Is AI Taking Your Job? A 5-Step Income Protection Plan

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Start a Budget — the foundation of money management

- How to Build Wealth From Zero — the equation that explains why some people build security and others don't

- The Complete Guide to FIRE — financial independence, explained

You're in a meeting. Your company just rolled out enterprise AI tools. Your manager mentions "efficiency gains" and "productivity enhancements."

Everyone nods.

But you're thinking: Is my job next?

You're not paranoid. You're paying attention to something real.

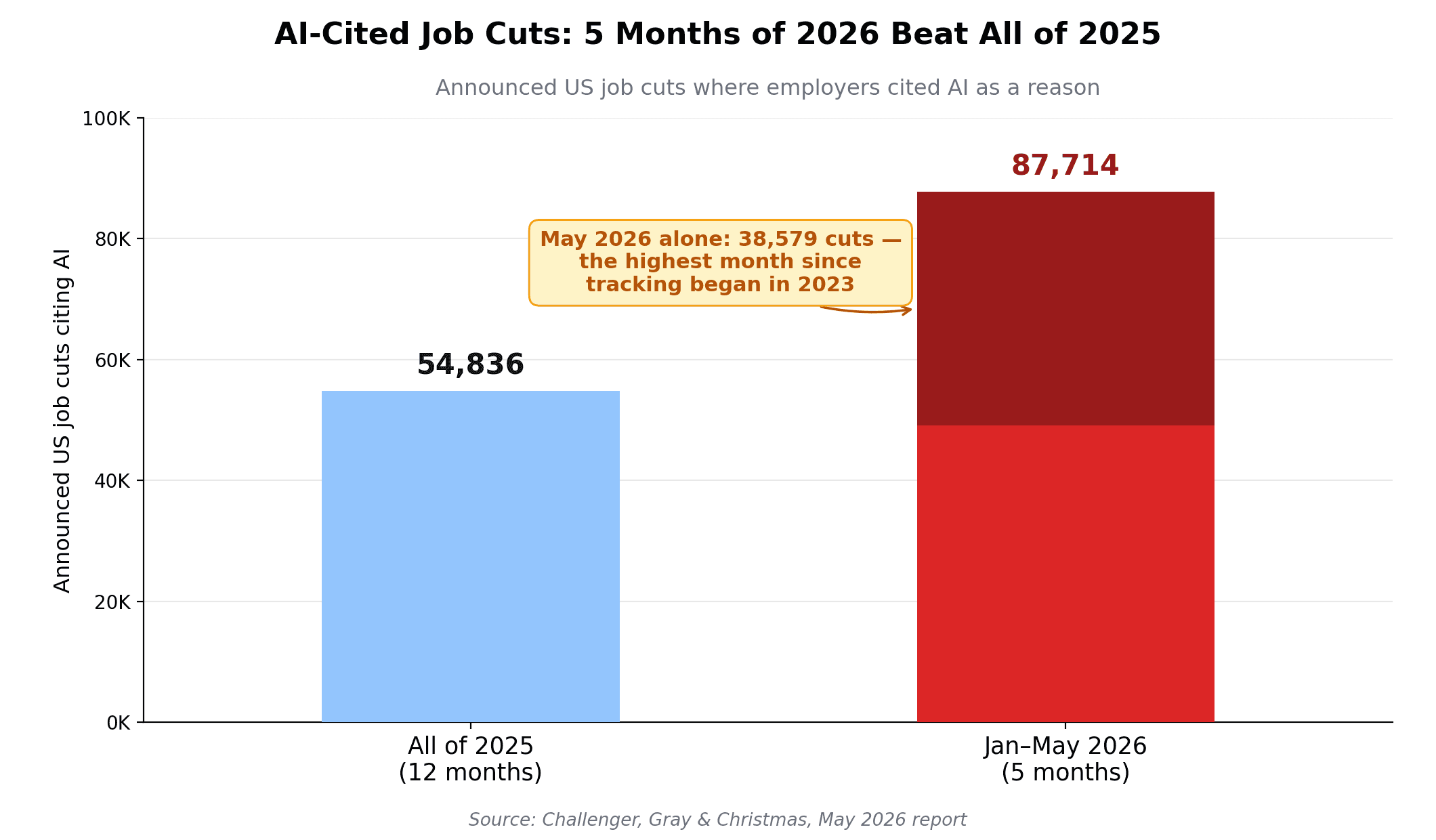

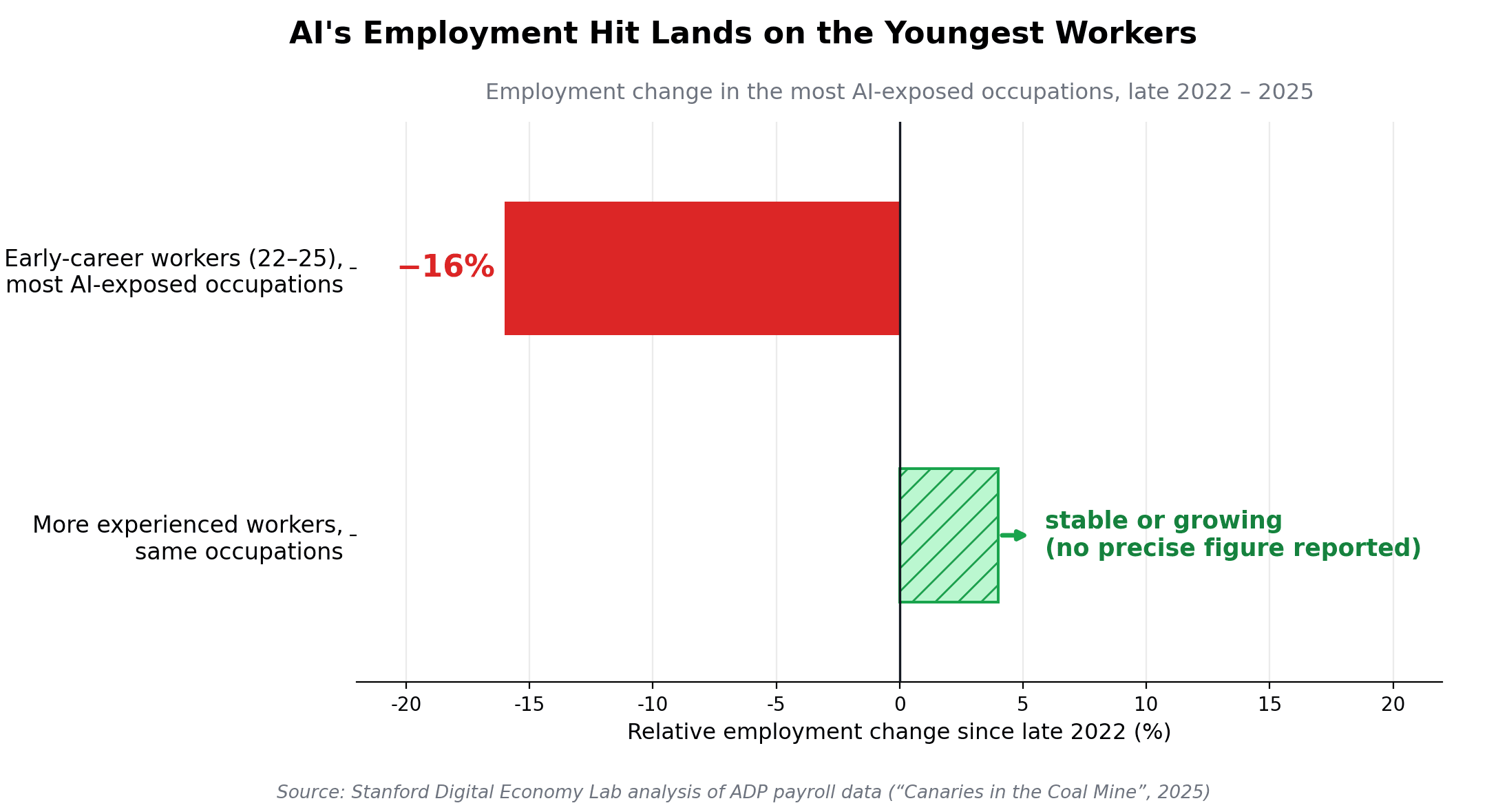

In the first five months of 2026, US employers cited AI in 87,714 announced job cuts — 22% of all layoffs — including a record 38,579 in May alone, per Challenger, Gray & Christmas. And here's the part that should worry you: early-career workers aged 22–25 in the most AI-exposed occupations have seen a 16% relative decline in employment since late 2022, while employment for more experienced workers in the same fields has stayed stable or kept growing — that's the headline finding of the Stanford Digital Economy Lab's analysis of ADP payroll data.

This isn't the optimistic "AI will create new jobs" narrative. This is the timing crisis: new jobs might exist in 10 years, but your career is happening now.

This article is going to show you exactly which jobs are at highest risk, why experience actually protects you (and why youth doesn't), and a 5-step income protection strategy that works whether your job gets automated or not.

The AI Job Apocalypse That Isn't (But Actually Is)

Let me start with the headline that confuses everyone.

The World Economic Forum's Future of Jobs Report 2020 projected 85 million jobs displaced by 2025 — but 97 million new ones created. Net positive.

The updated Future of Jobs Report 2025 projects 92 million jobs displaced and 170 million created by 2030. Also net positive.

