FinTok Money Myths: 3 Mistakes Gen Z Women Make

TL;DR: 79% of millennials and Gen Z get financial advice from social media, and FinTok has genuinely helped — 68% say its advice improved their financial situation. But three myths cost real money: manifestation rituals instead of automated investing, extreme no-spend challenges that rebound, and uncredentialed finfluencers selling courses. The fix isn't leaving FinTok — it's the credibility checklist below plus an evidence-based system: baseline, goals, automation, measurement.

New to personal finance and investing?

If you're just getting started, I recommend checking these out first:

- How to Start a Budget — the foundation of money management

- How to Start a Budget — escape paycheck-to-paycheck living

- Financial Levels Step by Step — where everything fits in sequence

Your TikTok feed has 47 videos from creators with purple nails and coffee shop backgrounds. They're telling you about manifestation rituals, "girl math" spending logic, no-spend challenges, and finfluencers who promise wealth without the boring math.

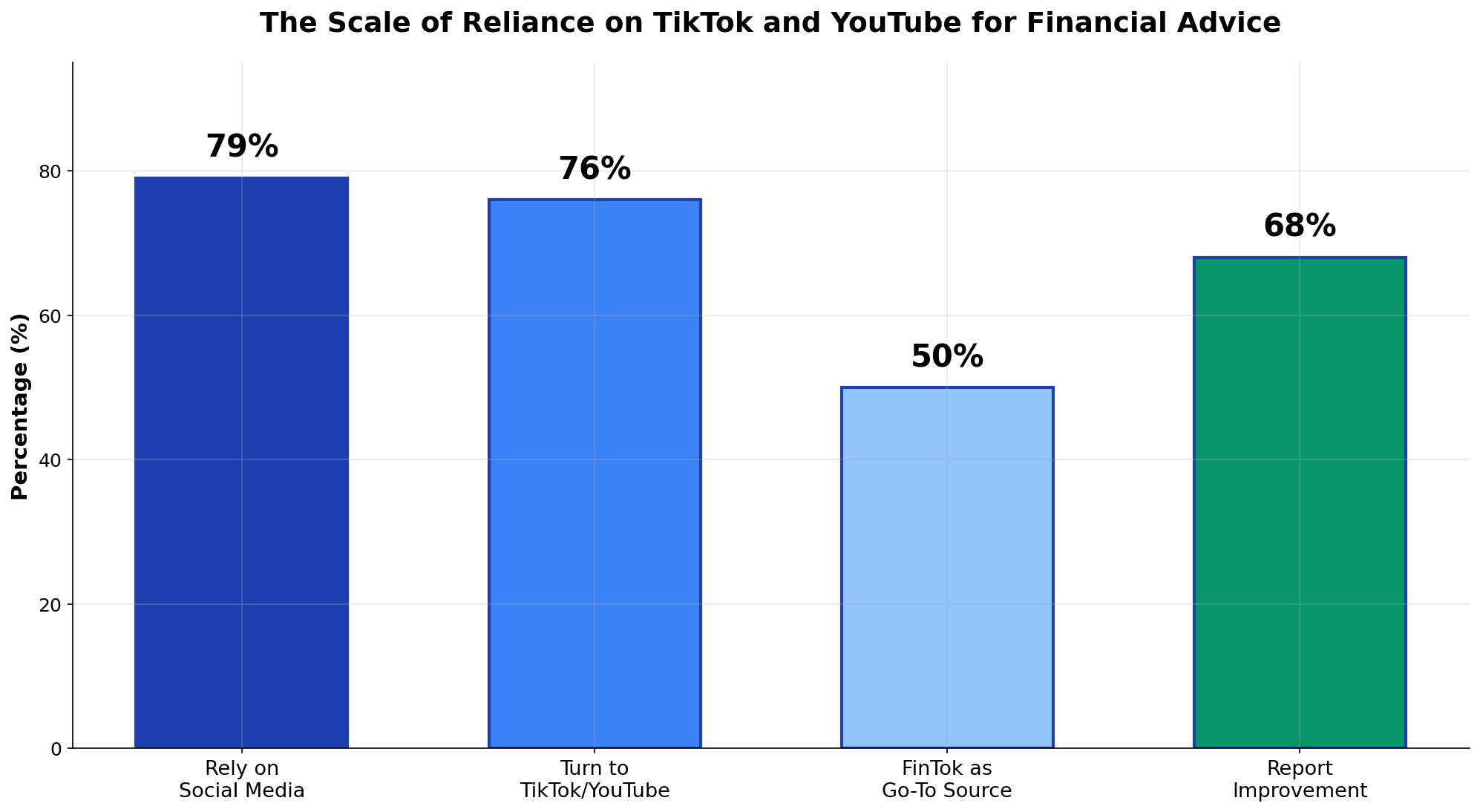

And here's what's insane: 79% of your generation is learning about money this way.

