Cash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

I got into all this at eighteen, watching a guy on YouTube count cash into envelopes, so I have a soft spot for the method — but I've spent the years since learning, the hard way, that feeling organized about money and actually growing it are two very different things. So when cash stuffing took over my feed again this year, I wanted to do what I always do: stop scrolling and test it with real numbers.

Open TikTok and you'll see it within about thirty seconds of scrolling: a pair of manicured hands sliding crisp twenties into a pastel binder, each pocket labeled in careful handwriting. Groceries. Gas. Fun money. The video has two million views.

This is cash stuffing — the envelope budgeting method your grandmother used, rebranded for a generation that grew up tapping a phone to pay.

And in 2026, it is everywhere. So is its gamified cousin, the 100-envelope challenge, with its irresistible promise: save $5,050 in 100 days.

But here's the question almost nobody on your feed is asking: does cash stuffing actually build wealth? Or does it just feel productive while quietly costing you money?

Let's put it to the test — with real 2026 numbers and no hype.

Key takeaways

- Cash stuffing is a spending brake, not a wealth builder. Handing over physical cash makes people spend 12–18% less — but the cash itself earns nothing.

- The 100-envelope challenge is a great kickstart: filling envelopes 1–100 once banks $5,050 in about 100 days. Treat it as a savings sprint, then move the money.

- Idle cash quietly loses to inflation. $5,000 in a drawer has the buying power of about $3,300 in a decade at 2026 inflation; in a 4% account it grows to roughly $7,400.

- Best of both worlds: use cash (or a digital "envelope" app) to control spending, then route the savings into an insured, interest-earning account — or, for long-term money, a low-cost index fund.

- Who it's for: chronic overspenders and tactile learners. Disciplined savers, online-bill payers, and anyone carrying high-interest debt should skip the literal cash.

What Is Cash Stuffing? The Viral Envelope Method Explained

Cash stuffing is dead simple. You decide how much you'll spend in each category for the month — groceries, dining, gas, entertainment — then you withdraw that exact amount in cash and physically divide it into labeled envelopes.

When an envelope is empty, you're done spending in that category. No tapping a card and "figuring it out later." No overdraft. The money is simply gone, and you can see it happening.

It's the same envelope system financial counselors have taught for decades. What's new is the aesthetic: color-coded binders, satisfying cash-counting videos, and a community of millions sharing their setups online. The method went viral because it turns the abstract, joyless act of budgeting into something tactile and oddly satisfying.

The appeal is obvious in a world of one-tap payments. When money is invisible, it slips away. Cash stuffing makes it visible again. The real question is whether "visible" also means "growing."