So why are people panicking?

Because the headline masks the real crisis: timing, age, and skill mismatch.

The jobs being destroyed now are entry-level, codifiable roles. The jobs being created later require skills you don't have yet. For someone aged 22 trying to launch a career, "wait 10 years for the market to rebalance" isn't a strategy. That's a decade of missed earnings and compound growth.

Here's what the data actually says:

Challenger, Gray & Christmas (May 2026): AI has been cited in 87,714 announced US job cuts in 2026 through May — 22% of all layoff announcements. For all of 2025 the figure was 54,836, just 5% of cuts. In May 2026 alone, employers attributed 38,579 cuts to AI — the highest monthly total since tracking began in 2023, and the third straight month AI led all stated reasons for layoffs.

That's not zero displacement. That's an accelerating, measurable subtraction from specific corners of the US job market.

McKinsey: the McKinsey Global Institute estimates that current generative AI and other technologies could automate work activities that absorb 60–70% of employees' time today. But actual adoption runs years behind technical potential because of legal, regulatory, and organizational friction. The gap between "could" and "will" is measured in years, not months. That gap is closing.

The real problem isn't net job loss long-term. The real problem is you can't wait for the long term when your mortgage is due next month.

The Quiet Crisis: Young Workers Are Losing Ground

Here's where the data gets personal.

Stanford Digital Economy Lab (Brynjolfsson, Chandar & Chen): using payroll records from ADP — the largest payroll provider in the US — the researchers found that among early-career workers aged 22–25 in the most AI-exposed occupations, employment saw a 16% relative decline since late 2022. Meanwhile, employment for more experienced workers in the same occupations, and for workers in less-exposed fields, remained stable or continued to grow.