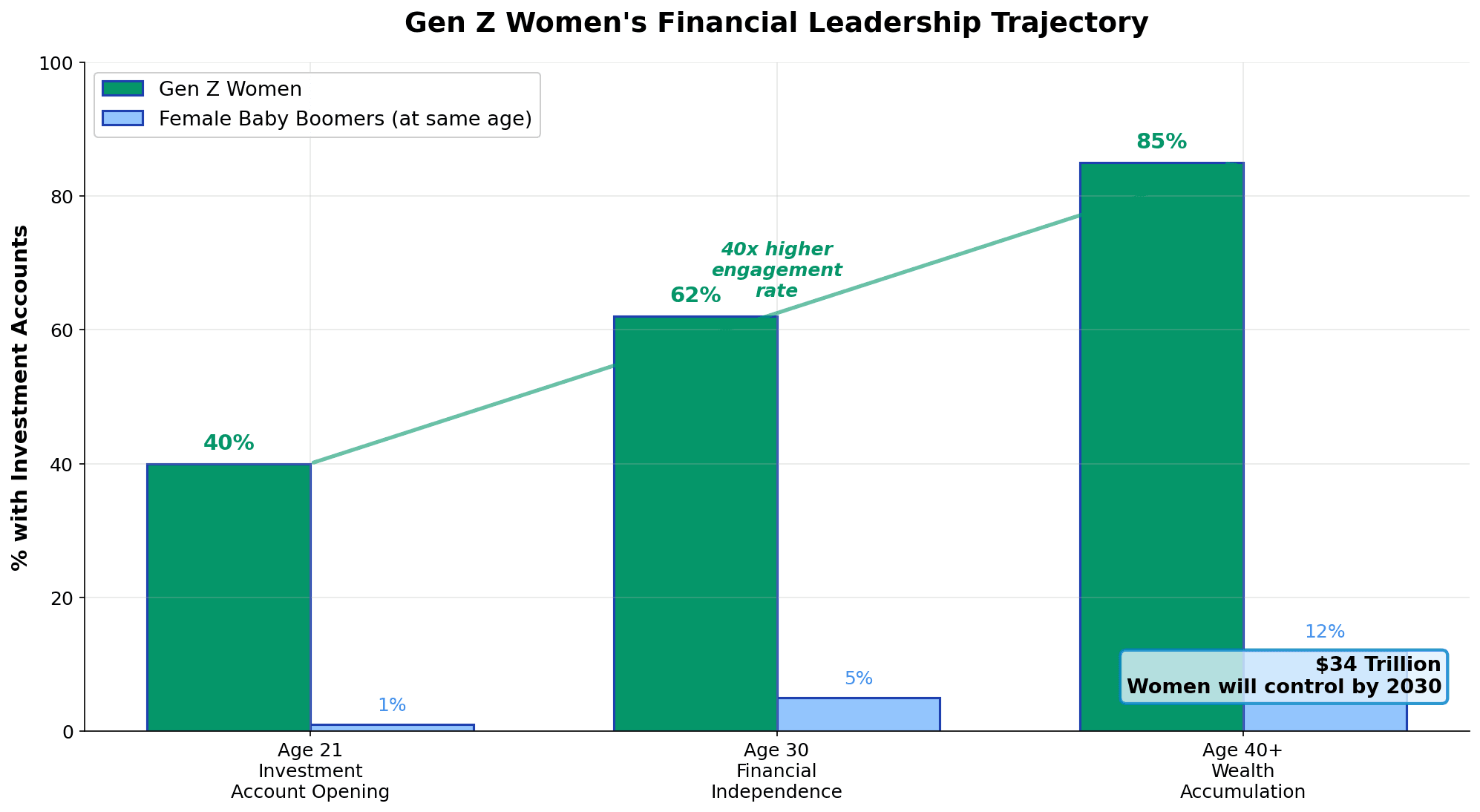

Gen Z women are leading a financial revolution on TikTok. Nearly 40% of Gen Z women have opened investment accounts by age 21, compared to just 6% of female Baby Boomers. By 2030, women will control $34 trillion in investible assets. The confidence, the transparency, the refusal to be ashamed of money conversations — that's all genuinely powerful.