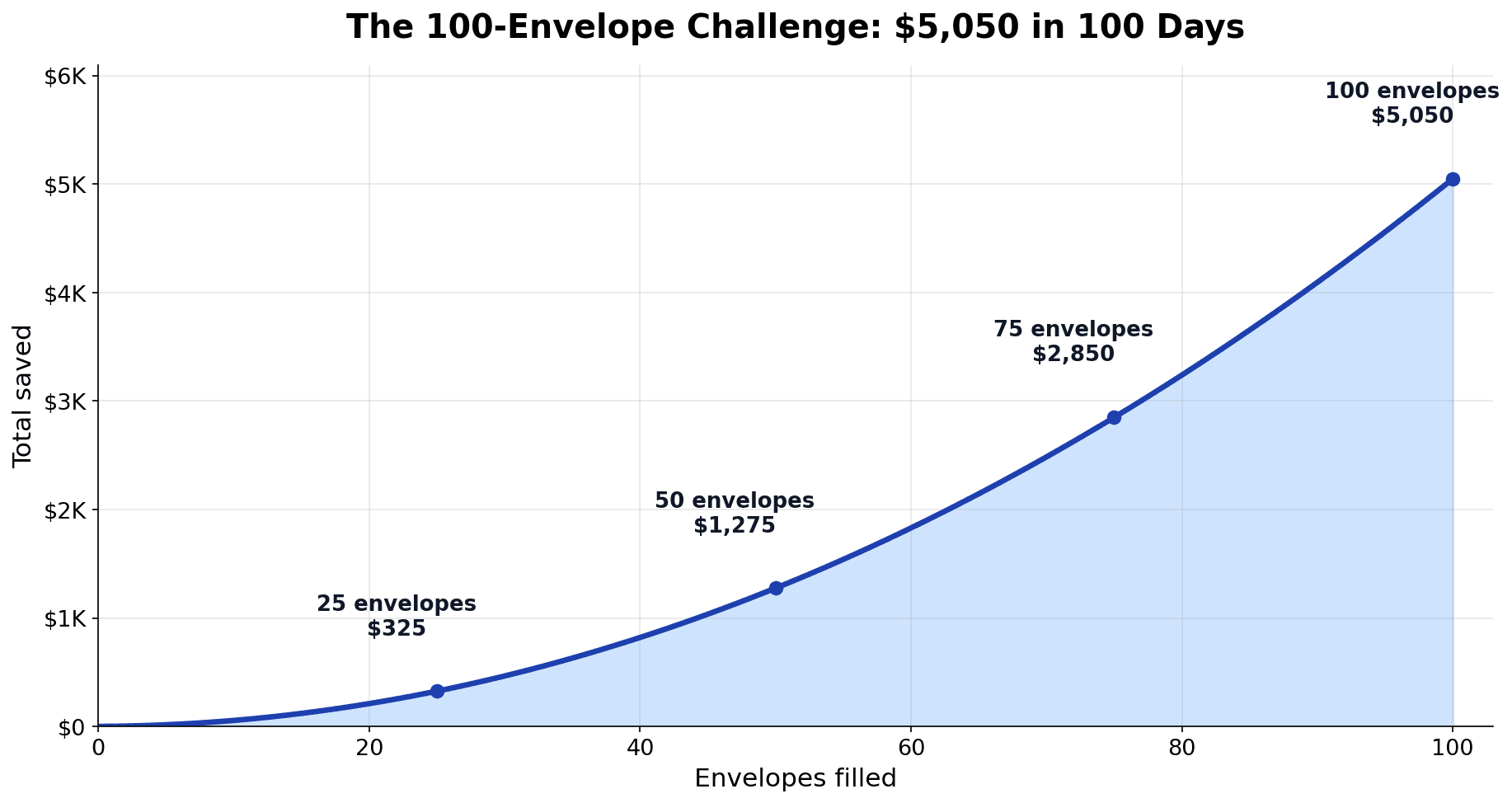

The 100-Envelope Challenge: How $5,050 in 100 Days Really Works

The 100-envelope challenge is cash stuffing turned into a game, and it's the single biggest reason the trend exploded.

Here's how it works: grab 100 envelopes and number them 1 to 100. Each day, pick one envelope and stuff it with that dollar amount. Envelope 1 gets $1. Envelope 67 gets $67. You can go in order, or draw randomly to keep it interesting.

Add every envelope together — $1 + $2 + $3, all the way to $100 — and you land on a strangely motivating total: $5,050 in 100 days.

The momentum is the point. Watching the pile grow is what keeps people going.

If $100 in a single day feels impossible, there are gentler versions:

| Variation | How it works | Total saved |

|---|---|---|

| Half challenge | Envelopes 1 to 50 only | $1,275 |

| Standard | Envelopes 1 to 100 | $5,050 |

| Double | Each envelope amount times two | $10,100 |

| Weekly | One envelope per week instead of per day | $5,050 over ~2 years |

Whatever version you pick, the challenge proves something powerful: you can find $5,050 you didn't know you had. Hold that thought — because where that $5,050 ends up matters far more than the fact that you saved it.

Why Cash Stuffing Works: The Psychology of Physical Money

Let me say this clearly, because the rest of this article gets skeptical: the behavioral science behind cash stuffing is real, and it's strong.

I'll be honest about my own bias here: I'm an engineer, and I don't trust a money tool I can't see the math behind. An empty envelope is the most honest interface there is — when it's gone, it's gone, no hidden fees, no "figure it out later." That visibility is exactly why it works, and it's the same reason I want the budgeting tools I use to never hide their numbers from me either.

