Sinking Funds: The System That Stops Surprise Bills (2026)

It's the third week of December. Your car insurance auto-renews for the year, the dentist wants $400 for the crown you've been ignoring, and Christmas is, as always, on the 25th. None of it was a surprise — the insurance renews every single year, the tooth has hurt since October, and Santa has kept the same schedule for a while now. Yet all three land in the same two weeks, and there's no pot of money waiting for any of them. So one goes on the card, one raids your emergency fund, and the third quietly ruins your January. This pile-up is exactly the problem sinking funds are built to solve.

Key takeaways (as of June 2026)

- A sinking fund is money you set aside gradually for a known but irregular bill (Christmas, tires, insurance) — so it never lands as a shock.

- It's different from an emergency fund (for the genuine unknown) and a generic savings account (money with no job). Build the emergency layer first.

- The math is one line: (total needed − already saved) ÷ paychecks until due.

- Keep the cash in a high-yield savings account (~4.1–4.2% APY in mid-2026), ideally split into named buckets in one account.

- Start with 3–5 funds, automate the transfer the day after payday, and refill each bucket after you spend it.

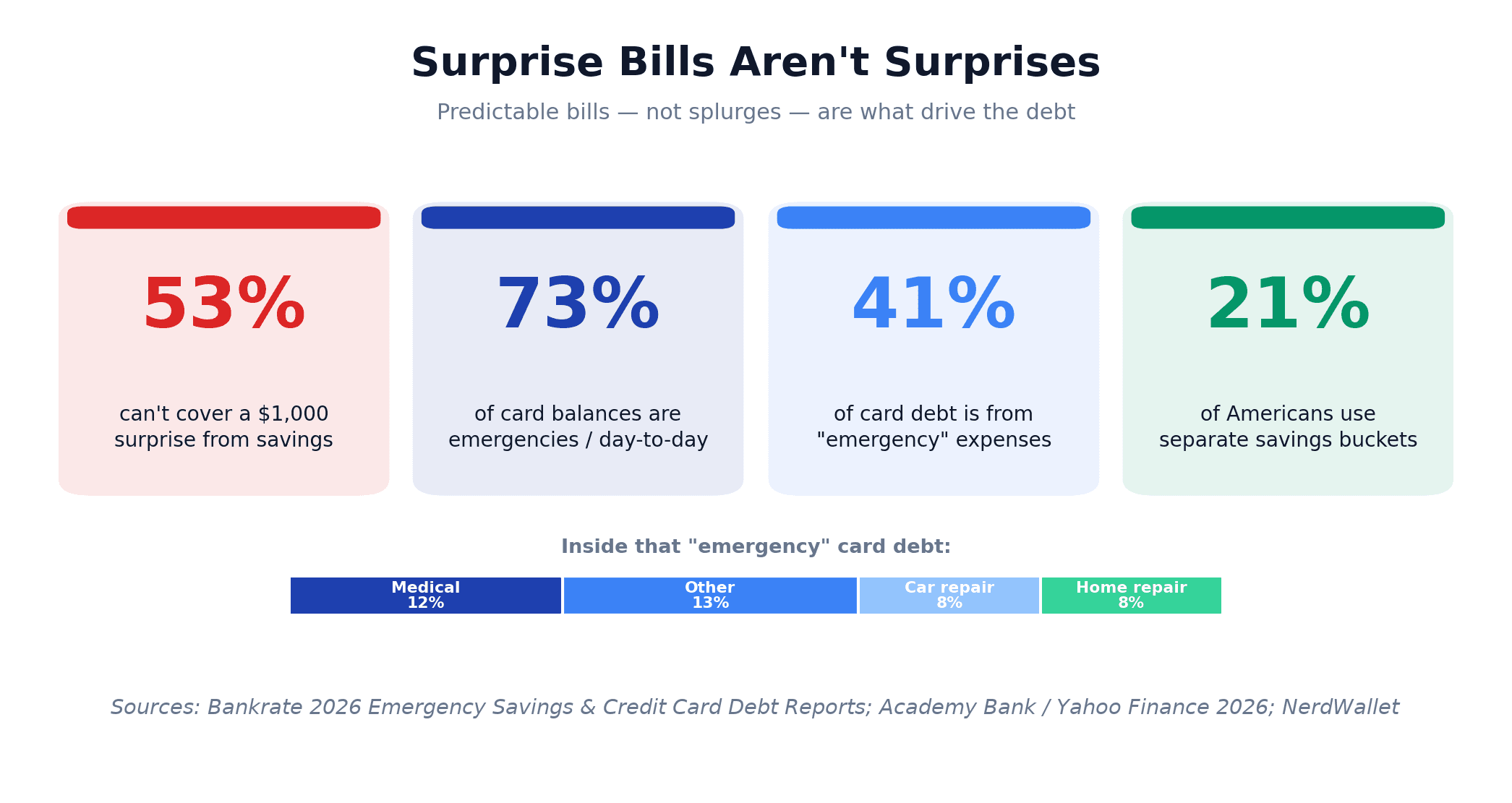

Here's the stat that frames why this matters in 2026: 53% of Americans cannot cover a $1,000 emergency from savings (Bankrate's 2026 Emergency Savings Report), and a third say they'd go straight into debt for it. The cruelest part is that most of those "emergencies" aren't emergencies at all — they're bills you could see coming a year out.