That's not a mild shift. That's a generational cliff. The study's title says it plainly: young workers are the "canaries in the coal mine."

And critically, the declines aren't mostly layoffs — the adjustment shows up in hiring. Entry-level positions quietly stop being posted.

Let me translate what's happening in plain English:

The learning curve is being erased.

Traditionally, a junior programmer spends 3–5 years learning through routine tasks: writing basic code, debugging, reviewing APIs. That experience becomes tacit knowledge—judgment about system design, risk management, performance tradeoffs.

But AI can now do those routine tasks. So companies don't need juniors anymore. They need seniors who can use AI to work 2x faster.

The career ladder is being pulled up before young workers can climb it.

Which Jobs Are at Highest Risk Right Now

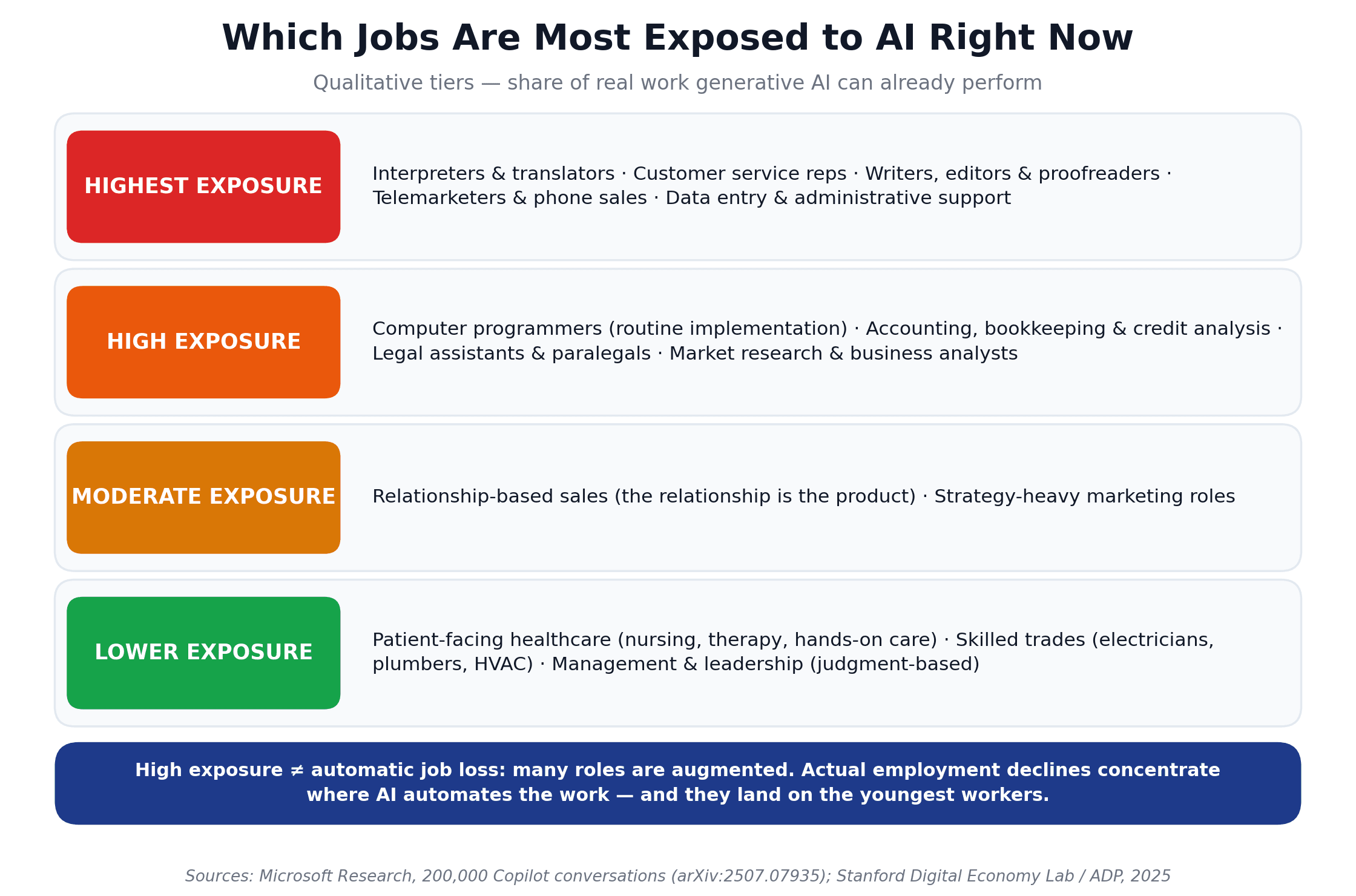

Not every job is equally vulnerable. The best occupation-level evidence we have comes from Microsoft Research's 2025 study of 200,000 real Copilot conversations, which scored occupations by how much of their actual work generative AI can already perform, and from the Stanford/ADP employment data on where jobs are actually disappearing:

Highest exposure (AI can already do much of the core work):

- Interpreters and translators

- Customer service representatives

- Writers, editors, and proofreaders

- Telemarketers and telephone-based sales

- Data entry and administrative/clerical support

High exposure:

- Computer programmers (routine implementation work)

- Accounting, bookkeeping, and credit analysis

- Legal assistants and paralegals

- Market research and business analysts

Moderate exposure:

- Relationship-based sales (the human relationship is the product)

- Marketing roles with heavy strategy components

Lower exposure:

- Patient-facing healthcare (nursing, therapy, hands-on care)

- Skilled trades (electricians, plumbers, HVAC)

- Management and leadership (judgment-based)

One important caveat from the Microsoft researchers themselves: high AI applicability does not automatically mean job elimination — many of these roles are being augmented rather than replaced. The Stanford data adds the sharper warning: actual employment declines so far are concentrated in occupations where AI automates the work rather than augments it — and they land on the youngest workers.

