Quiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Your coworker drives a nine-year-old Civic, skips the group trips, and never posts a single thing about money. You quietly assume she's bad with cash.

She's not. She's past $40,000 in savings and investments — and she's never told a soul.

This is quiet saving, the breakout 2026 money trend. Instead of broadcasting your wins (loud budgeting) or punishing yourself with deprivation (no-buy), you automate your savings, let compounding do the heavy lifting in the background, and stop measuring your life against everyone's highlight reel. The people who look the least rich online are very often the ones building the most wealth.

I've been doing a version of this for years, and I'm convinced it's the most psychologically sustainable way to get ahead. So let me show you what quiet saving actually is, why it exploded this year, and — most importantly — how to turn the vibe into a concrete, privacy-first system you can run on autopilot.

What Quiet Saving Actually Is (and Why It Exploded in 2026)

Quiet saving is exactly what it sounds like: building wealth privately and quietly, on autopilot, without announcing it to anyone. No public spreadsheets. No savings-goal posts. No performance. Just stability over status, and your own number instead of anyone else's feed.

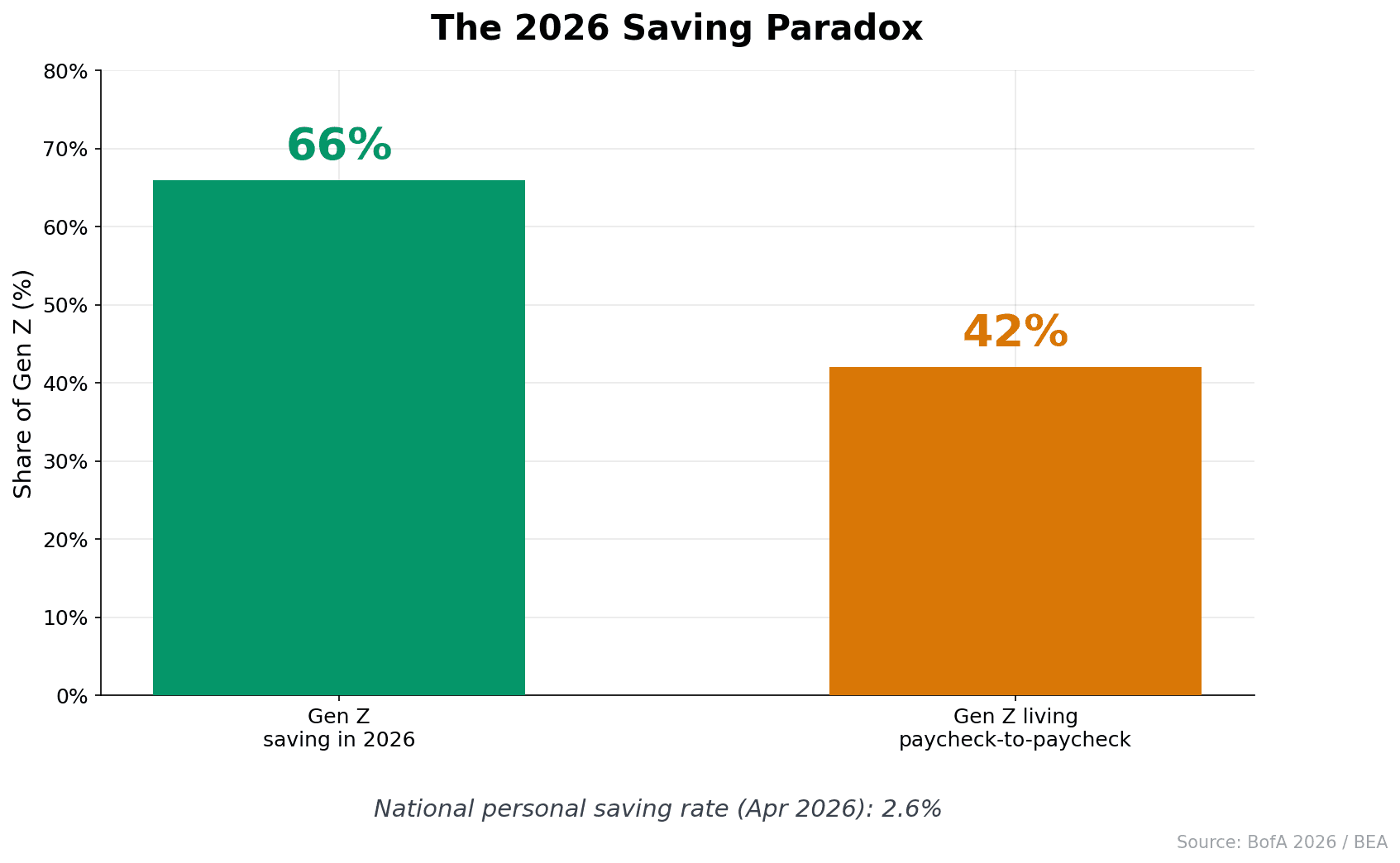

The trend is real and it's measurable. Bank of America's 2026 Better Money Habits study found that 66% of Gen Z (ages 18-29) are now saving — up from 60% in 2024. Even more telling: when asked what they'd do with a surprise extra $300 a month, 54% of Gen Z said they'd put it straight into savings, outpacing Millennials (44%), Gen X (40%) and Boomers (45%).