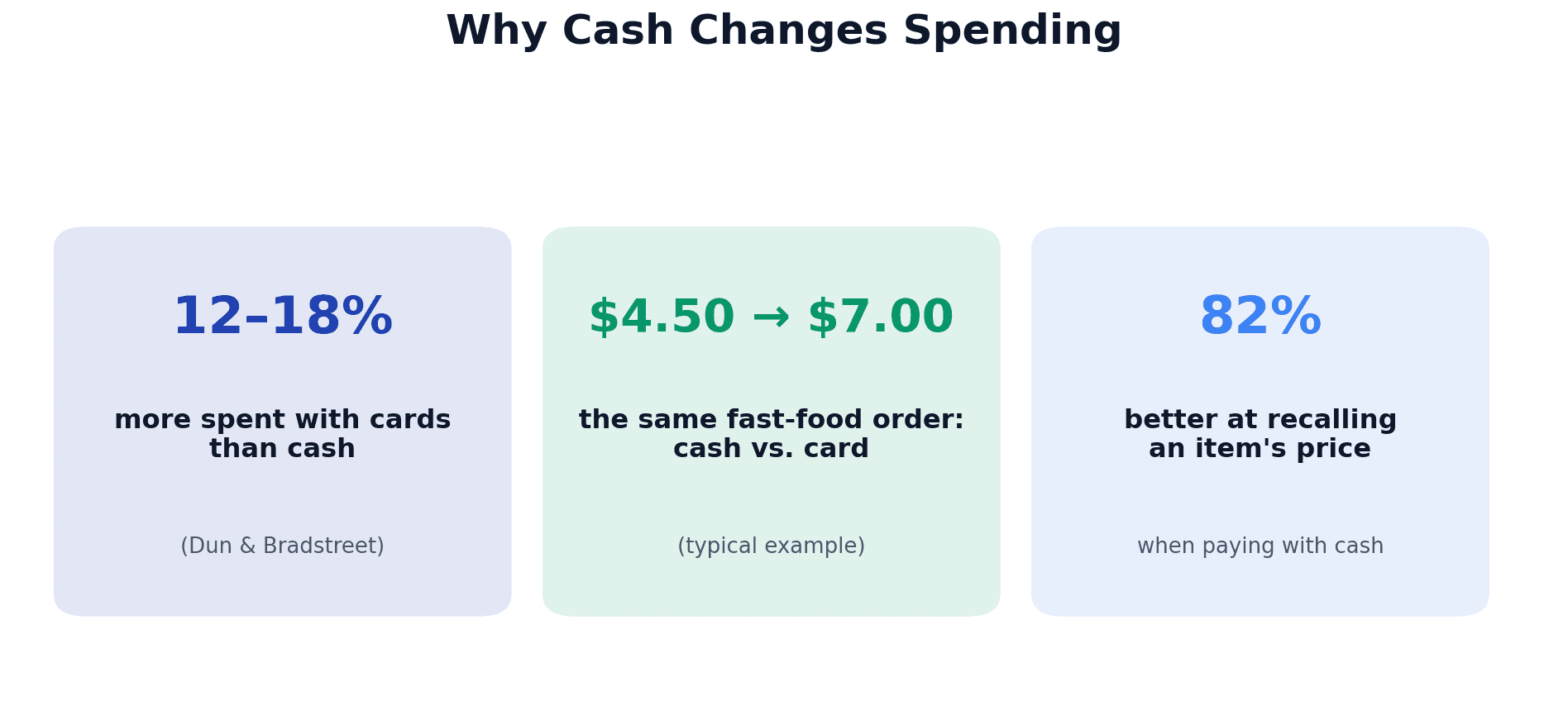

Researchers call it the pain of paying. When you hand over physical cash, your brain registers a small, genuine sting of loss. When you tap a card, that sting is muted — the payment is decoupled from the purchase, and your spending brakes quietly release.

The numbers are striking. An oft-cited Dun & Bradstreet finding is that people spend 12 to 18% more when paying by card instead of cash. One classic lab study put the gap as high as 83% in specific situations. MIT Sloan researchers have shown that cards literally activate the brain's reward center. One classic example: McDonald's reportedly found the average order jumps from $4.50 in cash to $7.00 on a card.

There's a memory effect, too. Research on payment and memory found cash users were 82% better at recalling what they'd paid for something. When money moves through your hands, it moves through your attention.

