Money Dysmorphia: Why You Feel Broke When You’re Fine

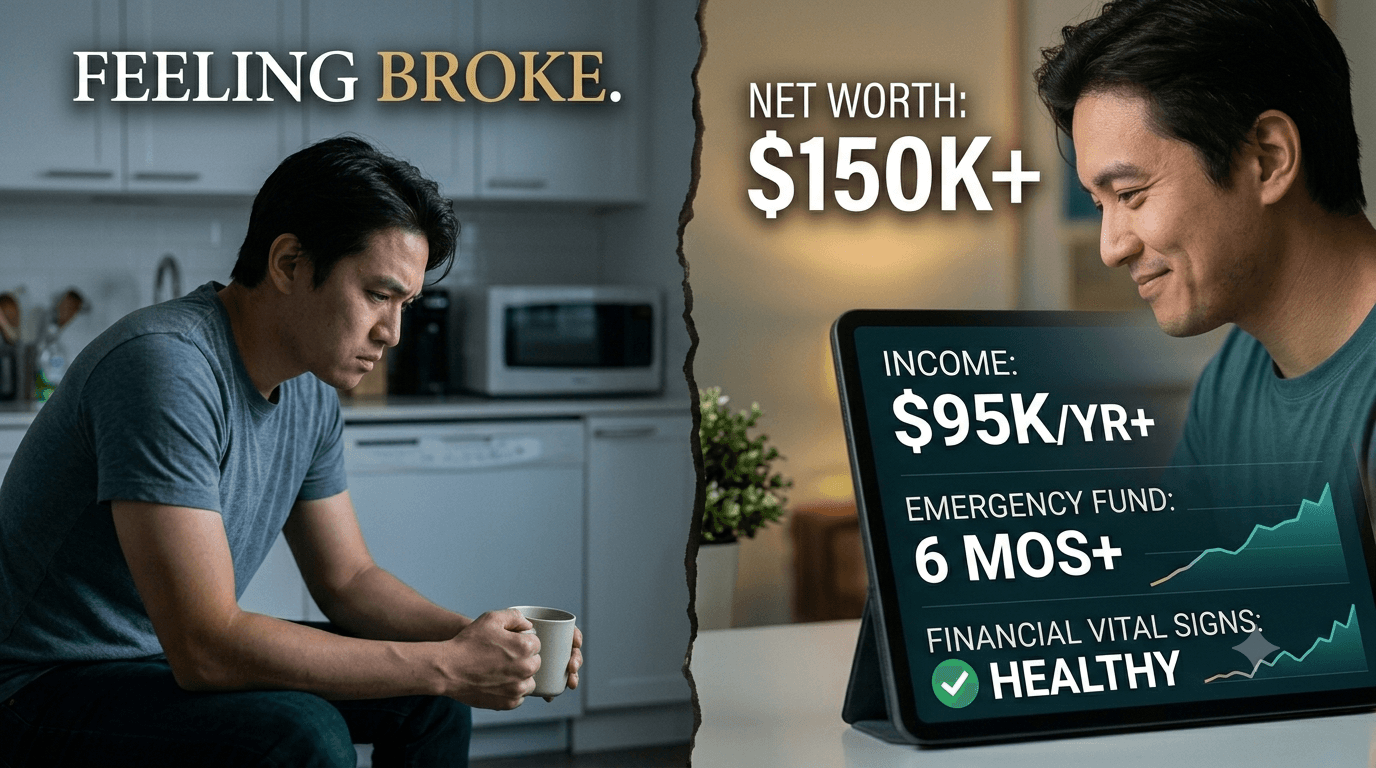

Sarah, a 28-year-old marketing manager, makes $78,000 a year. She has $22,000 in a savings account and a 401(k) that grows every paycheck. By every benchmark that exists, she is ahead of the typical 28-year-old in America. She is winning.

She does not feel like she is winning. She feels broke.

Last Tuesday she turned down a $40 dinner she could easily afford, then spent the night doom-scrolling net-worth comparison videos and a former classmate's down-payment announcement. She has not opened her brokerage app in three weeks because looking at it makes her stomach tighten. The spreadsheet says she is fine. Her nervous system did not get the memo.