Here's what matters about this list: the high-risk roles are exactly where young workers are trying to start their careers. Programming, accounting, customer service, administrative roles—these are entry-level hiring grounds.

The roles that are safer—management, trades, healthcare—require either years of experience or specific training most people don't have going in.

The Experience Paradox: Why Seniority Actually Protects You

This is the part that surprised even the researchers.

AI is augmenting experienced workers while replacing junior workers.

The Stanford/ADP data shows employment holding up — even growing — for experienced workers in the very same AI-exposed occupations where 22–25-year-olds are losing ground. A senior programmer with 12 years of experience is worth more to employers using AI, not less.

Here's why:

Tacit knowledge can't be automated. Tacit knowledge is what you learn by doing—judgment calls about edge cases, understanding what "good" looks like in ambiguous situations, knowing when to break the rules. This takes years to acquire.

AI is fantastic at routine, codifiable tasks (the things junior workers do). AI is terrible at decisions under uncertainty, vendor negotiations, strategic positioning, team dynamics—the things senior workers do.

When a senior programmer uses AI to write boilerplate code, they're 2x faster at the routine parts. But their judgment—which AI can't replicate—becomes even more valuable.

The wage data confirms the value of AI skills:

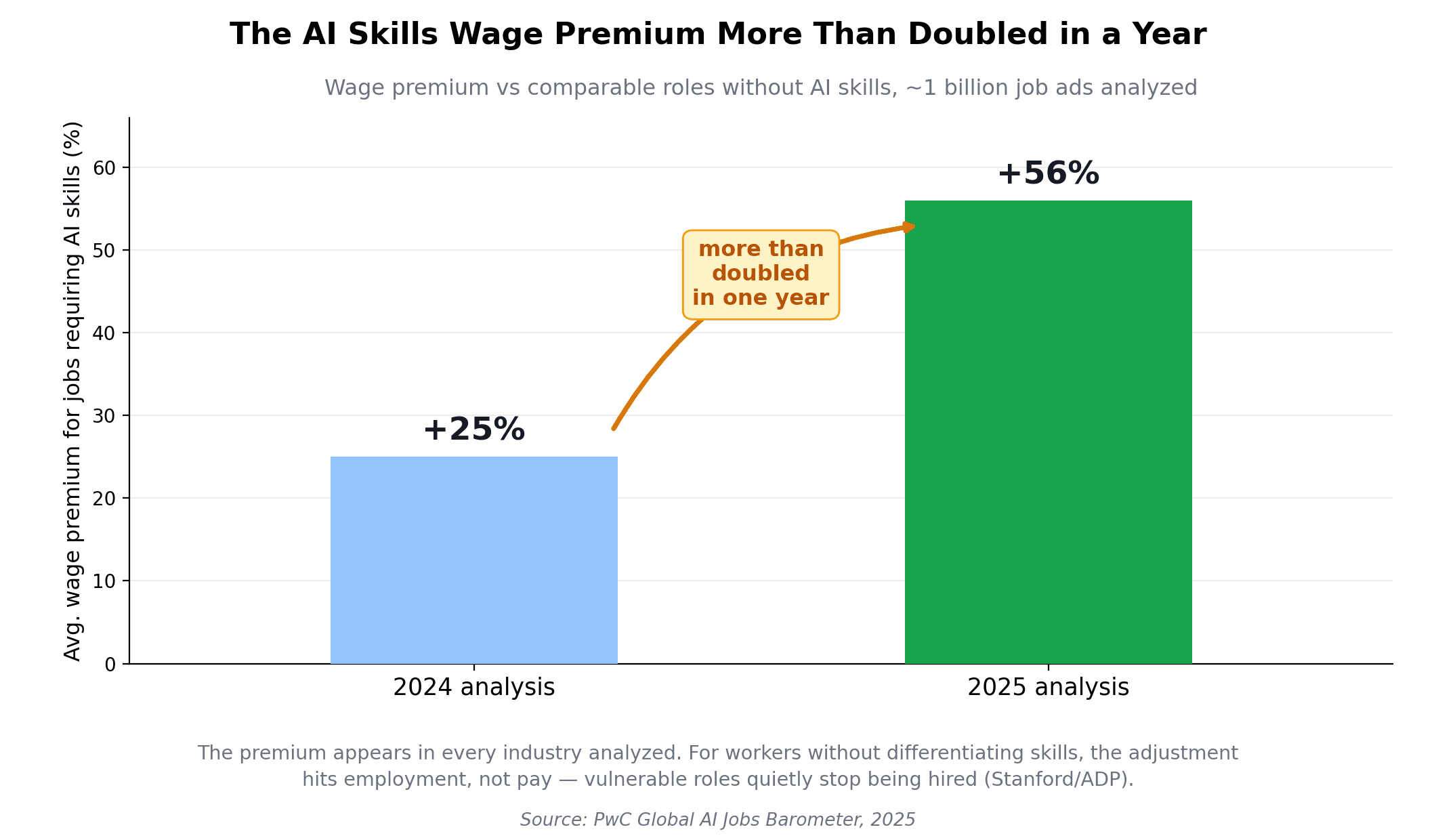

- PwC's 2025 Global AI Jobs Barometer, built on analysis of nearly a billion job ads, found that jobs requiring AI skills pay an average 56% wage premium over comparable roles that don't — up from 25% just a year earlier

- That premium shows up in every industry analyzed, and the skills employers demand are changing 66% faster in the most AI-exposed occupations

- For workers without differentiating skills, the Stanford/ADP research found the labor-market adjustment happens through employment, not pay — vulnerable roles don't get a wage cut, they quietly stop being hired for

In plain language: if you're experienced or AI-skilled, AI makes you worth more. If you're just starting with neither, it makes your job disappear from the listings.