I went years without this layer, and every December I'd act shocked by costs I'd known about since January. What finally changed it for me wasn't an app — it was one weekend where I sat down and went through every recurring expense, line by line: re-shopping insurance, energy, a couple of liabilities, and cutting a meaningful chunk off my monthly outgoings just by paying attention. The leftover lesson was bigger than the savings — most of what wrecks a budget is predictable, and the fix is boring on purpose. A sinking fund is that boring fix: the thing that finally made my budget stop breaking in the same places every year. Let me show you exactly what it is, the 12 categories most people forget, the per-paycheck math to fund each one, and where to keep the money in a falling-rate year.

What Is a Sinking Fund? (And Why Two Money Buckets Aren't Enough)

A sinking fund is a pot of money you build up gradually, on purpose, for a specific expense you know is coming. Instead of treating a $1,200 Christmas as one scary December event, you set aside $100 a month from January and arrive in December with the cash already sitting there. The name is old banking jargon — companies "sink" money into a fund over time to pay off a future debt — but the idea is dead simple: save a little each month for a bill you can see coming.

The reason most people need this is structural. The typical household runs with only two money compartments: a checking account for this month, and (if they're doing well) an emergency fund for disasters. That leaves a gap — and every predictable-but-irregular cost falls straight through it. The car needed tires. The vet wanted $600. The annual membership renewed. Because there's no bucket for those, they get charged to a card or skimmed off the emergency fund, and the budget "fails" in the exact same spots every year.

The data backs this up hard. Among Americans carrying credit-card debt, 41% say that debt comes primarily from emergency or unexpected expenses — car repairs (8%), medical bills (12%), home repairs (8%), and other surprises (Bankrate's 2026 Credit Card Debt Report). Zoom out further and 73% of credit-card balances are tied to emergencies or everyday essentials, not discretionary splurges (Academy Bank survey, via Yahoo Finance, 2026). We're not buying yachts. We're buying tires and crowns on credit because nothing was set aside.

A quick note before we go further: a sinking fund sits on top of a working monthly budget — it's not a replacement for one. If you don't yet have a budget that tells you what's left after the bills, start there first; my 3-method budgeting walkthrough gives you the framework in an afternoon. The sinking layer is what you build once the monthly basics are running.