But there's a problem.

The same platform that's democratizing financial education is also spreading dangerous misconceptions. Finfluencers with 2M+ followers have no credentials, no disclosures, no accountability. Only 20% of finfluencer investment content includes ANY disclaimer. Manifestation trends have 1.7M TikTok posts teaching people that visualizing wealth is a substitute for actual wealth-building mechanics.

This article is about the balance: celebrating what Gen Z women are getting right, deconstructing what they're getting dangerously wrong, and building a framework that honors the transparency and community Gen Z loves while grounding it in actual mathematics.

The FinTok Explosion: 79% of Gen Z Is Learning About Money (And How)

Let me start with the scale of this shift.

79% of millennials and Gen Z rely on social media platforms for financial advice. Not traditional media. Not financial advisors. Not books. Social media.

Here's the breakdown:

- 76% of Gen Z turn to TikTok and YouTube for money matters

- 50% say FinTok is their go-to source for financial advice

- 34% specifically learned personal finance from TikTok and YouTube

- 68% report that FinTok advice has helped improve their financial situation

The platform has become the de facto financial education system for young people who would never read a Suze Orman book or pay $200/hour for an advisor.

And in some ways, that's a feature, not a bug. Traditional finance is gatekept. Financial advisors require minimum account balances. Banks are unwelcoming to people without generational wealth. Financial jargon is deliberately obscure to maintain authority.

FinTok broke that. Suddenly, a 23-year-old can teach 2M people about budgeting in 60 seconds. Suddenly, money conversations happen in the open instead of in shame-filled silence.

But with that democratization came a problem: the platform rewards virality more than accuracy.

What Gen Z Gets Right: Transparency, Community, and Breaking the Money Taboo

Before we talk about what's broken, let's credit what's working.

Gen Z women leading FinTok is changing something fundamental: money is no longer shameful.

For decades, people hid financial struggles. They didn't talk about budgets, debt, or how much they made. That silence created shame, prevented rational decision-making, and trapped people in cycles they couldn't talk their way out of.

Gen Z is saying: "Not anymore."

The Transparency Shift

Gen Z women are publicly sharing:

- Their actual budgets and spending categories

- Their salary negotiation wins (and failures)

- Their debt payoff progress

- Their investing mistakes

- The fact that they're struggling financially

This radical honesty is psychologically powerful. Research shows that 70% of Americans struggle with financial anxiety, but 76% feel alone in that struggle. When you're the only one talking about money problems, you internalize it as personal failure.

Gen Z women saying "I have $40K in student debt" or "I can't afford to move out" or "I'm paycheck-to-paycheck" removes the shame. It turns a personal problem into a collective problem — and collective problems get solved faster.

Early Investing and Financial Agency

Here's a stat that should make you optimistic: nearly 40% of Gen Z women opened investment accounts by age 21. That's 40x the rate of female Baby Boomers at the same age.

This matters because investing early is the single most powerful wealth-building tool. A person who starts investing at 20 will have roughly 3x the wealth of someone who starts at 30, all else equal. The stakes are spelled out in the female wealth gap and the 5-step plan to close it — every year of waiting compounds against you.

Gen Z women are opting in early. They're thinking about wealth-building as something for them, not something reserved for rich people or finance bros.

Community and Accountability (Loud Budgeting)

The loud budgeting movement started on TikTok and is having real effects. Gen Zers who practice loud budgeting save an average of $629 per month. They're building accountability systems where people share goals, celebrate wins, and support each other through setbacks.

That's not a small thing. That's the difference between willpower (which fails) and systems (which work).

Gen Z women are right about the core insight: transparency builds wealth faster than shame does.

The problem is what happens when transparency meets pseudoscience.

The Dangerous Myth #1: Money Manifestation, Astrological Timing, and Intention-Setting

Let me be direct: there is no scientific evidence that visualization, manifestation, crystals, tarot, or astrological timing builds wealth.

Not "limited evidence." Not "some research suggests." None.