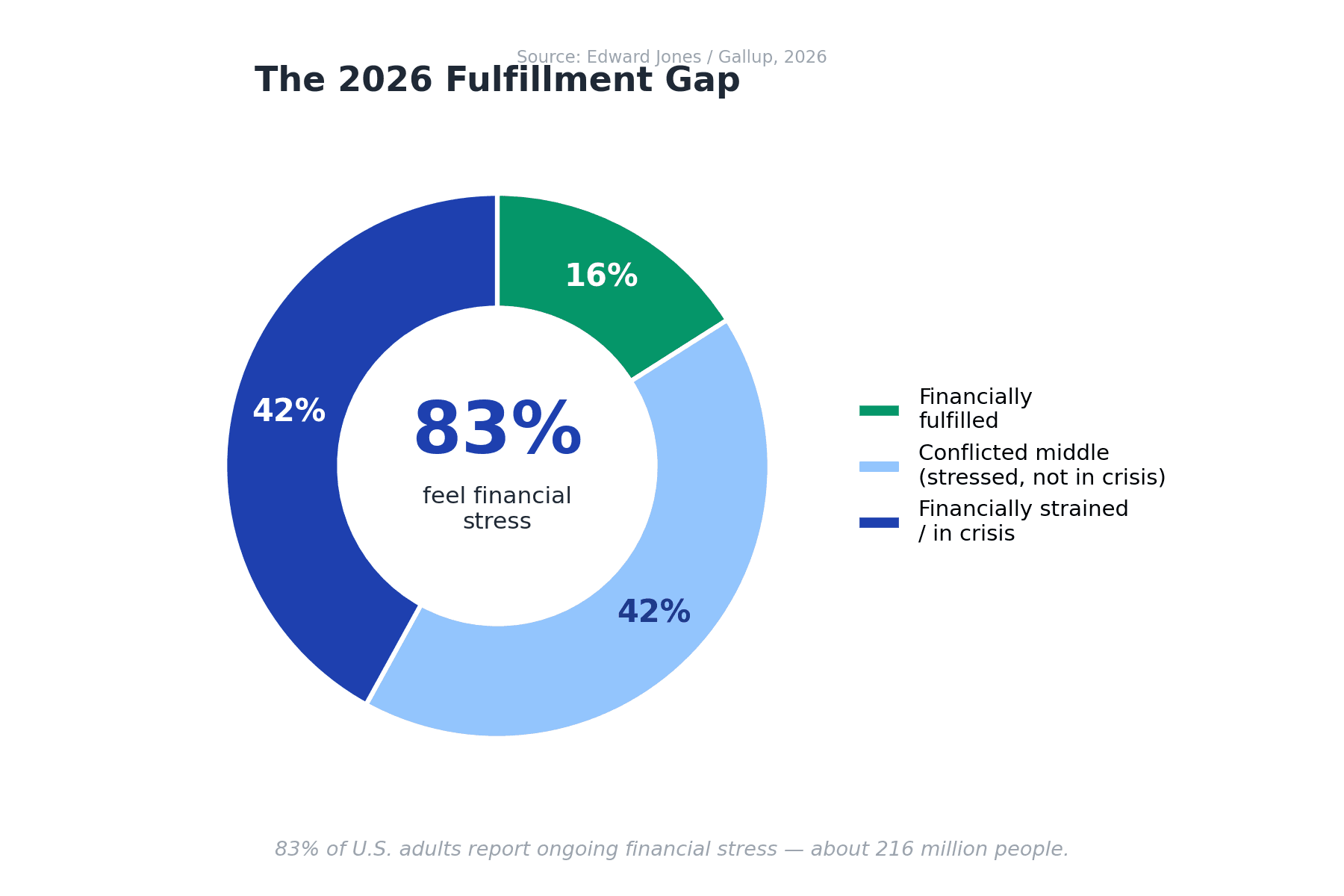

Sarah has money dysmorphia — a distorted perception of your own financial reality. And in 2026, she has a lot of company. A brand-new Edward Jones/Gallup study released June 2 found that only 16% of U.S. adults feel financially fulfilled, while 83% — roughly 216 million people — report ongoing financial stress, strain, or uncertainty. The startling part: a huge share of that strain is showing up in people whose numbers look perfectly healthy.

This is the article I wish Sarah had read before her midnight scroll. We are going to define what money dysmorphia actually is, prove with data that most people feeling broke are richer than they think, map exactly how social media rewires the perception, count the real-dollar damage, and then walk through a step-by-step reality-check protocol that replaces the vibe with your actual numbers.

What Is Money Dysmorphia? The 2026 Phenomenon Hiding in Plain Sight

Let's start with a clear definition, because the term gets thrown around loosely.

Money dysmorphia is a distorted view of your own finances — a persistent gap between how you feel about your money and what your money actually is. The name borrows from body dysmorphia, where a person sees a reflection that does not match reality. With money, the mirror is your bank balance, and the distortion runs the same way: you can be objectively fine and still see "broke" every time you look.

Intuit Credit Karma data puts the prevalence at about 29% of all Americans, and it skews young: 43% of Gen Z and 41% of millennials report it, versus 25% of Gen X and just 14% of people 59 and older. So if you are in your twenties or thirties and you feel perpetually behind, you are not unusual. You are the statistical center of this thing.

Here is the line I want you to hold onto, from Gen Z money coach Nia Baiyeroju: "Financial security is an emotion before it's ever a number. If you grew up watching your parents stress about bills, your nervous system doesn't automatically update when your bank account does."

That is the whole phenomenon in two sentences.

The crucial distinction: money dysmorphia is not the same as genuine financial hardship. If you are choosing between rent and groceries, your stress is accurate and this article is not gaslighting you — real cost-of-living pressure is real, and we will come back to it. Money dysmorphia is specifically the gap between feeling and fact. It is the above-median saver who is convinced she is drowning. The whole game is closing that gap, and the first step is admitting it might exist.

The Edward Jones managing partner Penny Pennington framed the 2026 finding bluntly: "Financial stress isn't limited to people in crisis — it's affecting millions who appear stable but don't feel secure or fulfilled." Her study found that 51% of stressed Americans land in a "conflicted middle" — not in crisis, paying every bill on time, contributing to retirement, yet still saying finances "often" or "always" control their lives. That conflicted-middle everyman is the most relatable archetype in personal finance right now, and there is a decent chance it is you.

The Numbers Say You're Fine: Why Today's Young Adults Are Richer Than They Feel

Now for the part nobody posts about.

If you feel broke despite a steady income, the odds are good that you are not just fine — you are ahead of the generations who came before you at the same age. The data is genuinely surprising.

