Sandwich Generation 2026: A 4-Bucket Plan to Keep Saving

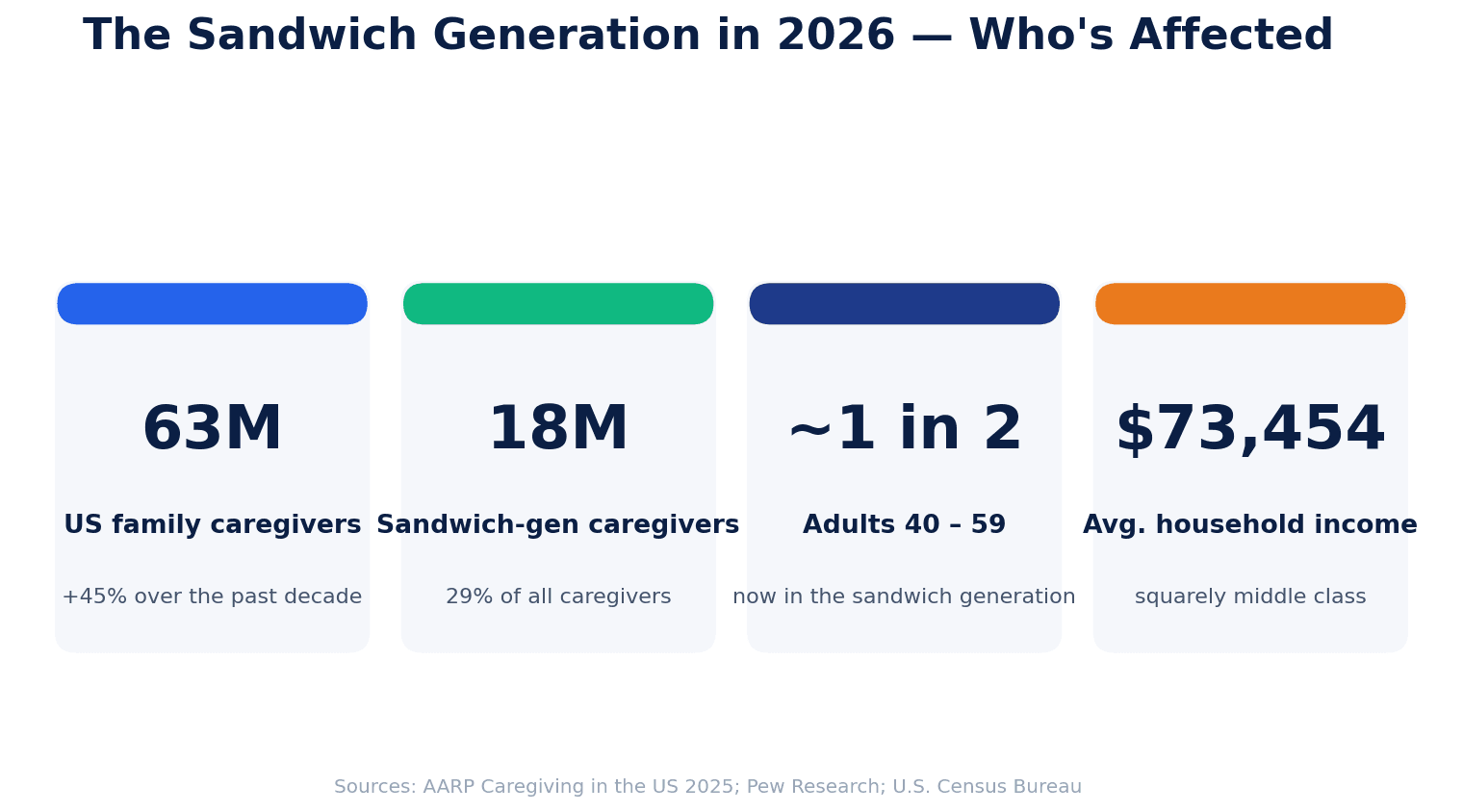

TL;DR: 63 million Americans are family caregivers and 29% are sandwich-generation — raising kids while supporting aging parents. The average cost is brutal: roughly $21,000 a year in lost income plus $10,000 in direct caregiving expenses, on a typical $73,454 household income. The four-bucket framework funds your retirement floor first, then kids' essentials, then a visible parent-care budget, then your own emergency reserve — in that order, because nobody will lend you money for retirement.