The #MoneyManifestation hashtag has 1.7M posts on TikTok. Creators with millions of followers are teaching people to:

- Visualize wealth during Mercury retrograde's end

- Write financial goals on specific "lucky" dates

- Spend money on manifestation crystals and tarot readings

- Practice "abundance thinking" as a substitute for budgeting

And Gen Z women are taking this advice.

The Mechanism is Wrong

Here's what manifestation proponents claim: Your thoughts attract wealth through the "law of attraction." The universe responds to your energy. If you visualize money, it comes to you.

This is pseudoscience. It's been studied extensively, and the mechanism doesn't exist. Thoughts don't emit frequencies that attract cash. The universe doesn't negotiate with your intentions.

But here's where it gets dangerous: there's a kernel of psychology that makes it seem real.

When you visualize a financial goal, you become more motivated to work toward it. When you meditate, you reduce stress and think more clearly. When you journal, you gain insight into your spending patterns. These are real psychological benefits.

But the benefit comes from behavior change, not metaphysical attraction. And crucially, these benefits only work if you also change your behavior.

The Cost of Waiting for Magic

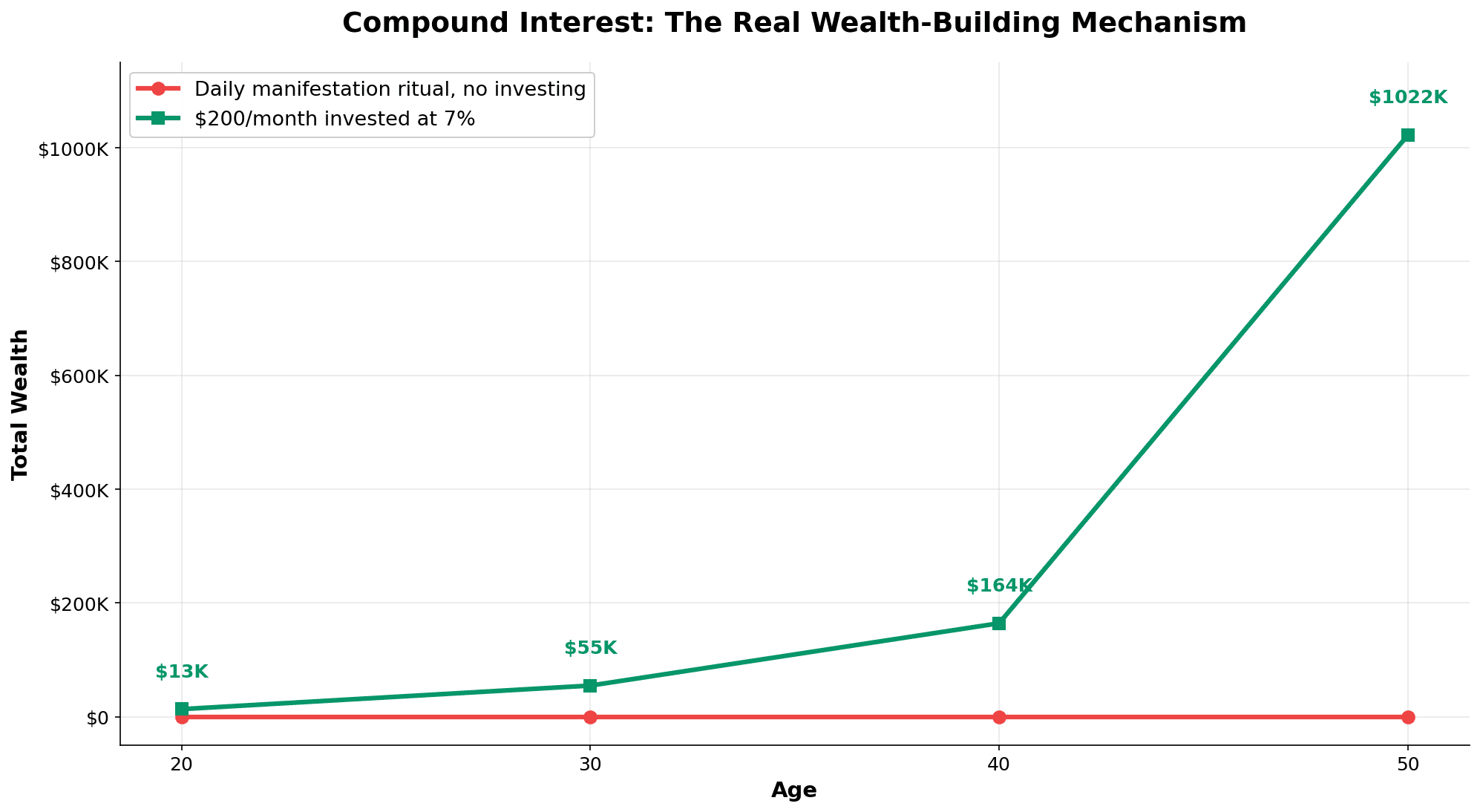

Madison is a real case from my research. At 23, she got inspired by a FinTok creator and spent 30 minutes each morning visualizing wealth, writing her financial goals on specific lucky dates, and buying "manifestation crystals" ($150).

