Micro-Retirement Without Wrecking Your FIRE Plan (2026)

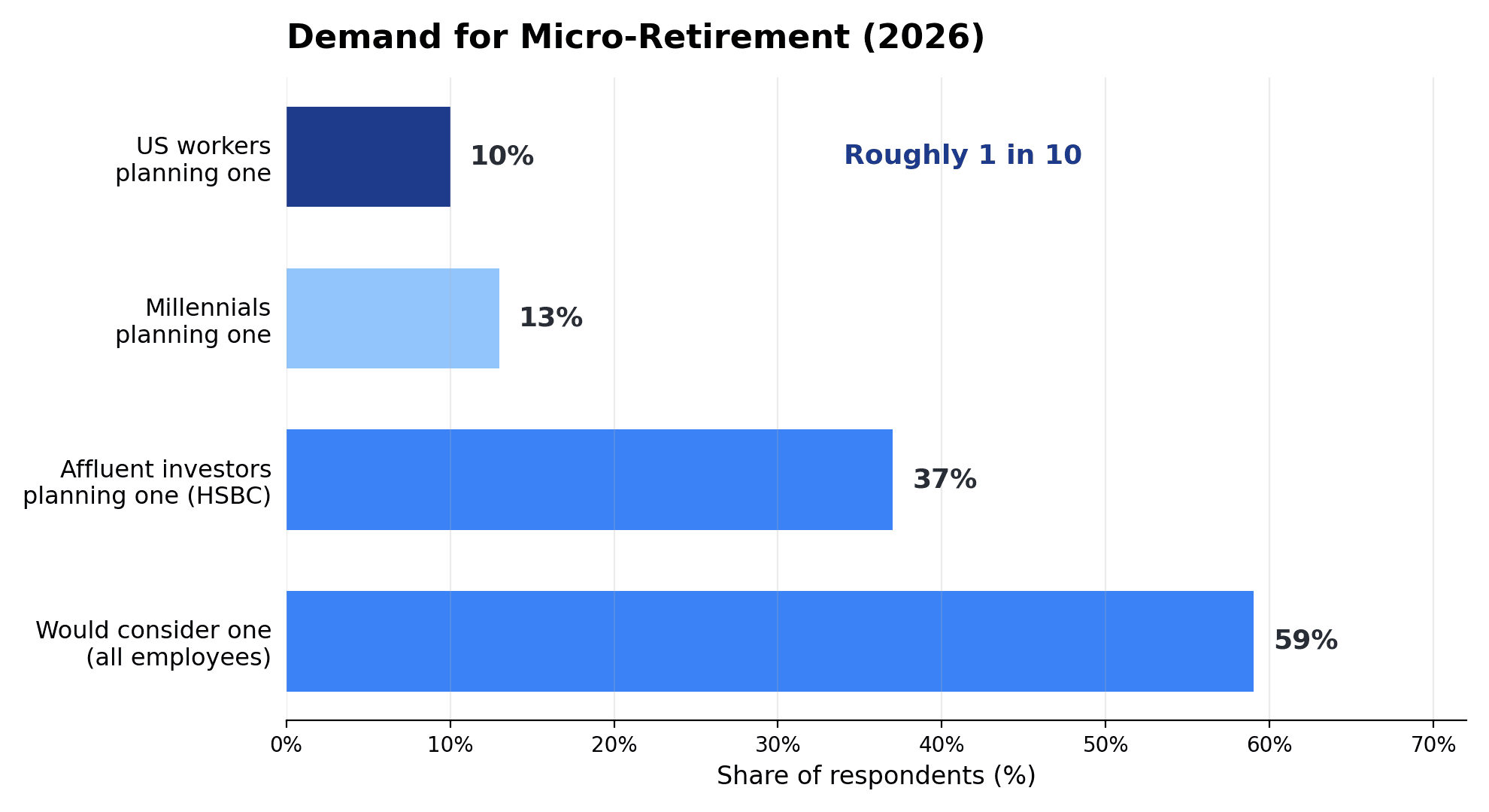

I got into this whole world at 18, and the version of freedom I'm building toward isn't quitting at the end — it's optionality along the way. My own plan is unglamorous: contribute hard until 40, then let compounding do the heavy lifting into my 50s, partly because of my kids. So a micro-retirement — taking a slice of that freedom now, mid-career, then going back to work — landed differently for me than I expected. Here's the stat that made me pay attention: about 1 in 10 US workers planned to take one in 2025, stepping away for months in their 30s or 40s, then coming back. And the part nobody likes to print: financial planners find that people who go in underfunded cut the break short 82% of the time, often by raiding the exact accounts meant to carry them to financial independence.

A micro-retirement is either the smartest "buy back your time" move of your decade or a quiet wrecking ball aimed at your FIRE plan — and the difference is whether you fund the gap deliberately or impulsively. Done with math, a mid-career break gives back a year of your life now and leaves your long-term freedom intact. I'll give you the mechanics most coverage skips: how to size a dedicated break fund, what the break actually costs, a 12-to-18-month funding runway, how to protect your net worth, and a readiness check.

Key takeaways

- A micro-retirement is a self-funded 6-month-to-2-year break taken mid-career — closer to a FIRE rehearsal than a vacation.

- Fund it from a dedicated break fund, completely separate from your emergency fund: at least 12 months of expenses plus a 20% buffer.

- The real cost is three layers — living expenses, lost salary, and the silent one: lost 401(k) contributions, employer match, and compounding.

- Never raid your 401(k) or IRA. If that's the only way to afford the break, the answer is "wait and save more," not "do it anyway."

- Building the fund is usually a 12-to-18-month project — and re-entry penalties are largely avoidable with preparation.