Who Actually Benefits From AI (Spoiler: Not Struggling Entry-Level Workers)

The winners in the AI economy are:

1. Experienced workers with tacit knowledge

You spent 10+ years learning judgment. AI can't do that. You're now 2x more productive. Your job security increased.

2. Workers who develop AI literacy fast

If you can operate AI tools, prompt them effectively, and interpret results critically, you're competing for the roles that PwC found pay an average 56% wage premium. But this requires existing competency in your field—you can't jump straight to "AI prompt engineer" without domain expertise.

3. People in relationship-based or leadership roles

Sales, management, complex negotiations, client relationships—these are human-dominated. AI is a tool, not a replacement.

4. Specialized trades

Electricians, plumbers, HVAC technicians, carpenters. These require hands-on judgment and customization. Low AI exposure.

The losers?

1. Entry-level knowledge workers

Junior programmers, junior accountants, junior analysts, customer service reps, data entry keyers. Your codifiable work is exactly what AI does best.

2. Young workers who can't access senior roles

If you can't get hired because companies stopped hiring juniors, you can't accumulate the experience that would make you valuable later. This creates a permanent gap in your trajectory.

3. Workers in geographic or economic regions with limited alternative jobs

If your town has 5 accountants and AI just made 2 of them redundant, you're not moving to Silicon Valley for an AI specialist role. You're stuck competing for fewer jobs.

The Retraining Trap: Why It's Harder Than It Sounds

Everyone says: "Just retrain in AI skills."

Here's the problem: retraining takes 6–24 months, and companies need workers now.

Meet Jordan, a 27-year-old accountant making $65,000 a year. His firm just deployed AI-powered tax software. His billable hours dropped 30%. His firm isn't laying him off—not yet—but his path to partnership is gone.

Jordan considers retraining as a data analyst (potential $90K role). A bootcamp takes 16 weeks and costs $15,000–$25,000. Even if he pays out-of-pocket, that's 4 months of no income growth plus education costs.

Compare that to the opportunity: a senior analyst at his firm makes $85K. If he succeeds in retraining, he might get there in 2–3 years. But his firm might not have an analyst role open. He might need to job hunt in a market where he's competing against people who already have 5 years of experience.

The timeline mismatch is real. Retraining isn't fast enough to match job displacement speed.

This is where personal finance meets harsh reality: retraining is possible, but it requires financial runway (emergency fund, savings rate, willingness to take risk) that most people don't have.

Your 5-Step Income Protection Strategy

Okay, that's the crisis. Here's the protection plan.

Step 1: Audit Your Job's AI Exposure Score

Be honest about your role. Answer these questions:

- How much of my work is routine, repeatable tasks vs. judgment calls?

- Can my work be done faster with AI, or is it fundamentally non-automatable?

- Is my role mostly about translating requirements into systems (codifiable) or about making calls in ambiguous situations (tacit)?

If you're 70%+ routine tasks, you're in the high-risk zone. You need to develop your differentiation fast.

Step 2: Document Your Unique Knowledge & Judgment Calls

This is your moat. Write down:

- 3–5 decisions you make that AI can't (yet): Which vendor to use? How to handle edge cases? What "done" looks like in gray areas?

- Your track record: How many times has your judgment saved the company money or risk?

- Your tacit knowledge: What do you know from experience that isn't written down anywhere?

Make this visible to your employer. Explicitly. "Here's what I bring that AI can't replicate." This shifts the conversation from "you're expendable" to "you're irreplaceable."

Step 3: Build AI Literacy (Fast Track to 56% Wage Premium)

You don't need to become an AI engineer. You need to become dangerous with AI tools in your domain.

Spend 3–6 months learning:

- Prompt engineering (how to ask AI tools the right questions)

- Workflow automation (using AI to handle the routine 30% of your job faster)

- Basic fine-tuning (adapting AI models to your specific use case)

- AI limitations (where AI fails—and this is where your judgment comes in)

Courses: Andrew Ng's "AI for Everyone" (free), Short AI courses on Coursera, Practical experimentation with ChatGPT/Claude/Gemini in your domain.

Goal: Become the person in your org who translates between AI capabilities and business outcomes. That person is valuable. That person commands premium pay.

Step 4: Focus on Decision-Making & Soft Skills

AI handles routine tasks. Humans handle judgment, negotiation, leadership, creativity, stakeholder management.

Invest in:

- Complex problem-solving (learning to think through messy, ambiguous situations)

- Communication (the ability to explain decisions and influence others)

- Change management (helping people navigate disruption—you'll be needed for that)

- Strategic thinking (seeing the 3-year impact, not just the quarterly metric)

These skills age better than coding skills or spreadsheet skills. A strategic thinker at 50 is more valuable than a junior programmer at 50.