By the end of the year, she had saved nothing. The manifestation ritual gave her the illusion of progress while she did zero actual work.

Contrast this to a different approach: invest $200/month at 7% annual returns starting at age 23.

At age 30: $13,468 At age 40: $54,887 At age 50: $164,421 At age 65: $1,022,486

That's over a million dollars from a simple mechanical process. No visualization required. No astrological timing. Just math, consistency, and time.

The tragedy is that Gen Z women have the advantage of starting young. But they're being told the advantage comes from intention-setting instead of the thing that actually builds wealth: early, consistent investing compounded over decades.

The Real Mechanism

Wealth builds through three mechanisms:

- Income — earning money

- Savings — not spending it

- Time — letting compound interest do the work

No amount of manifestation changes these mechanics.

The Dangerous Myth #2: Extreme Frugality and No-Spend Challenges as Sustainable Strategy

The second major trend is actually closer to good advice, but taken to an unsustainable extreme.

"No-Buy 2025" and no-spend challenges are real. Thousands of Gen Z women are trying to go months without spending on non-essentials. Some save significant amounts. And initially, it feels great.

But here's what behavioral psychology tells us: deprivation-based budgets fail long-term.

Research by Gretchen Rubin and others shows that extreme restriction often leads to overcorrection. You can't say no to everything for four months and then suddenly return to moderate spending. The deprivation creates a psychological need for release.

The Rebound Effect

Chelsea saw a viral "No-Buy 2025" challenge. For three months, she avoided all discretionary spending — no coffee, no meals out, no entertainment. She saved $1,200.

But in month four, psychologically exhausted by deprivation, she overspent on a shopping spree ($2,000). The $1,200 gain was completely wiped out, plus she added $800 in debt. And she felt ashamed.

The data supports this pattern: 67% of people using no-spend challenges report burnout by week 8, and most rebound spending within 3-4 months.

The Sustainable Alternative

A better approach is loud budgeting: setting a realistic savings rate (20-25% of income) while explicitly allocating money for joy spending ($50-100/month for things you care about).

This isn't sexy. It won't go viral on TikTok. But it works.

People practicing loud budgeting save $629/month consistently. They don't crash. They don't shame spiral. They build wealth predictably.

The difference between saving $1,200 once via extreme frugality and then spending it all, versus saving $600-700/month consistently, is the difference between a trend and a wealth-building system.

The Math of Sustainable Budgeting

| Approach | Monthly Savings | Year 1 | Year 5 | Consistency |

|---|---|---|---|---|

| No-Spend Challenge (extreme) | $1,200 then rebound | $3,000-6,000 | $0 (cycles back) | Low |

| Loud Budgeting (22% rate) | $550 | $6,600 | $40,000 | High |

| Manifestation only | $0 | $0 | $0 | Failed |

The message Gen Z women should hear: small, consistent actions compound. Extreme deprivation doesn't.

The Dangerous Myth #3: Finfluencers Without Disclosures or Credentials

This is where things get truly dangerous.

Only 20% of finfluencer investment content includes ANY disclosure. That means 80% of investment advice on TikTok comes with no indication of:

- Whether the creator has credentials (CFP, CFA, FINRA)

- Whether they're being paid to recommend something

- Whether they have conflicts of interest

- Whether they have a financial advisor license

Meanwhile, 70% of finfluencers are non-compliant with transparency requirements. This isn't a gray area. The SEC and FINRA have been explicit about what needs to be disclosed. Finfluencers are simply ignoring it.

The Credential Gap

A CFP® (Certified Financial Planner) requires:

- 6,000 hours of documented planning experience

- Passing a 10-hour comprehensive exam

- Ongoing education requirements

- Fiduciary duty (legally required to act in clients' best interests)

- Regulatory oversight

A "money coach," "wealth mentor," or "finfluencer" requires:

- A TikTok account

- Follower count

- Confidence

These are not equivalent. Not even close.