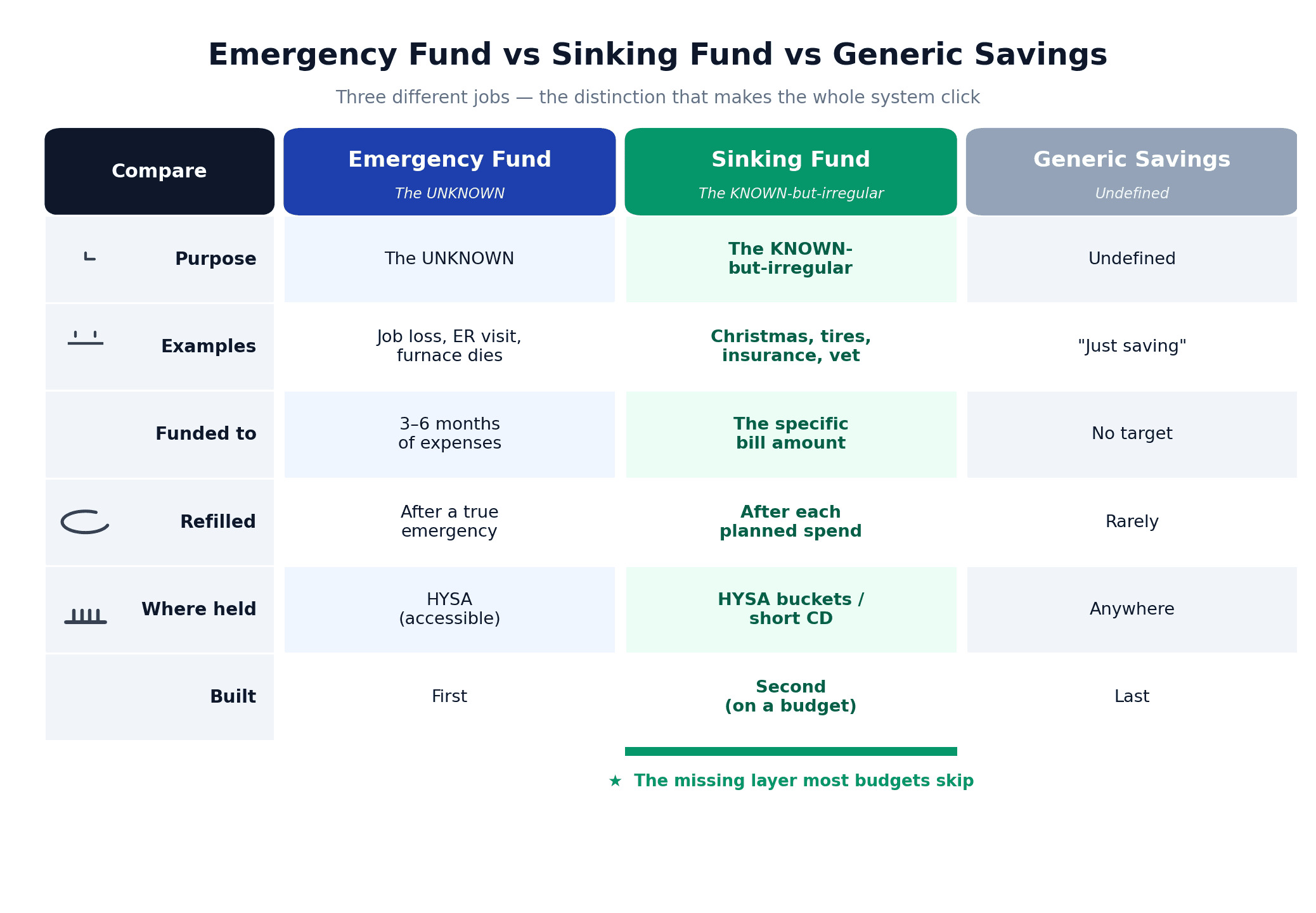

Sinking Fund vs Emergency Fund vs Savings: The Difference That Matters

This is the distinction that makes the whole system click, and it's where most people get tangled. An emergency fund is for the genuinely unknown — a job loss, an ER visit, the furnace dying in February. A sinking fund is for the known but irregular — Christmas, new tires, the insurance renewal, the vet's annual checkup. And a generic savings account is the murky third thing: money with no defined job, which is exactly why it tends to get spent.

Why does the line matter so much? Because when there's no sinking layer, your emergency fund quietly becomes the fund for everything. Every "known" expense you forgot to plan for gets pulled from it, so it's perpetually half-drained and never actually available for a real emergency. That's the structural reason emergency funds get raided — and it's why the planned-spending layer is the missing piece. (For how to size and build that emergency layer in the first place — and it should come first — here's my full guide to the 2026 emergency fund.)

Here's the clean comparison I keep coming back to:

| Emergency Fund | Sinking Fund | Generic Savings | |

|---|---|---|---|

| Purpose | The UNKNOWN | The KNOWN-but-irregular | Undefined |

| Examples | Job loss, ER visit, furnace dies | Christmas, tires, insurance renewal, vet | "Just saving" |

| Funded to | 3–6 months of expenses | The specific bill amount | No target |

| Refilled | After a true emergency | After each planned spend | Rarely |

| Where held | HYSA (accessible) | HYSA buckets / short CD | Anywhere |

| Built | First | Second (on top of a budget) | Last |

The headline behavioral problem: almost nobody actually separates these. Only about 21% of Americans — barely 1 in 5 — keep multiple savings buckets for different goals (NerdWallet). The other four out of five are running everything out of one pile, which is precisely why a predictable bill feels like a crisis.