What a Micro-Retirement Actually Is (and Why 2026 Is Its Breakout Year)

A micro-retirement is an intentional, repeatable break from work of roughly six months to two years, taken mid-career rather than at the end of it: you take a slice of retirement now, go back to work, then maybe do it again a decade later. Some call it a mini-retirement, an adult gap year, or a multi-retirement.

This is not a vacation: it's long enough that you must solve for income, health coverage, and re-entry — which is why it needs a budget, not just a packing list.

Why is 2026 its breakout year? Burnout, for one: US employee engagement just hit a 10-year low of 31%, and Deloitte found 36% of Gen Z feel exhausted all or most of the time. And a rejection of the "one retirement, at the very end" model — people watched their parents grind 40 years to enjoy freedom only when their knees gave out, and decided to front-load some of it.

The numbers confirm the momentum: beyond that 1-in-10 figure, 13% of millennials are planning one and 59% of all employees would consider it. And it isn't only younger workers — HSBC's 2025 study found 37% of affluent US investors plan a mini-retirement, ideal first-break age around 46, while Gusto watched the share of workers on sabbatical roughly double between 2019 and 2024.

A micro-retirement isn't quitting on your future. Done right, it's a planned, partially-funded preview of the freedom you're saving toward — taken while you're young enough to enjoy it.

That "freedom in installments" idea is the same non-linear model I walked through in Gen Z Retirement Math: Start at 22, Semi-Retire by 45-50. A micro-retirement is one tool in that kit — and you need to know which one you're holding.

Micro-Retirement vs FIRE, Coast FIRE, and a Sabbatical: Which One Are You Really Doing?

People use these terms interchangeably, and that's where money mistakes start. FIRE (Financial Independence, Retire Early) is the destination: save roughly 25x your annual expenses, then live off withdrawals — traditionally ~4% a year — possibly forever. A micro-retirement is temporary and partially funded: you spend down a dedicated pot of cash for a fixed window, then return to a paycheck — the money only has to last the break.

The cleanest framing: a micro-retirement is a FIRE rehearsal you can test-drive. You learn what unstructured time feels like, whether you get restless by month three, and whether your "retirement budget" survives reality — before betting your entire net worth.

Here's how it stacks up:

| Path | Duration | How it's funded | Back to work? |

|---|---|---|---|

| Full FIRE | Permanent | ~25x expenses; live on ~4% | No |

| Coast FIRE | Ongoing | Retirement number on autopilot; cover today's bills | Yes, lighter |

| Barista FIRE | Ongoing | Part-time income + portfolio | Yes, part-time |

| Micro-retirement | 6 mo–2 yr | Dedicated cash "break fund" | Yes, full-time |

| Employer sabbatical | Weeks–months | Often paid or job-protected | Yes — same job |

That last row hides the biggest trap. Most people picture a micro-retirement as a sabbatical — a job-protected pause where your employer holds your seat and your insurance. For most workers, that doesn't exist: only around 5-18% of employers offer sabbaticals, far fewer paid. So a true micro-retirement usually means you quit — no employer coverage, no guaranteed job to return to.

If that made your stomach drop, that's useful information — it might mean a steadier path fits you better. Coast FIRE — where your savings are already big enough to grow into your number on their own while you cover only today's expenses — lets you downshift without the cliff edge of quitting. Just know which one you're signing up for; the price tag is very different.

