe: if your cash cushion isn't solid yet, route those weekly wins into your emergency fund before you invest the difference — a plugged leak is worthless if the next surprise puts it back on a credit card.

That's the quiet superpower of weekend budgeting: a 15-minute habit becomes a savings-rate machine — and your savings rate becomes years of your life back.

Weekend Budgeting Without the Spreadsheet: Turning It Into a 5-Minute Habit

The honest risk with any weekly ritual: if it stays manual, it feels like a chore, and chores get skipped. So automate the boring parts and the human part shrinks toward five minutes.

Put three things on autopilot. Auto-categorization so step 4 nearly does itself. Auto-savings transfers right after payday — in behavioral experiments, people who automate save roughly twice as much as those moving money by hand, because a scheduled transfer never gets tired or talks itself out of it. And auto-bill-pay so no due date ambushes your weekly number.

What's left for the human is what a machine can't do: the judgment calls. Was that delivery order worth it? Is this subscription still earning its keep? What's next week's number? Those are the five minutes worth protecting.

A tracker makes this realistic, and you don't need to hand over your bank login to get it — I rounded up the privacy-first trackers that don't link to your bank for exactly this use case. The split to aim for: glance at spending weekly, check net worth monthly. Most experts agree quarterly is enough for the big number, monthly the practical minimum — weekly net-worth checking just invites market-noise anxiety. A good tool auto-updates that snapshot so it's a two-minute look.

Common Mistakes That Make the Sunday Reset Backfire

Weekend budgeting is simple, which is why it's easy to do wrong. Here are the failure modes I see most, with the fix for each.

Turning it into a two-hour guilt session. The big one. If your reset becomes a post-mortem on every regret, you'll quit within a month. Keep it short, factual, and forward-looking — the goal is next week's number, not a trial of last week's.

Over-monitoring until it becomes anxiety. A scheduled weekly check is healthy; refreshing your balance many times a day is a symptom of financial anxiety, not diligence. The reset should replace the anxious refreshing, not add to it — therapists put it plainly: check once or twice a week, then step back.

Obsessing over net worth weekly. Your net worth bounces with the market; staring at it every Sunday feeds anxiety and tempts you to tinker with investments you should leave alone. Spending is the weekly metric; net worth is the monthly one.

How to Start This Sunday: Your First 4 Weeks

You don't need all six steps on day one. The fastest way to make this stick is to start embarrassingly small and build:

Week 1 — Just look (10 minutes). Open your accounts and read last week's transactions. No categorizing, no judgment, no plan. The only job is to look without flinching. For a lot of people that's the genuinely hard part — and the most important to normalize.

Week 2 — Add the flag (12 minutes). Add step 2: star the impulse buys and unplanned spend. Still no plan — you're just building awareness, which curbs repeat purchases on its own.

Week 3 — Add the number (14 minutes). Add step 5: set one discretionary number for the coming week. This is where the reset stops being a review and starts steering the week.

Week 4 — Run the full reset (15 minutes). Add recurring-charge scanning, quick categorizing, and the net-worth glance on the first Sunday of the month. Habit-stack it onto your Sunday coffee and you've got a ritual that runs itself.

From there, pair it with the rest of your plan: the reset feeds your sinking funds (small monthly amounts set aside for irregular costs), your emergency fund gets first claim on every leak you plug, and your investing runs automatically — reviewed quarterly, not weekly.

That's the whole system. Weekend budgeting doesn't ask you to be more disciplined or build a perfect spreadsheet you'll abandon by March. It asks for 15 honest minutes on a Sunday — a glance, a flag, and a number — repeated often enough to become invisible. A short weekly loop beats a perfect monthly plan you never reopen, because consistency and fast feedback change behavior in a way precision never will.

So this Sunday, after your coffee, give it ten minutes. Just look. The leak you catch in week one instead of week four might be the most profitable cup of coffee you ever sit with.

If you want the boring parts handled so your reset stays a 5-minute habit, track your spending, net worth, and savings rate with MFFT — no bank linking, no upsell. And if your first Sunday reset turns up a leak that surprises you, email me at vymerd@gmail.com and tell me what it was. Mine, the first time, was $38 a month in streaming I'd forgotten I had.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyRent vs Buy in 2026: I Ran the Numbers, Kept Renting, and Invested the Difference

My uncle swears renting is throwing money away. So I built the rent vs buy 2026 model: renting wins in all 50 metros, but only if you invest the difference.

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.