This is why cash stuffing genuinely helps a certain kind of spender. If you routinely blow past your dining or shopping budget because tapping is frictionless, reintroducing that friction can cut your spending fast. That's not a gimmick. That's behavioral economics doing real work.

But notice what this strength is really about. Cash stuffing is a tool for controlling spending. That is a completely different job from growing money — and this is exactly where the trend starts to cost people.

The Hidden Costs: What Cash Stuffing Quietly Takes From You

Here's the part the satisfying binder videos never show: idle cash doesn't just sit there. It slowly bleeds value.

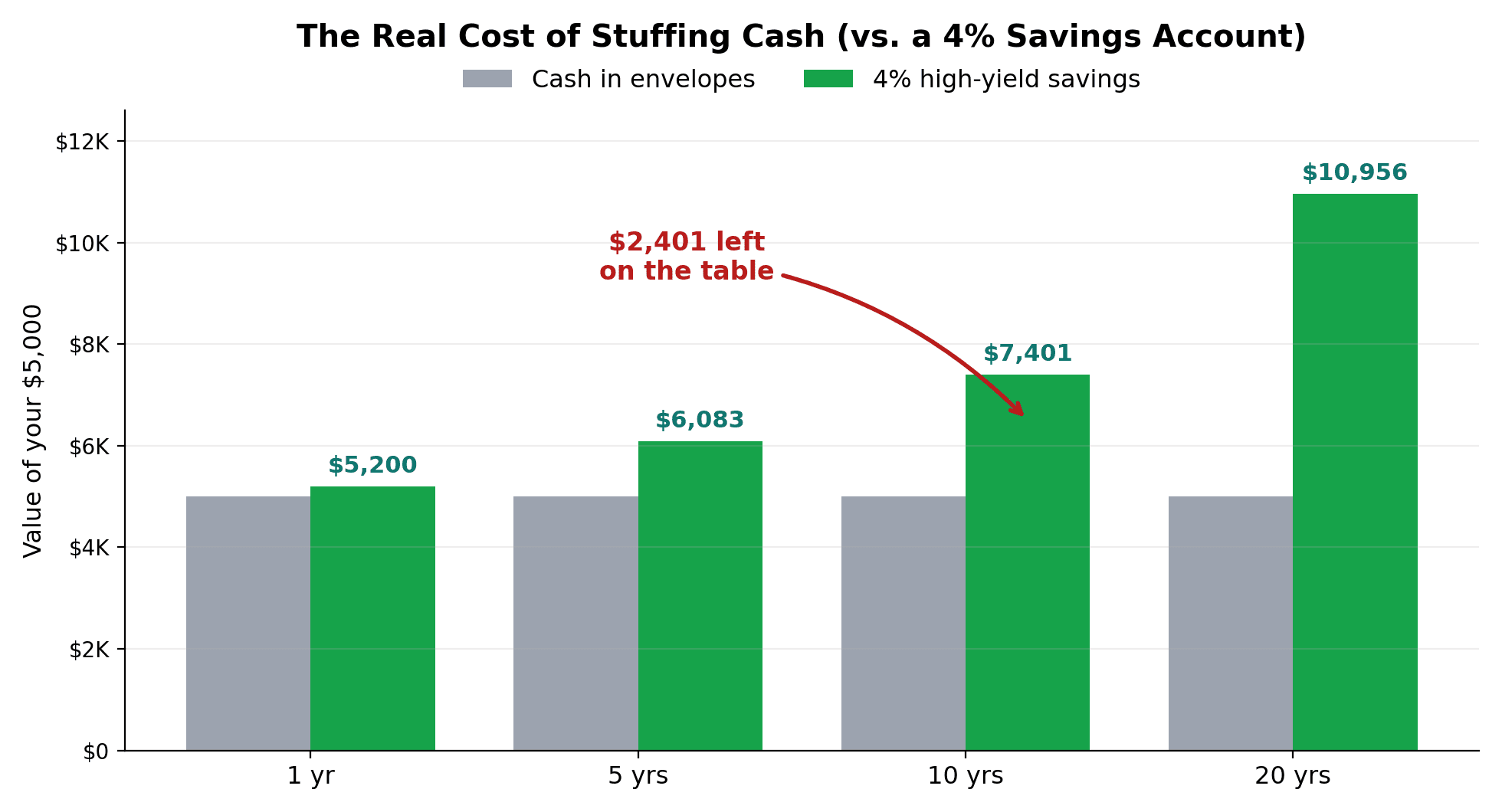

Picture Jake. He crushes the 100-envelope challenge, finishes with $5,050 in a shoebox on his closet shelf, and feels fantastic. A year later, that pile is still exactly $5,050.