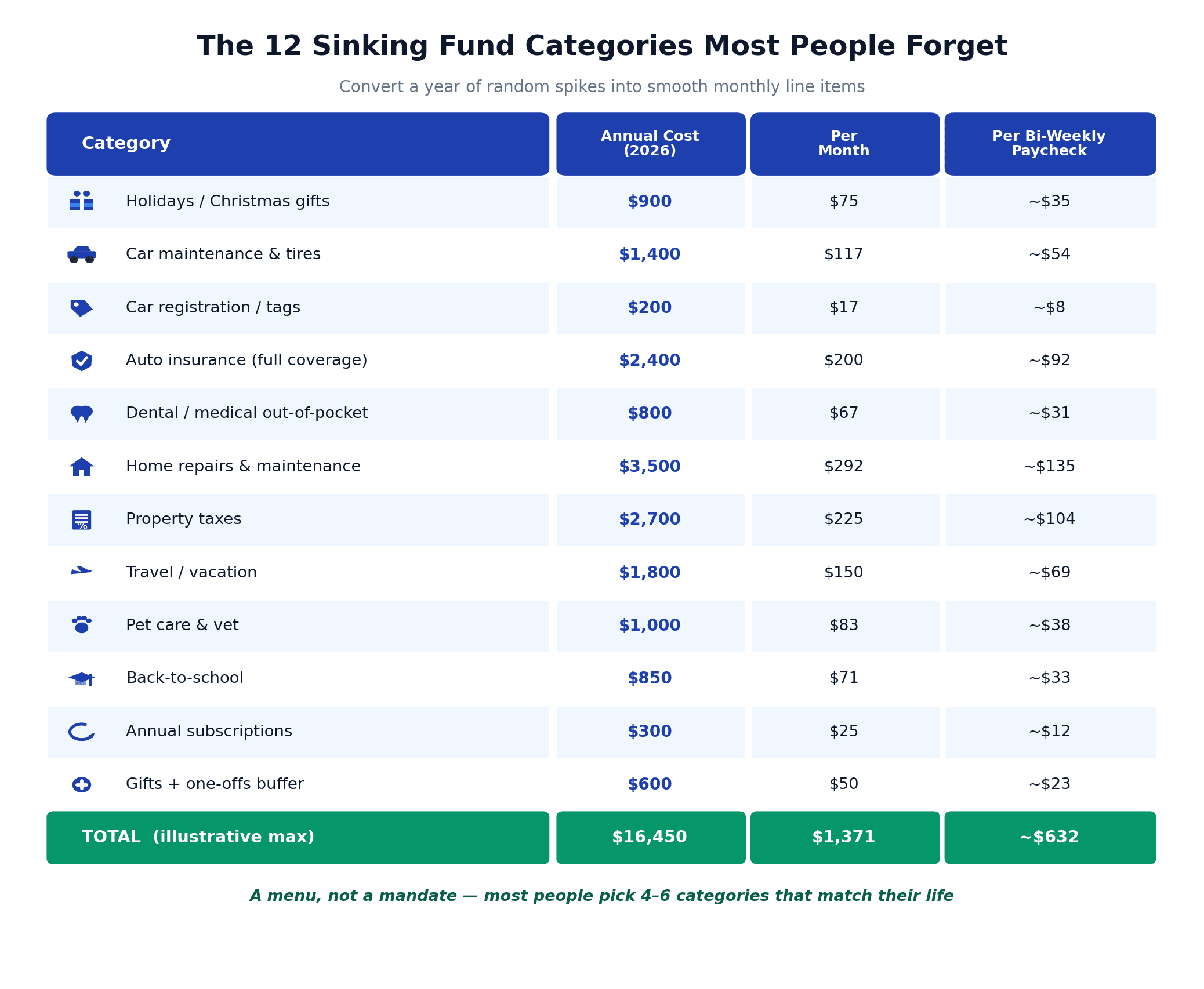

The 12 Sinking Fund Categories Most People Forget

Here's the part you can copy. Below are the twelve categories that ambush budgets most often, each with a realistic 2026 annual cost and what it works out to per month and per bi-weekly paycheck. Treat this as a menu, not a mandate — almost nobody funds all twelve. Most people pick four to six rows that match their life. The point isn't to save more; it's to convert a year of random spikes into smooth monthly lines.

| Category | Typical Annual Cost (2026) | Monthly | Per Bi-Weekly Paycheck |

|---|---|---|---|

| Holidays / Christmas gifts | $900 | $75 | ~$35 |

| Car maintenance & tires | $1,400 | $117 | ~$54 |

| Car registration / tags | $200 | $17 | ~$8 |

| Auto insurance (full coverage) | $2,400 | $200 | ~$92 |

| Dental / medical out-of-pocket | $800 | $67 | ~$31 |

| Home repairs & maintenance | $3,500 | $292 | ~$135 |

| Property taxes | $2,700 | $225 | ~$104 |

| Travel / vacation | $1,800 | $150 | ~$69 |

| Pet care & vet | $1,000 | $83 | ~$38 |

| Back-to-school | $850 | $71 | ~$33 |

| Annual subscriptions | $300 | $25 | ~$12 |

| Gifts + one-offs buffer | $600 | $50 | ~$23 |

| TOTAL (illustrative max) | $16,450 | $1,371 | ~$632 |

A few of these are worth a word. Those 2026 numbers aren't guesses — full-coverage auto insurance now averages about $2,900 a year nationally (Experian), ranging from roughly $1,400 to $4,200 by state, the typical household spends $500–$1,000+ on out-of-pocket dental, pet owners ran an average $2,360 across pets in 2025 (MetLife Pet, up 13% year over year), and the 1% home-maintenance rule puts a $350,000 house at roughly $3,500 a year. Property taxes swing wildly by location — a national median near $2,940 (Census ACS 2024), but anywhere from ~$880 in West Virginia to ~$9,360 in New Jersey — so use your own number there.

One category deserves a flag: annual subscriptions. Before you bucket them, audit them. A startling share of subscription spend is for things people forgot they're paying for, and there's no sense pre-funding a renewal you'd cancel if you noticed it. Run a quick subscription creep audit first — it routinely turns up around $1,600 a year in charges — then sink money only into what survives the cut.

I'm biased on this one. The single most effective money move I ever made wasn't an investment — it was that recurring-charge weekend I mentioned up top — the one where I cancelled things I'd quietly forgotten I paid for. It freed up real money every month before I'd saved a single crown into a bucket. So treat the audit as step zero: there's no point pre-funding a renewal you'd cancel the moment you actually looked at it.

How to Calculate Each Sinking Fund (The Per-Paycheck Math)

The math is the easiest part, and it's one line:

(Total needed − Amount already saved) ÷ Number of paychecks until due = Per-paycheck contribution.

The monthly version is even simpler: Total ÷ months until due.

That's the whole engine. Let me run it through three real people so you can see how it behaves at different speeds.