Marcus is thirty-eight. He has two kids, a mortgage, and a mom who was just diagnosed with early-stage Alzheimer's.

Last year he cut his hours from forty to thirty-two so he could drive his mom to appointments. He paused his Roth contributions "just for a little while." He told his wife not to worry about it.

Eighteen months later, his retirement account hasn't grown. His credit card balance has. And the only thing he's certain about is that he's tired.

If any part of that story sounds familiar, you are not alone. You are part of a wave that's already 63 million people deep in the United States — and growing. Welcome to the sandwich generation in 2026.

This is the most honest financial planning conversation we can have right now: how do you protect your own future while two other generations need money from you, today?

What the Sandwich Generation Looks Like in 2026 (And Why It's Growing Fast)

The sandwich generation is the group of adults who are simultaneously raising children and helping support aging parents. Most of us picture this as a Gen X problem. In 2026, it's a millennial problem too.

A few numbers that explain why:

- The number of family caregivers in the U.S. has jumped to 63 million — a 45% increase over the past decade.

- 29% of those caregivers are sandwich-generation caregivers, supporting both kids and adults at the same time.

- Almost half of adults aged 40 to 59 are now in this group, according to Pew Research.

- The average sandwich-generation household income is $73,454 — squarely middle class, with caregiving costs that aren't.

Three forces are driving the growth. People are living longer (and needing more years of care). Couples are having kids later, so school-age children and aging parents now overlap in the same decade. And the cost of professional care — assisted living, in-home help, adult day programs — has outrun wage growth almost everywhere.

The result is that the sandwich generation isn't a tiny demographic anymore. It's a default life stage for working-age Americans.