The average 25-year-old today earns more than 50% more than baby boomers did at the same age, with household income above $40,000. Gen Z at ages 25 to 26 has a higher median inflation-adjusted income than even millennials did at that age. And millennials born in 1989 earned a cumulative median of $446,570 across ages 25–34 (in 2023 dollars) — versus $417,700 for Gen X and $362,330 for boomers over the same stretch of life. You out-earned your parents at your age. You just never see that number on your feed.

It is not just one stat, either — the whole "our parents had it easier" comparison gets murkier the closer you look. Starting salaries are up across fields, not only in tech (numbers are illustrative — focus on the ratios):

| Field | Starting salary, 2000 | Starting salary, 2024 |

|---|---|---|

| Software/IT | ~$40,000 | $80,000–$120,000 |

| Finance/Accounting | ~$35,000 | $55,000–$75,000 |

| Marketing | ~$28,000 | $50,000–$65,000 |

| Engineering | ~$45,000 | $70,000–$90,000 |

And the classic parental wealth engine — buy a house as early as possible, pay it off over 30 years — has a modern equivalent that performs in the same league. A $120,000 home bought in 2000 is worth roughly $400,000–$500,000 today; the same decades of consistent index investing land in a similar range or higher. The modern version usually means not buying in a trophy coastal market, then investing the gap (numbers are illustrative — focus on the ratios):

| Option | Home price | Monthly mortgage | Left over to invest |

|---|---|---|---|

| Condo in San Francisco | $1,300,000 | ~$8,200/mo | $0 |

| House in Austin suburbs | $450,000 | ~$2,800/mo | $1,500/mo |

| House in Raleigh-Durham | $380,000 | ~$2,400/mo | $2,000/mo |

Invest that $2,000/month difference at historical S&P 500 returns for 25 years and it compounds to roughly $1.5 million — a house plus a portfolio, where your parents had only the house. The point for your perception: a real wealth path exists for your generation. It just doesn't look like the one you were raised to measure yourself against, which is exactly why your internal benchmark keeps reporting "behind."

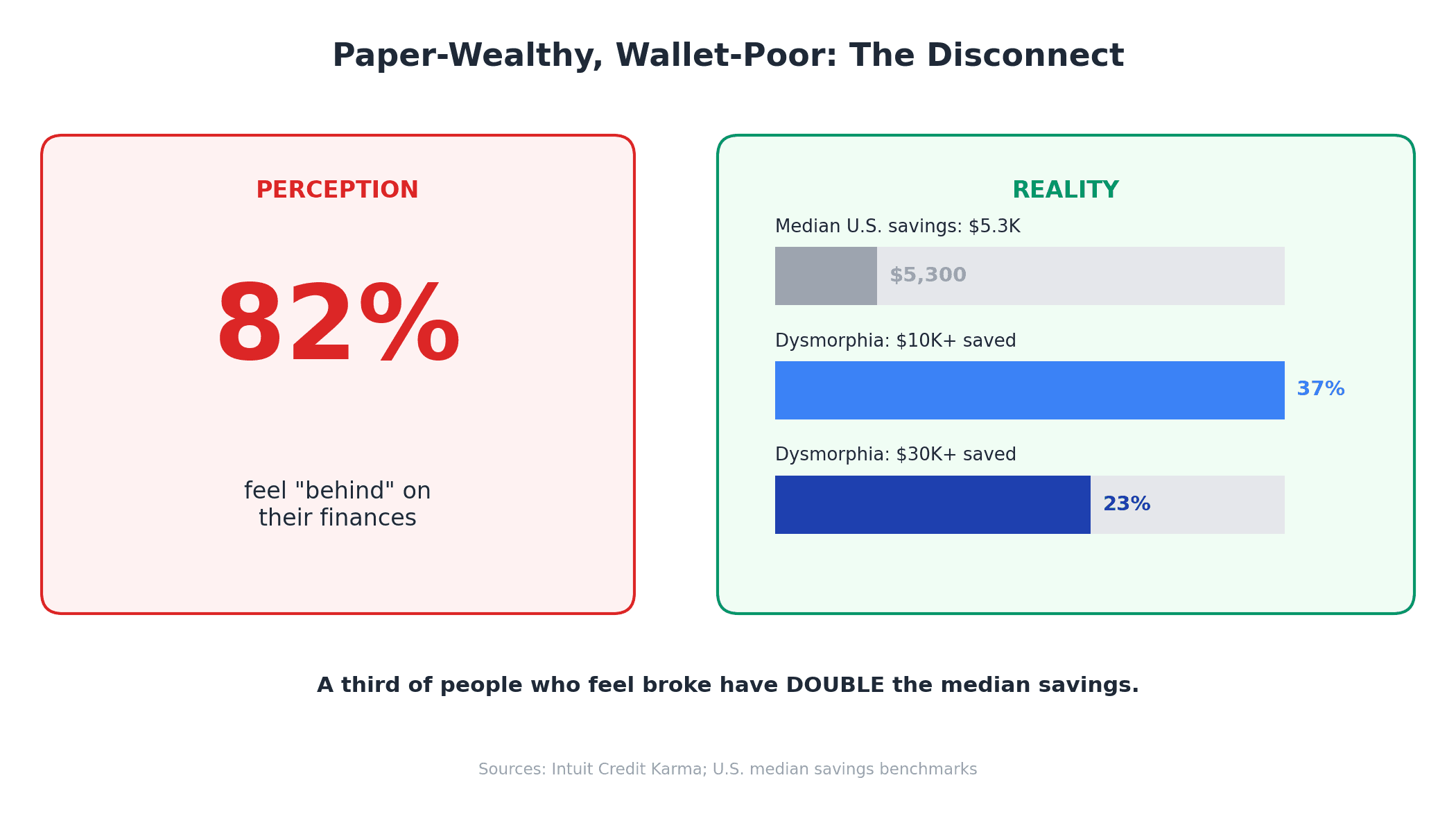

The savings picture tells the same story. Among people with money dysmorphia, 37% have more than $10,000 saved and 23% have more than $30,000 — all while the median American savings sits around $5,300. Read that again. A third of the people who feel broke are sitting on double the median, and nearly a quarter have six times it.