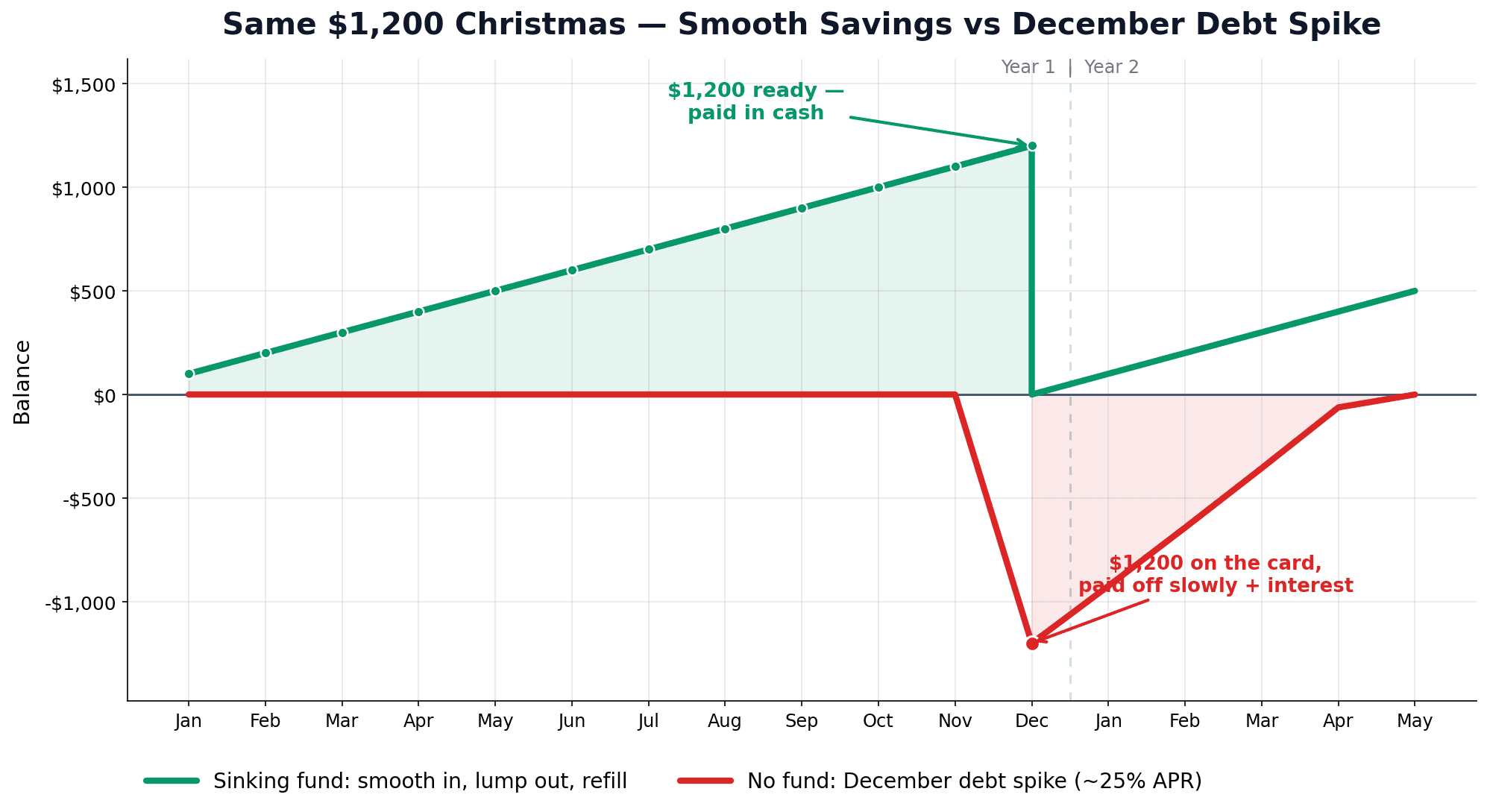

Sarah's Christmas fund — smoothing the spike

Sarah overspent last December, put $1,200 of gifts on a card at ~25% APR, and dragged the balance into March. This year she opens a "Christmas" bucket in January. Target is $1,200, due in 12 months: $1,200 ÷ 12 = $100/month (about $46 per bi-weekly paycheck). When December arrives she pays cash, carries no balance, and skips the ~$60–$150 in interest she ate last year. Same Christmas, same money — just scheduled instead of shocking. This is the fix for the NerdWallet finding that 35% of Americans called their 2025 holiday spending financially irresponsible.

Jake's car bucket — combining the annual and the irregular

Jake stops letting each car cost ambush him separately and bundles them into one "Car" fund: full-coverage insurance ~$1,800/yr, registration ~$200/yr, and a maintenance-and-tires reserve ~$1,200/yr (in the ballpark of AAA's 11¢/mile estimate for maintenance, repair and tires). Total = $3,200/yr, so $3,200 ÷ 12 = **$267/month**. Now when a $700 set of tires shows up in August, it comes out of a bucket that's already full — not his emergency fund, and not a credit card.

Michelle's short runway — why starting early is everything

Michelle's property-tax installment of $900 is due in 5 months and she has $0 saved. $900 ÷ 5 = $180/month. If she'd opened the bucket 10 months out, it'd be $90/month — half the bite. That's the single most important lesson in this whole system: the sooner a bucket exists, the gentler the monthly contribution. The painful funds are always the ones you start late. (Michelle can also pair this with a no-buy challenge to free up that $180 without touching her normal budget.)