These aren't people throwing a no-spend party online. They're quietly funneling money away. Among Gen Z, 21% put a set percentage of every paycheck into savings automatically, and 22% contribute to a 401(k) — a 401(k) being your employer-sponsored retirement account that often comes with free matching money.

But here's the paradox that makes this story interesting. While intent to save is climbing, the actual cushion is thin. The U.S. personal saving rate — the share of income people keep instead of spend — was just 2.6% in April 2026. And 59% of Americans can't cover a $1,000 emergency without going into debt, with 54% saying inflation is forcing them to save less.

So why did quiet saving catch fire now? Because people are exhausted. Exhausted by hustle culture, by lifestyle inflation, and by the pressure to perform financial responsibility online. Holly O'Neill, President of Consumer at Bank of America, put it well: "Gen Z knows money stress is real — but they're meeting it head-on." Quiet saving is what meeting it head-on looks like when you've stopped caring about applause.

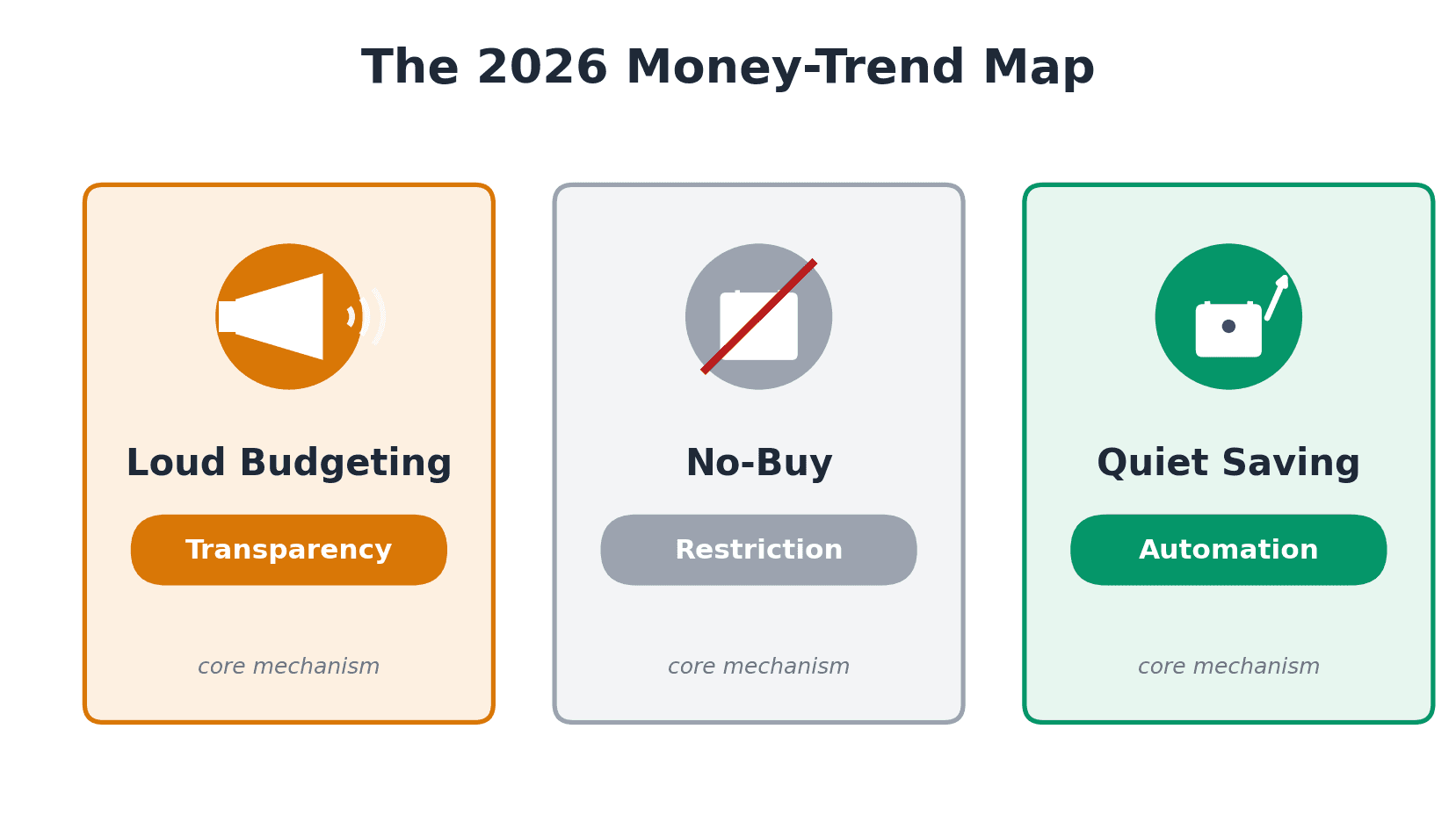

Quiet Saving vs Loud Budgeting vs No-Buy: The 2026 Money-Trend Map

If you've been online at all this year, you've seen three competing money movements. They're often lumped together, but they work in completely different ways. Here's the map I use to explain them.