Real Stories of Getting Burned

Zara, 22, followed a finfluencer with 4.5M followers who promoted "EZ Coin," claiming it was "the next Bitcoin." She invested her $3,000 emergency fund. Within three weeks, the creator posted less, the coin lost 65% of value, and Zara lost $1,950.

She later discovered the creator had been paid to promote the coin — undisclosed.

This is happening at scale. The FTC estimates that cryptocurrency pump-and-dump schemes orchestrated via finfluencers steal millions annually, primarily from young people.

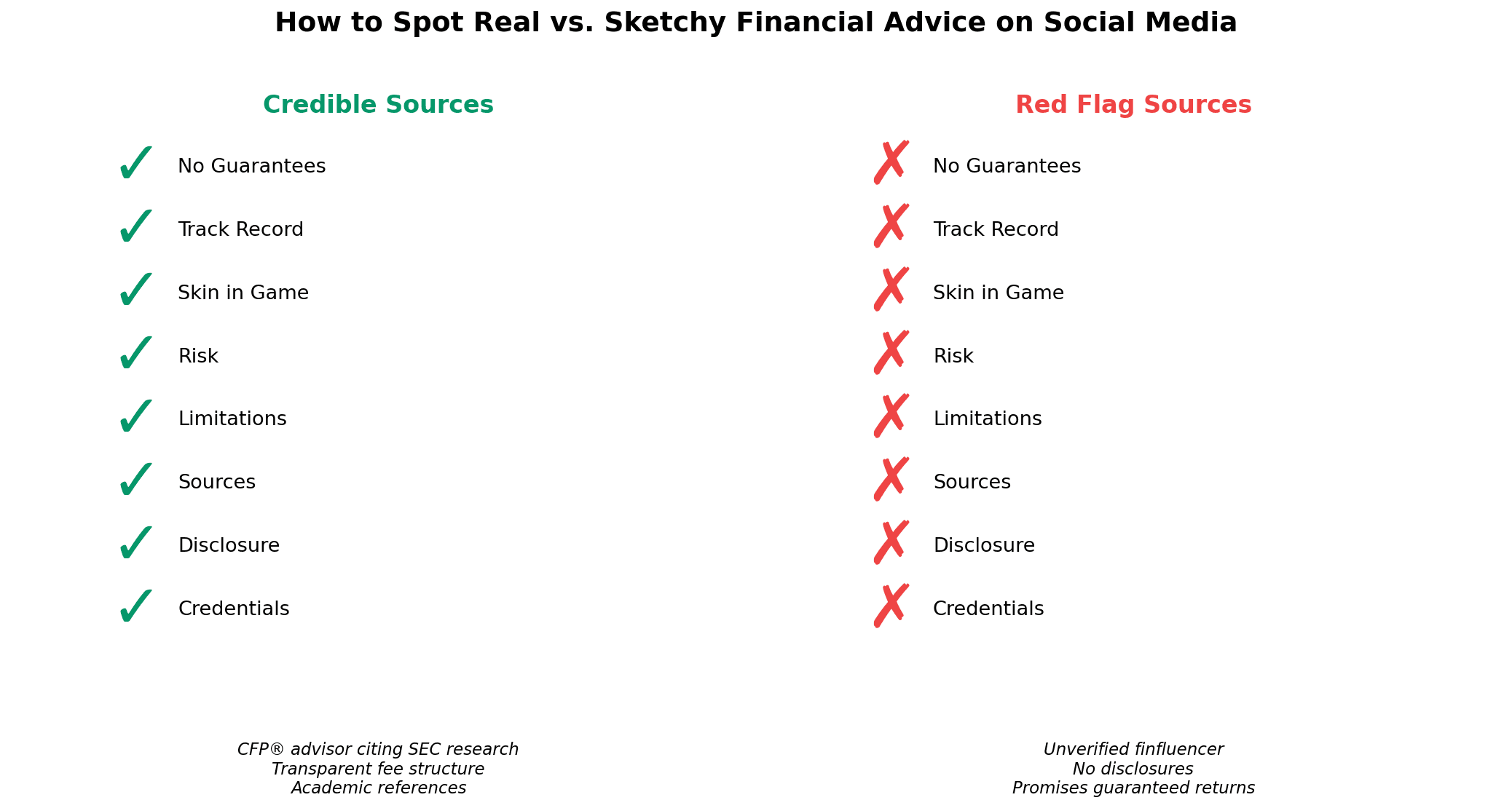

How to Spot Real vs. Fake

A credible financial voice (on or off social media):