The Real Price Tag: Lost Income + Lost Compounding + the Benefits Gap

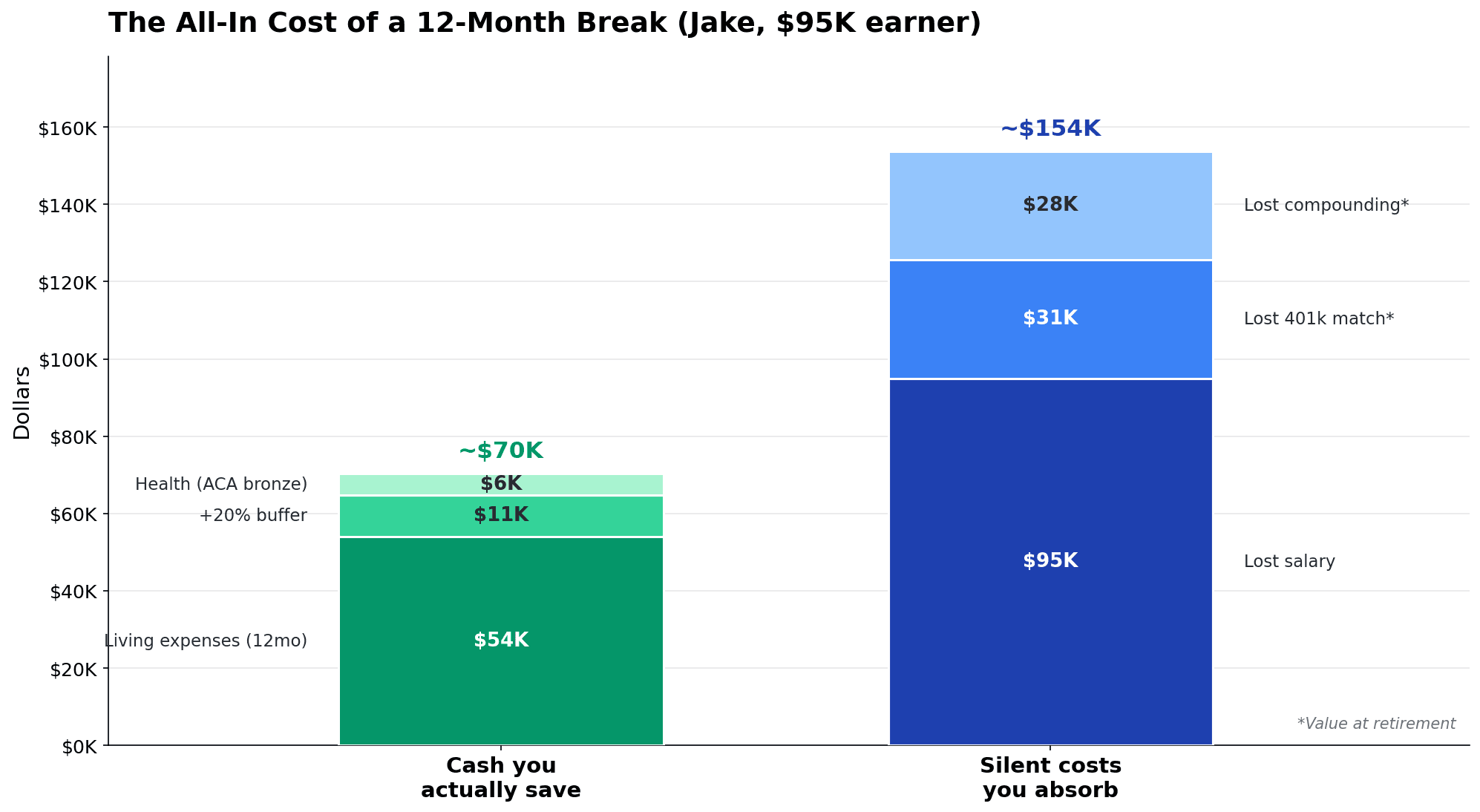

The cost of a micro-retirement comes in three layers, and the rent you pay is only the visible one.

Layer 1 — Living expenses. Rent, food, travel, insurance, fun — the only layer most people budget for.

Layer 2 — Lost income. The salary you don't earn. For Jake, a $95,000 earner taking a year off, that's $95,000 of forgone pay, even if his spending stays modest.

Layer 3 — The silent killers: lost compounding and the benefits gap. This does the most long-term damage precisely because it never shows up on a monthly budget. Stop contributing to your 401(k) and you lose your contributions, the employer match (free money), and decades of compounding on both — all at once.

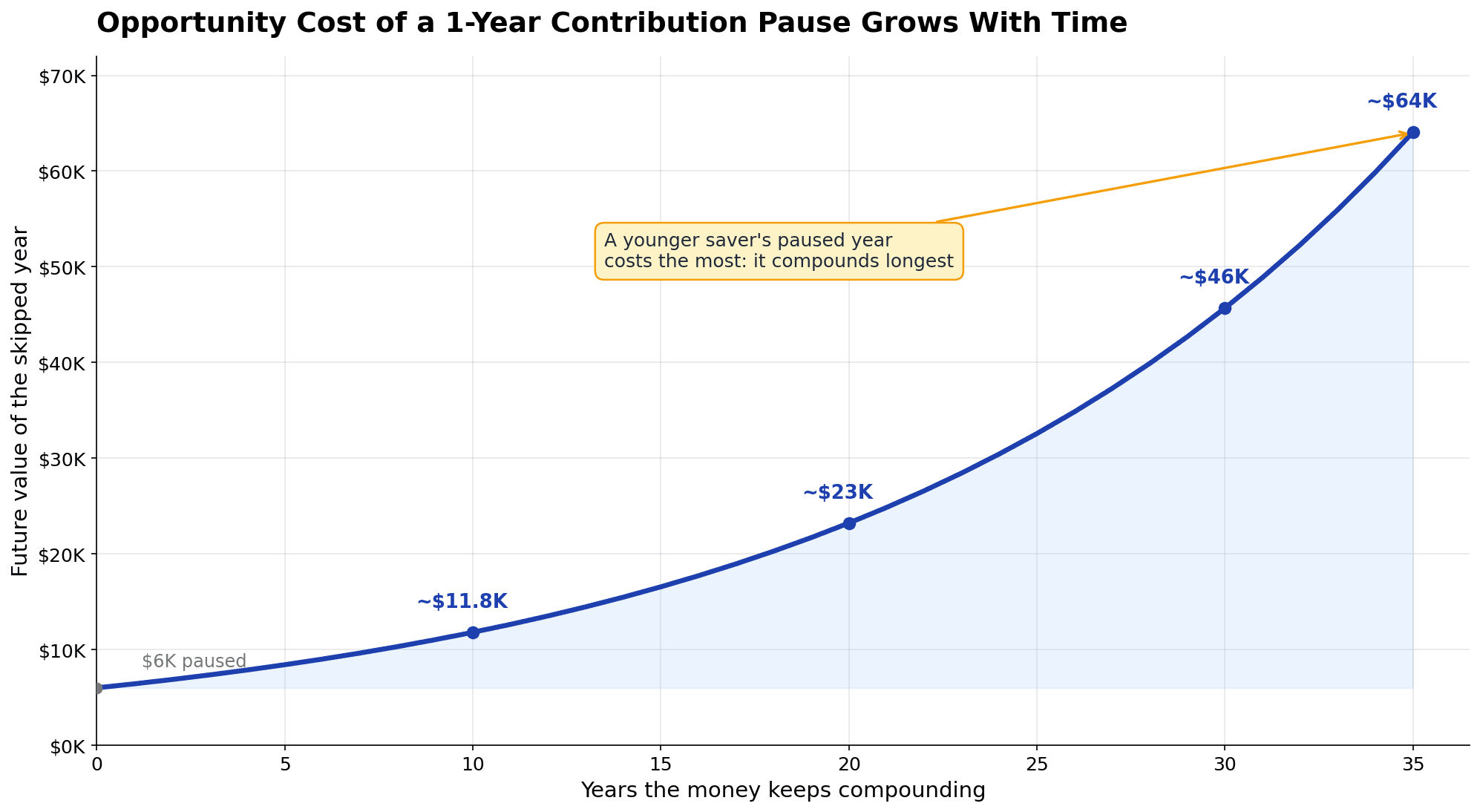

I'm biased here, because the single thing I believe most about money is that time plus compounding is the most magical force you've got — and being young is the biggest edge of all. That's exactly why a paused contribution year stings me more than the forgone salary: you're not just skipping a deposit, you're taxing every future year that deposit would have grown.