Now picture the same $5,000 sitting in a high-yield savings account. In June 2026, the best HYSAs pay around 4% APY — while the national average savings account pays a pathetic 0.38%. At 4%, Jake's money would have earned about $200 in that first year. A free month of groceries, gone, because the cash sat in a closet.

It gets worse over time, because of two forces working against him at once.

Force one: forgone interest. Money in a 4% account compounds. Money in an envelope doesn't.

Force two: inflation. Prices rose 4.2% over the year ending May 2026 — above 4% for the first time in three years, driven largely by an energy shock. Inflation eats the purchasing power of idle cash every single day.

Put both together and the gap is brutal:

| Time | $5,000 in envelopes (cash) | $5,000 in a 4% HYSA | The cost of stuffing |

|---|---|---|---|

| 1 year | $5,000 (worth ~$4,798 in real terms) | $5,200 | ~$200 lost + inflation |

| 5 years | $5,000 (worth ~$4,070) | $6,083 | ~$1,083 behind |

| 10 years | $5,000 (worth ~$3,314) | $7,401 | ~$2,401 behind |

| 20 years | $5,000 (worth ~$2,196) | $10,956 | ~$5,956 behind |

That drawer of "saved" money has the buying power of about $3,300 in a decade. Stuffing protected Jake from overspending, then quietly punished him for saving the wrong way.

And we haven't even mentioned the practical risks: cash at home isn't insured against theft, fire, or a flood the way an FDIC-insured account is (protected up to $250,000 per depositor, per insured bank, per ownership category). Lose the envelope and you lose everything. Try paying your rent, your utilities, or your emergency fund target with a binder, and the cracks show fast.

