Start Here

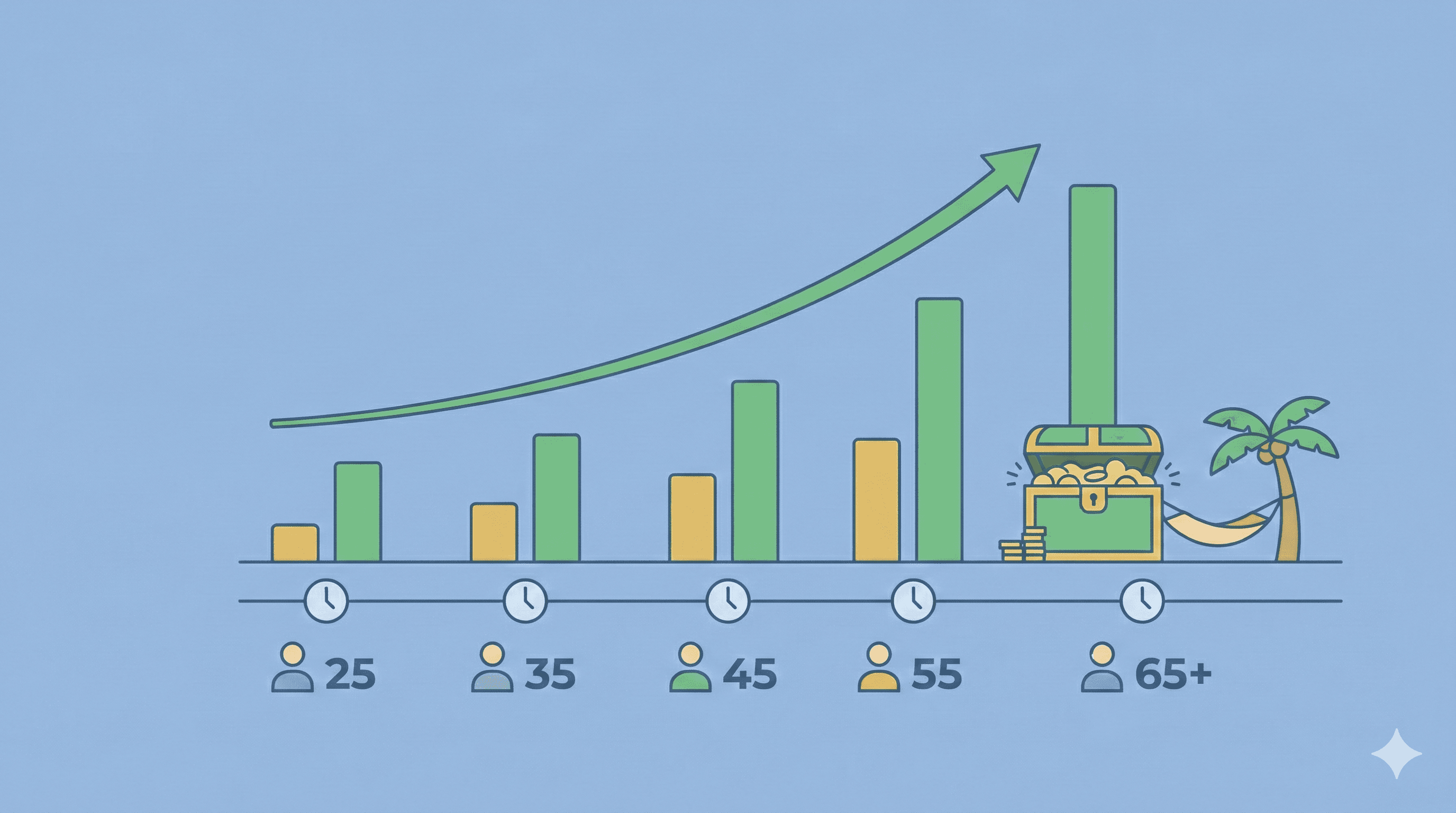

Barista FIRE vs Coast FIRE: Two Paths to Time Freedom

Mar 16, 202619 min read

Barista FIRE vs Coast FIRE: both can cut your FI target 40-60% below 25x expenses. The math, trade-offs, and why 1 in 5 retirees go back to work anyway.

Read More

![My path to Financial Freedom [FIRE]](/_next/image?url=%2Fimages%2Fcovers%2Fdennis_eugene.jpg&w=3840&q=75&dpl=dpl_H7y7kpqnqRcyEBiFtUiguXCA2AfH)