Yet 82% of people with money dysmorphia say they feel "behind" on their finances, compared to just 29% of people without it. The feeling and the facts have completely decoupled.

This is what the Washington Post called paper-wealthy, wallet-poor: balance sheets that quietly look fine attached to people who are convinced they are failing.

One honest caveat, because I will not sell you a fairy tale. Younger generations genuinely pay more in rent, even adjusting for age, and housing, healthcare, and childcare are real headwinds that did not weigh as heavily on prior generations. The argument here is not "all your stress is imaginary." It is "your perception is very likely running ahead of your reality" — and the only way to know which is true for you is to look at the actual numbers, which we will do in a minute.

The Comparison Machine: How RichTok and Social Media Rewire Your Money Brain

So if you are objectively doing well, where does the broke feeling come from? Mostly from a phone in your hand for several hours a day.

Social media is a comparison machine, and money is its most efficient fuel. Your feed is a curated highlight reel — Tulum trips, first-class boarding passes, kitchen renovations, a friend's "we bought a house!" carousel. None of it shows the financing, the parental help, the credit-card balance, or the burnout behind it. But your brain does not file it as "edited content." It files it as the new normal, and quietly resets your reference point for what enough looks like.

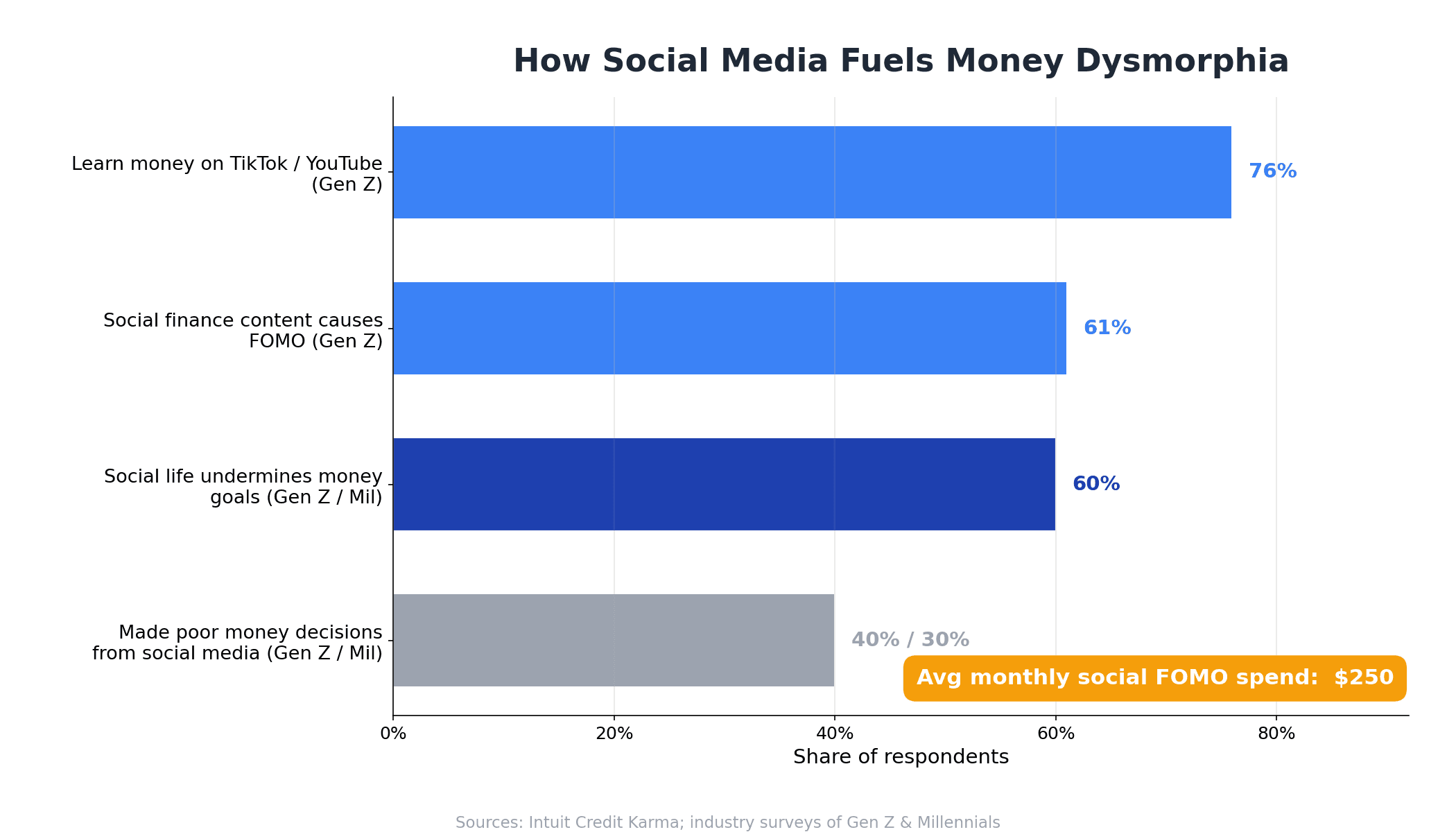

The numbers on this are stark. Start with where the financial advice even comes from: roughly 76% of Gen Z now learn about money on TikTok and YouTube — a feed tuned for watch-time, not accuracy. Nearly 60% of millennials and Gen Z believe their social lives actively undermine their money goals, with social FOMO spending averaging about $250 a month. 61% of Gen Z say learning about personal finance on social media contributes to their FOMO. And 40% of Gen Z plus 30% of millennials admit they have made poor financial decisions based on what they saw online.