Step 5: Diversify Your Income (Side Hustles as Income Insurance)

One income stream = one point of failure. In the AI economy, that's dangerous.

Build 2–3 income sources:

- Side hustles that leverage your judgment, not routine work: consulting, teaching, content creation, advisory

- Avoid: data entry, content mills, basic copywriting (all automatable)

- Target: $500–$2,000/month in side income within 12 months

This serves two purposes: (1) it's actual income diversification, and (2) it's your insurance policy. If your day job gets eliminated, you have a runway to retrain or job hunt without panic.

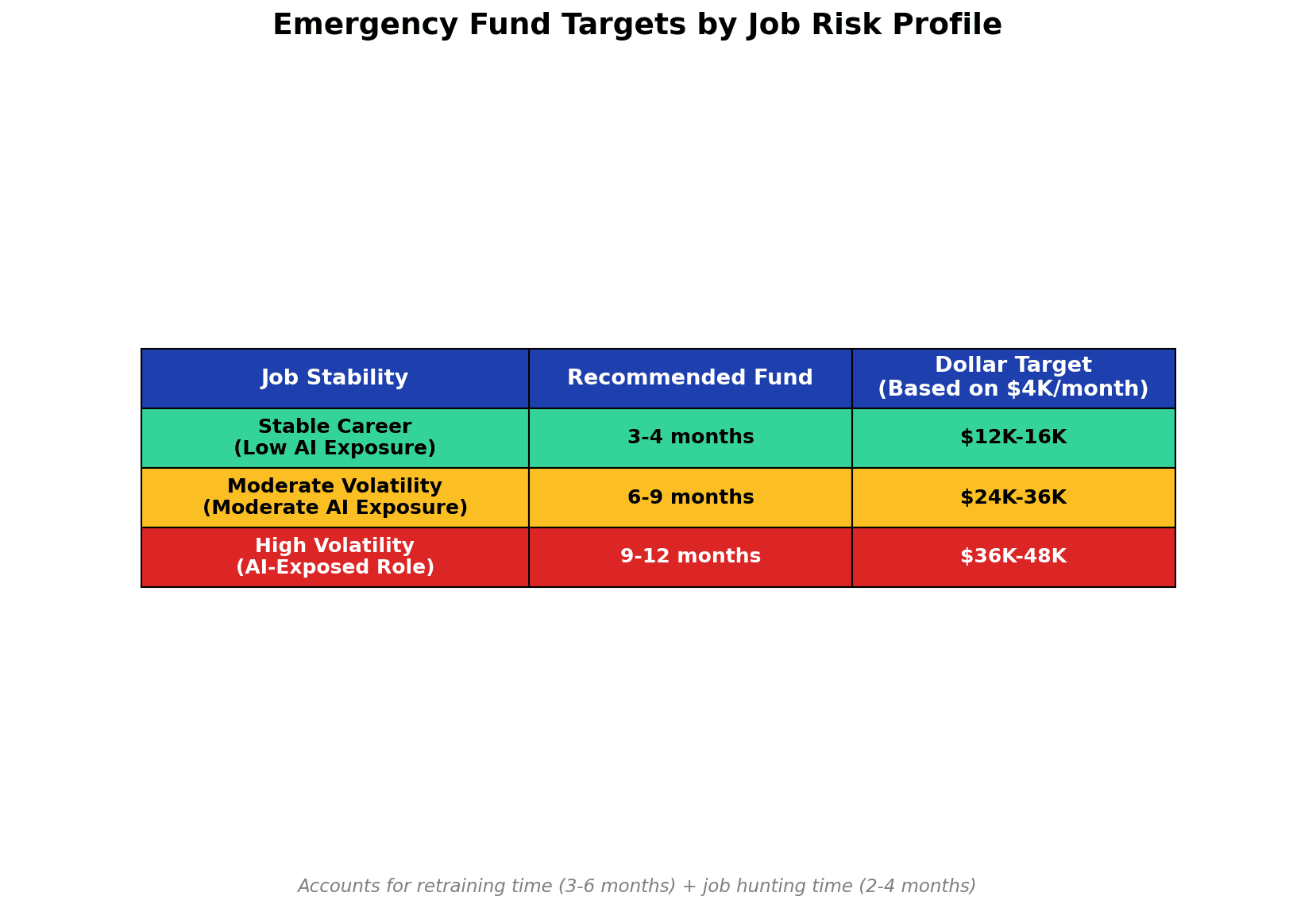

The 6-Month Emergency Fund Rule for AI-Exposed Jobs

Here's the emergency fund calculation that changed with AI risk.

Traditional rule: 3–6 months of expenses

New rule for AI-exposed roles: 6–12 months of expenses

Why? Because retraining takes 3–6 months, and job hunting in a competitive AI-disrupted market takes another 2–4 months.

If your monthly expenses are $4,000:

- Traditional emergency fund: $12,000–$24,000

- AI-risk-adjusted: $24,000–$48,000

59% of Americans can't cover a $1,000 emergency. If your job is AI-exposed, you need to be in the 41% that can survive a shock. Build this ruthlessly.