| Loud Budgeting | No-Buy Challenge | Quiet Saving | |

|---|---|---|---|

| Core mechanism | Transparency / accountability | Restriction / deprivation | Automation / accumulation |

| Visibility | Public | Often public | Private |

| Psychology | Social accountability, anti-shame | Willpower, reset | Defaults, low-friction |

| Best for | Extroverts, social spenders | Resetting bad habits short-term | Most people, long-term |

| Main risk | Performance pressure | Burnout, rebound spending | Hoarding cash, secrecy |

Loud budgeting is the extrovert's tool. You say "I can't afford that" out loud, you tell friends your goals, and the accountability does the work. If that's you, it genuinely works — I've written a full breakdown of the loud budgeting movement and the psychology behind it.

No-buy challenges are the reset button. You ban a category of spending for 30 days to break a habit and see your triggers clearly. They're powerful short-term, but restriction-based plans tend to rebound. My deep dive on running a no-buy challenge without the burnout covers how to avoid the snap-back.

Quiet saving is the introvert's autopilot answer to both. No announcement, no white-knuckle willpower — just defaults working in the background. It's not "better" than the other two. It's a different tool for a different temperament, and for most people, it's the one that actually lasts.

The Psychology: Why Showing Off Is the Enemy of Wealth

Here's the uncomfortable truth at the center of quiet saving: broadcasting your finances — in either direction — can quietly sabotage you.

The classic research on this is The Millionaire Next Door by Thomas Stanley and William Danko. Their finding, decades old and still true: most real millionaires live below their means, drive used cars, and live in ordinary neighborhoods. The people flashing the markers of wealth are frequently, as they put it, "big hat, no cattle." Genuine wealth correlates with under-consumption and invisibility, not display.

Social media supercharged the opposite instinct. Lifestyle inflation used to mean keeping up with your literal neighbors. Now your comparison set is everyone's curated highlight reel, all at once. The result is predictable: 48% of social-media users admit they've impulsively bought something they saw on social media — and 68% of those buyers later regretted at least one of those purchases.

That pressure hits younger savers hardest. 41% of Gen Z report feeling financial guilt at least once a week, and 40% seek validation from family or friends before or after a purchase. If you've ever felt broke while your actual numbers were fine, that's a real and documented phenomenon — I unpack it fully in money dysmorphia: feeling broke when the numbers say otherwise.

Quiet saving cuts the cord. When nobody's watching your spending or your saving, you make decisions for one person: future you. That same logic is why the loudest finance advice is rarely the best — the boring, consistent, quiet stuff wins, which is the whole argument in my piece on why real wealth beats performative FinTok. The mindset shift here is the same one behind minimalism as a wealth accelerator: when your sense of "enough" stops being set by a feed, your savings rate quietly climbs on its own.

I live this one personally. On weekends I wear clothes with holes in them and ride a thirty-year-old bike my dad handed down, and my idea of a great Saturday is sausages over an open fire. I don't want a flashy car or a four-star all-inclusive — some of my best trips have been a cheap ticket and a backpack, where you meet far more interesting people than you ever do at a resort. I'm happy with what I have and the path I chose, and that contentment is what keeps my savings rate high with almost no willpower. (Full disclosure: I'm not perfectly quiet anymore — this article, a podcast, a newspaper. But that's me being loud about the idea, not my net worth. The numbers stay mine.)

The Quiet Saving System: Automate the Boring Middle

This is the part competitors skip. Everyone says "quiet saving is a vibe." Almost nobody gives you the system. Here it is.

The core principle comes straight from behavioral economics: defaults beat willpower, every single time. In the landmark study of one large employer, switching the 401(k) to automatic enrollment lifted participation from around 40% to over 85% — and most people never changed the default. You are not lazy. You are human, and humans follow the path of least resistance. So the trick is to make saving the path of least resistance.

Economists Richard Thaler and Shlomo Benartzi built an entire program around this called Save More Tomorrow. The insight: the thing stopping you from saving isn't math, it's psychology — inertia, present bias, and loss aversion. The fix is structural, not motivational. Here's how to build it.