Per SmartAsset, pausing 401(k) contributions for one year on a $60,000 salary (6% contribution, 50% match) costs roughly $20,900 over 20 years at 7%. Missing a single year of a typical ~$4,000 employer match compounds to roughly $30,000+ over 30 years at 7%. And the younger you are, the worse it gets:

| Age at break | Approx. lost retirement wealth from a 1-year pause |

|---|---|

| 30 | ~$64,000 |

| 40 | ~$32,500 |

| 50 | ~$16,500 |

(~$6,000/yr contribution paused one year, 7% growth, compounded to 65. Source: a 2026 Yahoo Finance analysis.)

A 30-year-old who pauses contributions for one year quietly hands back $64,000 of future wealth. The plane ticket cost $800; the pause cost sixty grand. That gap between visible and silent cost is the whole reason this article exists.

Then there's the benefits gap — health insurance — which in 2026 is unusually brutal (numbers below). With enhanced ACA subsidies expired, covering yourself during a break costs more this year than usual; budget for it explicitly, or it forces you back early. The point of mapping all three layers isn't to scare you off — it's to make sure that when you say a break is worth it, you're saying yes to the real price.

Build a "Break Fund" — Separate From Your Emergency Fund

Here's the core mechanic — the rule that keeps you in the 18% who finish: your micro-retirement money must live in its own pot, completely separate from your emergency fund.

Why does separation matter? Blend the two and you'll "see" more money than you can really spend — and overspend. And when a real emergency hits during the break (life doesn't pause just because you did), you'll have nothing to absorb it, so you cut the break short or raid a retirement account. The separation is a guardrail against your own future panic.

This isn't theory for me. When I got married and a family entered the picture, I quietly moved our emergency fund from the standard 3-6 months to a full 12 — not because the math demanded it, but because once other people depend on you, "safe" beats "optimal." A break fund is that same instinct, one drawer over: separate pot, separate job, never the money that's there to absorb a real emergency.

A break fund is additional savings, not a repurposed safety net. The typical American emergency fund is already thin — Bankrate pegs the average at $16,800 but the median at just $5,000, and 1 in 3 couldn't cover one month of expenses. If that's you, build it first; I laid out how much and how fast in Emergency Fund 2026: How Much You Need and How to Build It. The break fund sits on top of that emergency fund, never instead of it.

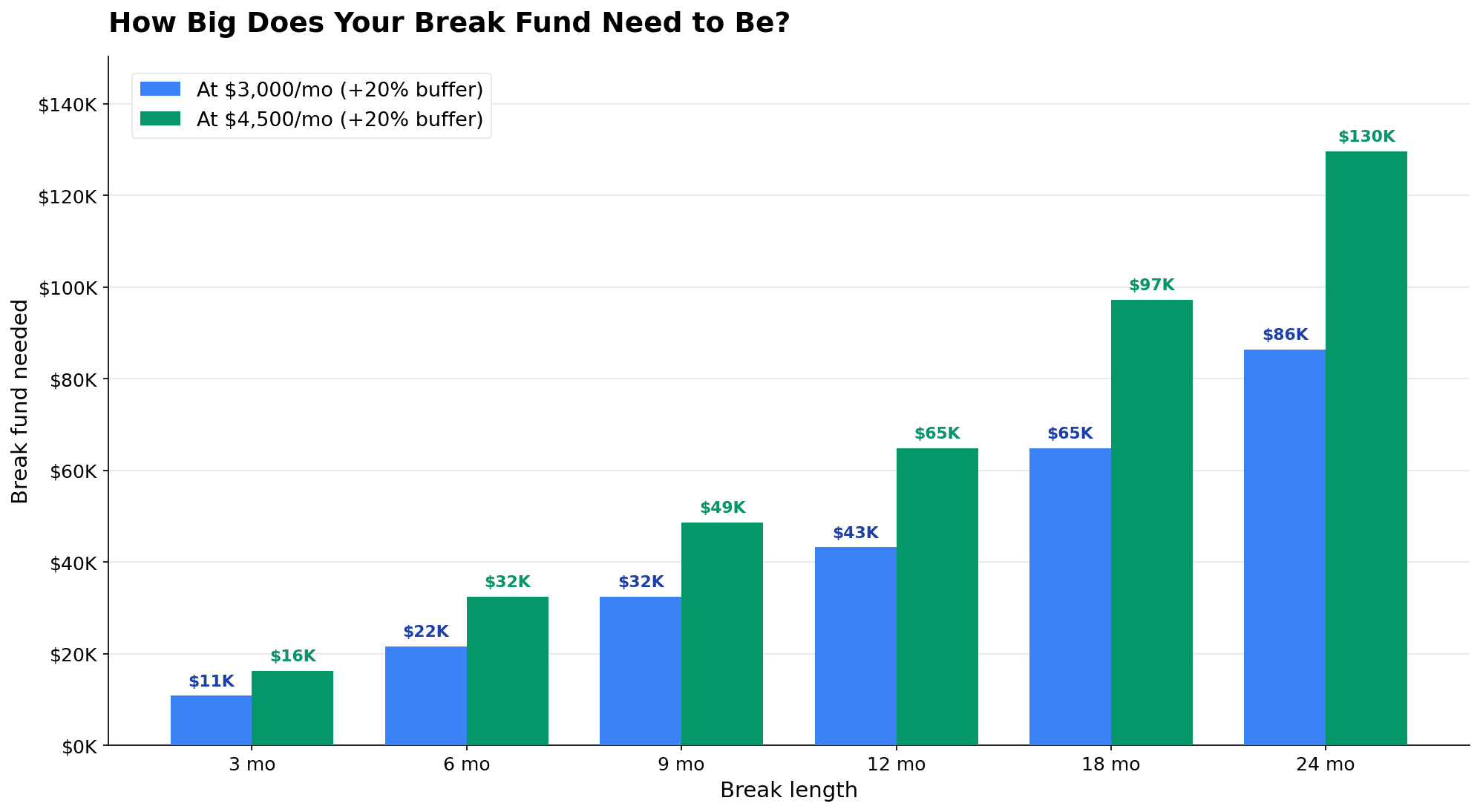

How big? The planner formula is simple:

Break fund = (monthly expenses × break length) + a 20% buffer.