The 90-Day Income Future-Proofing Checklist

You don't need to do everything. Start this month:

Week 1–2: Audit & Awareness

- Map your job's AI exposure score (routine vs. judgment percentage)

- Research what AI tools are being used in your industry right now

- List your 3–5 unique judgment calls that AI can't do (yet)

- Calculate your monthly expenses (this is your emergency fund baseline)

Week 3–4: Build Foundations

- Calculate your target emergency fund (6–12 months of expenses)

- If you don't have 3 months' emergency fund yet, prioritize building this first

- Open a high-yield savings account earning 4%–5% for your emergency fund

- Make your first contribution (even $100 counts)

Week 5–8: AI Literacy Sprint

- Spend 5 hours learning one AI tool relevant to your job (ChatGPT, Claude, Google Gemini, domain-specific tools)

- Identify 3 routine tasks in your job that AI could speed up

- Document how AI could augment (not replace) your work

- Share findings with your manager: "Here's how I can use AI to work 2x faster on routine work, freeing time for strategic projects"

Week 9–12: Side Hustle & Skill Building

- Identify 1–2 side hustles based on your judgment skills (not routine work)

- Launch a test version (Upwork gig, freelance project, content creation—something with < $50 cost)

- Calculate your effective hourly rate (gross income – taxes – fees) ÷ hours worked

- Commit to reinvesting 70%+ of side hustle income into index funds or your emergency fund

- Enroll in one skill-building course (communication, strategic thinking, or advanced domain expertise)

What to track:

- Emergency fund balance (update monthly)

- Side hustle income & hours (calculate real hourly rate)

- AI tool proficiency (confidence level 1–10)

- New skills acquired (courses, certifications, judgment calls documented)

Why This Matters for Your FIRE Timeline

Here's the connection to financial independence.

If you're building toward FIRE (financial independence, retire early), AI job risk changes your strategy.

Scenario A (No AI protection):

- Current savings rate: 25% of $80K income = $20,000/year invested

- Age target to FIRE: 45 (on the 25x rule)

Scenario B (With AI protection strategy):

- AI literacy increases your wage premium: +15% compensation = $92K income

- Side hustle income: $500/month ($6,000/year) after taxes

- New savings rate: 32% of increased income = $31,360/year

- Age target to FIRE: 40 (5 years faster!)

The side hustle paradox shows that $500/month in reinvested side income cuts 5 years off your FIRE timeline. But only if it's a strategic side hustle (high judgment, low burnout) and you actually invest the money.

The income protection strategy is also wealth acceleration strategy.

The Counterargument: Why Optimists Might Be Right (But Timing Still Matters)

I need to acknowledge the case for optimism because it has real merit.

Historical precedent: Past tech waves (steam, electricity, computing, the internet) destroyed routine jobs and created new ones. In the long term, technological change is a net positive for employment.

Implementation delays: McKinsey estimates that today's technology could automate activities absorbing 60–70% of employees' time, yet actual adoption runs years behind that technical potential. The gap suggests the worst displacement is still ahead of us, not behind.

Legal and regulatory friction: Companies can't just fire accountants. There are regulatory requirements, client relationships, institutional knowledge that prevents instant automation.

All of this is true. The long-term story might be fine.

But here's why timing still matters:

If you're 24 right now, the "long term" is when you're 34. You've lost 10 years of career-building and compound growth. That gap never fully closes.

Even if 170 million jobs are created by 2030, they'll require different skills than the 92 million destroyed. The accountant displaced now can't just switch to "AI strategy consultant" without retraining, and retraining costs time and money.

The optimists are probably right that the aggregate job market recovers. But your personal career timeline is your only timeline.

Case Studies: Who Wins, Who Loses

Let me show you three real scenarios:

Maya: The Vulnerable Junior (Age 23)

Profile: Graduated with a BS in Computer Science in 2024. Junior developer at a fintech company, $68,000/year. No emergency fund. No side income.

The AI impact: Her firm deployed GitHub Copilot enterprise-wide. Within 6 months, they're consolidating junior roles. She's moved to a 6-month contract.

Why she's vulnerable: Maya's job was 80% routine tasks (implementing standard patterns, writing boilerplate, debugging). That's exactly what Copilot does. Her lack of tacit knowledge (3–5 years of experience) means she has no moat.

The recovery challenge: She lacks the emergency fund to survive retraining. She lacks side income to bridge a gap. She's trying to find a new junior role in a market where companies stopped hiring juniors.

Outcome (likely): Contract work at lower rates, or 6-month bootcamp into a different field. Her FIRE timeline shifts from 40 → 50+.

Ethan: The Protected Senior (Age 38)

Profile: 12 years in operations at a logistics company. Managing 8 people, $95,000 + $15,000 bonus. Married, one kid, $180,000 emergency fund.

The AI impact: His firm deployed an AI workflow optimization tool. Instead of eliminating his job, it amplified his impact. He now makes faster strategic decisions with real-time data. His boss asks him to lead the "AI-augmented operations" task force.

Why he's protected: Ethan's role was 60% judgment (which vendors to use, how to negotiate, team decisions) and 40% routine (scheduling, reporting). AI accelerates the routine 40%. His judgment-based 60% becomes even more valuable.

The recovery advantage: He has savings, emergency fund, visible strategic value. His tacit knowledge (years of vendor relationships, negotiating skill, team dynamics) is irreplaceable.

Outcome: Compensation rises to $115K + $25K bonus. His FIRE timeline accelerates. He's insulated.

Jordan: The Adaptable Specialist (Age 31)

Profile: Self-employed accountant with 5 years of practice. 40 clients, $110,000/year income. No employees. $12,000 emergency fund.

The AI impact: AI-powered tax software (Intuit, Thomson Reuters) does 70% of what he used to do. His billable hours drop 30%.

The pivot: Jordan recognizes the threat early. He repositions from "tax preparer" to "AI-optimized tax strategy advisor." He charges $250/hour for strategy work (vs. $150/hour for prep work). He adds a YouTube channel teaching small business owners AI tax tools. New side income: $2,000/month.