The stacking reality: if Sarah eventually ran several buckets at once — Christmas ($100), car ($267), home maintenance ($250), pet ($100), dental ($75), travel ($150) — that's about $942/month of "planned spending." That number looks terrifying until you realize it isn't new spending at all — it's the exact same money those bills always cost her, just paid in smooth installments instead of random shocks. That reframe — same money, scheduled — is the entire reason sinking funds stop the emergency-fund raids and credit-card creep.

Where to Actually Keep Sinking Fund Money in 2026

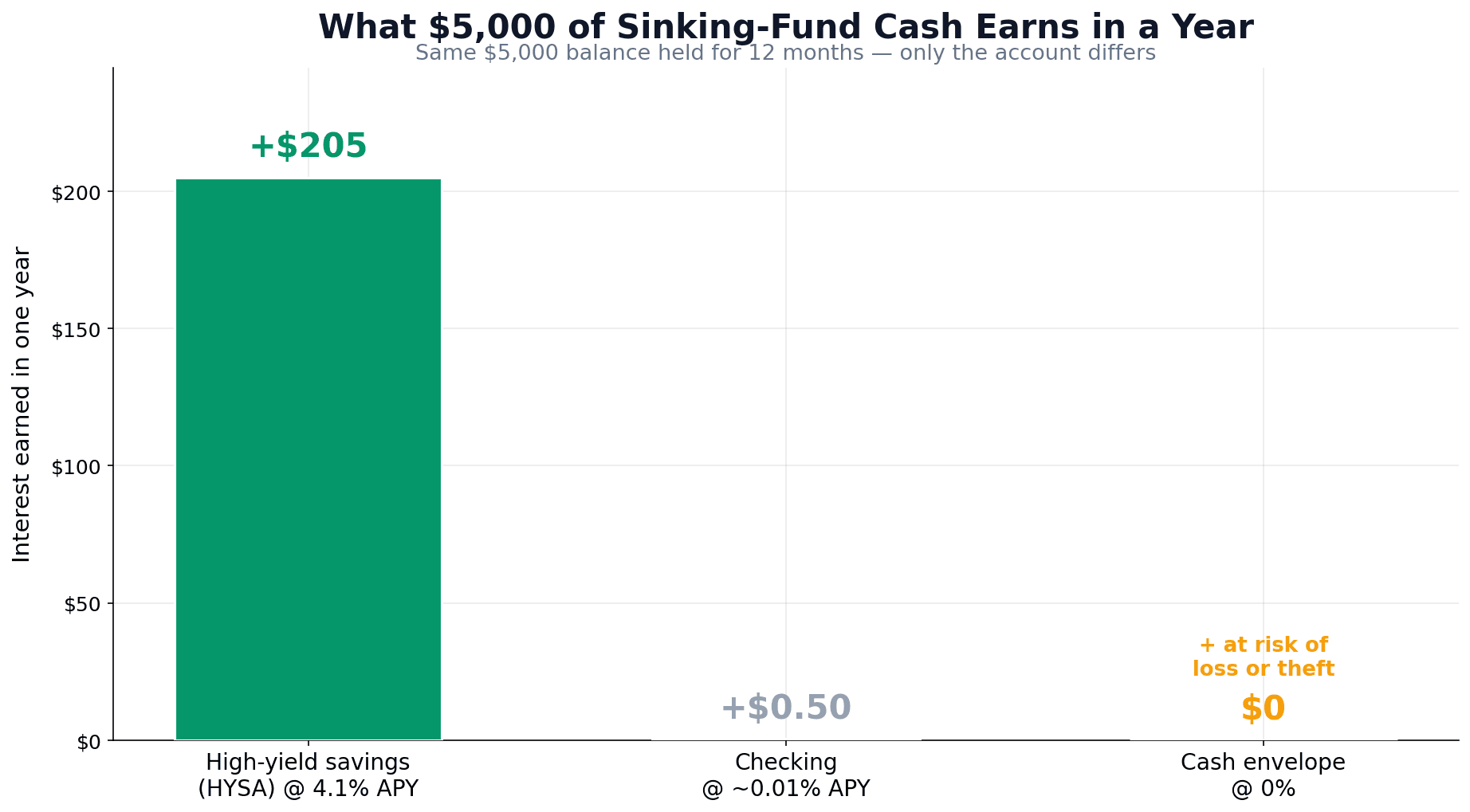

So you've calculated the contributions. Where does the cash live? Not in checking — that's where money goes to get accidentally spent. The home for a sinking fund is a high-yield savings account (HYSA) — an online savings account paying far more interest than a normal bank account. As of June 2026, with the Fed holding its target at 3.50–3.75%, the top HYSAs pay around 4.1–4.2% APY. A HYSA does two jobs at once: it earns ~4% on money that would earn nothing in checking, and it adds friction so you're less tempted to dip in.