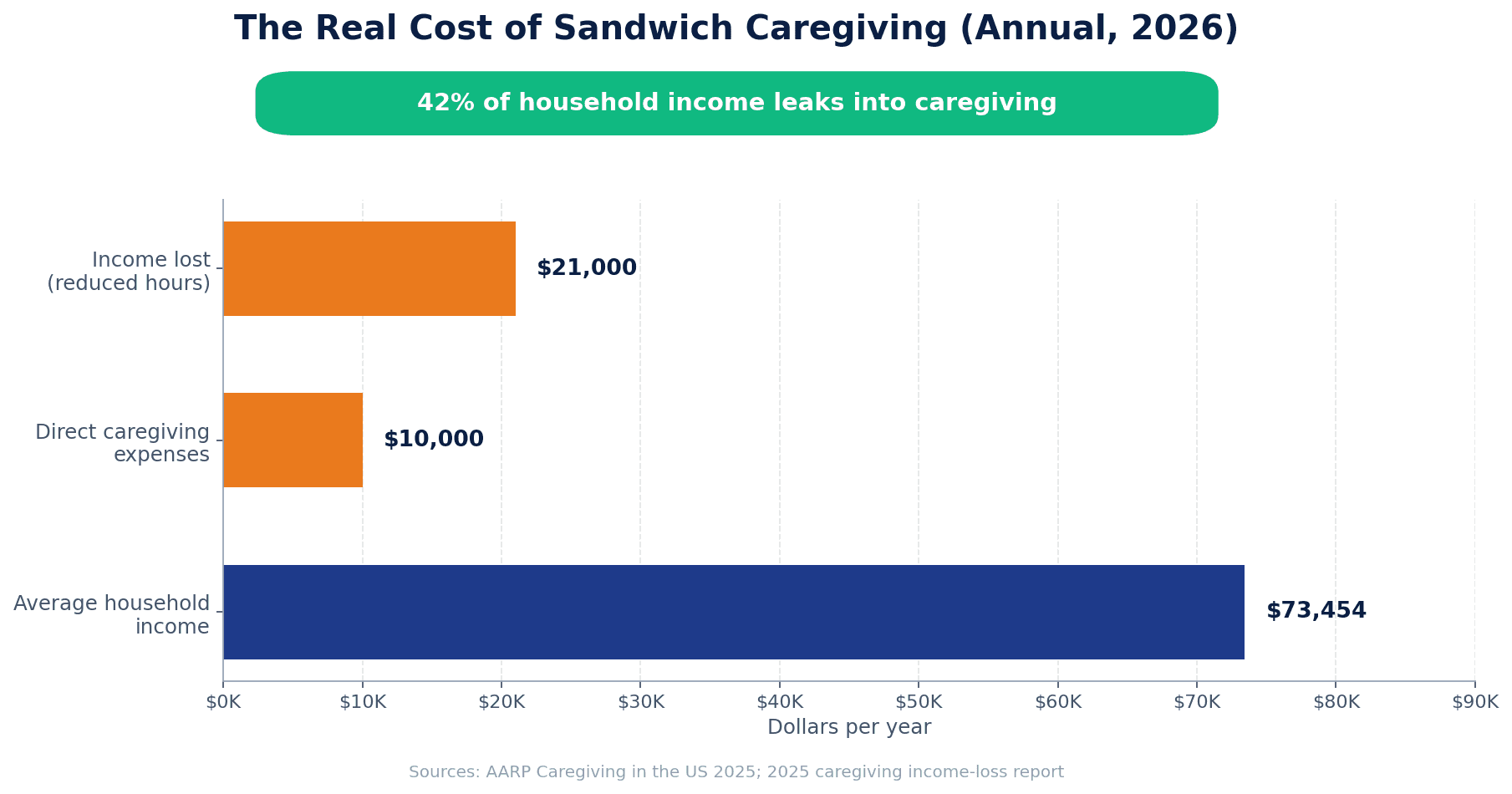

The Real Cost: $21,000 a Year, 50 Hours a Week, and a Retirement Quietly Slipping Away

Here's what the financial press almost never says clearly enough: caregiving doesn't just cost money — it costs time that could have been money. And the math is brutal.

A 2025 caregiving report found that sandwich-generation caregivers lose, on average, $21,000 per year in income because of reduced hours, missed promotions, and time taken off work. That's not the bill from the pharmacy. That's just the wages they didn't earn.

On top of that, AARP data shows the average sandwich caregiver spends roughly $10,000 a year in direct caregiving expenses — co-pays, transportation, equipment, in-home help, food, and a hundred small things nobody itemizes.

Add it together and you get a leak of about $31,000 a year on a $73,454 household income. That's 42% of household income disappearing into something most people don't even have a budget category for.

The downstream damage is what worries financial planners most. According to AARP's 2025 caregiving survey:

- 72% of sandwich caregivers have cut back on necessities like food and medical care, or pulled from retirement savings.

- About one-third have stopped saving entirely.

- 24% have exhausted personal short-term savings.

- 13% have tapped long-term savings, like 401(k) accounts or 529 college funds.

Meanwhile time is a different kind of cost. New York Life's Wealth Watch survey found sandwich caregivers spend an average of 50 hours per week caregiving — 22 hours for an elder, 28 for the kids — on top of full- or part-time work. After sleep, that leaves roughly four hours of daily life that doesn't belong to someone else.

When people talk about caregiver burnout, they usually mean emotional fatigue. The financial version of burnout is different. It's slower. It looks fine on Tuesday and shows up at age 65, when you discover you have $130,000 less in retirement than you would have had.