- Discloses credentials (CFP®, CFA®) or clearly states they don't have them

- Lists potential conflicts of interest

- Cites sources and data

- Discusses downsides and risks

- Emphasizes that advice should be personalized

- Avoids extreme guarantees

A sketchy finfluencer:

- No credential disclosure

- Promises quick wealth or "passive income"

- Heavy lifestyle flexing (designer bags, luxury vacations)

- No mention of risk

- Pressure to act immediately or miss out

The FINRA takeaway is important here: a large follower count is not a credential.

Loud Budgeting 2.0: What FinTok Did Right, Refined

Now here's the path forward that actually works.

Loud budgeting takes the transparency and community that made FinTok powerful and adds data-driven decision-making and realistic targets.

What Loud Budgeting Does Right

- Removes shame from having limits: Saying "I can't afford that" becomes empowering instead of embarrassing

- Builds accountability: Public commitment to goals increases follow-through by 60%

- Creates community: Shared struggles reduce financial anxiety

- Normalizes money talk: Younger generations growing up with financial transparency will build wealth faster

How to Refine It

Add these elements to make loud budgeting even more powerful:

- Evidence-based targets — not "spend nothing," but "save 20-25% of income"

- Fact-checking — cite sources when discussing financial strategies

- Risk disclosure — talk about what could go wrong, not just what could go right

- Personalization — "This works for me, but it might not be right for your situation"

- Long-term focus — celebrate 3-year progress, not just 30-day wins

The goal isn't to kill the FinTok energy. It's to supercharge it with actual mechanics.

The Wealth-Building Framework Gen Z Actually Needs

Okay, you want to build actual wealth. Here's the step-by-step framework.

Step 1: Understand Your Baseline

- Calculate monthly expenses (actual outflow, not budget)

- Know your current income (after taxes)

- Track where money is going for 30 days in a budgeting app

Don't guess. Don't estimate. Know the actual numbers.

Step 2: Set Evidence-Based Goals

- Emergency fund: 3-6 months of expenses (why this matters)

- Savings rate: 15-25% of after-tax income

- Retirement: 10-15% of gross income (including employer match)

- Debt payoff: Accelerated plan if you have it

These aren't arbitrary. They're based on decades of personal finance research.

Step 3: Build Systems (Not Rituals)

- Automate your savings (payday → savings account before you see the money)

- Dollar-cost average your investments (same amount every month, regardless of market)

- Use budgeting tools to track progress monthly

Rituals make you feel like you're doing something. Systems actually make you build wealth.

Step 4: Measure and Adapt

- Monthly check-in: Did you hit your targets?

- Quarterly review: Is your savings rate sustainable?

- Annual adjustment: Increase contributions as income rises

The framework is boring. But boring works. The people who reach financial independence aren't usually the ones visualizing wealth. They're the ones with spreadsheets and automatic transfers.

How to Spot Credible Financial Information on Social Media

Let me give you a practical tool you can use today.

Before following financial advice from anyone on social media (FinTok, Instagram, Twitter, YouTube), ask these questions:

The Credibility Checklist

1. Credentials — Does this person have skin in the game?

- Do they have CFP®, CFA®, or relevant credentials? (Verify on CFP Board or CFA Institute websites)

- If not, do they clearly state that they're not a financial advisor?

- Have they actually done the thing they're teaching?

2. Disclosure — Are conflicts of interest clear?

- Do they mention if they're being paid to recommend something?

- Do they state their own holdings if recommending investments?

- Is there a link to their financial advisory registration (if applicable)?

3. Sources — Can they cite actual research?

- Do they reference academic studies, SEC data, or government reports?

- Or do they just say "I read somewhere" or "Studies show"?

- Can you fact-check their claims?

4. Limitations — Do they acknowledge uncertainty?

- Do they say "This might not apply to your situation"?

- Do they discuss worst-case scenarios?

- Or do they promise results?

5. Risk — Is risk discussed?

- Do they talk about downside scenarios?

- Do they mention fees, volatility, and potential losses?

- Or do they only talk about upside?

6. Skin in the Game — Are they using their own strategies?

- Do they invest their own money the way they're recommending?