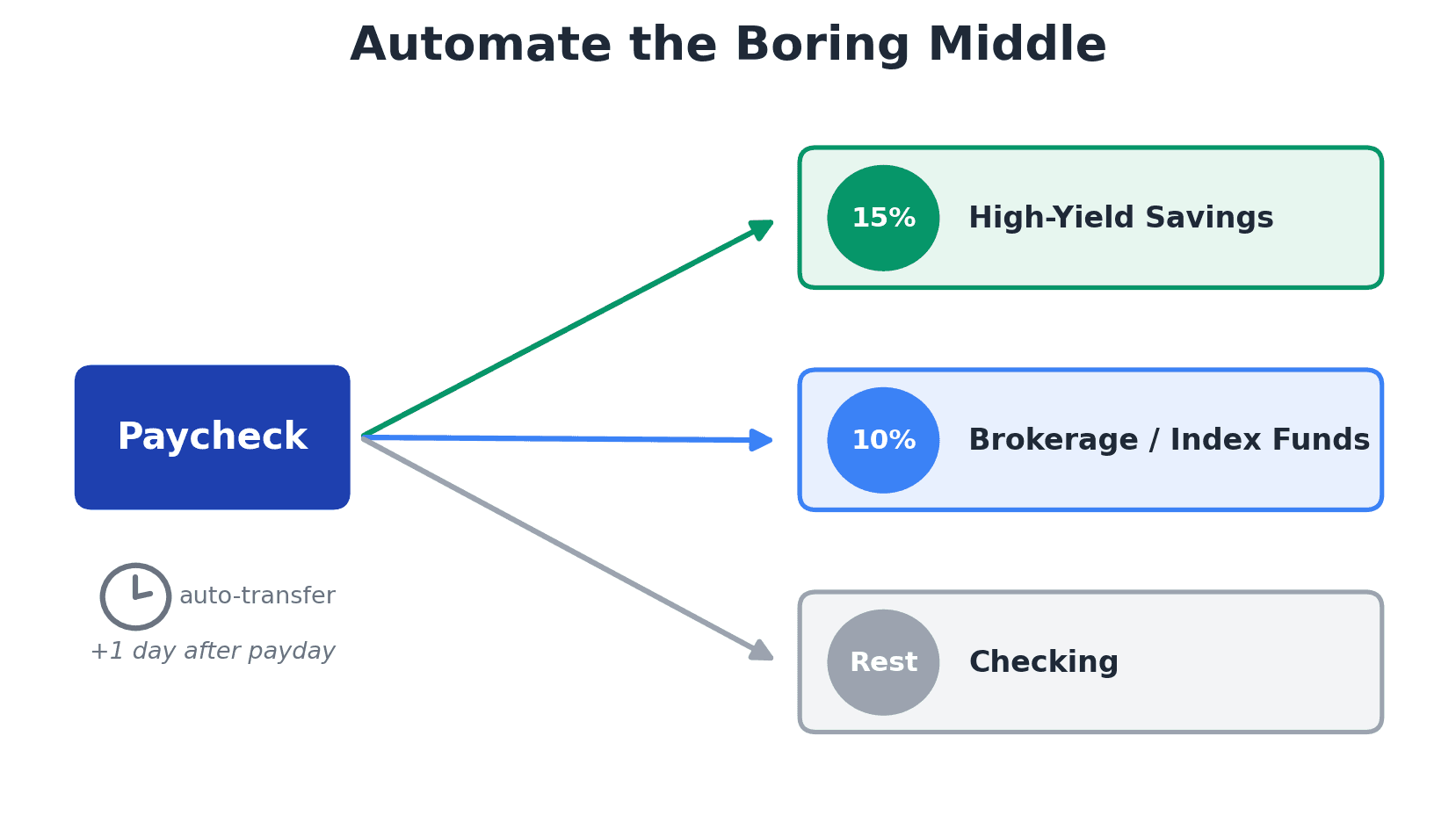

Step 1 — Pay yourself first, at the source. Split your direct deposit before the money ever touches your checking account. Send 10-20% to savings and another slice to a brokerage automatically; the rest goes to checking. If you never see it, you never "decide" to save. Saving becomes the default; spending becomes the leftover.

Step 2 — Automate transfers the day after payday clears. This is a small thing that prevents a big headache. Scheduling auto-transfers a day after deposit avoids accidental overdrafts when timing is tight.

Step 3 — Build the emergency layer first, then invest. Route your automation into a high-yield savings account (HYSA — an online savings account paying meaningfully more interest than a typical bank account, around 4%+ in early 2026) until you have three to six months of essential expenses. Then redirect new automation into low-cost index funds so quiet saving doesn't quietly turn into cash hoarding.

Step 4 — Save your raises. Every time you get a raise, bump your automatic saving rate by one percentage point. You never feel it because you never lived on that money. This is the Save More Tomorrow method, and it's the single most painless way to escalate over time.

The beauty of this system is that it requires zero announcements and almost zero ongoing willpower. You set it once. It runs in the background while you live your life.