The buffer is non-negotiable — it covers the pricier flight, the dental work, the extra weeks. Here it is across common break lengths at two spending levels:

| Break length | Bare @ $3,000/mo | Fund (+20%) | Bare @ $4,500/mo | Fund (+20%) |

|---|---|---|---|---|

| 3 months | $9,000 | $10,800 | $13,500 | $16,200 |

| 6 months | $18,000 | $21,600 | $27,000 | $32,400 |

| 9 months | $27,000 | $32,400 | $40,500 | $48,600 |

| 12 months | $36,000 | $43,200 | $54,000 | $64,800 |

| 18 months | $54,000 | $64,800 | $81,000 | $97,200 |

| 24 months | $72,000 | $86,400 | $108,000 | $129,600 |

The "enough" benchmark, from Abid Salahi of FinlyWealth (the source of that 82% stat): at least 12 months of living expenses set aside separately before you go. Below that, breaks collapse into involuntary unemployment far too often. For longer breaks, target the full length plus a re-entry buffer on top.

Where should it sit? Liquid and earning something — a high-yield savings account for the cash you'll need first, and a CD ladder (staggered certificates of deposit maturing in sequence) for the back half of the break, so money you won't touch until month nine still earns yield while landing on schedule.

The 12-18 Month Savings Runway: A Step-by-Step Funding Plan

Sizing the fund is the easy part; building it is usually a 12-to-18-month project, not a one-quarter sprint. Here's the five-step runway.

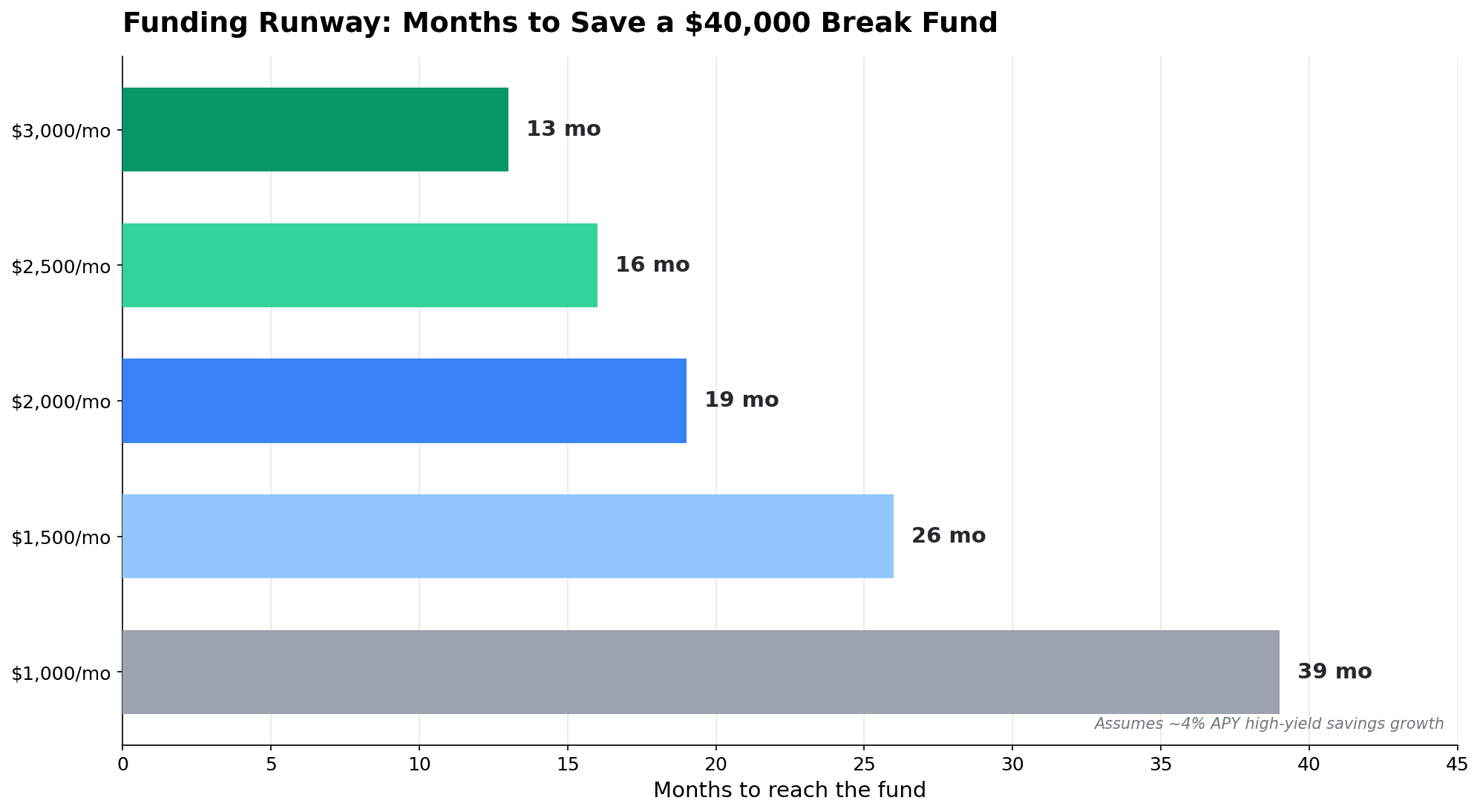

Step 1: Earmark a fixed slice of income — 15% to 30%. Decide the percentage that goes only to the break fund and automate it the day after payday. How long it takes depends entirely on the monthly amount:

| Monthly amount earmarked | Months to reach a $40,000 break fund* |

|---|---|

| $1,000 | ~39 months |

| $1,500 | ~26 months |

| $2,000 | ~19 months |

| $2,500 | ~16 months |

| $3,000 | ~13 months |

*Approximate, assuming ~4% APY high-yield savings growth on the balance.