Here is the mechanism, named plainly. Availability bias: you have seen seventeen posts of people your age buying homes, so your brain concludes everyone your age is buying homes and you are the only one falling behind. Social proof: thousands of likes feel like proof the lifestyle is real and normal. Stack those on top of a curated, filtered, financed highlight reel, and you get a perpetual, low-grade sense that you are losing a race nobody told you the rules to.

This is exactly why the anti-influence movement has been growing — a quiet revolt against performative FinTok that treats your attention as the product and your insecurity as the hook. And it is why even high earners feel broke. Roughly 20% of households earning over $150,000 spend more than 95% of their income on necessities, and a jaw-dropping 40% of people earning over $500,000 live paycheck to paycheck — often a higher rate than those earning $50K–$100K. More income just raises the bar of what your feed tells you "normal" should cost. The comparison machine does not care how much you make. It always finds someone above you.

For a closer look at the specific FinTok myths that make the inadequacy feel worse — especially the ones aimed at women — I broke three of them down in FinTok Money Myths: 3 Mistakes Gen Z Women Make.

The Real Cost: How a Distorted Self-Image Drains Your Wallet

You might be tempted to file all this under "just a feelings problem." It is not. Distorted perception costs real money, and the data on this is unambiguous.

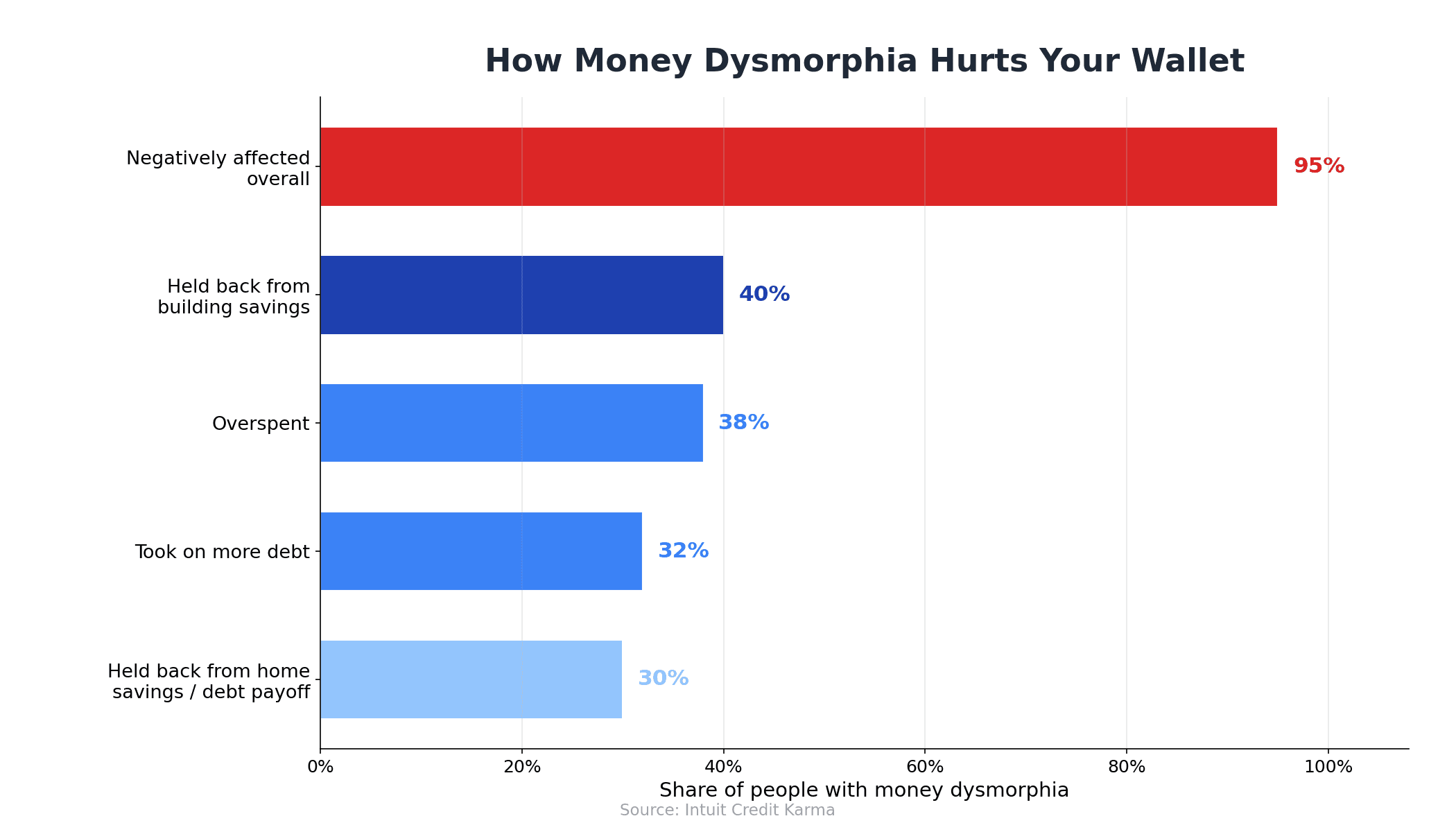

95% of people with money dysmorphia say it negatively impacts their finances. That is not a typo. Ninety-five percent. The damage breaks down like this:

- 40% say it held them back from building savings

- 38% overspent because of it

- 32% took on more debt

- 30% say it kept them from saving for a home or paying down debt

How does a feeling drain a bank account? Two opposite ways, and both sabotage your future.

Revenge spending. "I feel broke anyway, so what's the point" becomes a $300 impulse buy, a too-expensive vacation you charged, a lifestyle that creeps up to match the feed. The distortion convinces you that you are already losing, so you stop playing carefully — which actually makes you lose.

Paralysis and hoarding. The opposite reaction. You are so afraid of being broke that you refuse to spend on anything, refuse to invest because the market feels scary, and let cash sit and decay to inflation while you white-knuckle a savings balance you will not touch. Financial therapist Lindsay Bryan-Podvin describes it perfectly: "the safety of having that money gets completely canceled out by the fear of actually touching it."

Either way, the cost compounds. Remember that $250/month average of FOMO spending? Redirect it into investments at a 7% return for 30 years and it grows to roughly $283,000. That is the price tag on a distorted perception — a quarter-million dollars and a delayed retirement, paid in installments of feelings.

This is also where chronic financial anxiety bleeds into the rest of your life. The low-grade dread that "I'm always behind" is a known driver of burnout, and burnout has its own measurable hit on savings rates and earning power — I dug into that loop in Quiet Burnout: The Hidden Financial Impact.

5 Signs You Have Money Dysmorphia (And When It's Actually a Real Problem)

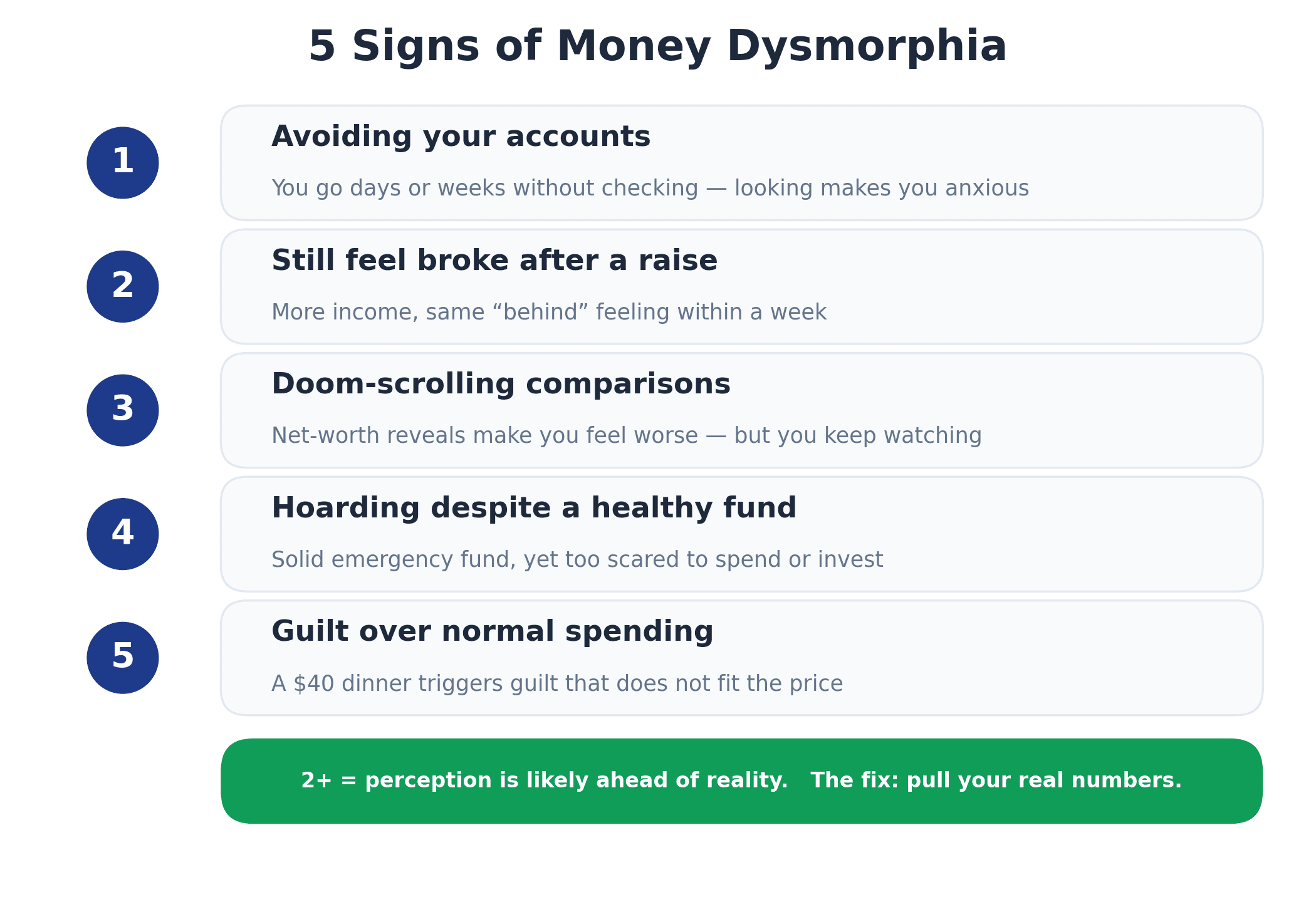

So how do you know if you have it? Here is the diagnostic checklist. If two or more of these sound like you, perception is probably running ahead of reality.