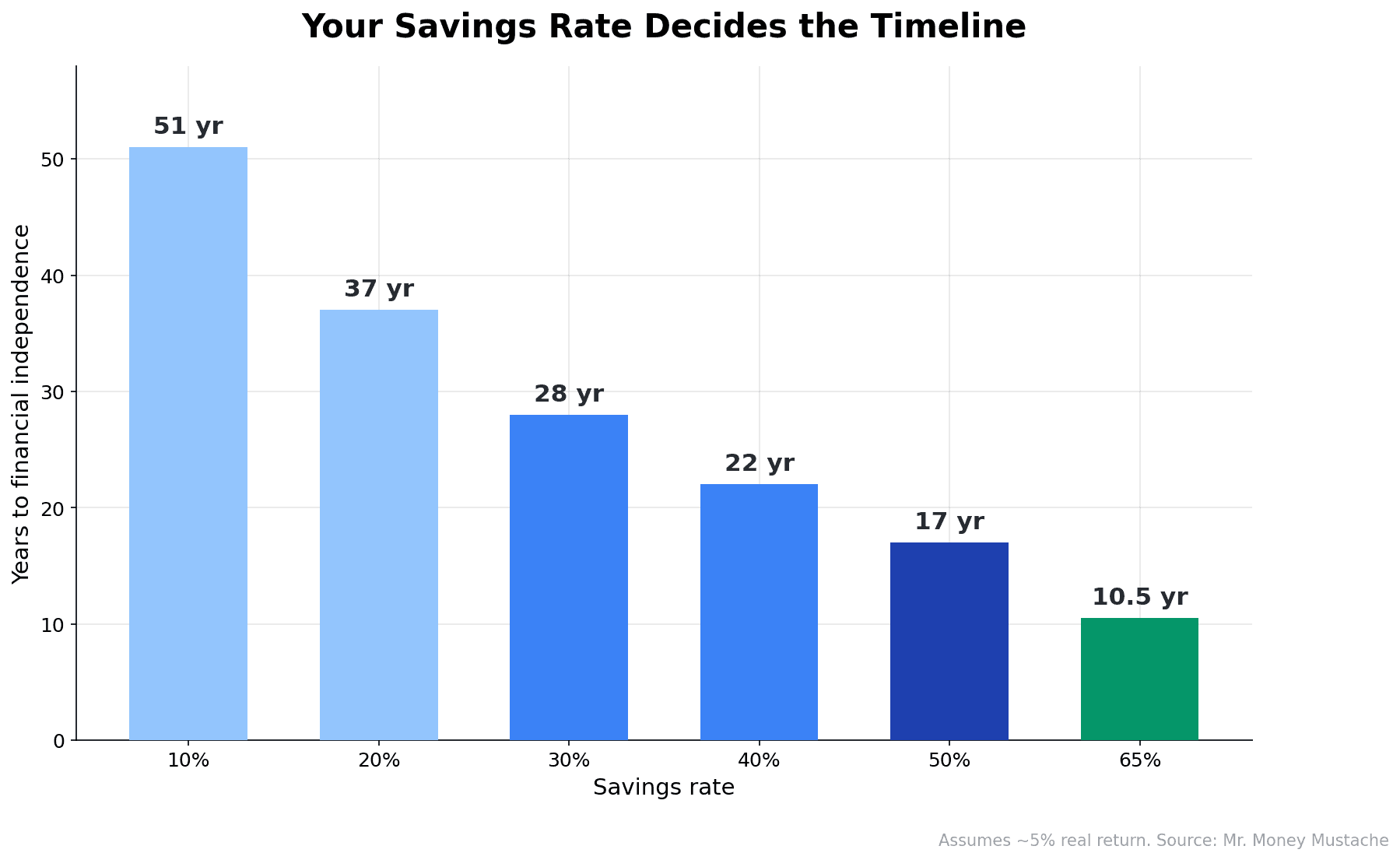

How Much to Quietly Save: A Savings-Rate Framework With Real Math

Once your automation is running, the only dial that really matters is your savings rate — the percentage of your take-home pay you keep. And here's the part that turns quiet saving from a feeling into a plan: your savings rate, far more than your income, decides how soon you reach financial freedom.

The math is famously non-linear, because a higher savings rate does two things at once — it grows your portfolio faster and lowers the lifetime expenses you need to fund. Here's the classic table (assuming a steady ~5% real return):

| Savings rate | Approx. years to financial independence |

|---|---|

| 10% | ~51 years |

| 20% | ~37 years |

| 30% | ~28 years |

| 40% | ~22 years |

| 50% | ~17 years |

| 65% | ~10.5 years |

Look at the jump between 10% and 20%: doubling your rate cuts 14 years off the clock. That's the quiet saver's superpower — every automated percentage point compounds into years of freedom.