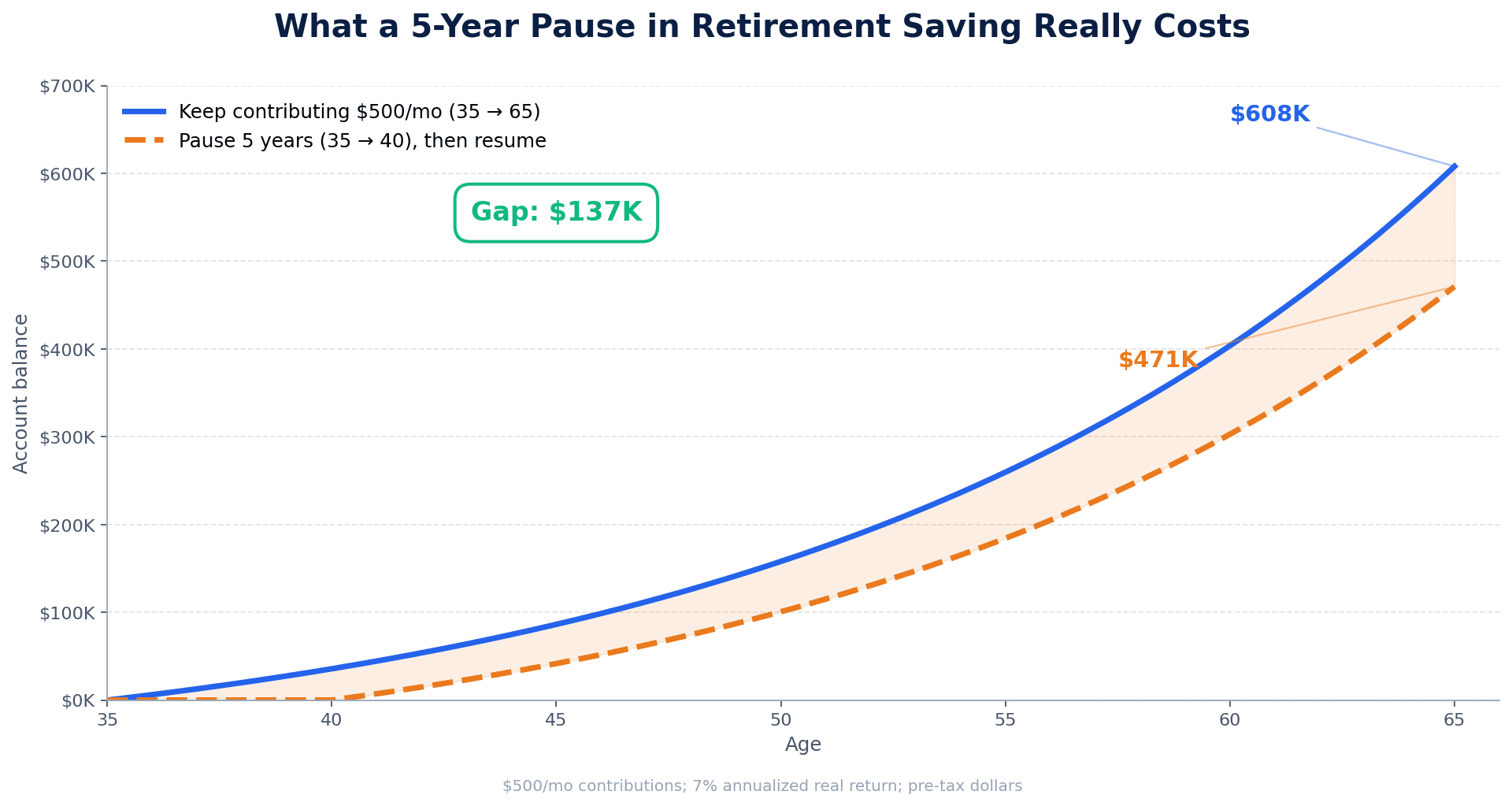

Why "I'll Catch Up Later" Doesn't Work for Retirement

A lot of sandwich caregivers tell themselves the same story Marcus did: I'll pause my retirement contributions for a year or two, then catch up when this is over.

The math doesn't agree.

Imagine someone contributing $500 a month to a Roth IRA from age 35 to 65, earning a 7% real return. That's roughly $608,000 at retirement. Now imagine they pause for five years — say, ages 35 to 40 — and resume normally afterward. End value drops to about $471,000.

That's a $137,000 gap for a five-year pause. Not a five-year delay in retirement. A five-year pause in contributions.

This is why most financial planners now use the airplane oxygen-mask framing for sandwich caregivers: secure your own retirement contributions first, even at a reduced level, before you reroute money toward your parents' care. Not because you love your parents less. Because the years of compound growth you can't recover are the most valuable thing on your balance sheet.

If you've never run the numbers on your own trajectory, our net worth at age guide will help you see how off-pace caregiving is actually pushing you. Most readers are surprised — sometimes encouragingly, sometimes not.