Why he survives: Jordan moved from a high-AI-exposure role (tax prep, codifiable) to a judgment-based role (strategy). He built a side income. He's actively evolving.

Outcome: Same $110K income, but composition changed (60% advisory, 40% YouTube/side). His job security increased because his core business is now judgment-based, not routine.

The lesson: Position matters more than luck.

The Burnout Amplifier: Why AI Job Anxiety Destroys Your Finances

One thing nobody talks about: AI job anxiety amplifies burnout, and burnout destroys your income resilience.

When you're worried your job might be automated, you work harder. You try to prove your value. You stop setting boundaries. You stay late. You take on more projects.

Quiet burnout is what happens next: you're exhausted while appearing productive. Your stress-driven spending spikes ($300+ monthly on stress purchases). Your savings rate collapses from 25% to 5%.

That burnout costs you $5,000–$15,000 per year in direct costs, plus years of delayed FIRE timeline.

The protection strategy isn't just about future-proofing your income. It's about protecting your psychological capacity to make smart financial decisions today.

When you have a concrete income protection plan (emergency fund, side hustle, AI literacy), the anxiety decreases. You stop catastrophizing. You can think clearly.

Clear thinking = better financial decisions = faster path to freedom.

The Gen Z Opportunity: Starting Early Wins

Here's the one piece of good news: Gen Z can win this.

Because they're starting their careers now, they can build AI literacy before it becomes essential. They can develop side hustles while living at home (lower expenses). They can accept lower entry-level pay if the company offers AI training.

Gen Z can retire by 50 with phased part-time work starting at age 22 precisely because they have 40+ years for compound growth. If they use those early years to build AI literacy and side income, they accelerate everything.

The Gen Z cohort that is reading this and implementing the 5-step strategy now will be the generation that actually reaches FIRE, because they'll have weathered the AI transition instead of being blindsided by it.

Millennials and Gen X: you can still implement this strategy. It's harder because you have fewer working years, but the math still works. You need the same 5-step plan, just executed faster.

Your 90-Day Tracker: Making Progress Visible

The reason people fail at financial protection is lack of visibility.

You can use My Financial Freedom Tracker to monitor:

- Emergency fund progress: How many months of expenses saved?

- Side hustle income: Is your monthly take-home growing?

- Net worth by source: How much comes from salary vs. side income?

- AI skill development: Track courses completed, tools learned, hours invested

- Savings rate trend: Is it trending up as you add side income?

The magic of tracking is that visibility drives behavior. When you see your emergency fund grow from $5K → $10K → $15K, you stay motivated. When you see side hustle income increasing from $200 → $400 → $600/month, you keep pushing.

Without tracking, progress feels invisible. You quit.

With tracking, progress is measurable. You keep going.

The Bottom Line: Your Income Is Under Threat, But Your Career Isn't

Let me be clear: this isn't doomsday talk. This is reality talk.

Your specific job might be vulnerable to AI. But your career isn't—if you make the right moves now.

The difference is:

- Job vulnerability: Your specific role might be automated in 2–5 years

- Career resilience: You can build skills, income streams, and financial security that survive job disruption

The 5-step strategy (audit exposure, document unique value, build AI literacy, develop soft skills, diversify income) is how you move from vulnerable to resilient.

Will it take effort? Yes. 3–6 months of focused work, ongoing learning, side hustle execution.

Is it worth it? Absolutely. The difference between someone who implements this strategy and someone who doesn't is $500K–$1M+ in lifetime wealth and 5–10 years on your FIRE timeline.

Action Plan: This Week

Don't wait. The math works better if you start now:

Today: Answer this one question: "On a scale of 1–10, how much of my job is routine tasks vs. judgment calls?" If it's 7+, move to tomorrow.

Tomorrow: List your 3–5 unique judgment calls that your company pays you for. (This is your moat.)

Day 3: Research one AI tool relevant to your industry. Spend 30 minutes learning it.

Day 4: Calculate your target emergency fund (monthly expenses × 6–12 months). Write the number down.

Day 5: Open a high-yield savings account earning 4%–5%. Make your first deposit (any amount).

Day 6: Identify one side hustle idea based on your judgment skills. Research three potential clients/platforms.

Day 7: Share your income protection plan with someone you trust. External accountability changes everything.

That's your week. From there, you have momentum.

Conclusion: The Choice Is Yours

The data is clear: AI is disrupting the job market now. Young workers are being hit hardest. Entry-level roles are disappearing.

But disruption doesn't mean disaster.

It means opportunity for those who prepare.

The people who will thrive in the 2026–2030 labor market are those who:

- Understood the risk early (you're doing this now)

- Built AI literacy while it was still an advantage (not a requirement)

- Diversified income streams (side hustles as insurance)

- Documented their irreplaceable judgment (moat building)

- Protected their financial resilience (emergency fund, savings rate)

You have all the information you need. You have the 5-step plan. You have a 90-day checklist.

What you do with the next 90 days determines whether you're protected or vulnerable when AI reshapes your industry.

The choice isn't whether AI automation will affect you. It will.

The choice is whether you'll be ready.

📩 Have questions about your specific industry or role? Email me at dennis.vymer@myfinancialfreedomtracker.com. I'm interested in what's happening in your sector and how the income protection strategy applies to your situation.

For tracking your side hustle income and seeing how it accelerates your path to financial independence, use MFFT's multiple income stream tracking. Visibility changes everything.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.