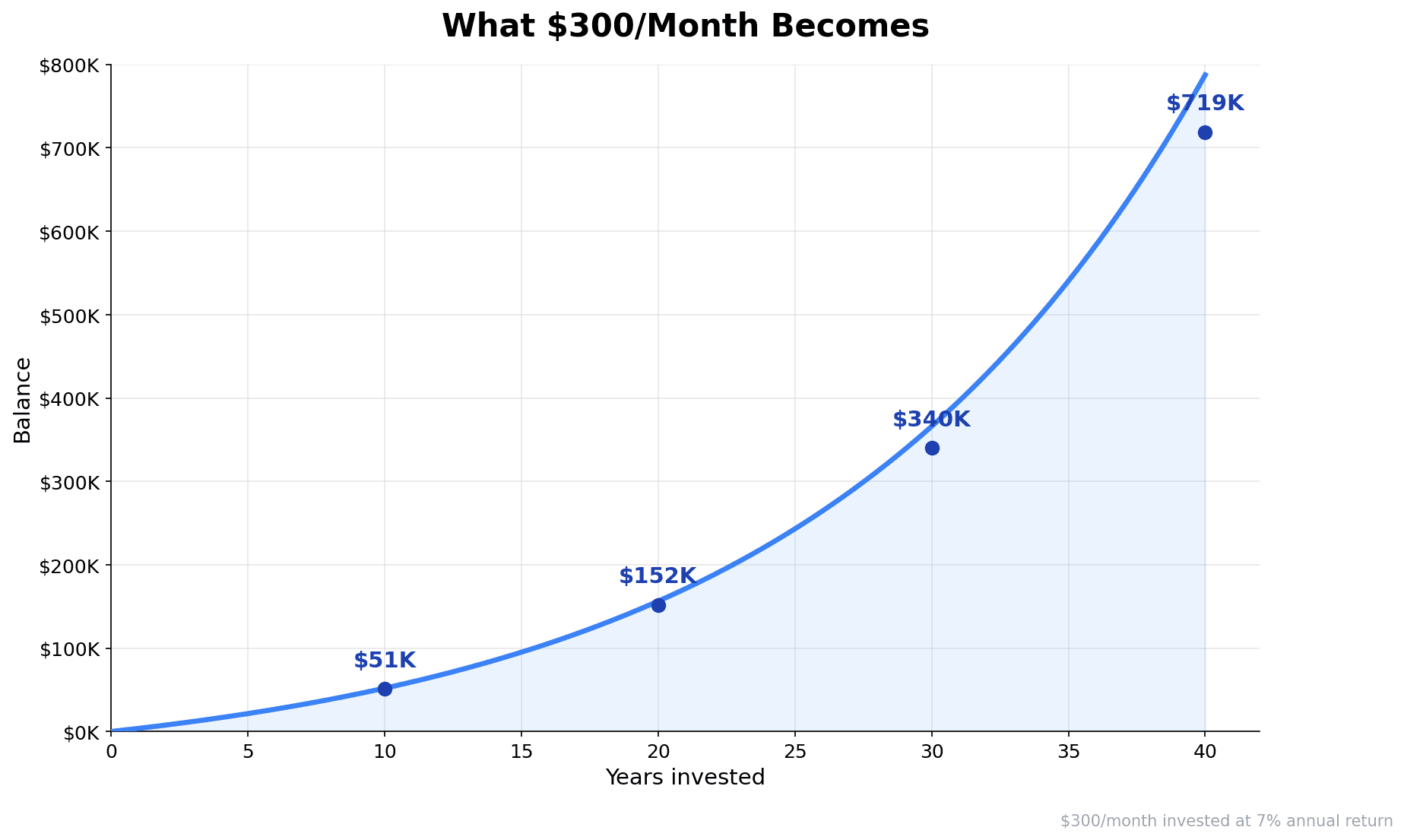

Now make it tangible. Remember the BofA stat that 54% of Gen Z would quietly save a surprise $300/month? Here's what that single habit becomes, invested at a 7% annual return:

| Years | Approx. balance |

|---|---|

| 10 | ~$51,000 |

| 20 | ~$152,000 |

| 30 | ~$340,000 |

| 40 | ~$719,000 |

That's $340,000 from a habit nobody ever knew about. You don't even need to retire decades early to win here. The first milestone for a lot of quiet savers is Coast FIRE — the point where you've saved enough that compounding alone will carry you to retirement without another contribution. I walk through exactly how to calculate that number in my guide to what Coast FIRE actually means. Hit Coast FIRE quietly and the pressure comes off your whole life.

If 20% feels impossible right now, that's fine — and honest. With 42% of Gen Z living paycheck-to-paycheck, "just save 20%" can be tone-deaf. Start at 1%. Automate whatever you can. Then escalate as your income grows. A quiet 1% that you never stop is worth more than a loud 30% that lasts a month.

Track Your Progress Privately (Without Posting It Anywhere)

Here's where quiet saving and most personal-finance tools quietly part ways. The whole point of this trend is privacy — yet the default way to stay motivated has become posting your progress publicly. That's a contradiction.

The fix is a private measurement layer. You measure success by your own number trending up, not by beating anyone's feed. Practically, that means tracking two things every month: your net worth (everything you own minus everything you owe) and your savings rate. That's it. Those two numbers tell you almost everything about whether quiet saving is working.