Step 2: Test-drive the break budget before you leave. Salahi's best clients trim monthly expenses 25-35% while still working and live on the leaner budget for three to six months. It proves the number holds, and every dollar you don't spend pours into the fund. Can't hit it with a paycheck? You won't manage it with no income.

Step 3: Add a side-income top-up. Roughly 1 in 3 planners lean on freelance work — to build the fund faster and keep cash trickling in during the break. Even $500-$800/month shrinks the fund you need.

Step 4: Use geographic and lifestyle arbitrage — twice. Before you leave, a lower cost of living builds savings faster; during the break, basing yourself somewhere cheaper stretches every dollar. It's the same engine from Geographic Arbitrage: Keep a Big-City Salary, Save $40K/Yr — applied here, it can turn a 9-month fund into 12 months of runway.

Step 5: Kill high-interest debt first. Enter with only a mortgage, if any debt at all. Salahi's take is blunt: in his experience, breakers who enter debt-free (a mortgage aside) are far more likely to finish without financial stress. Pay off any 20%+ balances before you go — they'll eat your fund alive while you're not earning. Do all five over a year-plus and the fund builds in the background — which is what separates a planned micro-retirement from an impulsive resignation.

Protect Your Net Worth and FIRE Timeline While You're Off

The question that keeps people up at night: if I take a year off, do I blow up my FIRE timeline? A little if you do it cleanly, a lot if you do it carelessly. The gap comes down to three moves.

Move 1: Front-load retirement contributions before you leave. You can't contribute without a paycheck, but you can max what you're able to beforehand — hit your IRA early in the year, push extra into the 401(k) before your last day. It won't fully beat the pause, but it softens it.

Move 2: Do NOT sell investments in a down market to fund the break. Forced to liquidate stocks in a downturn, you lock in losses and permanently remove those shares from the recovery — a trap called sequence-of-returns risk. This is why the break must be funded with cash saved in advance, not a raided brokerage account; I went deep on it in Sequence of Returns Risk: The 2026 FIRE Defense Playbook, and a fully-funded break fund is your defense. Some planners even shift 15-20% of the portfolio to conservative holdings beforehand so a bad market can't force their hand.

Move 3 — the cardinal rule: never raid your 401(k) or IRA. This is the difference between a FIRE rehearsal and a FIRE disaster. An early withdrawal means a 10% penalty, plus income tax, plus permanent loss of all future compounding — the single worst way to pay for time off. If the only way you can afford the break is cracking open your 401(k), you can't afford it: that's a "wait 12 more months" signal, not a "do it anyway" one.

Keep these three rules — front-load, don't sell low, never raid retirement — and a clean micro-retirement pushes your FIRE date out by months, not years: one skipped year of contributions, a known cost you decided was worth it. A raided break sets you back years and adds penalties on top — same break, wildly different outcome.

Health Insurance, Taxes, and the Boring Stuff That Sinks People

Logistics sink more breaks than wanderlust ever does. Three things to handle.

Health coverage (and why 2026 makes it worse)