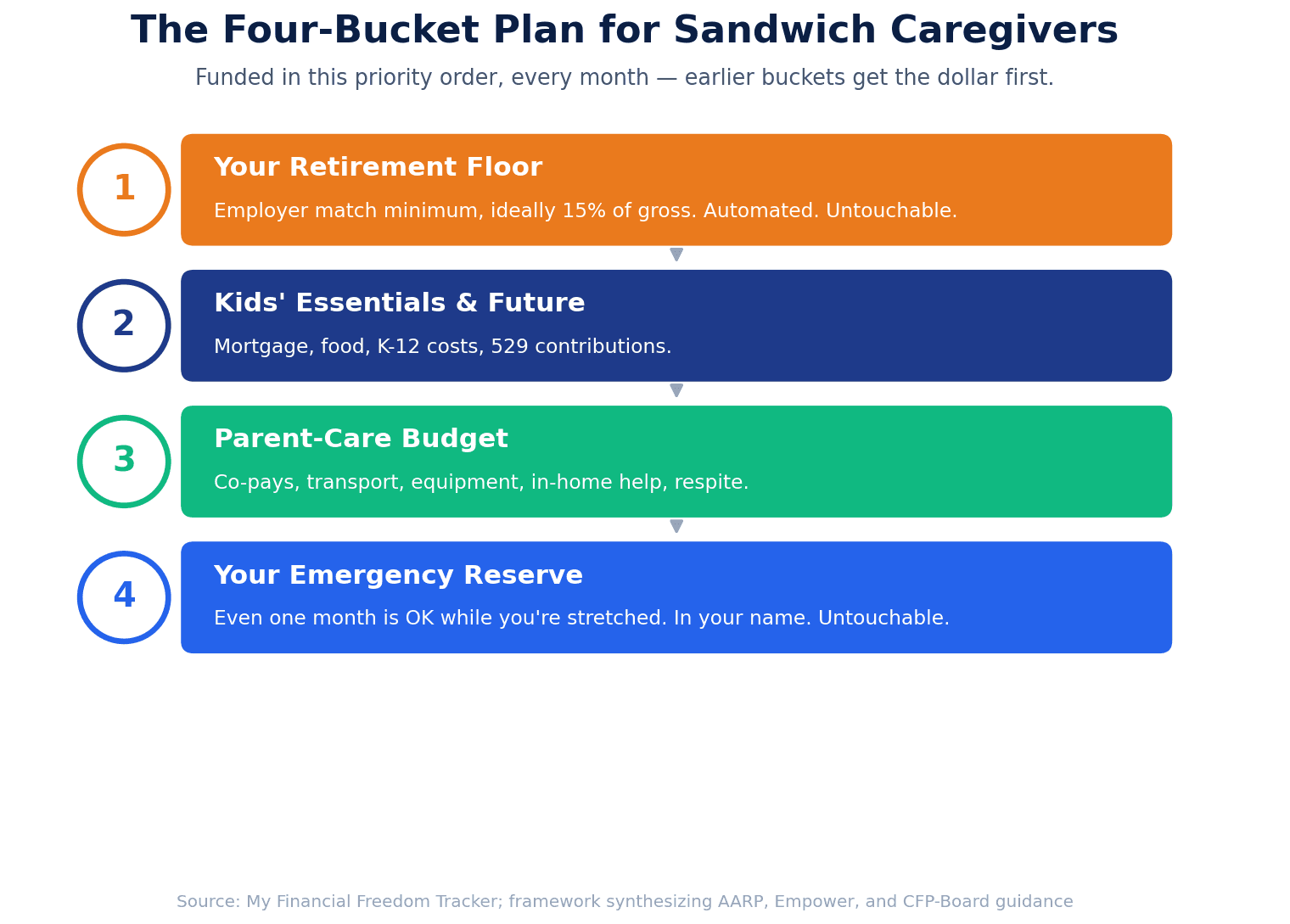

The Four-Bucket Framework: How to Protect Your Money When Everyone Needs It

Most sandwich-generation budgeting advice starts from "rebalance everything." That's not how exhausted humans actually behave. They protect what they have automated and let everything else drift.