The other 2026-friendly move is one account, many buckets. You don't need a dozen separate logins: Ally lets you split a single savings account into up to 30 named "Buckets," and SoFi offers up to 20 "Vaults." One account, one login, but clearly labeled "Christmas," "Car," and "Vet" pots inside it — so the money is mentally pre-spent and you can watch each balance climb.

I'll admit my own bias: I default to simplicity in everything money-related — global ETFs instead of fifty positions, one joint household account instead of a sprawl of logins. So one-account-many-buckets is exactly how I'd run it: a single labeled account I actually check, not a dozen I forget about. Fewer moving parts is a feature, not a compromise.

A caveat for this specific year: the rate outlook is uncertain. Of the accounts that changed APYs in the weeks before this was written, more lowered than raised — but the Fed's June 2026 hold and its slightly hawkish projections mean a clean downward path is no longer the consensus. For short-horizon sinking funds (anything you'll spend within a few months) a flexible HYSA is still the right call. But for long-dated buckets — next year's property taxes, a planned big purchase 12–24 months out — a CD or a short CD ladder can lock in today's yield. Because June's hold and that slightly hawkish dot plot leave the path genuinely two-sided, locking a long-dated bucket is best framed as a hedge against either direction, not a race to beat guaranteed cuts. I walk through exactly how to build one in my CD ladder strategy for 2026; the key idea is that your emergency layer needs to stay liquid, but your longest-dated sinking money can afford to be locked.

The Cash-Stuffing & Underconsumption Connection (Why This Trend Has Legs)

If you've been anywhere near TikTok, you've seen cash-stuffing: people dividing cash into labeled envelopes — "groceries," "gas," "fun" — and spending only what's in each. The hashtag has racked up 3.5 billion-plus views. You've probably also seen underconsumption-core, the quieter trend of deliberately buying less and using what you already own. Here's the thing almost nobody says out loud: cash-stuffing and underconsumption are sinking funds with better branding. Named envelopes are named buckets. The viral version just made the idea visual and tactile.

(It's the same instinct behind the wider loud-budgeting movement — making money habits visible enough that they actually stick.)

That tactile feeling is genuinely valuable — watching real cash leave an envelope creates a small, useful "pain" that a tap-to-pay never does, and it changes spending behavior. But physical envelopes have one real cost in 2026: they earn 0%, and they can be lost or stolen. Park $5,000 in a HYSA at ~4.1% and it earns roughly $205 a year; the same $5,000 in a shoebox earns nothing. So my take is to keep the behavioral win and drop the yield penalty: run the named-bucket system digitally for anything over a few hundred dollars, and reserve real cash envelopes for the small discretionary categories where the psychological friction actually helps.

The deeper reason this trend has legs is that the named-bucket structure is what makes the viral habit survive past week three. A no-spend pledge or a stack of envelopes runs on willpower, and willpower fades. A set of pre-funded, automated buckets runs on defaults, and defaults don't get tired. To channel that underconsumption energy into something that lasts, pair a short no-buy reset with sinking funds: the no-buy frees up cash, and the buckets give it a job before it drifts away.

Common Sinking Fund Mistakes (And How to Avoid Them)

Sinking funds are simple, which is exactly why they're easy to do wrong. Here are the failure modes I see most, and the fix for each.

Building sinking funds before an emergency fund exists. This is the big sequencing error, and I feel it personally. For years I ran a fairly lean 3-to-6-month emergency fund — then I got married, we started a family, and my whole sense of "enough" shifted. We deliberately widened ours to a full twelve months, because once other people depend on you, the cost of being wrong goes up. Sinking funds are worth building, but never at the expense of that base layer: if a real emergency hits and you've funded "Travel" but have no cushion, you're still going into debt. Fund the genuine unknown first, then layer the knowns on top. (I wrote more about how marriage reshaped how we handle money in my own path to financial freedom.)

Too many micro-funds. Fifteen separate pots create decision fatigue and admin you'll abandon by spring. Ramsey's guidance — and it matches what I've seen — is to start with 3 to 5 funds, then add more once the habit is automatic. Consolidate where it's sensible: one "Gifts" fund instead of separate birthday, wedding, and holiday funds.

Leaving the money in checking. Money sitting in your spending account is money that gets spent. Move it to a separate HYSA (or a labeled bucket) where it's both out of sight and earning interest.

Forgetting to refill after you spend. This is the most-skipped step. The moment you drain the "Car" fund on tires, the contribution restarts — the bucket is a cycle, not a one-time event.

Treating every known expense as an "emergency." If you're pulling from the emergency fund for tires and Christmas, you don't have an emergency-fund problem — you have a missing sinking layer. Name the bucket and the "emergency" stops being one.

Your 30-Minute Sinking Fund Setup (Step-by-Step)

You can stand the whole system up in about half an hour. Here's the exact sequence I'd give a friend.

1. Confirm the foundation (5 min). Make sure you have a working monthly budget and at least a starter emergency fund. Sinking funds are layer three, not layer one.

2. List every known irregular expense for the next 12 months (10 min). This is the step that does most of the work. A CFP I trust recommends pulling the last 12 months of bank and credit-card statements and hunting for the lumpy, non-monthly stuff — the insurance renewal, the registration, the vet bill, the holidays. Statements don't lie about what actually hit you.