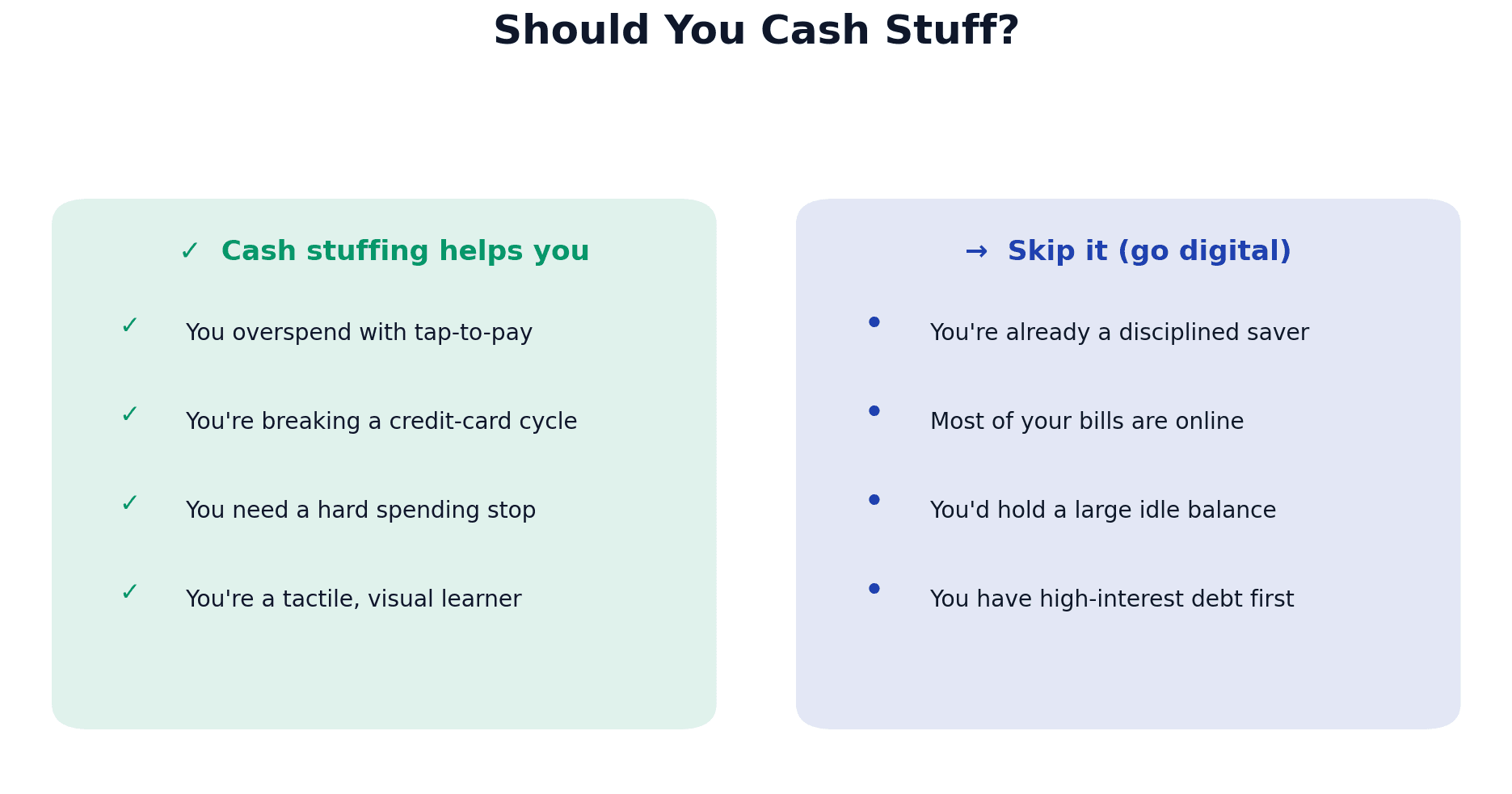

Who Cash Stuffing Is Actually For (and Who Should Skip It)

So is cash stuffing good or bad? The honest answer: it depends entirely on who you are.

Meet Maya. She earns well but bleeds money on dining out and impulse buys — every month, tapping her card, "treating herself." For Maya, cash stuffing is a near-miracle. She pulls out $300 for "dining" and "fun money," and when those envelopes are empty, the month is over. Her overspending in those two categories drops about 15%. The friction is worth far more to her than 4% interest, because the alternative was leaking money she never even noticed.

Now meet Jake again. Jake is already disciplined. He doesn't overspend; he just wanted a fun savings challenge. For Jake, cash stuffing is a step backward — he's adding risk and forfeiting growth to solve a problem he doesn't have.

Here's the rule of thumb:

If you carry high-interest debt, by the way, neither envelopes nor a savings account is your best move — throwing that money at the debt almost always wins. (If that's you, start with a credit card payoff plan and build the budget around it.)

Cash Stuffing vs. Digital Envelopes: The Smarter 2026 Hybrid

Here's the good news: you don't have to choose between behavioral friction and financial growth. You can have both.

The trick is to separate the psychology from the storage. The magic of cash stuffing was never the paper envelopes — it was the hard limit and the visibility. You can recreate that digitally and keep your money insured and earning.

This is the digital envelope approach, and it's what most financial planners now recommend for 2026. You assign every dollar a category (this is just zero-based budgeting), you set hard caps, and you create "sinking funds" — dedicated buckets for irregular costs like car repairs, holidays, or annual insurance. The visibility of the binder, none of the dead money.

A privacy-first budgeting app like MFFT is built for exactly this. You get the category-by-category hard stops that make cash stuffing work, automatic tracking so you actually remember where your money went, and — crucially — it helps you see and route savings into your own interest-earning, insured accounts instead of a closet. You can even watch it move the needle on your net worth instead of vanishing into a drawer.

This is the same low-effort, high-consistency philosophy behind quiet saving: automate the discipline, skip the theater.

Meet Sarah, who gets it right. She runs "groceries" and "going out" — her two weak spots — as real physical cash for the friction. Everything else (rent, utilities, subscriptions) is automated. And every Friday, she sweeps any leftover envelope cash into a goal-tagged savings bucket earning 4%. Best of both worlds: the behavior change and the growth.

How to Start a Cash (or Digital) Envelope System in 4 Weeks

You don't need to overhaul your whole financial life this weekend. Here's a calm, four-week ramp.