So we use a different framework. Four buckets, in priority order. The earlier buckets get funded first, every month, no matter what.

Bucket 1 — Your retirement floor. This is non-negotiable. Whatever your minimum is — at least the full employer 401(k) match, ideally 15% of gross — keep it automated. Treat it like rent.

Bucket 2 — Your kids' essentials and future. Mortgage, food, K-12 costs, the 529 contribution if you have one. You already have this dialed in. Protect it.

Bucket 3 — The parent-care budget. This is the new category. Track it like any other bill: co-pays, durable medical equipment, transportation, respite care, in-home services, and eventually possibly part of a facility cost.

Bucket 4 — Your own emergency reserve. Smaller than the textbook six months — even one month is fine while you're stretched — but it has to exist. In your own name. Untouchable for daily expenses.

If your current budget doesn't have a third category for caregiving, that's almost certainly where the leak is hiding. The first thing to do is make it visible. Our budgeting setup guide walks through how to add a new category and connect it to your real bank activity.

Building a Caregiving Budget That Actually Works

A caregiving budget is different from a regular budget for one big reason: you're managing money across two households (yours and your parents'), and possibly across multiple siblings.

Here's a starting structure that holds up under pressure.

Track these as separate line items, not one big "elder care" category:

- Insurance co-pays and prescriptions

- Transportation (gas, rideshare, parking at appointments)

- In-home help (housekeeper, aide, respite care)

- Durable medical equipment (walker, lift chair, shower bench)

- Food and groceries delivered or shopped for parents

- Home modifications (grab bars, ramps)

- Care facility or adult day program contributions

- Legal and administrative (attorney fees, document copies, notary)

The point of separating them isn't bureaucratic. It's that caregiving costs aren't constant. Some categories grow steadily (medications). Some explode in a single month (a fall, a hospital discharge, a sudden need for in-home care). When they're separate, you can see the spike, and decide what to do.

Review this category weekly, not monthly. Caregiving expenses change too fast for a once-a-month check. A fifteen-minute Sunday-night look is enough.

Keep one parent-care account if siblings are contributing. A shared account or shared sheet, with a common scheme — equal shares, or pro-rated by income, or whatever your family agrees to — beats splitting receipts after the fact every time. Pro-rating by income is what most therapists and elder-law attorneys recommend, because it preserves long-term family relationships better than equal splits do.

The Hard Conversations: How to Talk to Parents and Siblings About Money

Most sandwich-generation financial pain isn't a math problem. It's a conversation problem.

There are two conversations you have to have eventually. Better to start now, while it's still calm.

Conversation 1: With your parents, about their finances.

You're not asking for a bank statement. You're trying to learn three things:

- Do they have long-term care insurance, and if so, what's covered?

- Do they have a healthcare proxy and a power of attorney filed?

- What's the rough monthly gap between their income and their expenses today?

A useful opening line: "Mom, Dad — I'm not trying to take anything over. I just want to make sure that if something happens, I'm not figuring this out under stress at 2 a.m. Can we walk through what's already in place, and what's not?"

That sentence works because it puts you on their side. You're not auditing them. You're trying to spare everyone a crisis.

Conversation 2: With your siblings, about who pays for what.

If you have siblings and they're not currently chipping in, you need to fix that — gently but specifically. The math of parent care is too big to absorb solo, and resentment is the silent killer of family relationships during this stage of life.

Most fair frameworks use one of three structures: equal shares, pro-rated by income, or proximity-weighted (whoever lives closest contributes more time, others contribute more money). Pick the one your family can actually live with for the long haul, and write it down.

You're not enforcing a contract. You're avoiding the situation where, three years from now, one sibling silently feels like they paid for everything.