(If a yearly dig feels like a lot, a recurring weekend money reset keeps the same habit small and regular.)

3. Assign each one a dollar amount and a due date (5 min). Use the category table above as a starting menu, then adjust to your real numbers and your location.

4. Run the formula and pick 3–5 to start (5 min). For each fund: (total − saved) ÷ paychecks until due. Don't launch all twelve — choose the three to five most imminent or most painful, and add more later.

5. Open or label the buckets and automate the transfers (5 min). Set up named buckets in a HYSA and schedule the transfers for the day after payday, so saving happens before you can spend it. Automation beats willpower every time — the contribution that fires automatically is the one that actually happens.

6. Track it, and refill after every spend. This is where the system lives or dies. You need one place to see each bucket's target, its balance, and whether this paycheck's contribution went in.

That last point is the whole reason I built MFFT the way I did — I wanted one private place to track sinking funds, budget categories, and net worth manually, with no bank linking, so the buckets, balances, and refills live together instead of scattered across apps I'd forget to check.

Sinking Fund FAQ

How many sinking funds should I have? Start with 3 to 5 — the most imminent or most painful — then add more once the habit is automatic. More than a dozen tiny pots just create admin you'll abandon by spring.

What's the best account for sinking funds? A high-yield savings account, ideally one that splits into named buckets (Ally offers up to 30 Buckets, SoFi up to 20 Vaults). It earns ~4% in mid-2026 and adds friction so you're less tempted to dip in. For money you won't touch for 12–24 months, a short CD ladder is an option.

Sinking fund vs emergency fund — what's the difference? An emergency fund covers the genuine unknown (job loss, ER visit). A sinking fund covers the known but irregular (Christmas, tires, insurance renewal). Build the emergency layer first, then sinking funds on top.

How do I calculate a monthly sinking fund contribution? (Total needed − amount already saved) ÷ number of paychecks until due. The monthly version is just total ÷ months until due.

Conclusion: Turn Surprise Bills Into Scheduled Ones

The surprises that wreck budgets are rarely surprises. The insurance renews on schedule, the tires wear out on schedule, and Christmas keeps its annual appointment. Sinking funds are simply the layer that lets you see those bills coming and arrive with the cash already set aside — the missing piece between your monthly budget and your emergency fund.

The math is one line, the categories are a menu you can copy, and the home is a high-yield account where ~4% interest and a little useful friction both work in your favor. You don't need fifteen accounts or perfect discipline — just three to five named buckets, an automatic transfer the day after payday, and the habit of refilling each one after you spend it.

Do that, and the December pile-up I opened with simply stops happening — every bill comes out of a pot that was quietly filling all year. Same money, scheduled instead of shocking. That's the entire promise of sinking funds: you stop being ambushed by your own life.

For me this is really the same thing the rest of my writing keeps circling back to: freedom is optionality. You can't control the genuine emergencies, but you can stop the predictable bills from quietly stealing your choices. This is my path, and yours will differ — I deliberately leave the exact numbers out, because "enough" looks different for everyone — but the structure travels.

📩 Want a private place to run your buckets — no bank linking, no audience? Track your sinking funds and net worth with My Financial Freedom Tracker. And if you set up your first sinking fund this week, email me at dennis.vymer@myfinancialfreedomtracker.com and tell me which bill you scheduled away — mine, the first time, was the car insurance renewal that used to wreck every December.

Stay Updated

Get notified when we publish new articles.

Ready to Apply This?

Start tracking your finances today and put these tips into practice.

- Import bank statements in seconds

- AI-powered categorization

- Beautiful visualizations

- Set and track financial goals

Related posts

Master Your Money

Master Your MoneyCash Stuffing, Tested: Does the Viral Envelope Method Actually Build Wealth in 2026?

Cash stuffing and the 100-envelope challenge are everywhere in 2026 — but do they build wealth? The psychology, the hidden cost of idle cash, and a smarter fix.

Master Your Money

Master Your MoneyThe Sunday Money Reset: The 15-Minute Weekly Habit Beating Monthly Budgets in 2026

Weekend budgeting is winning in 2026: a 15-minute Sunday Money Reset that catches overspending weekly — the exact 6-step checklist and the science.

Master Your Money

Master Your MoneyQuiet Saving: How to Build Wealth Without Telling Anyone (The 2026 Anti-Flex Trend)

Quiet saving is the 2026 anti-flex money trend: automate your savings, skip the loud posts, and build wealth privately. Here is the system and the math.

Master Your Money

Master Your MoneyMoney Dysmorphia: Why You Feel Broke When You’re Fine

83% of Americans report money stress while only 16% feel fulfilled (Edward Jones/Gallup, 2026) — often despite healthy numbers. The 5 signs and the fix.

Master Your Money

Master Your MoneyAI Scams Stole $21 Billion: How to Protect Yourself in 2026

AI scams hit a record $20.9B and could reach $40B by 2027. Scammers clone a loved one's voice from 3 seconds of audio. Here's the calm, free, afternoon-long defense playbook to protect your money in 2026.