Before you can track, you need a foundation — a budget that tells you what you're actually working with. If you're starting from zero, my walkthrough on how to start a budget that you'll actually keep is the right first step. A budget isn't the opposite of quiet saving; it's the engine room that makes the automation possible.

This is honestly the problem I built My Financial Freedom Tracker to solve. MFFT is a privacy-first dashboard — you can track your net worth without linking a single bank account, entering numbers manually so nothing ever leaves your control. It's the literal product expression of quiet saving: a place where your number quietly goes up, with no audience, no bank connections, and no feed. You watch the line climb in private, and that's the only validation you need.

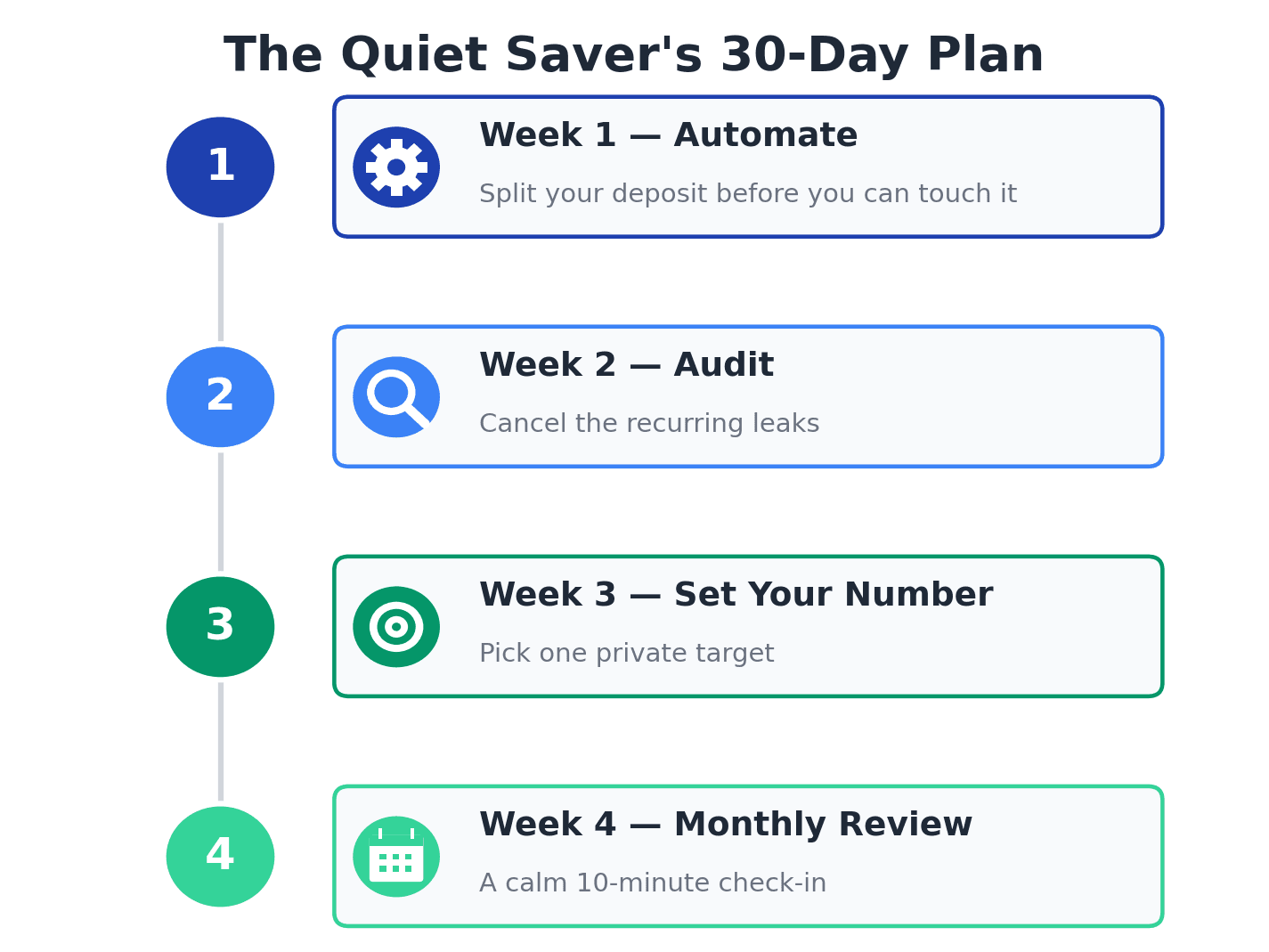

The Quiet Saver's 30-Day Starter Plan

You don't need to overhaul your life. You need four quiet weeks. Here's the plan I'd hand a friend.

Week 1 — Set up the automation. Open a high-yield savings account if you don't have one. Split your direct deposit (or set a recurring auto-transfer the day after payday) so a fixed percentage moves out before you can touch it. Start with a number you genuinely won't notice — even 5%.

Week 2 — Audit the recurring leaks. Spend 30 minutes finding the subscriptions and auto-renewals draining you quietly. Cancel what you forgot you had. Every dollar you stop leaking is a dollar your automation can redirect — no income increase required.