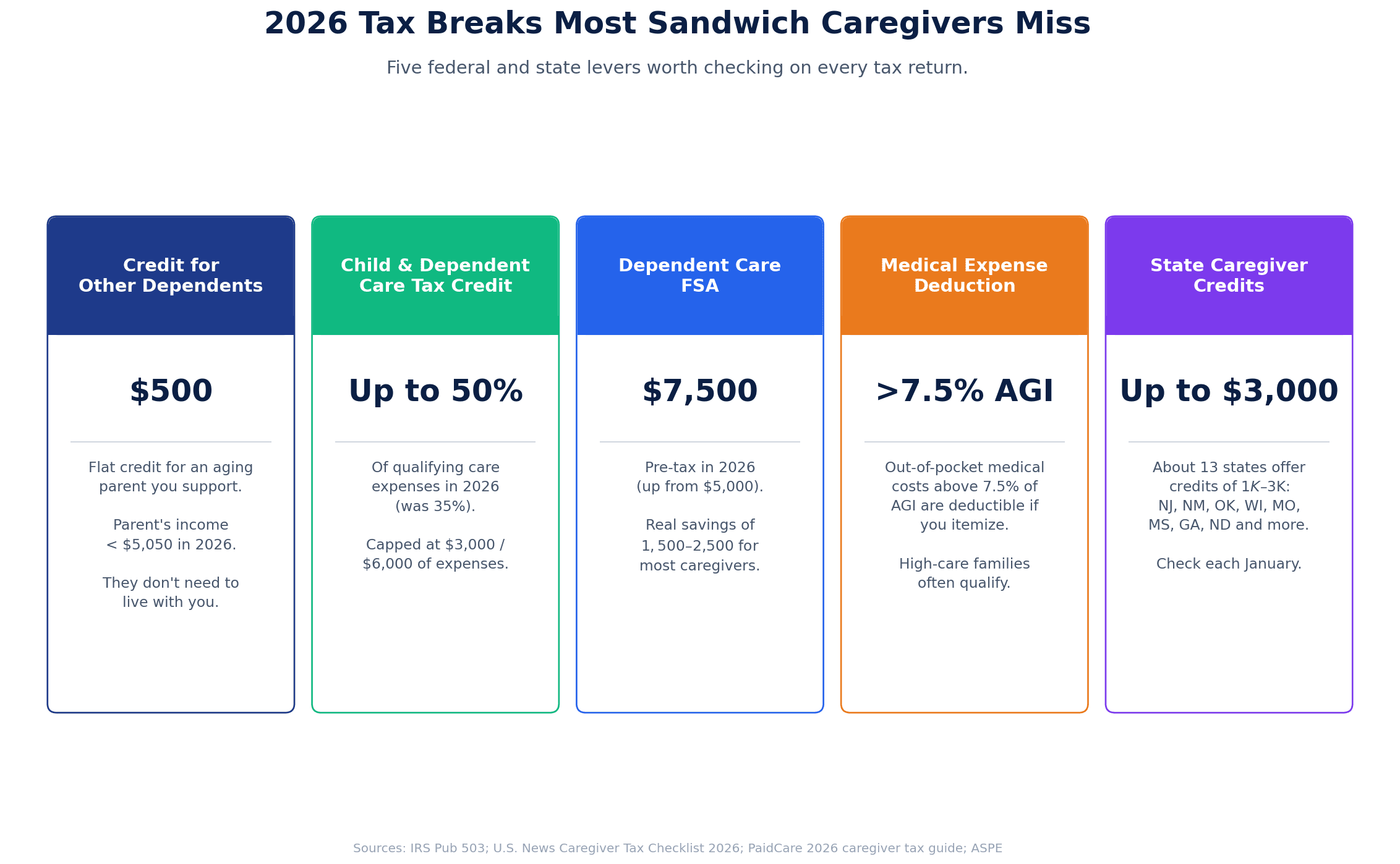

Tax Breaks Most Sandwich Caregivers Miss

The biggest invisible saving most sandwich caregivers can claim is on their tax return. The 2026 rules are friendlier than they've been in years, but only if you know they exist.

Credit for Other Dependents — $500. A flat, nonrefundable credit if you can claim an aging parent as a dependent. To qualify, the parent's gross income must be under $5,050 in 2026 and you must provide more than half of their financial support. They don't have to live with you — many sandwich caregivers don't realize that.

Child and Dependent Care Tax Credit — up to 50% of qualifying expenses in 2026. This is the bigger lever. The CDCTC may reimburse up to 50% of qualifying expenses (it was 35%) — capped at $3,000 for one qualifying person or $6,000 for two or more. You can claim it for an aging parent who can't physically or mentally care for themselves while you work.