1. You avoid your own accounts. You go days or weeks without checking your balance or your brokerage because looking makes you anxious — even though nothing is actually wrong in there. Avoidance is the tell. People in real trouble usually know their numbers cold.

2. You felt broke after a raise. Your income went up and the relief lasted about a week before "behind" came back. If more money never moves the feeling, the feeling is not about money.

3. You doom-scroll comparison content. You watch net-worth reveals, "day in my life as a six-figure earner" videos, and house tours, and you feel worse every time but keep watching. The scroll is the wound and the salt.

4. You hoard out of fear despite a healthy cushion. You have a solid emergency fund and you still cannot bring yourself to spend on a vacation you have earned or invest money that is just sitting there. Bryan-Podvin's clients call this being "stuck in the loop."

5. You feel guilt over completely normal spending. A $40 dinner, a $15 streaming service, a reasonable gift — and a wave of guilt that does not match the size of the purchase.

Now the honest inverse — when feeling fine is the actual problem. Money dysmorphia is a gap between feeling and fact, and it runs both directions. Meet Jake, 34, a software engineer with a $165,000 household income. On paper he is a top-15% earner, and he tells himself "I make plenty, I'm fine." In reality he has a big mortgage, a leased EV, lifestyle creep, and a savings rate near zero — he is one of those $150K+ households spending 95% of income on necessities. His over-optimism is hiding a genuine cash-flow problem. That is dysmorphia too, just in the flattering direction.

The point: do not trust the feeling in either direction. The only way to tell perception from reality is to pull the actual numbers. Which brings us to the fix.

The Reality-Check Protocol: Replace Vibes With Your Actual Numbers

Every financial therapist I read while researching this prescribed the same core medicine: ground the feeling in facts. Stop arguing with your anxiety and start measuring. Here is the five-step protocol, built directly from what the experts recommend.

Step 1 — Pull your true number. Calculate your real net worth (everything you own minus everything you owe) and your real savings rate (the percentage of income you actually keep). Write it down — the physical act of seeing it on paper is the single most-cited therapist intervention, because it forces the vibe to meet the math. Then schedule a fixed monthly review so checking your accounts becomes a calm routine instead of a panic event. If you have been avoiding your accounts entirely, the gentlest on-ramp is How to Start a Budget — start by simply seeing where the money goes.