Week 3 — Set your number. Pick one private target: a net-worth figure, a savings rate, or your Coast FIRE number. Write it down somewhere only you see it. This becomes the scoreboard that replaces the social feed.

Week 4 — Build the monthly review ritual. Block 10 minutes once a month. Update your net worth, confirm your automations actually fired, and resist the urge to react to short-term market noise. That's the entire ritual. Quiet saving isn't zero attention — it's calm attention.

Do those four things and the system runs itself. No willpower marathons. No announcements. Just a quietly rising number.

Common Mistakes That Turn Quiet Saving Into Quiet Quitting on Your Goals

Quiet saving is powerful, but it has failure modes. I'd be doing you a disservice if I only sold you the upside. Here are the three traps I see most.

Mistake 1 — Hoarding cash instead of investing. This is the big one. Quietly piling money into a savings account feels productive, but even a high-yield account at around 4% barely outruns inflation over the long haul. Quiet saving has to include investing, or you're just slowly losing purchasing power in private. Once your emergency fund is full, automate the rest into low-cost index funds and let the market do what cash can't.

Mistake 2 — Letting "private" curdle into "secret." There's a bright line here: private from the feed is healthy; hidden from your spouse or partner is financial infidelity. I've watched couples who never really talk about money each drift into their own separate plan — not helping each other, sometimes not even staying together. My wife and I run the opposite: we're completely open about our finances and talk regularly about where we want to be, how we'll get there, and why. The rule is simple — keep your numbers off social media, but be fully transparent at home. If you share finances with someone, my piece on handling money as a couple covers how to keep both partners aligned without losing privacy from the outside world.

Mistake 3 — Going fully on autopilot and never looking. Set-and-forget is the goal, but it has a dark side. An automatic transfer can quietly trigger overdrafts if your timing drifts. A savings rate you set three raises ago is now embarrassingly low. Automation needs a quarterly glance, not constant fiddling — which is exactly what that 10-minute monthly ritual is for.

There's also a competing trend worth naming: soft saving, where some people deliberately prioritize present experiences over aggressive accumulation. That's a legitimate choice, not a failure. Quiet saving isn't a moral demand to deprive yourself — it's permission to build wealth and live, without performing either one.

Conclusion: Let Your Number Do the Talking

The loudest financial flex in 2026 is staying quiet. Quiet saving wins not because it's trendy, but because it removes the two things that wreck most money plans: the willpower tax and the comparison trap.

You automate the boring middle so saving happens before you can overthink it. You let your savings rate — not your income, and definitely not your feed — set your timeline to freedom. And you track the whole thing privately, measuring success by your own rising number instead of anyone's highlight reel.

The coworker in the nine-year-old Civic isn't bad with money. She just figured out that wealth is built in silence and spent in freedom. You can start the exact same system this week: one automatic transfer, one private number, one calm monthly check-in.

Set it up quietly. Tell no one. And let compounding do the bragging for you.

📩 Questions about building your own quiet saving system? Email me at vymerd@gmail.com. And if you want a private place to watch your number climb — no bank linking, no audience — track it with My Financial Freedom Tracker.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyRent vs Buy in 2026: I Ran the Numbers, Kept Renting, and Invested the Difference

My uncle swears renting is throwing money away. So I built the rent vs buy 2026 model: renting wins in all 50 metros, but only if you invest the difference.

Master Your Money

Master Your MoneyWhy Did Your Mortgage Payment Go Up in 2026? The Escrow Shock Behind the 'Fixed-Rate' Myth

My home-insurance bill jumped about 40% in one renewal and caught me $460 short, and I don't even have a mortgage. Millions of Americans got a nastier version in 2026. Here's why your 'fixed-rate' payment isn't fixed, and how to stop the escrow shock ambushing you again.

Master Your Money

Master Your MoneySavings Rate vs Investment Returns: I Spent Years Optimizing the Wrong One

I spent years optimizing investment returns I couldn't control while ignoring the one lever I actually could. Here's the savings rate vs investment returns math that embarrassed me, the honest crossover where returns finally take over, and how to raise your rate without hating your life.

Master Your Money

Master Your MoneyCar Loan Interest Tax Deduction 2026: The Real Math Behind the $10,000 Headline

Everyone's acting like the government now pays your car interest. So I opened a spreadsheet. The car loan interest tax deduction 2026 is real, but on the average new-car loan it's worth about $572 in year one and roughly $1,978 total, not $10,000. Claim it, don't chase it, invest the difference.

Master Your Money

Master Your MoneyThe Cash-Sweep Trap: Why Your Brokerage Might Be Paying You 0.01% on Cash in 2026 (And How to Fix It)

I found dead money in my own accounts: a cash sweep account paying 0.01% sitting right next to a money fund paying hundreds of times more, and I never chose it. Here's the real dollar cost of idle cash in 2026, and the two-minute audit that fixes it.