Dependent Care FSA — up to $7,500 pre-tax in 2026. A real bump from the previous $5,000 limit. If your employer offers one, this is one of the highest-return moves on a sandwich-caregiver's tax form. The savings depend on your bracket, but most caregivers see $1,500 to $2,500 in real money.

Medical expense deduction. Out-of-pocket medical expenses that exceed 7.5% of your AGI are deductible if you itemize. For families spending heavily on a parent's care, this often crosses the threshold without you realizing it.

State-level caregiver credits. About 13 states have their own credits, generally $1,000 to $3,000, including New Jersey, New Mexico, Oklahoma, Wisconsin, Missouri, Mississippi, Georgia, and North Dakota. Check your state's department of revenue site each January.

These aren't loopholes. They're benefits that exist because Congress and state legislatures have started, slowly, to recognize that family caregivers are doing work that would otherwise fall to the public system.

Your Sandwich Generation Survival Checklist (Use This Quarterly)

Once a quarter — pick a date, put it on the calendar, do not skip it — walk through this list. It takes about thirty minutes.

- Confirm your retirement contributions are still automated. Open the brokerage. Verify the dollar amount.

- Run a net-worth check. Is the line going up, flat, or down? If down, by how much, and is it recoverable?

- Review the parent-care category in your budget. Are siblings contributing on schedule?

- Update beneficiaries on your accounts (401(k), IRA, life insurance, HSA). Most sandwich caregivers haven't touched these since they got married.

- Verify the healthcare proxy and power of attorney for both parents are still valid and findable.

- Schedule one money meeting with your spouse or partner. Twenty minutes. Calendar invite. Just the two of you.

- Once a year: actually file every tax document required to claim the dependent care credits. Most caregivers leave a few hundred dollars on the table by missing a single form.

If your emergency reserve has dropped during the quarter, that's the most important number on this list. It's also the one that, in our experience, predicts whether someone gets through this stage of life in good financial shape. For more on rebuilding an emergency fund under pressure, see our deeper take on the emergency fund crisis in 2026.

If you're 50 or older, this is also the year to double-check the new 2026 retirement contribution rules — the catch-up rules changed, and most sandwich caregivers in that age bracket haven't updated their plans.

You're Not Failing — You're Carrying Two Generations. Here's How to Carry Yours Too.

If you're reading this with a knot in your stomach, take a breath. You're not behind because you did something wrong. You're behind because you're doing two jobs at once and one of them is invisible.

Here's the part most articles won't say out loud: you are allowed to plan for your own future while you take care of everyone else's. In fact, you have to. There's no version of this where ignoring your retirement helps your kids or your parents.

Three things make the difference for sandwich-generation households I see come through the other side intact:

- They protect a tiny floor of automated saving every month, no matter what. Even $200. Compound interest doesn't care about how busy you are.

- They make caregiving costs visible. They put it in the budget, in the dashboard, on the family group chat — wherever they're already looking.

- They have one ugly, awkward family conversation early. Not the perfect one. Just the honest one.

If you want a place to start, open a tracker — ours included, but the brand doesn't matter — and just create a fourth budget category called "Caregiving." Then watch what happens for thirty days. Most readers find that simply naming the category recovers a few hundred dollars a month, because they finally see what's been quietly draining away.

You can keep being the person who shows up for everyone. You just have to be the person who shows up for yourself, too. Start small. Be honest. Stay in the game.

For everything else, our broader guide on taking control of your finances is a reasonable next step. The sandwich years end, eventually. The financial habits you build during them will carry you through everything that comes next.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.

Master Your Money

Master Your MoneyAI Scams Stole $21 Billion: How to Protect Yourself in 2026

AI scams hit a record $20.9B and could reach $40B by 2027. Scammers clone a loved one's voice from 3 seconds of audio. Here's the calm, free, afternoon-long defense playbook to protect your money in 2026.

Master Your Money

Master Your MoneyPrediction Markets: Why 69% of Polymarket Users Lose

69% of Polymarket users lose money and the top 1% take 76.5% of profits. The math, why Gen Z is targeted, and a 30-day reset plan.