Week 1 — Find your leaks. Look at the last two months of spending and identify the two or three categories where you consistently overspend. Don't envelope your whole budget; target the problem areas. (New to this? Start with the basics in how to start a budget.)

I did this myself one weekend a while back — sat down and went through every recurring bill, re-shopped my insurance, energy and liability cover line by line. It wasn't glamorous and it took an afternoon, but it quietly freed up around 4,000 CZK every single month. No envelope can beat finding money you were already losing on autopilot.

Week 2 — Set real amounts. Base each envelope on what you actually spend, not a fantasy number. A cap you can't live with is a cap you'll abandon. Decide now: physical cash or a digital envelope?

Week 3 — Run a pilot. Use the system for one full week in those categories only. When an envelope (or digital bucket) is empty, stop. Notice how the friction changes your choices — this is the loud-budgeting-style awareness that makes viral money challenges actually work.

Week 4 — Review and route the savings. Did you come in under budget? Don't let that surplus sit idle. Sweep it toward your emergency fund, high-interest debt, or a sinking fund. The leftover is the whole reward — give it a job. If you want a structured spending reset alongside this, pair it with a no-buy challenge.

The goal isn't to live out of envelopes forever. It's to retrain your spending, then graduate to a system that grows your money automatically.

Frequently Asked Questions

Does cash stuffing actually save you money? It helps you spend less — people consistently spend 12–18% more with cards than with cash, and watching physical money leave your hand creates real friction. But the cash itself earns 0%, so as a wealth-building tool it loses to even a basic savings account.

What is the 100-envelope challenge? You number 100 envelopes 1 through 100, then fill one each day (in any order) with that dollar amount. Fill all 100 and you've saved 1 + 2 + … + 100 = $5,050 in about three months. It's a motivation hack — the key is moving that $5,050 somewhere it can actually grow once the challenge ends.

Is cash stuffing worth it in 2026? For breaking an overspending habit, it can be genuinely worth it. As a place to keep money, no — with the best high-yield savings near 4% APY and inflation above 4%, cash in a drawer loses buying power every year. Use it to build the habit, not to store the savings.

What's better than cash stuffing? A "digital envelope" setup: keep the buckets-and-limits psychology, but in an insured, interest-earning account (or a budgeting app) instead of physical cash. You get the spending control without leaving money idle — or exposed to theft, fire, or flood.

The Verdict: Does Cash Stuffing Build Wealth?

After running the numbers, here's my honest take.

Cash stuffing is an excellent behavior-change tool and a poor wealth-storage strategy. Those are two different jobs, and confusing them is what costs people money.

If you overspend, the envelope method can genuinely rewire your habits — the pain of paying is real, and the friction works. That's worth a lot. But the moment the money is saved, its job changes: it needs to be safe, insured, and earning. A closet full of cash fails all three tests, and over a decade it can quietly cost you a couple thousand dollars in forgone interest and lost purchasing power.

So use the discipline. Skip the drawer.

Let the 100-envelope challenge prove you can find $5,050. Then send it somewhere boring and automatic — a low-cost global index fund for genuine long-term money, or at minimum that 4% insured account for cash you might actually need. The single most powerful force I've ever seen in my own finances isn't a clever budget; it's time plus compound interest, and being young is the biggest advantage there is. The envelopes were always just training wheels — the real win is the habit, and the habit is portable.

Cash stuffing won't make you wealthy. But the discipline it teaches, pointed at the right accounts, absolutely can.

📩 If you try one of these and get stuck — or you just want to argue with my math — I genuinely want to hear it; that's half the reason I write these. Reach me any time at dennis.vymer@myfinancialfreedomtracker.com.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneySinking Funds: The System That Stops Surprise Bills (2026)

Sinking funds are the missing layer between your budget and emergency fund — pre-funded buckets for bills you see coming. Get the categories, math & 2026 setup.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.

Master Your Money

Master Your MoneyAI Scams Stole $21 Billion: How to Protect Yourself in 2026

AI scams hit a record $20.9B and could reach $40B by 2027. Scammers clone a loved one's voice from 3 seconds of audio. Here's the calm, free, afternoon-long defense playbook to protect your money in 2026.