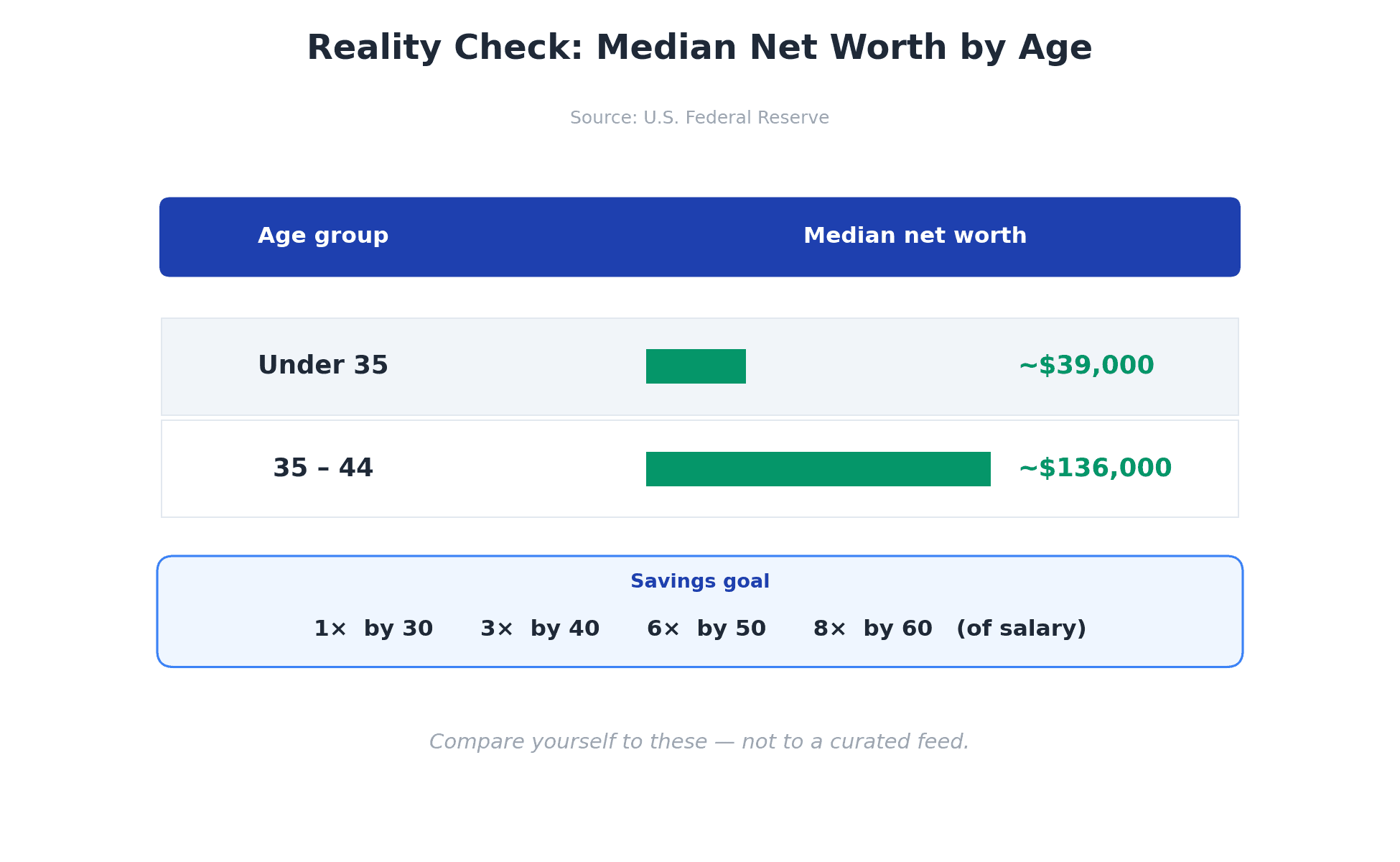

Step 2 — Benchmark against reality, not influencers. Compare your number to objective age medians, not your feed. For context: median net worth is around $39,000 for people under 35 and $136,000 for ages 35–44, and a common savings guidepost is 1× your salary saved by 30, 3× by 40, 6× by 50, and 8× by 60. Pull your real position against real medians here: Net Worth by Age: Where Do You Actually Stand?. A lot of readers discover, with genuine shock, that they are at or above median.

Step 3 — Mute the comparison machine. Unfollow or mute every account that makes you feel bad about money. Bryan-Podvin calls this "such a simple way to take back control" — you stop measuring your daily life against someone else's filtered highlight reel and get the breathing room to focus on your own trajectory. Replace the RichTok inputs with your own dashboard.

Step 4 — Define "enough" and set ONE forward target. Baiyeroju is sharp on this: defining what "enough" means for you "is not a math problem, it's a clarity problem. More money doesn't fix it — understanding what you're building toward does." Pick one concrete goal — a six-month emergency fund, a Coast FIRE number, a down payment — instead of chasing a vague, infinite "more." A target you can name is a target you can hit, and hitting it feels like progress in a way that out-earning your feed never will.

Step 5 — Practice financial gratitude and values-based spending. Here is the most hopeful stat in the entire Edward Jones study: gratitude is the most-felt financial emotion, with 63% of people feeling it often or always — nearly double the rate of joy, peace, or contentment. Gratitude correlates strongly with fulfillment. So give yourself permission to spend on what actually matters. Bryan-Podvin teaches an affirmation for it: "I've got a healthy savings cushion. It's safe for me to spend this money, and it's important for me to have a nice time with my friends." Spend on experiences, relationships, and generosity — the things fulfilled people consistently report bring them the most joy.

The reason this protocol works is that steps 1 and 2 are the cure, automated. A tool that surfaces your real net worth, your savings rate, and your forward trajectory does exactly what the therapists prescribe — it replaces the vibe with data. That is the entire idea behind the MFFT net-worth tracker: a calm, private place to see the real number going up, so your perception finally has somewhere accurate to look.

From Anxiety to Agency: Building a Money Life That Feels as Good as It Looks

Here is what the whole article comes down to.

Money dysmorphia is, at its core, a perception problem — and that means it is fixable without earning a single extra dollar. Financial fulfillment is not a bigger number. The Edward Jones data proves it: only 16% of people feel fulfilled, and that group is not simply the richest — they are the ones whose perception and reality are aligned and who have a clear plan. Among financially fulfilled adults, 83% describe themselves as "thriving" and just 2% say finances control their lives. Among the stressed, those figures flip to 18% and 52%. The difference is not the size of the account. It is the gap between how you feel and what is actually true — and whether you have a plan you believe in.

So close the gap. Pull your true number. Benchmark against real medians instead of influencers. Mute the feed that resets your sense of normal. Name one goal and aim at it. Practice gratitude for the position you have actually built — which, if you have read this far, is very likely better than you have been giving yourself credit for.

You may already be ahead. But you will never feel ahead until you can see it. Replace the curated feed with your own objective numbers, and the broke feeling loses the only thing it was ever running on: your imagination.

The fastest way to do that is to look. Track your real net worth, savings rate, and trajectory with MFFT — no signup gate, no upsell. Watch the real number, not the feed.

If you do the reality check and discover you were ahead the whole time, email me at dennis.vymer@myfinancialfreedomtracker.com and tell me what the gap was. And if you discover you are a "Jake" — that the optimism was hiding a real problem — good. Either way you've proved the same point: the feeling was never the truth, the numbers are. Whichever direction your gap runs, the fix is identical — stop guessing and look. That habit, repeated every month, is the whole game.

So go pull your real number. It's almost certainly trying to tell you something kinder, or more honest, than the feeling ever did.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyRent vs Buy in 2026: I Ran the Numbers, Kept Renting, and Invested the Difference

My uncle swears renting is throwing money away. So I built the rent vs buy 2026 model: renting wins in all 50 metros, but only if you invest the difference.

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.