- Or are they recommending products they don't use?

7. Track Record — Can they show long-term results?

- Not cherry-picked wins, but actual historical performance?

- Audited results or just testimonials?

8. Guarantees — Do they avoid extreme claims?

- Legitimate advisors never promise specific returns

- "Get rich quick" and "Passive income without work" are red flags

Red Flag Examples:

- "This one weird trick banks don't want you to know"

- "Guaranteed 50% returns"

- Crypto promotion with no risk disclosure

- Extreme claims about passive income

- No mention of who's paying them

If someone fails 4 or more of these, they're not credible. It doesn't matter if they have millions of followers.

Gen Z Women Are Right to Take Control — Here's How to Do It Right

Let me affirm something real here.

Gen Z women taking charge of their finances is powerful. The fact that 40% have investment accounts by age 21, that 79% are actively seeking financial information, that money conversations are becoming normalized — this is genuinely transformational.

Women historically were kept out of financial decisions. Older generations of women had financial advisors (husbands) managing their money. Financial literacy materials were written for men. The assumption was that women didn't care about or couldn't understand wealth.

Gen Z women are rejecting that entirely. They're taking control. They're learning. They're building.

That impulse is exactly right.

The only adjustment is to pair that impulse with rigor. Not rigor that kills the joy of community, but rigor that makes the community more effective.

Here's the path:

- Keep the transparency — talk openly about money, celebrate wins, support each other

- Add data-driven decision-making — know your numbers, cite sources, fact-check trends

- Evaluate finfluencers ruthlessly — follow creators with credentials, not just followers

- Demand better from platforms — TikTok should require financial advice disclaimers

- Teach media literacy — treat financial claims like you'd treat news claims: verify before accepting

The future of personal finance belongs to people who educate themselves rigorously while building community. That's gen Z women's competitive advantage.

Action Plan: Start This Week

You don't need to overhaul your entire financial life. You just need to make smarter choices moving forward.

If You've Been Influenced by Manifestation Trends

Replace the 30-minute daily visualization ritual with:

- 5 minutes setting a real financial goal (specific number, specific date)

- 5 minutes tracking your actual progress toward it

Math beats magic every time.

If You're Doing a No-Spend Challenge

Transition to loud budgeting:

- Calculate your realistic savings rate (20-25%)

- Build in explicit joy spending ($50-100/month)

- Share your real goal (not "spend nothing," but "save 25% this month") with a friend

Sustainable beats extreme.

If You're Following Unvetted Finfluencers

This week, do a credibility audit:

- Pick 3 financial creators you follow

- Run them through the checklist above

- If they fail 4+ criteria, unfollow

- Replace them with one CFP-credentialed creator

Credentials matter.

Universal Action: Find Your Money Circle

Find 2-4 people (friends, family, online community) who want to talk about finances honestly.

Meet monthly or quarterly. Share:

- Your savings goal

- Whether you hit it

- One thing you learned

- One challenge you faced

This is loud budgeting at its best. It's free, it's powerful, and it actually builds wealth.

Conclusion: The Future of Gen Z Women's Wealth

I started this article by celebrating Gen Z women's financial revolution. I want to end the same way.

You're doing something genuinely unprecedented. You're talking about money openly. You're investing younger than any generation before you. You're building communities around financial goals instead of hiding them.

That's powerful.

The only ask is to pair that power with rigor. Don't abandon the transparency and community that's working. Add fact-checking, data, and credibility standards.

The finfluencers with the most followers aren't always the ones building the most wealth for their audiences. The creators with credentials might not be viral on TikTok. But they're the ones who'll actually help you reach financial independence.

By 2030, women will control $34 trillion in assets. Gen Z women are going to lead that shift. The question is whether you'll build that wealth through manifestation and TikTok trends, or through the boring, reliable, proven mechanisms that actually work.

I know which one I'd choose.

Start this week. Pick one thing from the action plan. Change one habit. Follow one credible creator instead of a viral one.

In 10 years, you'll be grateful you did.

📩 Questions about financial literacy, evaluating finfluencers, or building actual wealth? Email me at dennis.vymer@myfinancialfreedomtracker.com. I read every message.

For a data-driven framework on wealth building and goal tracking, use My Financial Freedom Tracker to set and monitor your financial goals. For specific budgeting help, check out our budgeting guide. For understanding where wealth-building fits in your overall financial journey, see Financial Levels Step by Step.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.