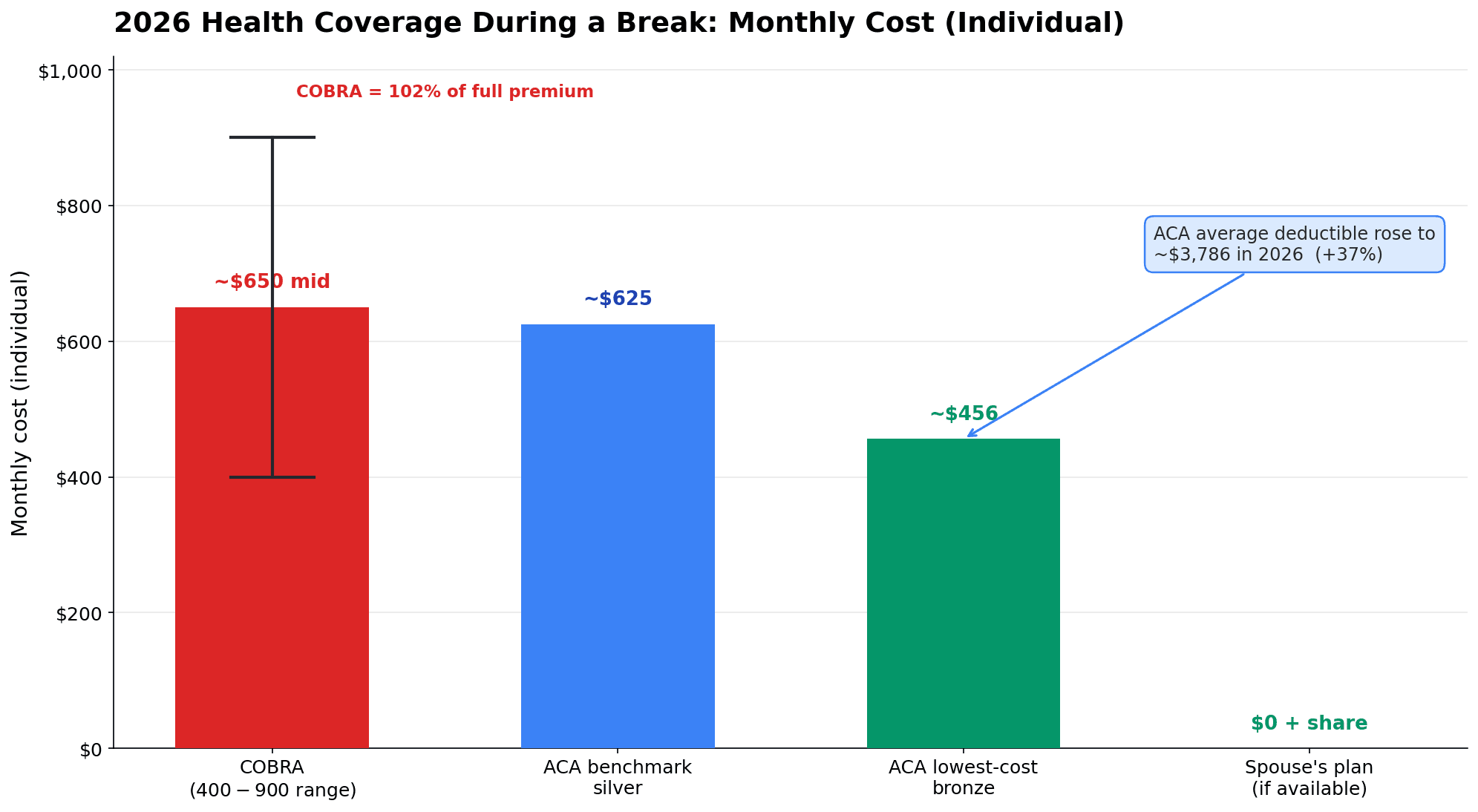

Quit and you lose employer insurance — and in 2026 the replacements are pricier than they've been in years, because the enhanced ACA (Affordable Care Act) marketplace subsidies expired. A KFF analysis estimated subsidized enrollees' premium payments would rise about 114% on average if the enhanced tax credits expired (from an average of $888 to $1,904 a year). Four main paths, all worth pricing before you set a break date:

| Option | Typical 2026 monthly cost (individual) | Notes |

|---|---|---|

| COBRA | $400–$900 | Keep your exact employer plan/doctors up to 18 months — but you pay 102% of the full premium (your share plus the employer's, plus a 2% fee). |

| ACA benchmark silver | ~$625 (gross) | Mid-tier marketplace plan; 60-day special enrollment from your last day of coverage. |

| ACA lowest-cost bronze | ~$456 (gross) | Cheapest ACA-compliant option; higher deductible (the 2026 average marketplace deductible across all plans is ~$3,786, up 37% from $2,759; bronze deductibles typically run higher). |

| Spouse's plan | $0 + premium share | Almost always cheapest if available. |

(Sources: a 2026 CobraInsurance.com cost guide and the 2026 KFF marketplace analysis.)

A detail people miss: COBRA lets you keep your employer plan temporarily after leaving, but you absorb the entire premium — which is why it's often the priciest option despite keeping your doctors. For a healthy single person on a short break, a bronze ACA plan is usually cheaper. Planners suggest budgeting $15,000-$20,000 for healthcare across a full year off. One bright spot: an HSA is portable, stays yours, and grows tax-free — so it can help cover the deductible during the gap.

The tax silver lining: a Roth conversion window

A break year is usually a low-income year — the best time for a partial Roth conversion: move money from a traditional IRA to a Roth and pay tax now, at an unusually low rate. With little salary, you can convert a chunk while filling only the lowest brackets — a rare case where a low-income year becomes a strategic asset, pre-paying tax cheaply on money that then grows tax-free forever.

Re-Entry Without a Permanent Pay Cut

The scariest part isn't the time off — it's the worry you'll come back and never earn what you did before. That fear is legitimate but increasingly manageable, and the difference is almost entirely preparation. First, the honest risk. Some studies find a 1-2 year interruption carries a wage penalty around 22%, and even a clean 12-month gap can leave a ~7-9% dent that lingers for years. Among returners, 73% reported trouble finding work and only 40% landed full-time roles, per Career Returners data.

But the counterbalance is significant: the stigma is fading fast. LinkedIn's research found 52% of hiring managers believe candidates with career breaks bring valuable skills, and 51% said they'd be more likely to call back a candidate once they understood the context. The penalty is largely avoidable if you do four things:

- Keep your skills warm. A few hours a month staying current — a course, a side project, an industry newsletter — meaningfully shortens the eventual job search.

- Keep your network warm. Maintaining relationships — quarterly coffees, the occasional check-in — tends to surface your next role faster. Most jobs still come through someone you already know.

- Frame the gap with confidence. Use LinkedIn's "Career Break" feature and tell the story plainly: an intentional, planned break, here's what you did. Owned confidently, that reads very differently from "unemployed."

- Use the break as leverage. You're returning recharged, often with new skills. Frame re-entry as choosing the right role, not grabbing any role, and negotiate accordingly.

The proof it works: one of Salahi's clients, a software developer, took a 14-month micro-retirement, built side income covering 45% of expenses, learned new languages — and returned to a job paying 22% more. Preparation turned a break into a raise.

Is a Micro-Retirement Right for You? A 6-Question Readiness Check

Run honestly through these six questions. They'll tell you whether to go now, wait 12 months, or pick a different path.

- Is my high-interest debt gone? Carrying credit-card balances? Not yet. Enter with only a mortgage.

- Is my break fund fully funded — and separate from my emergency fund? At least 12 months of expenses (full break length plus a buffer is better), in its own account, on top of an intact emergency fund.

- Do I have a written re-entry plan? A target return date, a skill-upkeep schedule (5-10 hrs/month), and a warm network. A break without a return trigger drifts into an open-ended, savings-draining gap.

- Have I solved health coverage? A specific plan chosen and priced — not "I'll figure it out."

- Have I test-driven the budget? Three-to-six months on the leaner break budget while still working, so you know the number holds.

- Can I do all this WITHOUT touching my 401(k) or IRA? If funding the break requires raiding retirement accounts, the answer is no — wait and save more.

How to read your score:

- Yes to all six? You're ready — model the FIRE-timeline impact first, then go.

- Yes to most, no on the fund? A "save 12 more months" case: you have the plan, you need the runway.

- No on debt or the separate fund? A candidate for a steadier path first. Pay off the cards, build the fund, and meanwhile consider whether ongoing time freedom suits you better than a one-off break — Barista FIRE vs Coast FIRE lays out two ways to buy back time without stepping fully away.

Take "Michelle," 36, a nurse earning $72,000. She wants a six-month break but has $9,000 in credit-card debt and only $6,000 saved outside her 401(k), so she fails questions 1 and 2. The right move isn't to force it — clear the cards, build a $25,000 break fund over ~18 months, then go. Michelle isn't a "no." She's a "not yet" — and knowing the difference keeps her out of that 82%.

And before anyone with six green checkmarks pulls the trigger: model it first. Model the dip and recovery in MFFT's net worth tracker so you see exactly how many months a 6-, 12-, or 18-month break moves your finish line. My honest take, and I'll be upfront that this is my path and yours will differ: I lean toward optionality over a hard stop, which for me looks more like Coast FIRE — easing off without quitting outright, partly for my kids' sake. But I won't pretend a clean, fully-funded break is wrong; for plenty of people who pass this check, buying back a year while you're young enough to enjoy it is absolutely worth it. The point is to choose it with the math in front of you, not on a feeling.

The Bottom Line

A micro-retirement is one of the most powerful "buy back your time" moves available in 2026 — and one of the easiest to get catastrophically wrong. The whole outcome hinges on one fork: did you fund the gap deliberately, or impulsively?

The disciplined version has a fixed length, a dedicated break fund separate from emergency savings, a solved health plan, and an iron rule never to raid retirement accounts. Built that way, a break costs a known, bounded slice of compounding and pushes your FIRE date out by months — a price plenty of people happily pay to spend a year awake instead of exhausted. The other version skips the runway, blends the funds, and ends in involuntary unemployment with a cracked-open 401(k). The rules aren't heroic — they just have to happen before you hand in your notice.

So if a mid-career break is calling you, don't answer it on a feeling — run the six-question readiness check and build the separate break fund first. I built our net-worth tracker because I never trusted finance tools that hide their math, so when you model the dip and recovery you can see every assumption, not just a green "you're fine." And if you've taken a micro-retirement, or you're sizing up your break fund right now and the numbers surprised you, email me at dennis.vymer@myfinancialfreedomtracker.com and tell me what you found — I read every one. The best version of this trend isn't a vibe or a rebellion — it's a budget. Build the budget, and you can buy back a year of your life now and keep your financial freedom fully intact.

Frequently Asked Questions

How much money do you need for a micro-retirement? Size a dedicated break fund as (monthly expenses × break length) + a 20% buffer, and aim for at least 12 months of living expenses set aside separately before you go. At $3,000/month that's roughly $43,000 for a 12-month break; at $4,500/month it's closer to $65,000.

What's the difference between a break fund and an emergency fund? They're two separate pots. Your emergency fund absorbs life's surprises and stays intact; your break fund is additional savings that exists only to pay for the planned break. Blend them and you'll overspend — and have nothing left when a real emergency hits mid-break.

Can I take a micro-retirement and still retire early? Yes, if you do it cleanly: front-load contributions before you leave, fund the break with cash saved in advance (never a raided 401(k) or IRA), and don't sell investments in a down market. Done that way, one paused year typically pushes your FIRE date out by months, not years.

How do I handle health insurance during a career break? Price your options before you set a date: a spouse's plan (usually cheapest), an ACA marketplace plan (bronze ~$456 or benchmark silver ~$625 per month in 2026, before subsidies), or COBRA ($400-$900 to keep your exact plan). Budget roughly $15,000-$20,000 for a full year off.

Will a career break hurt my salary when I return? It can, but the penalty is largely avoidable. Keep your skills and network warm (5-10 hours a month), frame the gap as intentional, and use the break as leverage — one of the worked examples here returned to a job paying 22% more.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Start Here

Start HereSafe Withdrawal Rate 2026: Is the 4% Rule Still Right?

Morningstar says the safe withdrawal rate in 2026 is 3.9%; the 4% rule's inventor now says 4.7-5.5%. Here's why both are right, and how to find your number.

Start Here

Start HereEmpower vs Monarch Money (2026): Fees, Features, Verdict

Empower is free but sells 0.89%/yr advice once you link $100K. Monarch costs $99.99/yr and budgets better. June 2026 verified pricing, honest verdict.

Start Here

Start HereNet Worth Trackers That Don't Link to Your Bank (2026)

Track net worth without handing over bank logins: spreadsheets, GnuCash, Wealthfolio, Worthy, Kubera, and my manual-first tracker — honestly compared.

Start Here

Start HereYNAB Alternatives That Are Actually Free (2026 Guide)

YNAB costs $109/year in 2026. EveryDollar, Goodbudget, Actual Budget, spreadsheets, and my own tracker — what's actually free, with every catch listed.

Start Here

Start HereSocial Security 2033: FIRE-Proof Your Plan for a 23% Cut

The May 2026 CBO update moved insolvency to 2032 — a 23-28% benefit cut by 2033. How FIRE investors recalibrate nest egg, claiming age, and withdrawals.